- Medical Devices

- Cell-free Fetal DNA Testing Market

Cell-free Fetal DNA Testing Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Cell-free Fetal DNA Testing Market by Test Type (Non-Invasive Prenatal Testing (NIPT), Chromosomal Abnormality Testing (Trisomy 21, 18, 13), Fetal Gender Determination, Others), End-user (Hospitals & Maternity Clinics, Diagnostic Laboratories, Specialty Prenatal Clinics), and Regional Analysis, 2026 - 2033

Cell-free Fetal DNA Testing Market Size and Trend Analysis

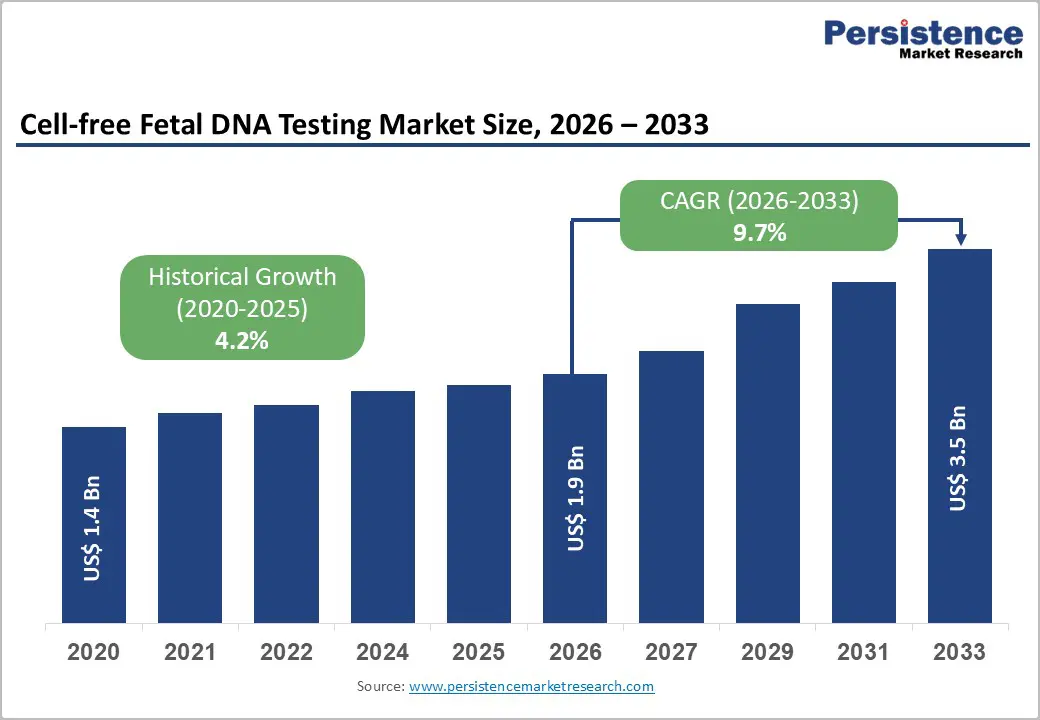

The global cell-free fetal DNA testing market size is expected to be valued at US$ 1.9 billion in 2026 and projected to reach US$ 3.5 billion by 2033, growing at a CAGR of 9.7% between 2026 and 2033.

The market is experiencing accelerating growth driven by three convergent factors: the worldwide trend toward advanced maternal age pregnancies, particularly in developed nations where women aged 35 years and older represent a substantially larger proportion of pregnancies, requiring reliable chromosomal abnormality screening; the demonstrated superior clinical performance of NIPT compared to traditional maternal serum screening, with detection rates exceeding 98% for trisomy 21, 96% for trisomy 18, and 100% for trisomy 13; and expanding insurance coverage and reimbursement pathways across North America and Europe, making cell-free fetal DNA testing increasingly accessible to broader populations regardless of baseline risk profiles.

Key Industry Highlights:

