- Biotechnology

- Plasmid DNA Manufacturing Market

Plasmid DNA Manufacturing Market Size, Share, and Growth Forecast, 2026 – 2033

Plasmid DNA Manufacturing Market by Grade (R&D Grade, GMP Grade), Disease (Infectious Disease, Cancer, Genetic Disorder, Others), Application (DNA Vaccines, Cell & Gene Therapy, Immunotherapy, Others), and Regional Analysis 2026 – 2033

Plasmid DNA Manufacturing Market Size and Trends Analysis

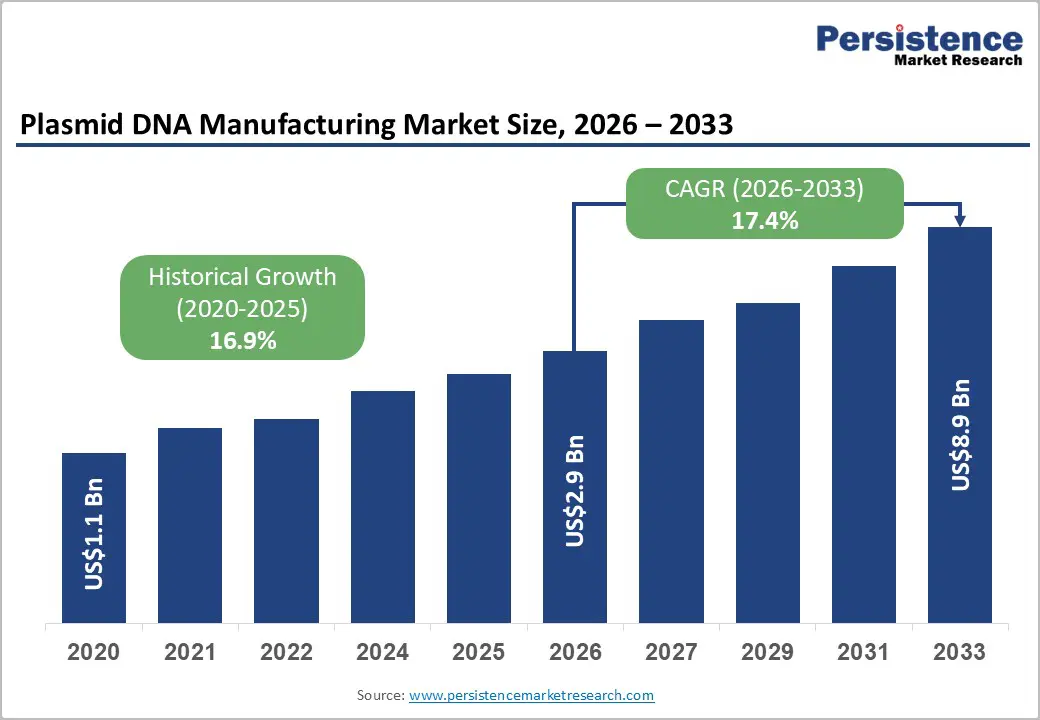

The global plasmid DNA manufacturing market size is likely to be valued at US$2.9 billion in 2026 and is expected to reach US$8.9 billion by 2033, growing at a CAGR of 17.4% during the forecast period from 2026 to 2033. Escalating demand for gene therapies propels this expansion as clinical pipelines intensify. Advanced fermentation platforms enhance yield efficiency, enabling scalable production for commercial applications.

Shifting regulatory frameworks are anticipated to drive stringent compliance protocols across sophisticated biomanufacturing production facilities. Advanced continuous bioprocessing technologies are positioned to optimize overall plasmid yield and critical purity metrics. Rising pipeline commercialization is likely to require scalable outsourcing partnerships for establishing a sustainable global supply.

