- Medical Devices

- Disposable Spinal Instrument Market

Disposable Spinal Instrument Market Size, Share, and Growth Forecast, 2026 – 2033

Disposable Spinal Instrument Market by Product Type (Spinal Surgical Tools, Spinal Implants & Devices, Sterilization Kits & Accessories, Cervical Kits, Lumbar Kits, Others), Procedure (Spinal Fusion Procedures, Decompression Surgeries, Disc Replacement Surgeries, Others), End-User (Hospitals & Surgical Centers, Ambulatory Surgical Centers (ASCs), Specialty Clinics, Others), and Regional Analysis for 2026-2033

Disposable Spinal Instrument Market Share and Trends Analysis

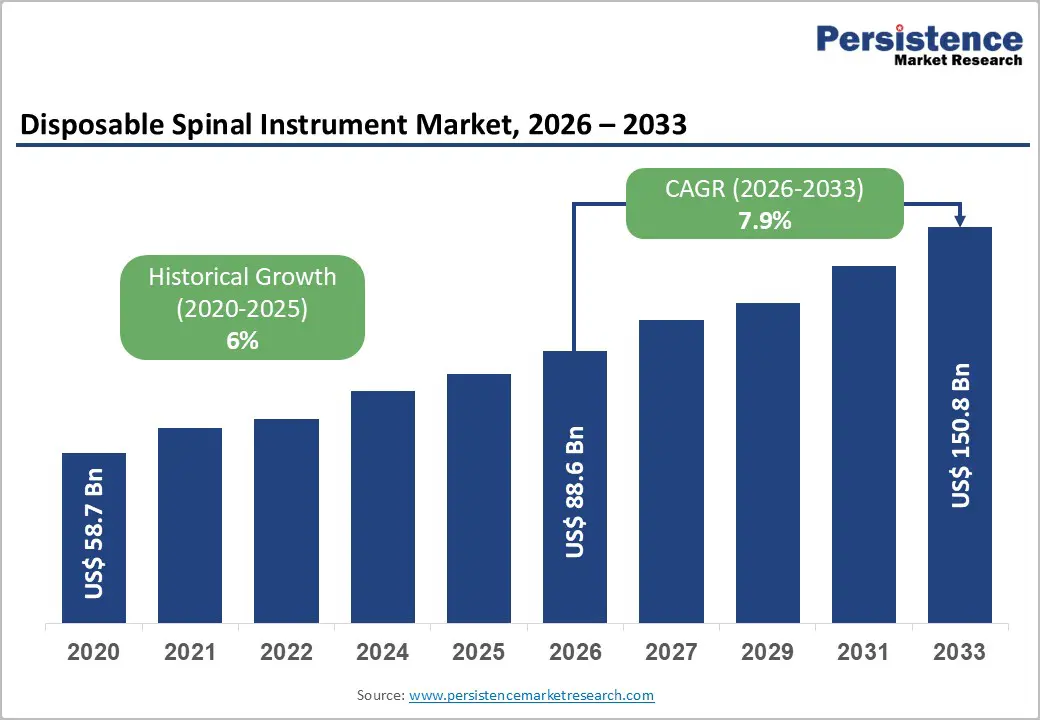

The global disposable spinal instrument market size is likely to be valued at US$ 88.6 billion in 2026, and is projected to reach US$ 150.8 billion by 2033, growing at a CAGR of 7.9% during the forecast period 2026−2033. Growth is primarily driven by rising spinal disorder incidence, expanding surgical volumes, and infection prevention priorities across healthcare systems. Aging populations increase degenerative spine conditions, including spinal stenosis and disc degeneration, creating sustained procedural demand. Clinical awareness initiatives led by agencies such as the World Health Organization (WHO) emphasize musculoskeletal health as a contributor to disability-adjusted life years, reinforcing early diagnosis and surgical intervention pathways.

Treatment adoption is likely to accelerate as surgeons prioritize single-use instrumentation to reduce cross-contamination risk and sterilization complexity. Infection control frameworks issued by the U.S. Centers for Disease Control and Prevention (CDC) support single-use device protocols in operative environments, strengthening procurement justification. Technological integration, including pre-sterilized kits and procedure-specific disposable sets, enhances operating room efficiency and standardization. Healthcare infrastructure expansion in emerging economies improves access to elective and trauma-related spinal procedures.