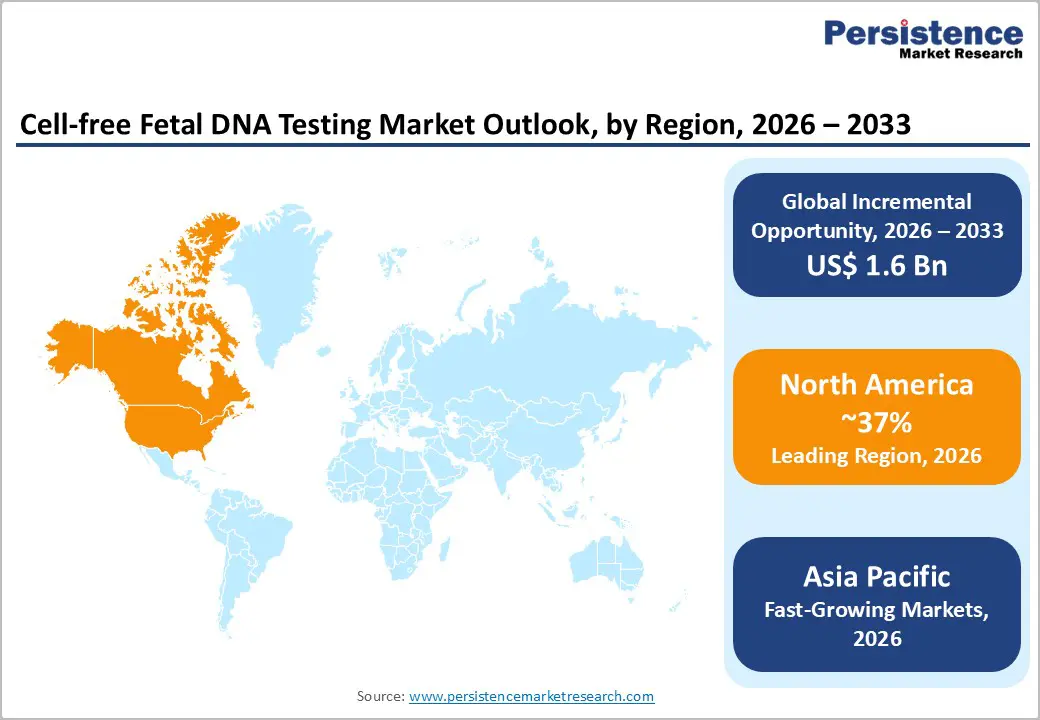

- Leading Region: North America dominates with 37% market share in 2025, supported by FDA regulatory clarity, widespread insurance coverage from major payers, biotechnology company concentration driving innovation, and telehealth integration extending prenatal care access to rural and underserved populations.

- Fastest Growing Region: Asia-Pacific represents the fastest-expanding market driven by China’s National Health Commission support for NIPT as birth defect prevention strategy, large population base, rapidly increasing maternal age trends, and companies like BGI Genomics developing cost-accessible solutions enabling widespread adoption.

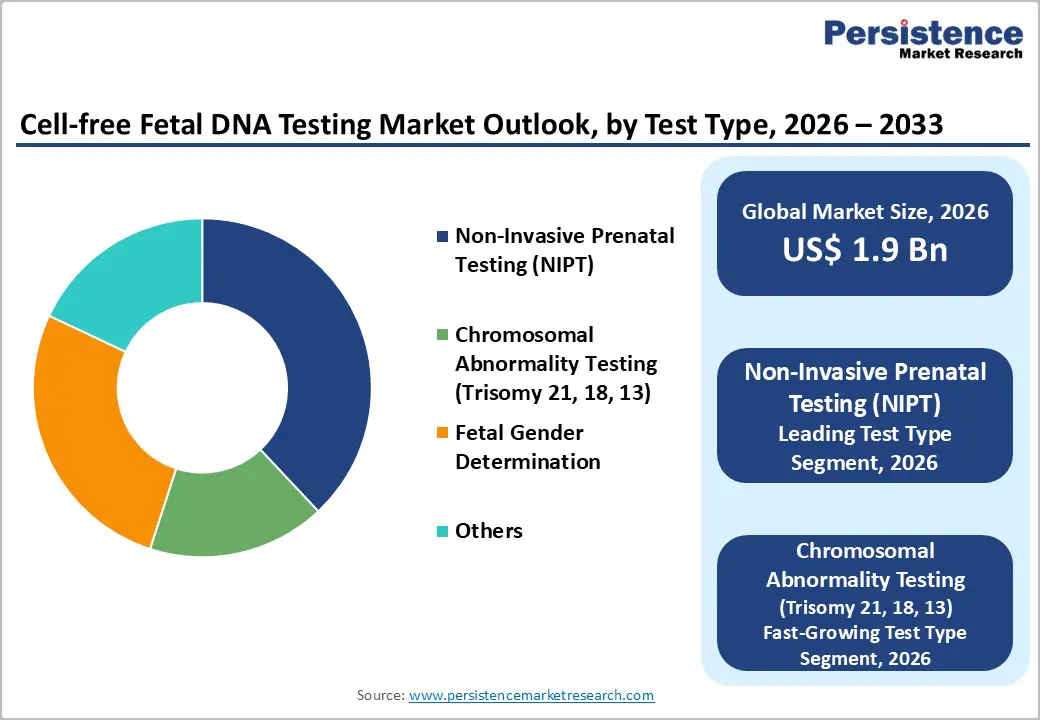

- Dominant Test Type: Non-Invasive Prenatal Testing (NIPT) controls approximately 38% of the cell-free fetal DNA testing market in 2025, justified by superior clinical performance with detection rates exceeding 98% for trisomy 21, accessibility from 9 weeks gestation, and endorsement by all major professional organizations, including ACOG, ACMG, ISPD, and SMFM.