Key Industry Highlights:

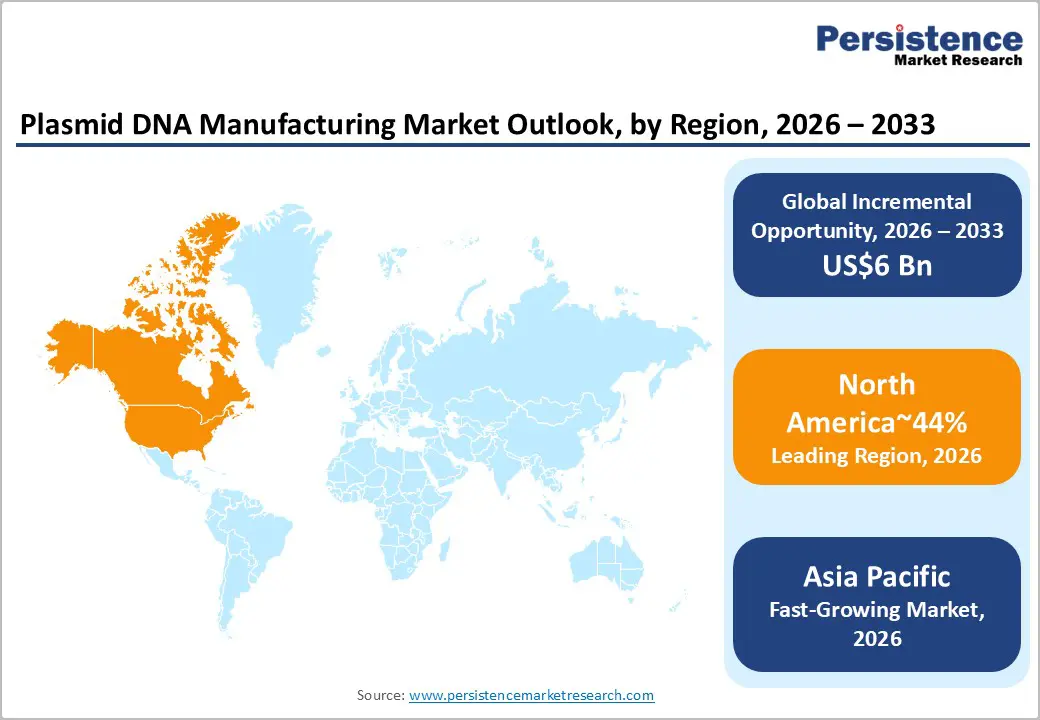

- Leading Region: North America is projected to lead, accounting for approximately 44% share in 2026, supported by mature biomanufacturing ecosystems, concentrated clinical trial activity, and robust venture capital inflows.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest, driven by rapid infrastructure buildout, cost-competitive scaling, and government-backed biotech incentives.

