- Baby Care & Accessories

- Disposable Hygiene Product Market

Disposable Hygiene Product Market Size, Share, and Growth Forecast, 2026 - 2033

Disposable Hygiene Product Market by Product Type (Tampons, Toilet Paper, Tissue Paper, Wipes, Sanitary Napkins, Diapers), Sales Channel (Drug Stores/Pharmacies, Online, Supermarkets/Hypermarkets), and Regional Analysis for 2026 - 2033

Disposable Hygiene Product Market Size and Trends Analysis

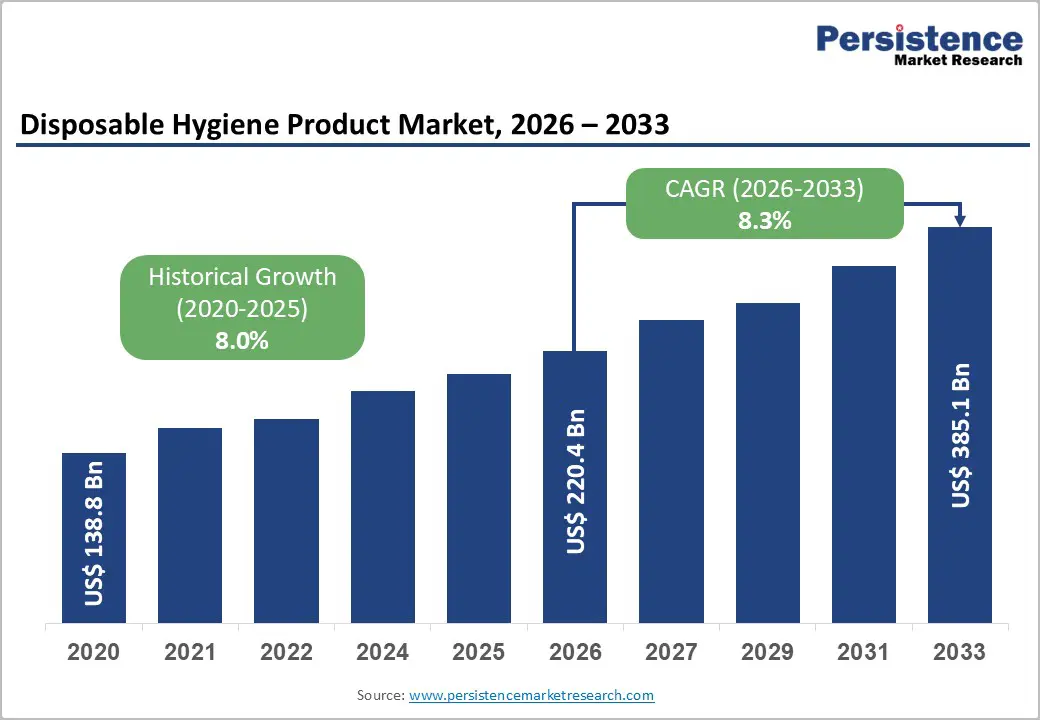

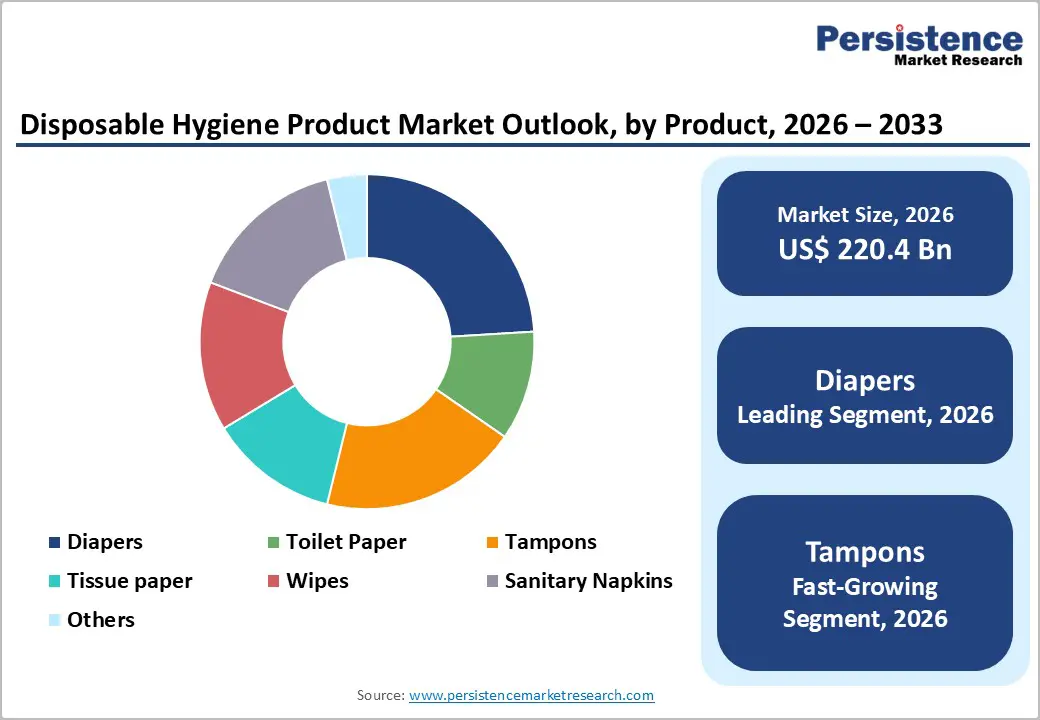

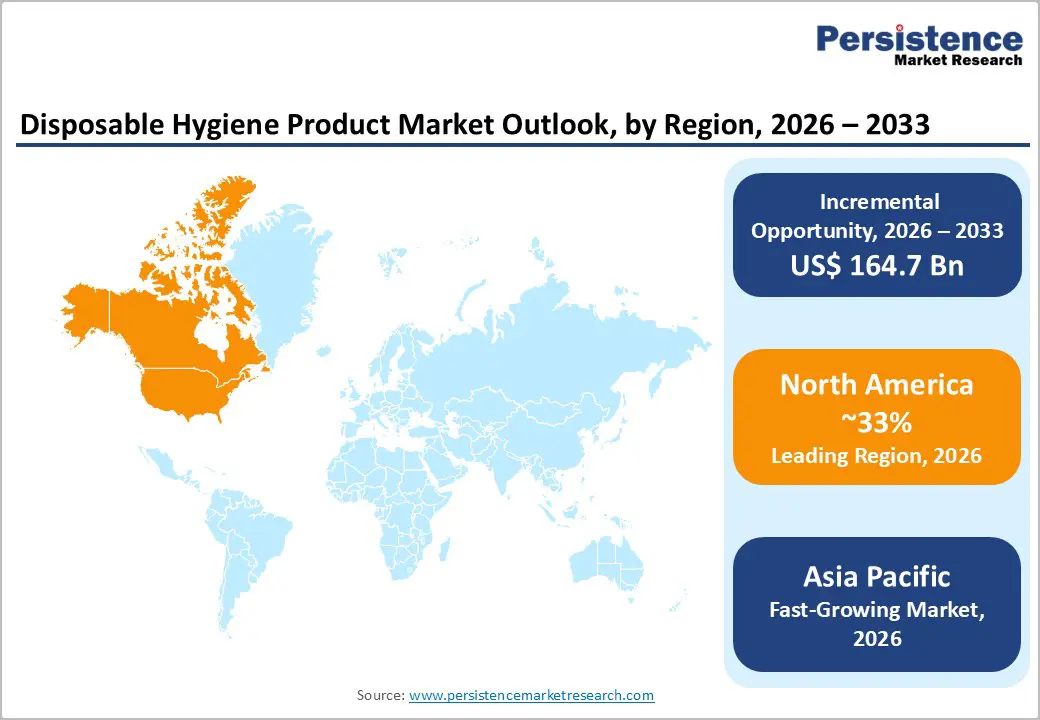

The global disposable hygiene product market size is likely to be valued at US$220.4 billion in 2026 and is expected to reach US$385.1 billion by 2033, growing at a CAGR of 8.3% during the forecast period from 2026 to 2033, driven by demographic changes, rising hygiene awareness, and evolving distribution channels. Increased participation of women in the workforce has fueled the adoption of feminine hygiene products, while aging populations in developed regions have created sustained demand for adult incontinence solutions.