- Fastest Growing Test Type: Chromosomal Abnormality Testing (Trisomy 21, 18, 13) demonstrates the fastest growth trajectory across the forecast period, driven by technological advances enabling improved detection accuracy, expansion into specialty prenatal clinics focused on comprehensive genetic risk assessment, and integration of artificial intelligence for result interpretation.

- Key Opportunity: Expanded genetic screening beyond traditional aneuploidies represents an exceptional market opportunity, with companies implementing comprehensive genetic condition detection, including microdeletions, single-gene disorders, and carrier status assessment, supported by professional organization guidance and increasing consumer demand for actionable prenatal health information.

| Key Insights | Details |

|---|---|

| Cell-free Fetal DNA Testing Market Size (2026E) | US$ 1.9 billion |

| Market Value Forecast (2033F) | US$ 3.5 billion |

| Projected Growth CAGR(2026 - 2033) | 9.7% |

| Historical Market Growth (2020 - 2025) | 4.2% |

Market Dynamics

Drivers - Rising Prevalence of Advanced Maternal Age and Chromosomal Abnormality Risk

Advanced maternal age represents a critical market driver as women increasingly delay childbearing due to professional, economic, and lifestyle considerations. Women aged 35 years and older at estimated date of delivery face substantially elevated risks of chromosomal abnormalities: approximately 1 in 350 pregnancies at age 35, escalating to 1 in 100 pregnancies at age 40, and 1 in 30 pregnancies at age 45. This demographic shift is particularly pronounced in developed countries, including the United States, United Kingdom, Germany, France, and Australia, where maternal age at first pregnancy now averages between 28 and 32 years. The accessibility of cell-free fetal DNA testing beginning at 9 weeks of gestation has fundamentally transformed prenatal screening paradigms, enabling early detection of trisomy 21 (Down syndrome), trisomy 18 (Edwards syndrome), and trisomy 13 (Patau syndrome) without invasive procedures carrying miscarriage risks of 0.1% to 0.3%.

Superior Diagnostic Performance and Regulatory Endorsements

Superior diagnostic performance is a key driver accelerating the adoption of cell-free fetal DNA (cfDNA) testing in prenatal care. cfDNA tests offer high sensitivity and specificity for detecting common chromosomal abnormalities such as trisomy 21, 18, and 13, significantly outperforming conventional serum screening methods. The non-invasive nature of these tests, requiring only a maternal blood sample, reduces the risk associated with invasive procedures like amniocentesis, thereby improving patient acceptance and physician confidence. Additionally, advances in next-generation sequencing and bioinformatics have enhanced test accuracy even at early gestational stages. Strong regulatory endorsement and clinical guideline support further reinforce market growth. Health authorities and professional bodies in several countries increasingly recommend cfDNA testing as a first-line or contingent screening option for high-risk pregnancies, and in some cases for the general obstetric population. Such endorsements drive wider reimbursement coverage, standardization of testing protocols, and integration of cfDNA testing into routine prenatal screening pathways, supporting sustained market expansion.

Restraints - Ethical Concerns and Psychological Sequelae Associated with Expanded Testing Panels

Despite its clinical promise, the expansion of cell-free fetal DNA (cfDNA) testing panels introduces ethical dilemmas and potential psychological burdens that may restrain market growth. Comprehensive panels capable of detecting microdeletions, rare genetic disorders, or predispositions can create complex decision-making scenarios for expectant parents, often before clinical symptoms manifest. The abundance of information may lead to anxiety, stress, or decisional conflict, particularly when results are ambiguous or of uncertain significance. Additionally, ethical questions around privacy, potential discrimination, and selective pregnancy termination can generate societal debate, influencing physician recommendations and regulatory scrutiny. Concerns over informed consent and appropriate genetic counseling further complicate adoption, as healthcare providers must ensure patients fully understand the implications of expanded testing. These psychological and ethical considerations act as a moderating force on the rapid uptake of advanced cfDNA panels, despite their diagnostic benefits.