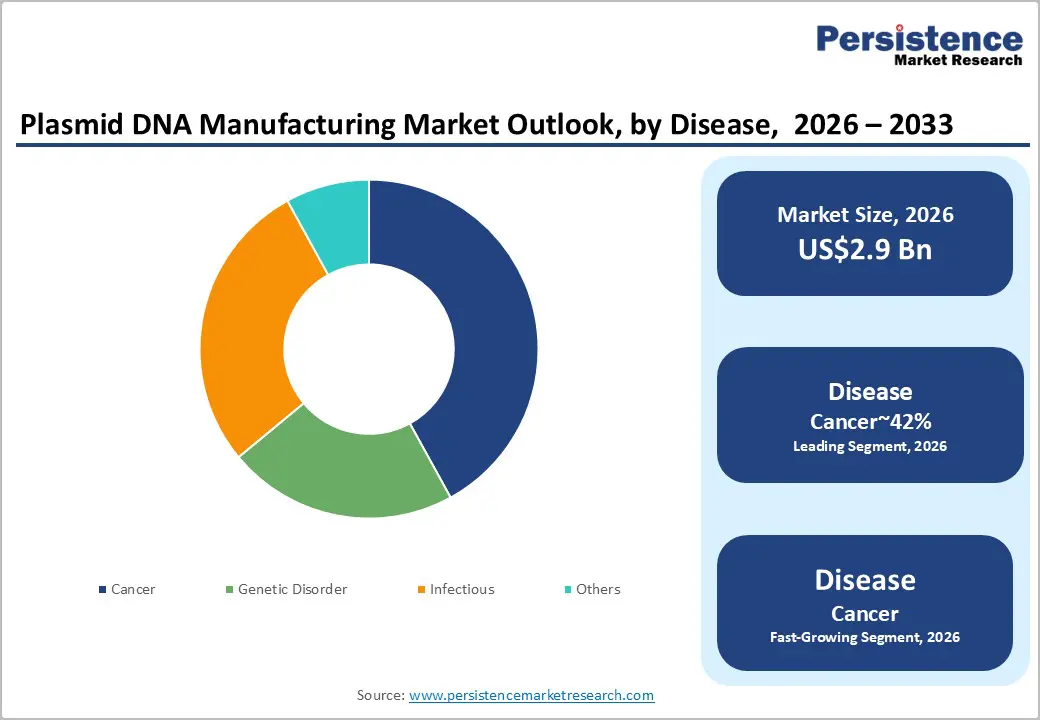

- Leading Disease: Cancer is projected to dominate, holding approximately 42% market share in 2026, driven by aggressive oncology pipelines, immunotherapy momentum, and precision medicine adoption.

- Leading Application: Cell & gene therapy is anticipated to lead, holding a substantial share in 2026, driven by vector production needs, Phase III trial escalations, and therapeutic approvals.

| Key Insights | Details |

|---|---|

|

Plasmid DNA Manufacturing Market Size (2026E) |

US$2.9 Bn |

|

Market Value Forecast (2033F) |

US$8.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

17.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

16.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Expanding Clinical Pipelines for Autologous Cell Therapies

Growth Dynamics – Autologous Cell Therapy Pipeline Expansion and Manufacturing Outsourcing

Expanding clinical pipelines for autologous cell therapies are intensifying demand for specialized vector manufacturing capacity globally. Accelerating regulatory clearances are institutionalizing advanced cellular therapies within frontline oncology treatment paradigms across major markets. Rising clinical trial volumes are exposing structural constraints in internal biomanufacturing infrastructure and capacity utilization efficiency. Biopharmaceutical developers are increasingly reallocating production toward external contract manufacturing to ensure scalability and timeline adherence. This transition is restructuring value capture across the manufacturing ecosystem, emphasizing flexibility, throughput optimization, and cost predictability. Platform standardization and modular production architectures are enabling more efficient handling of complex genetic constructs at scale. Consequently, outsourcing penetration is deepening as firms prioritize capital-light strategies and operational agility in clinical advancement.

Process intensification and analytical advancements are transforming vector manufacturing through improved monitoring and control capabilities. Emerging process analytical technologies are enabling real-time visibility into fermentation dynamics, reducing batch variability and failure risks. Continuous optimization of upstream and downstream workflows is improving yield efficiency and compressing production cycle timelines. Integration of automated control systems is lowering manual intervention requirements while enhancing reproducibility across manufacturing batches. These technological shifts are recalibrating cost structures by reducing waste, improving asset utilization, and stabilizing production economics. Digitalization of manufacturing environments is facilitating predictive maintenance and adaptive process adjustments in response to variability. Collectively, these advancements are strengthening supply reliability while supporting increasing complexity in autologous therapy production systems.

Shifting Preference toward High-Fidelity Continuous Bioprocessing Technologies

Shifting preference toward high-fidelity continuous bioprocessing technologies is restructuring global biomanufacturing operating frameworks and cost efficiencies. Escalating production expenditures are compelling manufacturers to transition from batch-based systems toward integrated continuous processing architectures. Intensified upstream methodologies are enhancing volumetric productivity while enabling more consistent output across complex biologics production cycles. Operational redesign is reducing equipment footprint requirements, optimizing facility utilization, and improving overall yield per manufacturing unit. Sustainability imperatives are reinforcing adoption as continuous systems minimize resource consumption, waste generation, and energy intensity. Standardized platform approaches are streamlining scale-up processes, reducing variability, and strengthening reproducibility across production environments. These dynamics collectively reposition continuous bioprocessing as a core enabler of cost-efficient, high-throughput biologics manufacturing ecosystems.