Key Industry Highlights

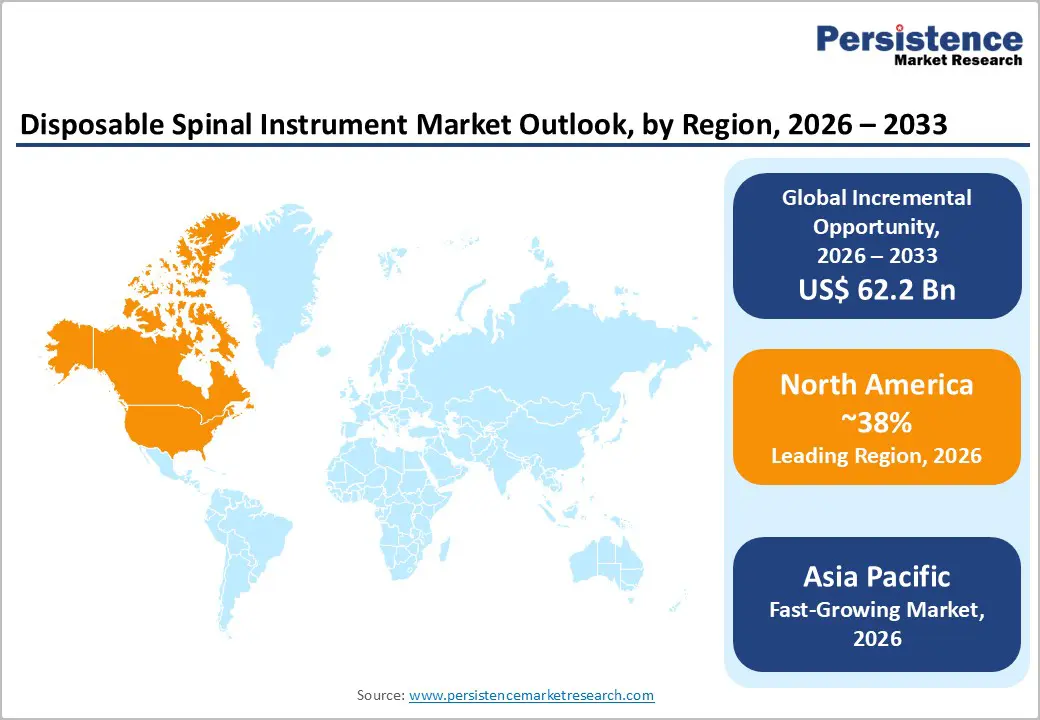

- Dominant Region: North America is projected to hold around 38% market share in 2026, driven by the widespread use of single-use spinal instruments.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing disposable spinal instrument market between 2026 and 2033, fueled by rising spinal disorder cases.