Urbanization, rising disposable incomes, and government-led sanitation initiatives in emerging economies have accelerated the use of convenient single-use hygiene items. The proliferation of modern retail formats and e-commerce platforms has expanded accessibility, allowing consumers to engage with a wider variety of products and brands. Innovation in product design, including enhanced absorbency, skin-friendly materials, and environmentally conscious alternatives such as biodegradable diapers and sanitary products.

Key Industry Highlights:

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 33% in 2026, driven by high per-capita consumption, aging demographics, women’s workforce participation, strong hygiene awareness, and a robust innovation ecosystem.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the disposable hygiene product market in 2026, supported by population growth, urbanization, rising incomes, government sanitation initiatives, and cost-efficient manufacturing hubs.

- Leading Product Type: Diapers are projected to represent the leading product type in 2026, accounting for 40% of the revenue share, driven by consistent birth rates, dual-income households, and demand for premium features such as ultra-thin cores and enhanced leak protection.

- Leading Sales Channel: Supermarkets/Hypermarkets are anticipated to be the leading sales channel, accounting for over 39% of the revenue share in 2026, supported by one-stop convenience, bulk discounts, private-label options, and immediate product availability for families and institutional buyers.

| Key Insights | Details |

|---|---|

|

Disposable Hygiene Product Market Size (2026E) |

US$220.4 Bn |

|

Market Value Forecast (2033F) |

US$385.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Increasing Female Workforce Participation and Menstrual Hygiene Awareness

The rising participation of women in the workforce has significantly boosted demand for disposable feminine hygiene products such as tampons, sanitary napkins, and panty liners. Working women prioritize convenience, comfort, and discretion, which drives consistent purchases across urban centers. Greater menstrual hygiene awareness supported by government programs, NGOs, and educational campaigns has reduced stigma and encouraged adoption of modern products. The combination of professional lifestyles, longer working hours, and easy access through retail and e-commerce channels has expanded usage frequency and brand loyalty, stimulating market growth in the feminine hygiene segment.

Increasing awareness of menstrual health in semi-urban and rural regions has widened the consumer base. Campaigns promoting hygienic practices, along with government subsidies and school programs, have increased the adoption of disposable menstrual products. Digital platforms and social media marketing reinforce awareness while enabling discreet purchasing, contributing to higher penetration rates. Brands are innovating with biodegradable, skin-friendly, and premium products to cater to the evolving needs of working women. This dual impact lifestyle-driven demand in urban areas and awareness-driven adoption in emerging markets makes female workforce participation and menstrual hygiene consciousness a sustained driver of market expansion.

Aging Population and Rising Incontinence Prevalence

Aging populations in developed countries are a major driver of the disposable hygiene market, particularly for adult diapers and incontinence products. As life expectancy rises, the prevalence of age-related conditions such as urinary incontinence and mobility challenges increases, creating consistent demand for convenient, hygienic solutions. Healthcare providers and caregivers prefer disposable products for their ease of use, absorbency, and odor control. Growing awareness of personal hygiene among elderly consumers fuels market penetration. This demographic shift, coupled with increasing institutional adoption in hospitals, nursing homes, and home care settings, strengthens the adult incontinence segment as a key contributor to overall market growth.

The rising incidence of post-surgical care needs, chronic illnesses, and mobility limitations among aging populations also propels demand for disposable hygiene solutions. Manufacturers are responding with high-performance, skin-sensitive, and comfortable designs, ensuring safety and repeated use. Healthcare reimbursement schemes in certain countries encourage the adoption of premium adult diaper products. Online and retail channels make these products more accessible for home-based caregivers. With the combination of demographic trends, increasing prevalence of chronic health conditions, and heightened awareness of hygiene.

Barrier Analysis - Environmental and Regulatory Pressures on Single-Use Plastics

Products such as diapers, wipes, and sanitary pads contribute to significant non-biodegradable waste, leading to stricter regulations in multiple regions. Governments are imposing bans on certain plastic components and mandating eco-friendly alternatives, which increase manufacturing costs and require product reformulation. Consumer pressure for sustainable products also forces companies to invest in R&D for biodegradable or compostable materials. These regulatory and societal expectations create both operational challenges and potential compliance risks, potentially slowing production cycles, increasing costs, and limiting the widespread adoption of conventional disposable hygiene products.