Advancements in downstream integration and analytical control systems are reinforcing performance gains within continuous production environments. Continuous chromatography innovations are eliminating batch-related bottlenecks, enabling uninterrupted purification and higher product recovery rates. Evolving sensor technologies are delivering precise, real-time environmental monitoring during sensitive cellular fermentation and vector production phases. Enhanced process visibility is reducing deviation risks while improving batch consistency and regulatory compliance readiness. Automation-driven control frameworks are lowering manual intervention, increasing operational reliability, and supporting scalable production expansion. These integrated technologies are reshaping cost structures by improving throughput predictability and reducing process inefficiencies.

Barrier Analysis – Complex Analytical Bottlenecks Delaying Critical Product Release

Complex analytical bottlenecks are prolonging critical product release timelines across advanced biomanufacturing and gene therapy workflows. Intricate quality control frameworks require multi-layered sequencing verification, increasing dependency on specialized instrumentation and expertise. Highly engineered supercoiled genetic constructs present characterization challenges that exceed conventional analytical resolution capabilities. Demand for ultra-pure materials is pushing existing validation technologies toward performance and sensitivity thresholds. These constraints are intensifying operational costs while extending cycle times across quality assurance and batch release functions. Stringent release specifications are reinforcing reliance on high-resolution mass spectrometry and advanced structural verification systems. Consequently, analytical throughput limitations are emerging as a critical constraint within scalable, high-complexity biologics production environments.

Evolving analytical technologies are partially mitigating constraints but introducing additional layers of process complexity and investment intensity. Advanced verification platforms are improving structural integrity assessment while requiring significant capital allocation and technical specialization. Integration of functional assays is expanding quality validation scope, increasing development timelines for customized therapeutic products. Enhanced characterization protocols are improving reliability yet contributing to longer validation cycles and workflow dependencies. Automation and digital analytics are supporting consistency, but remain constrained by assay sensitivity and data interpretation requirements. These dynamics are reshaping cost structures, with analytical validation becoming a disproportionately resource-intensive production stage. Analytical evolution is balancing improved quality assurance with persistent throughput and scalability challenges across manufacturing systems.

Intellectual Property Fragmentation in Plasmid Backbone Technologies

The overlapping patents on plasmid backbone architectures are constraining technology access across vector development and manufacturing ecosystems. Fragmented intellectual property landscapes are compelling developers to navigate complex licensing frameworks before initiating design workflows. Negotiation overheads are increasing transaction costs, delaying program timelines, and limiting cross-organizational collaboration in innovation cycles. This environment is fostering technological silos, reducing knowledge diffusion, and weakening cumulative research productivity across the sector. Restricted access to foundational genetic elements is also narrowing design flexibility for emerging therapeutic and industrial applications. Legal uncertainties surrounding freedom-to-operate are elevating risk exposure within early-stage development pipelines and commercialization strategies. Collectively, intellectual property fragmentation is embedding structural inefficiencies within upstream innovation and downstream manufacturing integration. Consolidation of key intellectual property positions is reinforcing competitive asymmetry across plasmid technology providers and service ecosystems.

Dominant patent holders are strengthening control over critical backbone platforms, shaping access terms and influencing market participation thresholds. Mid-tier providers are facing intensified pricing pressures as licensing dependencies compress margins and limit differentiation capabilities. Disputes over proprietary technologies are slowing broader adoption of advanced plasmid systems despite demonstrated performance advantages. This dynamic is redistributing value capture toward entities with established intellectual property portfolios and legal enforcement capacity. Barrier to entry is increasing as new participants encounter high compliance costs and constrained access to validated backbone constructs. The intellectual property concentration is reshaping competitive dynamics and moderating innovation velocity within plasmid-based production markets.

Opportunity Analysis – Viral Vector Integration and Platform Consolidation

Viral vector synergies are expanding capacity requirements across plasmid manufacturing and gene therapy production ecosystems. Integration with adeno-associated and lentiviral vector workflows is creating cross-service demand for aligned upstream inputs. Biopharmaceutical developers are prioritizing single-provider models to streamline procurement, reduce coordination complexity, and ensure scalability. End-to-end manufacturing alignment is enabling tighter process control, improving consistency across vector design, production, and delivery stages. This convergence is increasing contract scope, elevating deal sizes, and reinforcing long-term supplier relationships within integrated service frameworks. Operational interoperability between plasmid and viral vector platforms is reducing transition inefficiencies and enhancing overall production throughput. Integrated manufacturing ecosystems are emerging as critical enablers of efficiency and scalability in gene therapy pipelines.