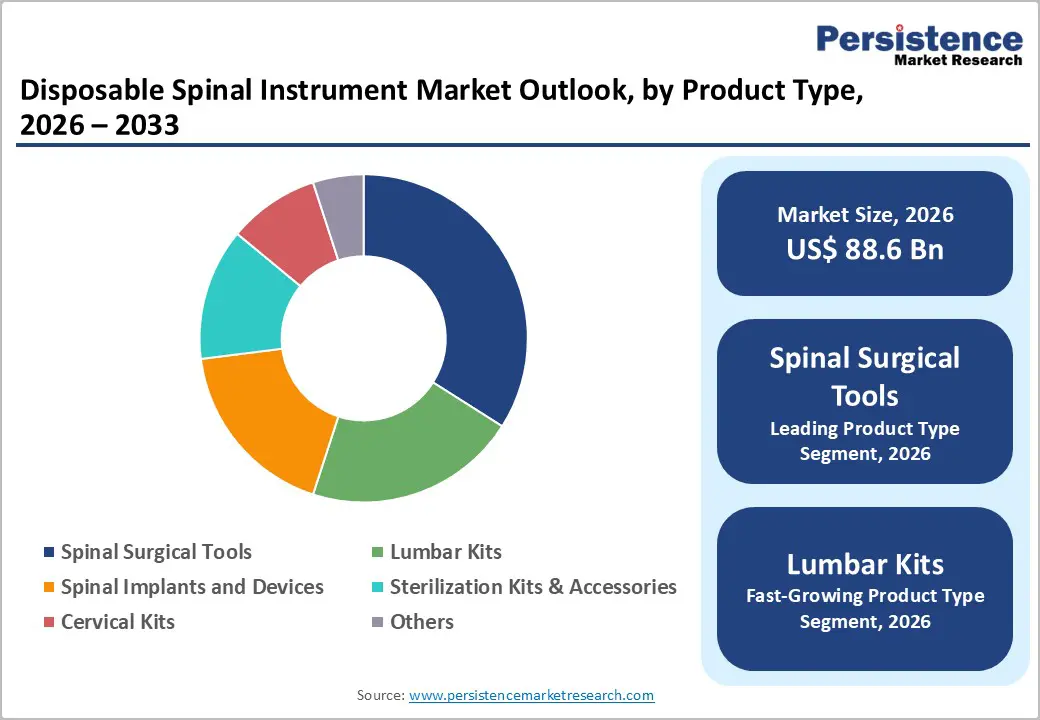

- Leading Product Type: Spinal surgical tools are set to lead with 34% of the disposable spinal instrument market in 2026, driven by broad applicability across procedures and high clinical adoption.

- Fastest-growing Product Type: Lumbar kits are expected to be the fastest-growing disposable spinal instrument segment between 2026 and 2033, propelled by rising lumbar degeneration and demand for minimally invasive fusion procedures.

| Key Insights | Details |

|---|---|

| Disposable Spinal Instrument Market Size (2026E) | US$ 88.6 Bn |

| Market Value Forecast (2033F) | US$ 150.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Degenerative and Trauma-Related Spinal Conditions

The expansion of chronic spinal conditions in aging populations is influencing pressures on healthcare systems and surgical demand. Population health data indicate that degenerative spinal pathologies such as disc degeneration, stenosis and spondylosis affect a significant portion of adults, with analyses of large-scale clinical claims showing an overall prevalence of diagnosed degenerative spine disease at approximately 27.3% in the United States and rising with age. These disorders often impair structural integrity and load management of the spine, increasing susceptibility to functional decline and presenting a growing caseload of patients requiring medical or surgical intervention. Trauma remains a consistent origin of acute spinal injury; mechanical forces from vehicular collisions, falls and other high-impact events contribute substantial numbers of injuries to the vertebral column and spinal cord annually.

Structural deterioration from degeneration alters biomechanical load distribution and reduces resilience to external forces, increasing both the frequency and complexity of clinical presentations involving neurological compromise or instability. Age-related changes in disc hydration, facet joint arthritis, and canal narrowing can progress to symptomatic conditions that require surgical correction or stabilization. Traumatic insults, whether from everyday falls in older adults or high-energy impacts in younger cohorts, further compound this burden by frequently necessitating urgent intervention and extended rehabilitation cycles.

Infection Prevention Protocols and Operating Room Efficiency Optimization

Stringent infection prevention protocols are reshaping surgical procurement strategies by prioritizing sterile, single-use solutions that reduce contamination exposure during spine procedures. Regulatory guidance from the CDC and standards aligned with the U.S. Department of Health and Human Services emphasize validated sterilization cycles, environmental monitoring, and traceable instrument processing workflows. Reusable spinal sets require multistep decontamination, inspection, packaging, and autoclave validation, creating operational complexity and documentation burden. Single-use systems eliminate reprocessing variability, lower risk of residual bioburden, and support audit readiness under hospital accreditation frameworks.

Operating room efficiency optimization further accelerates this shift by focusing on measurable throughput performance and cost containment. Reprocessing cycles consume labor hours, sterilizer capacity, water, and energy, creating hidden operational expenses within sterile processing departments. Disposable systems arrive procedure-ready, reducing setup time, minimizing tray assembly errors, and compressing turnover intervals between cases. Faster room readiness improves block utilization and strengthens scheduling predictability in high-volume spine programs. Streamlined logistics reduce dependency on instrument tracking software, maintenance contracts, and repair cycles linked to reusable equipment.

Environmental Sustainability Concerns and Waste Management Burden

Growing environmental regulation in the United States places significant pressure on healthcare operations that rely on single-use instruments, especially where waste volume and toxicity are concerned. Government data from the U.S. Environmental Protection Agency (EPA) indicates that healthcare facilities generate over 6,600 tons of medical waste daily, a large portion of which is from single-use products such as disposable instruments, packaging, sharps, and protective gear. Improper disposal of this regulated waste can lead to contamination of soil, air, and water resources, posing risks for communities and waste workers through potential exposure to infectious materials and release of toxic byproducts, including dioxins when incinerated.

Public policy emphasis on sustainable practices has created additional operational challenges. Legislators and regulators are encouraging reduction of waste generation and improved recycling practices across healthcare sectors, yet infrastructure and processes for segregating, reprocessing, or recycling single-use instruments remain immature relative to the volume of disposables currently used. Healthcare waste that enters landfills contributes to pollution and places pressure on limited waste management capacity, while stringent EPA and state requirements for safe disposal increase the cost and complexity for providers.