Opportunity -Integration of Artificial Intelligence and Expanded Genetic Screening Capabilities

Artificial intelligence-powered analysis of cell-free fetal DNA represents an exceptional growth opportunity, with multiple companies implementing machine learning algorithms to enhance result interpretation, reduce false-positive and false-negative findings, and expand detection capabilities for rare genetic conditions. Illumina partnered with Tempus AI in April 2025 to integrate artificial intelligence across cfDNA disease applications, accelerating interpretive accuracy and enabling the detection of previously difficult-to-identify variants at single-base-pair resolution. BillionToOne introduced expanded UNITY Fetal Risk Screen panels in May 2025, covering 14 genes, including five ACOG-recommended recessive conditions plus nine additional actionable conditions, extending screening scope beyond traditional chromosomal aneuploidies. These technological advancements position providers to offer comprehensive, risk-informed prenatal assessment from a single maternal blood sample, creating compelling value propositions that justify expanded reimbursement and increased market adoption across diverse geographic markets.

Expansion of Cell-Free Fetal DNA Testing into Specialty Prenatal Clinics and Direct-to-Consumer Pathways

Specialty prenatal clinics and telehealth-enabled genetic counseling represent rapidly growing market segments driven by increasing patient demand for accessible, early genetic information. Yourgene Health launched IONA Care + non-invasive prenatal screening service in the United Kingdom in February 2025, demonstrating the commercial viability of direct-to-consumer and clinic-integrated NIPT delivery models. This segment’s growth is propelled by advancing next-generation sequencing technology costs declining by approximately 40-50% annually, combined with shifting healthcare delivery toward decentralized testing and remote genetic counseling via telehealth platforms. Rising consumer awareness of genetic disorders, coupled with normalization of genetic testing across prenatal care, creates substantial opportunities for specialized facilities to differentiate through comprehensive genetic counseling, rapid turnaround times, and integrated care coordination supporting informed reproductive decision-making.

Category-wise Analysis

Test Type Insights

Non-Invasive Prenatal Testing (NIPT) dominates the cell-free fetal DNA testing market segment with approximately 38% market share in 2025. This leadership position reflects NIPT’s foundational role as the primary screening methodology for common chromosomal aneuploidies and its clinical validation through extensive prospective and retrospective cohort studies. NIPT leverages next-generation sequencing (NGS) technology and single-nucleotide polymorphism (SNP) analysis to quantify fetal chromosome representation in maternal circulation with exceptional precision. Clinical validations encompassing nearly two million pregnancies consistently demonstrate detection rates exceeding 98% for trisomy 21. The technology’s accessibility from 9 weeks of gestation, with turnaround times of 5-7 days, positions NIPT as the preferred initial screening approach across diverse healthcare settings. Professional organizations, including ACOG, ACMG, ISPD, and SMFM, collectively recommend NIPT as superior to conventional screening methodologies, establishing it as the benchmark screening approach globally. Major diagnostic providers, including Illumina with its VeriSeq NIPT solution, Natera with Panorama testing, Roche, and BGI Genomics with NIFTY testing, continuously optimize NIPT platforms through enhanced chemistry, expanded analytical capabilities, and improved result reporting mechanisms.

End-user Insights

Hospitals & Maternity Clinics constitute the leading end-user category for cell-free fetal DNA testing, representing approximately 52% market revenue in 2025. This dominance reflects the institutional infrastructure hospitals maintain for specimen collection, processing, and result reporting integrated into comprehensive prenatal care pathways. Hospitals benefit from direct collaborations with diagnostic kit suppliers and testing service providers, facilitating cost-effective implementation of standardized cfDNA protocols. Physician referral patterns favor hospital-based testing due to comprehensive maternal-fetal care program integration, established reimbursement arrangements with insurance entities, and institutional accreditation validating testing quality. The hospital setting’s ability to coordinate specimen collection, genetic counseling, and result interpretation within established care episodes supports clinical efficiency. Diagnostic laboratories represent the second-largest end-user segment, providing specialized cfDNA testing services to referring physicians and community healthcare providers. Specialty prenatal clinics represent the fastest-growing end-user category, driven by increasing demand for dedicated genetic counseling, expanded testing panels beyond standard chromosomal screening, and personalized risk assessment approaches. These specialized facilities differentiate through expertise in genetic conditions, comprehensive counseling, carrier screening integration, and follow-up diagnostic testing coordination.