Platform convergence strategies are intensifying competition among providers seeking to capture value across multiple stages of production. Bundled service offerings are enabling suppliers to internalize greater portions of the value chain while improving client retention. Technological alignment across plasmid and viral vector systems is supporting standardized workflows and reducing validation redundancies. Capacity expansion initiatives are being structured around multi-modality production capabilities to address diverse therapeutic requirements. These developments are reshaping cost structures by distributing fixed investments across broader service portfolios and higher utilization rates. Integrated platforms are strengthening switching costs as clients embed processes within unified manufacturing ecosystems. The viral vector integration is accelerating market consolidation while reinforcing scale-driven advantages in advanced therapy production.

Artificial Intelligence – Driven Vector Design Optimization

Artificial intelligence integration is transforming vector sequence design through advanced computational modeling and predictive optimization capabilities. Machine learning frameworks are reducing development timelines by accelerating the identification of high-performance genetic configurations. In-silico modeling paradigms are enhancing cellular expression yields through precise simulation of complex biological interactions. Growing computational power is enabling accurate prediction of supercoiled structural behavior under diverse production conditions. These advancements are reducing experimental dependency, lowering iteration cycles, and improving overall R&D efficiency. Algorithmic design platforms are facilitating rapid customization of vectors tailored to specific therapeutic and production requirements. AI-driven design is emerging as a critical lever for improving speed, precision, and scalability in vector development.

Integration of AI within manufacturing workflows is reshaping cost structures and operational reliability across vector production systems. Predictive modeling minimizes batch failure risks by optimizing process parameters before physical execution. Computational optimization tools are enhancing expression stability, supporting consistent output across scaled manufacturing environments. Strategic software collaborations are strengthening differentiation among service providers within competitive contract manufacturing landscapes. Digital design ecosystems are enabling seamless transition from sequence optimization to process development and production stages. These technologies are reducing material waste, improving yield predictability, and enhancing overall process economics. AI integration is reinforcing data-driven decision-making while advancing efficiency across vector design and manufacturing value chains.

Category–wise Analysis

Grade Insights

GMP grade is expected to lead, accounting for approximately 87% share in 2026, underpinned by mandatory clinical compliance and entrenched quality assurance frameworks across late-stage therapeutic production. Adoption remains anchored by superior purity thresholds, sequence fidelity, and qualification readiness required for human applications. Biopharmaceutical developers prioritize standardized, validated manufacturing environments to ensure seamless progression across clinical phases and commercialization.

Advanced platforms such as Aldevron’s pDNA-HQ, Thermo Fisher Scientific’s TheraPure, and Lonza’s pDNASelect reinforce operational consistency and impurity minimization. Ongoing evolution in automation, analytical validation, and real-time monitoring enhances throughput and scalability across facilities.

GMP grade is expected to be the fastest growing segment, driven by the accelerating commercialization of advanced gene and cell therapies requiring fully compliant production systems. Growth is catalyzed by continuous manufacturing innovations, modular cleanroom expansion, and AI-driven process controls, improving scalability and batch consistency. Increasing demand for large-scale oncology and CAR-T applications is amplifying the need for high-throughput, validated plasmid production.

Platforms such as Charles River Laboratories’ eXpDNA, Catalent’s UpTempo Virtuoso, and Thermo Fisher’s GeneArt plasmids are advancing integrated, high-efficiency workflows. As validation pathways, infrastructure readiness, and workforce expertise expand, GMP Grade is positioned to outpace overall market growth.

Disease Insights

Cancer is anticipated to lead, accounting for approximately 42% share in 2026, underpinned by expansive oncology pipelines and sustained demand for advanced immuno-oncology and cellular therapies. Adoption remains anchored by the critical role of high-purity plasmids in enabling efficient transduction for CAR-T and lentiviral-based applications across solid and hematologic malignancies. Biopharmaceutical companies prioritize scalable, validated production systems to support late-stage trials and commercial oncology programs.