The regulatory environment varies across countries, with some enforcing strict packaging, disposal, and material standards. Companies may face penalties or restrictions if products fail to meet eco-compliance standards. Extended producer responsibility policies require manufacturers to take accountability for end-of-life product management. Transitioning to sustainable materials often demands expensive supply chain modifications, while maintaining product performance, absorbency, and skin safety remains challenging. This creates a balancing act between sustainability and functionality. Environmental scrutiny and regulatory pressures on single-use plastics act as significant market restraints, particularly in Europe, North America, and Asia Pacific regions with stringent eco-friendly regulations.

Health and Skin-Sensitivity Concerns with Chemical Formulations

Health concerns related to chemical additives, fragrances, and dyes in disposable hygiene products limit market growth. Consumers are increasingly aware of potential skin irritation, allergies, and long-term dermatological effects from prolonged contact with synthetic materials. This is especially critical for baby diapers, feminine hygiene products, and adult incontinence items. Negative publicity or safety warnings can influence purchasing behavior, driving demand toward hypoallergenic or chemical-free alternatives. Companies must carefully balance performance features, absorbency, and comfort while avoiding harmful chemicals, increasing R&D and compliance costs, and creating cautious adoption patterns among sensitive consumer segments.

Parents and caregivers are particularly vigilant about infant skin sensitivity, prompting the growth of premium, dermatologically tested products. Women with sensitive skin prefer organic or natural menstrual products, impacting mainstream sales of chemically treated items. Adult users with prolonged usage needs are also concerned about rashes or allergic reactions. This scrutiny limits the ability of manufacturers to aggressively push standard formulations, leading to higher costs for safer alternatives. The need for transparency in ingredient disclosure and third-party safety certifications increases operational complexity.

Opportunity Analysis - Sustainable and Biodegradable Product Innovation

Sustainability and biodegradable product innovation represent a major opportunity in the disposable hygiene market. Rising environmental awareness among consumers drives demand for eco-friendly diapers, sanitary pads, and wipes made from compostable or plant-based materials. Manufacturers are investing in research to develop products that retain high absorbency, comfort, and durability while minimizing ecological impact. Brands offering sustainable alternatives gain competitive differentiation, particularly among environmentally conscious millennials and Gen Z consumers. E-commerce and premium retail channels provide the ideal platforms to market these innovations, enabling the wide distribution of biodegradable options that address both environmental concerns and modern consumer expectations.

Government initiatives and NGO programs supporting sustainable hygiene solutions amplify market potential. Products certified by environmental standards, such as FSC-certified tissues or compostable diapers, appeal to socially responsible consumers. Partnerships with waste management and recycling organizations enhance end-of-life disposal, strengthening brand credibility. The combination of eco-conscious branding, product innovation, and regulatory encouragement positions sustainability as a high-growth avenue. By aligning performance with environmental stewardship, companies can capture new customer segments, command premium pricing, and build long-term loyalty.

Expansion of Adult Incontinence and Post-Surgical Care Segments

Increasing life expectancy, chronic illnesses, and mobility limitations create rising demand for high-quality adult diapers, bed pads, and post-surgical hygiene products. Healthcare institutions, nursing homes, and home-care providers are expanding procurement, favoring products with superior absorbency, comfort, and odor control. Advances in product design, including skin-friendly materials, discreet sizing, and user-focused packaging, enhance adoption. Online channels and subscription-based delivery models improve accessibility, enabling patients and caregivers to obtain necessary products conveniently and discreetly.

The post-operative care market also fuels growth, as hospitals and rehabilitation centers increasingly rely on disposable hygiene solutions to prevent infection and improve patient comfort. Technological improvements, such as breathable materials and ergonomic designs, differentiate products and drive brand preference. As public awareness grows around incontinence and post-surgical hygiene, social stigma declines, expanding market penetration. Investment in targeted marketing, clinical partnerships, and e-commerce distribution enhances reach to both institutional and individual consumers. The adult incontinence and post-surgical care segments represent a durable opportunity for market expansion, leveraging demographic trends, healthcare demand, and innovation in hygiene solutions.