Supply Chain Vulnerability and Raw Material Dependency

Reliance on a narrow base of suppliers for critical inputs, including medical-grade plastics, specialized metals, and sterilization services, exposes production systems to interruption risk when upstream capacity is constrained or unpredictable. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) outline that disruptions in manufacturing, quality issues, or geopolitical events can trigger meaningful shortages in essential devices, as manufacturers often source key components globally and operate with limited transparency into their tier-2 and tier-3 suppliers. When a single source fails to deliver or when export restrictions tighten, lead times extend and production volumes shrink, driving unexpected cost inflation and weakening a company’s ability to fulfill delivery commitments.

Global upstream concentration in select regions creates structural risk that reduces flexibility in responding to supply fluctuations and elevates purchasing costs, particularly for niche polymers and alloy grades unique to precision surgical applications. Manufacturers face lengthy qualification cycles to validate alternative suppliers, often discouraging diversification and reinforcing single-source reliance. This dynamic slows inventory replenishment, inflates working capital requirements, and generates contractual penalties when deliveries slip. Furthermore, raw material scarcity can drive bidding competition with larger industrial sectors for basic feedstock, which undermines pricing stability and inflates input costs.

Expansion of Ambulatory Surgical Centers and Outpatient Spine Programs

The rapid shift of surgical volume from traditional hospital settings into ambulatory surgical centers (ASCs) and outpatient spine surgery programs is driving demand for disposable spinal instruments by positioning these sites as preferred venues for elective and minimally invasive spine procedures. ASCs offer shorter scheduling lead times, lower overhead costs and lower out-of-pocket expenses for patients compared with hospital outpatient departments, aligning with payer and provider cost containment priorities. CMS data indicate that about 6,300 ASCs treated 3.4 million fee-for-service Medicare beneficiaries in 2023, with the surgical volume per beneficiary increasing, underscoring sustained growth in outpatient surgical services within Medicare programs.

Outpatient spine programs are expanding as clinical practice evolves toward minimally invasive techniques that can be conducted safely without overnight stays, supported by regulatory updates broadening what procedures can be reimbursed in outpatient settings. As CMS finalizes expansions to the ambulatory surgery center covered procedures list, including additional musculoskeletal and spinal codes, hospitals and surgical groups are reallocating cases to ASCs and dedicated outpatient programs. This migration increases case volumes in non-hospital venues and amplifies demand for disposable instrument kits that reduce sterilization burden, decrease turnaround time and lower cross-contamination risks.

Technological Convergence with Minimally Invasive Spine Surgery

Integration of advanced imaging systems, robotics, and navigation technologies with minimally invasive spine procedures drives efficiency and precision in surgical interventions. Disposable spinal instruments complement this trend by reducing sterilization requirements, minimizing cross-contamination risk, and enhancing workflow in operating rooms. Surgeons gain improved access to targeted spinal regions while maintaining procedural safety and accuracy, leading to higher adoption of single-use instruments. Healthcare providers benefit from reduced operational downtime and lower inventory management complexities, supporting cost-effective deployment in high-volume surgical centers. The synergy between cutting-edge surgical tools and single-use devices strengthens procedural standardization and aligns with hospital priorities for patient safety and regulatory compliance.

Enhanced visualization, real-time feedback, and robotic-assisted maneuvering during minimally invasive spine surgeries elevate procedural outcomes and expand treatment options for complex spinal disorders. Disposable instruments offer compatibility with these systems, ensuring seamless integration without compromising sterility or instrument performance. Rising demand for outpatient and ambulatory surgical procedures drives adoption of lightweight, pre-sterilized instruments that streamline operations and reduce infection exposure. Market expansion is fueled by clinical preference for precise instrumentation and operational efficiency, encouraging investment in innovative disposable solutions tailored for next-generation surgical platforms.

Category-wise Analysis

Product Type Insights

Spinal surgical tools are poised to lead with a forecasted 34% of the disposable spinal instrument market revenue share in 2026, owing to broad applicability across fusion, decompression, and trauma procedures. Surgical drills, retractors, and curettes form the foundational instrument set for most spinal interventions, supporting a wide range of procedural requirements from basic decompression to complex spinal reconstructions. Clinical acceptance remains high due to standardized usage protocols, consistent performance, and compatibility with multiple procedural techniques, allowing surgeons to rely on predictable outcomes. Hospitals prioritize disposable surgical tools to reduce tray complexity, lower reprocessing variability, and mitigate cross-contamination risks.