Platforms such as Lonza’s pDNASelect, Genscript’s ProPlasmid, and Nature Technology’s SB-Fulcrum strengthen vector optimization and expression efficiency. Continuous advancements in antibiotic-free systems, combination therapies, and engineered constructs further reinforce utilization intensity. This convergence of clinical momentum, ecosystem lock-in, and high-volume demand sustains cancer’s dominance within advanced therapeutic manufacturing frameworks.

Cancer is expected to be the fastest-growing segment, driven by unmet needs in solid tumor targeting and rapid innovation in engineered cellular immunotherapies. Growth is catalyzed by advancements in armored CAR-T designs, bispecific constructs, and high-titer plasmid systems that improve therapeutic efficacy in resistant indications. Increasing demand for customized vector architectures is accelerating adoption across complex oncology workflows.

Platforms such as Aldevron’s GMP pDNA, VGXI’s HD Plasmid, and Vigene Biosciences’ pHelper plasmids are enabling high-performance, application-specific solutions. Adoption is further supported by AI-driven design, process optimization, and expanding personalized medicine frameworks, reducing development bottlenecks. As clinical validation deepens and manufacturing capabilities scale, cancer is positioned to outpace overall market growth.

Regional Insights

Asia Pacific Plasmid DNA Manufacturing Market Trends

Asia Pacific is expected to witness the fastest growth, supported by rapidly expanding market share driven by substantial infrastructure investments in contract biomanufacturing and production scale-up capabilities. Favorable government policies are likely to support the development of regional commercial manufacturing facilities through funding and incentives. Evolving global outsourcing trends are also anticipated to shift production volumes toward cost-efficient regional networks.

Scaling initiatives by GenScript through its ProPlasmid platform are expected to reshape biomanufacturing cost structures, while advanced processing technologies adopted by WuXi Advanced Therapies via XLenti are likely to strengthen regional clinical quality standards.

China is projected to decisively anchor this explosive regional momentum through aggressive domestic biotechnology and industrialization initiatives. Massive state-sponsored investments are projected to drastically accelerate the comprehensive modernization of localized biopharmaceutical clinical manufacturing ecosystems. Shifting regulatory modernization efforts are anticipated to increasingly align domestic clinical standards with stringent international commercial compliance frameworks.

Strategic capacity expansions by Thermo Fisher Scientific with TheraPure are likely to aggressively capture surging localized commercial demand. Expanding domestic clinical pipelines are positioned to generate unprecedented, sustained requirements for critical biological precursor developmental materials.

North America Plasmid DNA Manufacturing Market Trends

North America is expected to remain the leading regional market, accounting for approximately 44% share in 2026, supported by robust clinical pipelines and mature advanced biopharmaceutical manufacturing innovation ecosystems. Concentrated institutional capital allocations are projected to continuously fund massive infrastructure expansions across major contract manufacturing networks. Shifting technological paradigms are anticipated to drive the rapid adoption of highly advanced continuous bioprocessing system implementations.

Pioneering operational scale by Catalent with UpTempo Virtuoso is likely to structurally dominate the regional supply landscape. Sophisticated analytical integration from Charles River Laboratories with eXpDNA is positioned to firmly establish critical regional quality benchmarks.

The U.S. is expected to consistently anchor this dominant regional market growth trajectory moving forward. Aggressive regulatory modernization by federal agencies is projected to accelerate novel advanced therapeutic commercial market approvals. Shifting domestic procurement strategies are anticipated to strongly incentivize deeply localized critical biological material manufacturing supply chains. Strategic facility investments by Aldevron with pDNA-HQ are likely to perfectly secure massive domestic clinical production capacities. Expanding biotechnology hubs are positioned to perpetually foster unprecedented regional innovations in highly complex genetic medicine developments.

Europe Plasmid DNA Manufacturing Market Trends

Europe is expected to remain a mature and structurally stable regional market, approximating a significant market share, with demand primarily anchored in established clinical research frameworks and stringent quality compliance protocols. Sophisticated institutional healthcare systems are projected to systematically fund the steady adoption of targeted advanced cellular therapies. Shifting regulatory harmonizations are anticipated to streamline complex cross-border commercialization pathways across the entire continental industrial landscape.