Regional Insights

North America Cell-free Fetal DNA Testing Market Trends and Insights

North America maintains dominant regional position with approximately 37% market share in 2025, underpinned by advanced healthcare infrastructure, FDA regulatory clarity, and broad insurance coverage. The United States leads this region through multiple factors: the FDA has cleared numerous NIPT platforms including Illumina’s VeriSeq, Natera’s Panorama, and others, establishing regulatory precedent supporting widespread clinical adoption; insurance reimbursement from major payers including United Healthcare, Aetna, Cigna, and Anthem covers NIPT under high-risk criteria, with many now extending coverage to general-risk populations; and the concentration of biotechnology companies including Illumina, Thermo Fisher Scientific, Natera, Laboratory Corporation of America (LabCorp), and Quest Diagnostics drives continuous innovation and market penetration.

The North American market demonstrates accelerating adoption of expanded NIPT panels screening beyond traditional trisomies to include microdeletions, with 22q11.2 deletion (DiGeorge syndrome) receiving ACMG conditional recommendation for all pregnancies. Telehealth-linked genetic counseling enhances NIPT access in rural and underserved areas, expanding market reach. Healthcare systems increasingly incorporate risk stratification models leveraging cfDNA testing results to reduce invasive diagnostic procedures, supporting adoption across diverse institutional settings.

Asia Pacific Cell-free Fetal DNA Testing Market Trends and Insights

Asia Pacific is emerging as a dynamic market for cell-free fetal DNA (cfDNA) testing, driven by rising awareness of prenatal health and increasing maternal age in urban populations. Growing investments in advanced healthcare infrastructure, expanding molecular diagnostic laboratories, and the adoption of next-generation sequencing technologies are facilitating broader access to non-invasive prenatal testing (NIPT). Countries like China, India, and Japan are witnessing rapid uptake due to increasing high-risk pregnancies and government initiatives promoting maternal and child health. Moreover, expanding reimbursement frameworks and collaborations between local diagnostic providers and global cfDNA test developers are enhancing affordability and availability. Rising awareness campaigns by healthcare professionals and digital platforms are educating patients about the safety and accuracy of cfDNA testing, positioning the Asia Pacific as one of the fastest-growing regions in the global prenatal diagnostics landscape.

Competitive Landscape

The competitive landscape of the cell-free fetal DNA testing market is characterized by intense innovation, strategic partnerships, and differentiation through technological advancements. Key players compete on test accuracy, breadth of detectable conditions, and turnaround time to gain clinical preference and payer support. Investments in research and development drive the introduction of expanded panels and streamlined workflows, strengthening market positioning.

Key Developments:

- In May 2025, BillionToOne, Inc., launched an expanded offering for providers using the UNITY Fetal Risk™ Screen. The expanded offering screened for five recessive, severe, and actionable conditions recommended by the American College of Obstetricians and Gynecologists (ACOG) for screening in every pregnancy, along with nine additional actionable conditions commonly identified in Ashkenazi Jewish and pan-ethnic populations.

Companies Covered in Cell-free Fetal DNA Testing Market

- Illumina, Inc.

- Natera, Inc.

- F. Hoffmann-La Roche Ltd.

- Laboratory Corporation of America Holdings (LabCorp)

- Quest Diagnostics Incorporated

- Qiagen N.V.

- BillionToOne, Inc.

- Eurofins Scientific

- BGI Genomics Co., Ltd.

- Myriad Genetics, Inc.

- Fulgent Genetics

- Prenetics Group Limited

- Others

Frequently Asked Questions

The global cell-free fetal DNA testing market is expected to reach US$ 1.9 billion in 2026, with sustained growth toward US$ 3.5 billion by 2033 at a compound annual growth rate of 9.7%, driven by rising advanced maternal age pregnancies and expanding insurance coverage.

The cell-free fetal DNA testing market is propelled by two fundamental drivers: the worldwide trend toward advanced maternal age pregnancies where women 35 years and older face substantially elevated chromosomal abnormality risks; and the superior clinical performance of NIPT demonstrating detection rates exceeding 98% for trisomy 21, 96% for trisomy 18, and 100% for trisomy 13 with professional guideline endorsement from ACOG, ACMG, ISPD, and SMFM.

North America maintains the dominant regional position with 37% market share in 2025, supported by FDA regulatory clarity, widespread insurance reimbursement from major payers, concentration of biotechnology innovation companies, and telehealth-enabled genetic counseling extending prenatal care access nationally.

Expanded genetic screening capabilities beyond traditional chromosomal abnormalities represent exceptional market opportunity, with companies implementing comprehensive detection of microdeletions, single-gene disorders, and recessive genetic conditions.

Key market leaders include Illumina, Inc. with comprehensive VeriSeq NIPT platforms, Natera, Inc. processing over 840,000 tests quarterly with SNP-based Panorama technology, F. Hoffmann-La Roche Ltd. with integrated diagnostic solutions, Laboratory Corporation of America (LabCorp) and Quest Diagnostics leveraging extensive laboratory networks.