Category-wise Analysis

Product Type Insights

Diapers are expected to lead the disposable hygiene product market, accounting for approximately 40% of revenue in 2026, driven by sustained birth rates, increasing dual-income households, and growing consumer preference for premium features such as ultra-thin cores, leak protection, and hypoallergenic materials. Urban parents prioritize convenience, comfort, and skin safety, which encourages repeat purchases through supermarkets, hypermarkets, and e-commerce platforms. For example, Pampers by Procter & Gamble has maintained market leadership in baby diapers through product innovations such as their Swaddlers and Premium Care lines that offer improved absorbency and softness for sensitive infant skin. Caregivers increasingly rely on high-quality diapers to ensure hygienic, hassle-free management of infants, reinforcing brand loyalty and frequent repurchase.

Tampons are likely to represent the fastest-growing segment in 2026, supported by increasing personal-care awareness, lifestyle changes, and growing away-from-home demand. Consumers are increasingly seeking convenience, hygiene, and portability, which has led to high adoption rates of disposable wipes for both infant and adult use. Feminine hygiene awareness programs and government initiatives, such as menstrual-health campaigns in India, have accelerated the penetration of sanitary napkins and tampons, driving consistent growth. For example, Kotex by Kimberly-Clark has successfully promoted ultra-thin, skin-friendly pads with innovative odor-control features, paired with educational campaigns targeting young women in urban and semi-urban regions.

Sales Channel Insights

Supermarkets and hypermarkets are projected to lead the market, capturing around 39% of the revenue share in 2026, supported by their convenience, wide assortment, and bulk purchasing advantages. These retail formats provide a one-stop shopping experience, allowing consumers to access baby diapers, wipes, tissue papers, and feminine hygiene products under a single roof. Private-label options offered by supermarket chains appeal to price-conscious families, while institutional buyers rely on these channels for bulk procurement. For example, Walmart in the U.S. offers a wide range of branded and private-label diapers and wipes, ensuring product availability and affordability across different consumer segments. Supermarkets also provide promotional offers, loyalty programs, and visibility advantages that enhance repeat purchases.

Online is likely to be the fastest-growing sales channel in 2026, driven by subscription models, discreet delivery, and changing consumer habits accelerated by the pandemic. These platforms offer convenience, price transparency, and recurring deliveries, which are particularly attractive for sensitive products such as adult incontinence solutions, tampons, and sanitary pads. For example, Amazon’s “Subscribe & Save” program provides recurring shipments of diapers and feminine hygiene items, allowing consumers to maintain continuous supply without frequent store visits. Online channels also empower smaller brands to reach wider audiences, including tier-2 and tier-3 cities, while offering educational content and product guidance.

Regional Insights

North America Disposable Hygiene Product Market Trends

North America is anticipated to be the leading region, accounting for a market share of 33% in 2026, driven by increasing hygiene awareness, busy urban lifestyles, and high per-capita consumption of products such as diapers, wipes, tissue paper, and feminine hygiene items. Consumers in the region are prioritizing convenience, skin safety, and performance features, which has led to growing demand for premium and technologically advanced products. The market is also shaped by evolving retail channels, including supermarkets, hypermarkets, and e-commerce platforms that enable wide distribution and subscription-based models for recurring purchases.

These factors have encouraged continuous innovation in product design, absorbency, and skin-friendly formulations, while brand loyalty remains strong among consumers who prioritize trusted, high-quality products in their daily hygiene routines. Sustainability and convenience are key trends shaping the market. For example, Essity AB has introduced its TENA line of adult incontinence products with skin-friendly materials, odor control, and biodegradable packaging, catering to environmentally conscious and aging consumers. Companies are also leveraging digital channels to promote subscription services, e-commerce delivery, and consumer education.

Europe Disposable Hygiene Product Market Trends

Europe is likely to be a significant market for disposable hygiene product in 2026, due to strong regulatory oversight. Consumers prioritize product quality, skin safety, and sustainability, which drives the adoption of premium baby diapers, feminine hygiene products, wipes, and adult incontinence solutions. Urbanization, increasing dual-income households, and an aging population contribute to steady growth across core segments. The region also exhibits significant penetration of modern retail formats such as supermarkets, hypermarkets, and e-commerce platforms, which support repeat purchases and bulk buying.