Lumbar kits are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by increasing lumbar degeneration incidence and demand for minimally invasive lumbar fusion procedures. Procedure-specific kits streamline workflow, reduce assembly errors, and allow surgical teams to focus on patient care rather than instrument selection. Accessibility improves as outpatient centers and ambulatory surgical facilities increasingly adopt lumbar-focused programs, expanding the reach of targeted spinal interventions. Continuous product refinement enhances adherence to surgical best practices, incorporating innovations in guide systems, implant compatibility, and instrument ergonomics.

Procedure Insights

Spinal fusion procedures are likely to be the leading segment with a projected 41% market share in 2026, due to established clinical credibility and broad therapeutic indication coverage. Fusion remains a standard intervention for spinal instability, deformity correction, and degenerative disc disease, offering predictable structural outcomes for complex spinal conditions. Provider familiarity with surgical protocols, combined with clear reimbursement pathways, supports sustained utilization across hospitals and specialty centers. Disposable instrumentation ensures standardized intraoperative workflow, reduces sterilization requirements, and minimizes contamination risk, contributing to patient safety and operational efficiency.

Disc replacement surgeries are expected to grow the fastest between 2026 and 2033, driven by increasing acceptance of motion-preserving techniques and technological advancements in implant compatibility. Patients increasingly prefer minimally invasive solutions that maintain spinal mobility while addressing chronic pain and disc degeneration. Expansion of specialized spine centers and outpatient facilities enhances access to advanced surgical services, supporting broader procedure adoption. Preventive healthcare awareness encourages earlier intervention, resulting in timely patient referrals for disc replacement. Continuous innovation in implant design, navigation tools, and disposable instruments strengthens procedural safety and efficiency.

Regional Insights

North America Disposable Spinal Instrument Market Trends

North America is expected to dominate with an estimated 38% of the disposable spinal instrument market share in 2026, reflecting high procedural volume and extensive adoption of advanced spinal surgeries in the United States and Canada. Both countries feature well-established hospital networks and specialty spine centers that prioritize operational efficiency and patient safety, driving widespread integration of disposable spinal instruments. High demand in fusion, decompression, and motion-preserving interventions supports use of pre-sterilized, single-use tools, reducing turnaround times and sterilization constraints. Surgeons rely on standardized instrument sets to enhance workflow predictability and minimize intraoperative variability.

Investment in specialized training programs, procedural certifications, and research collaborations in the United States and Canada strengthens surgeon expertise and accelerates adoption of innovative surgical techniques. Clear regulatory frameworks and reimbursement pathways incentivize hospitals and outpatient facilities to implement disposable instruments, ensuring compliance with infection control standards while maintaining cost efficiency. Technological enhancements, including ergonomic design, precision cutting edges, and modular components, improve usability and reduce operational learning curves. Strong awareness of infection prevention and focus on patient outcomes drives adoption across public and private facilities.

Europe Disposable Spinal Instrument Market Trends

The European market is characterized by high adoption of advanced spinal procedures and strong infrastructure for surgical care, positioning it as a significant contributor to disposable spinal instrument demand. Established hospital networks and specialized spine centers prioritize patient safety, operational efficiency, and adherence to regulatory standards, driving integration of pre-sterilized, single-use instruments. High procedural volume in fusion, decompression, and motion-preserving interventions creates consistent demand for disposable solutions that streamline workflow and reduce sterilization requirements. Surgeons benefit from standardized instrument sets that improve intraoperative efficiency, minimize handling variability, and enhance precision during complex spinal procedures. Investment in navigation-assisted and robotic-supported surgeries further strengthens compatibility with disposable instruments, supporting repeated procurement and consistent utilization across both public and private healthcare facilities.

Government regulations and healthcare policies emphasizing infection control and procedural quality reinforce adoption of disposable instruments in clinical settings. Continuous focus on technological refinement, including ergonomic designs, modular instrument configurations, and precision cutting capabilities, enhances surgical efficiency and reduces operational learning curves. Increasing demand for minimally invasive procedures and outpatient surgical services encourages integration of disposable solutions to optimize procedural throughput and reduce cross-contamination risks. Collaborative initiatives between manufacturers and hospital networks ensure rapid product availability, training support, and clinical guidance, fostering trust and sustained adoption.