Rigorous engineering standards by Boehringer Ingelheim with ViraThera are likely to perfectly align with strict regional clinical mandates. Advanced validation methodologies from PlasmidFactory with High-Quality Grade In Vitro are positioned to ensure absolute continental operational compliance.

Germany is expected to play a key role in sustaining regional market stability, supported by its strong legacy in advanced biomanufacturing engineering. Its well-established industrial ecosystem is likely to enable the efficient deployment of automated production technologies. Shifting national health priorities are anticipated to heavily subsidize specialized research into targeted rare genetic pediatric disorders. Targeted facility upgrades by Cobra Biologics with HQ Plasmid are likely to effectively modernize aging domestic biological infrastructures. Expanding collaborative research networks are positioned to continuously sustain a highly predictable baseline of clinical material manufacturing demand.

Competitive Landscape

The global plasmid DNA manufacturing market remains moderately consolidated, as scale barriers favor established CDMOs with validated platforms amid surging gene therapy needs. Leading players exert influence through technology footprints and procurement lock-ins, where end-to-end capabilities command premium contracts. Lonza with pDNASelect, Aldevron with GMP pDNA, Catalent with Phoenix services, and Thermo Fisher with GeneArt plasmids benchmark purity and throughput, shaping industry standards via IP-protected processes. Brand equity secures repeat biopharma allocations, amplifying ecosystem dependencies.

Competitive positioning differentiates vertically via tiered offerings, with premium innovators building moats around automation IP. Vigene Biosciences with pHelper plasmids contrasts value players by emphasizing custom constructs, while horizontal expansions into viral services proliferate partnerships. D2C models evolve minimally, favoring B2B platforms; intensity tilts toward innovators gaining via capacity pre-books. Archetypes prioritizing agility are positioned to expand their share.

Key Industry Developments:

- In January 2026, Bionova Scientific formed a manufacturing alliance with Syenex to expand global plasmid DNA access. This partnership leverages IS-free cell lines to produce stable and reproducible vectors, significantly reducing the risk of genetic instability in cell and gene therapy (CGT) manufacturing.

- In January 2026, AGC Biologics launched a single-plasmid lentiviral packaging system via its Milan Center of Excellence. By consolidating the standard four-plasmid process into one, this development slashes production timelines and costs, providing a major competitive edge for developers seeking rapid clinical readiness.

- In November 2025, Bharat Biotech launched Nucelion Therapeutics to focus on cell and gene therapy manufacturing. This marks a strategic entry of a major Indian pharma player into the pDNA space, intensifying global competition for high-quality clinical-grade starting materials.

Companies Covered in Plasmid DNA Manufacturing Market

- Lonza

- Thermo Fisher Scientific

- Catalent

- WuXi Advanced Therapies

- Aldevron

- Charles River Laboratories

- AGC Biologics

- Kaneka Eurogentec

- VGXI, Inc.

- Boehringer Ingelheim

- Genscript

- Yposkesi

- PlasmidFactory GmbH & Co. KG

- Vigene Biosciences

- Nature Technology

- Biomay AG

Frequently Asked Questions

The global plasmid DNA manufacturing market is anticipated to be valued at US$ 2.9 billion in 2026. Tremendous structural expansion is projected to rapidly push this valuation to US$ 8.9 billion by 2033.

Expanding clinical pipelines for autologous cell therapies are expected to strongly drive unprecedented massive global market expansion. Surging commercialization requirements are projected to systematically force biopharmaceutical developers toward scalable external contract manufacturing partners.

The market is officially projected to systematically expand at a robust forecast CAGR of 17.4%. This impressive trajectory is expected to heavily reflect the massive historical CAGR of 16.9%.

North America is firmly positioned to dominantly lead the global landscape moving into the immediate future. This specific region is projected to heavily account for approximately 44% share in 2026.

Leading dominant industry participants are expected to systematically include Aldevron, Thermo Fisher Scientific, and Charles River Laboratories. Advanced engineering innovators such as Catalent and Genscript are projected to powerfully shape complex global competitive dynamics