Sustainability and environmental concerns heavily influence consumer behavior, encouraging brands to innovate with biodegradable, recyclable, and chemical-free formulations. Innovation and eco-consciousness are prominent trends shaping market dynamics. For example, Essity AB’s Libero line of baby diapers in Europe emphasizes sustainable materials, improved absorbency, and skin-friendly fabrics, catering to environmentally aware parents. Companies are also expanding digital marketing campaigns and subscription-based e-commerce models to enhance convenience and consumer engagement.

Asia Pacific Disposable Hygiene Product Market Trends

The Asia Pacific region is likely to be the fastest-growing region in 2026, driven by population expansion, urbanization, rising disposable incomes, and increasing awareness of personal hygiene. Key product segments such as baby diapers, wipes, tissue paper, and feminine hygiene items are seeing strong adoption across China, India, Japan, and ASEAN countries. Government initiatives, including menstrual hygiene schemes in India and public sanitation campaigns in China, have increased product penetration. The growing middle class in emerging markets is demanding premium products that combine convenience, comfort, and skin safety, while e-commerce platforms provide easy access to these items in both urban and semi-urban areas.

Demographic trends, including increasing female workforce participation and a rising elderly population, are boosting demand for feminine hygiene and adult incontinence products. Innovation and sustainability are shaping market dynamics in Asia Pacific. For example, Unicharm Corporation has introduced its MamyPoko diapers with ultra-absorbent cores, breathable fabrics, and eco-friendly materials in India and Southeast Asia, targeting both infant comfort and environmental concerns. Companies are leveraging online sales channels, subscription models, and digital marketing campaigns to enhance accessibility and build brand loyalty.

Competitive Landscape

The global disposable hygiene product market exhibits a moderately fragmented structure, driven by the presence of several well-established multinational corporations alongside numerous regional and local players competing across diverse product segments such as baby diapers, feminine hygiene, wipes, tissue products, and adult incontinence solutions. Major brands maintain strong positions through extensive distribution networks, broad product portfolios, and significant investments in research and development aimed at enhancing comfort, absorbency, and sustainability. Consumer preferences for premium, skin-friendly, and eco-conscious products have intensified competition, prompting continual product upgrades and marketing initiatives.

With key leaders including Procter & Gamble, Kimberly-Clark Corporation, Unicharm Corporation, Essity AB, Hengan International Group, Ontex Group NV, and Domtar Corporation, the competitive landscape features both scale and innovation rivalry. These players compete through differentiated product development, strategic partnerships, and geographic expansion to capture market share and address regional consumer preferences.

Key Industry Developments:

- In February 2026, Nobel Hygiene launched the biodegradable baby diaper, Teddyy Bio-Earth. Developed with Avgol and Polymateria Ltd, about 75% of the diaper’s weight was designed to biodegrade within two years under natural conditions, using cellulose-based absorbent core materials.

- In April 2025, Planet Smart introduced the bio-based super-absorbent polymer PlanetSorb, intended to replace conventional SAPs in disposable hygiene products. The company claimed the material could be manufactured on existing production lines while maintaining performance comparable to traditional polymers.

- In May 2025, Aquapak Polymers Ltd introduced the Hydropol water-soluble, non-toxic polymer to make disposable hygiene products more environmentally safe. The material replaces conventional plastics in products such as wet wipes and sanitary pads, allowing them to dissolve in wastewater without releasing microplastics or causing sewer blockages.

Companies Covered in Disposable Hygiene Product Market

- Procter & Gamble (P&G)

- Kimberly-Clark Corporation

- Essity AB

- Unicharm Corporation

- Ontex Group NV

- Domtar Corporation

- Kao Corporation

- Edgewell Personal Care Company

- Hengan International Group Co., Ltd.

- First Quality Enterprise

Frequently Asked Questions

The global disposable hygiene product market is projected to reach US$220.4 billion in 2026.

Rising hygiene awareness, increasing female workforce participation, aging populations, urbanization, and growing demand for convenient single-use products drive the disposable hygiene product market.

The disposable hygiene product market is expected to grow at a CAGR of 8.3% from 2026 to 2033.

Key market opportunities lie in sustainable and biodegradable product innovation, expansion of adult incontinence and post-surgical care segments, and the rapid growth of e-commerce and emerging market penetration.

Procter & Gamble (P&G), Kimberly-Clark Corporation, Essity AB, Unicharm Corporation, and Ontex Group NV are the leading players.