Asia Pacific Disposable Spinal Instrument Market Trends

Asia Pacific is forecasted to be the fastest-growing market for disposable spinal instrument between 2026 and 2033, propelled by increasing prevalence of spinal disorders and expanding access to advanced surgical care in countries such as China and India. Rising geriatric population and rapid urbanization contribute to higher incidence of degenerative disc disease, spinal trauma, and deformities, creating sustained demand for disposable spinal instruments. Expansion of specialty spine centers and adoption of minimally invasive and motion-preserving procedures enhance procedural standardization and operational efficiency. Surgeons prefer pre-sterilized, procedure-specific instruments that reduce intraoperative delays, minimize cross-contamination risk, and optimize workflow in high-volume surgical settings. Advanced operating room infrastructure and integration of navigation and robotic-assisted systems in countries such as Japan and South Korea further strengthen compatibility with disposable solutions, driving procurement preference and accelerating market penetration.

Government healthcare initiatives and rising healthcare expenditure in emerging economies support adoption of advanced surgical instruments. Increasing patient awareness and preventive care programs encourage earlier intervention for spinal conditions, boosting procedural uptake in both urban and semi-urban centers. Technological innovations, including modular instrument sets, ergonomic designs, and enhanced precision, improve surgeon efficiency and procedural outcomes, reinforcing reliance on disposable instruments. Growth of outpatient surgical facilities and multi-specialty hospitals enhances access to advanced spinal procedures, while concentrated clinical demand encourages bulk procurement and recurring revenue generation.

Competitive Landscape

The global disposable spinal instrument market demonstrates moderate consolidation, driven by a mix of multinational orthopedic device manufacturers and regional specialists. Key players such as Medtronic, Stryker, Johnson & Johnson, Zimmer Biomet, Globus Medical, Inc., and NuVasive® hold significant revenue share, leveraging extensive product portfolios and established clinical relationships. Competitive positioning revolves around technological innovation, including development of procedure-specific kits, ergonomic instruments, and compatibility with navigation and robotic-assisted systems. Strong distribution networks enable rapid product availability across hospitals, specialty spine centers, and outpatient facilities, supporting high-volume procedural demand.

Innovation capability remains a central differentiator, with leading manufacturers investing in research and development to enhance precision, reduce procedural complexity, and optimize workflow efficiency. Regulatory adherence and certifications bolster trust among healthcare providers, reinforcing repeat adoption of disposable instruments. Regional specialists complement market coverage by offering niche solutions tailored for specific spinal procedures or emerging markets, fostering localized penetration. Procedure-specific kits, modular designs, and pre-sterilized instruments improve operational efficiency, reduce cross-contamination risk, and streamline intraoperative workflow. Market consolidation reflects both competitive intensity and collaboration opportunities, as key players maintain leadership through strategic partnerships, clinical training programs, and investment in emerging technologies.

Key Industry Developments

- In January 2026, SurGenTec received U.S. FDA clearance for its ION-C Facet Fixation System, designed to support posterior cervical fusion while preserving natural spinal alignment. The system uses a zero-profile implant and single-use sterile instruments to enable controlled insertion and reduce surgical risks.

- In September 2025, Ruthless Spine received U.S. FDA 510(k) clearance and a U.S. patent for NavJam, a disposable spinal navigation instrument designed to improve pedicle screw placement accuracy while reducing surgical time and radiation exposure.

- In July 2025, VGI Medical introduced the T5 sterile-packed, single-use titanium implant system for posterior sacroiliac joint fusion, offering surgeons pre-sterilized implants and disposable instruments that simplify workflow, eliminate reprocessing, and support efficient minimally invasive procedures.

Companies Covered in Disposable Spinal Instrument Market

- Medtronic

- Stryker

- Johnson & Johnson

- Zimmer Biomet.

- Globus Medical, Inc.

- NuVasive®, Inc.

- Orthofix Medical Inc.

- Smith+Nephew.

- Arthrex, Inc.

Frequently Asked Questions

The global disposable spinal instrument market is projected to reach US$ 88.6 billion in 2026.

Rising adoption of minimally invasive and motion-preserving spinal surgeries, combined with demand for standardized, pre-sterilized instruments, is driving the market.

The market is poised to witness a CAGR of 7.9% from 2026 to 2033.

Integration of advanced surgical technologies with procedure-specific disposable kits and expansion of outpatient spinal surgery services are unlocking lucrative market opportunities.

Some of the key market players include Medtronic, Stryker, Johnson & Johnson, Zimmer Biomet, and Globus Medical, Inc.