- Baby Care & Accessories

- Diaper Rash Cream Market

Diaper Rash Cream Market Size, Share, and Growth Forecast 2026 - 2033

Diaper Rash Cream Market by Category-1 (Organic, Conventional), by Category-2 (Infants, Adults), by Category-3 (Household, Hospitals and Clinics, Day Care), by Category-4 (Hypermarkets/Supermarkets, Specialty Retailers, Multi-brand Stores, Drug Stores and Pharmacies, Online Retailers, Others), by Regional Analysis, 2026 - 2033

Diaper Rash Cream Market Size and Trend Analysis

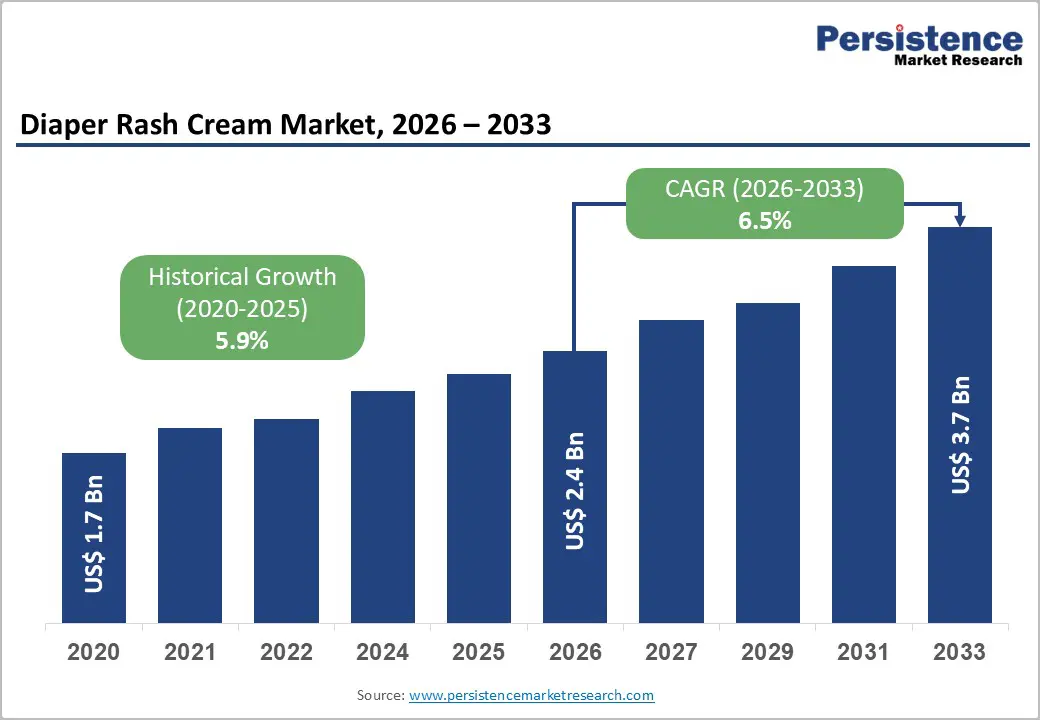

The global diaper rash cream market size is projected to be valued at US$ 2.4 billion in 2026 and is expected to reach US$ 3.7 billion by 2033, expanding at a CAGR of 6.5% during the forecast period.

Market growth is driven by sustained birth rates in emerging economies and by a growing elderly population in developed regions that requires incontinence care. The rising incidence of diaper dermatitis and incontinence-associated dermatitis is accelerating demand for effective skin protection solutions. Additionally, increasing consumer preference for preventive skin care, coupled with premiumization trends and demand for zinc oxide-based, dermatologist-tested formulations, is encouraging manufacturers to innovate advanced, breathable, and skin-friendly products.

Key Market highlights

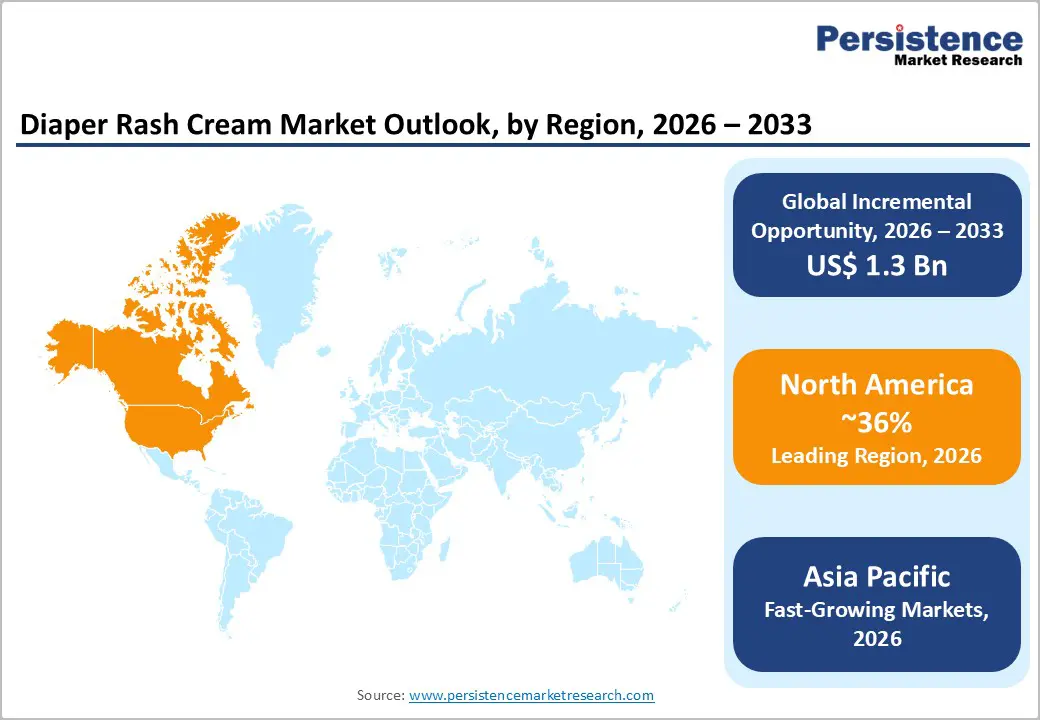

- Regional Leadership: North America holds approximately 36% share of the global Diaper Rash Cream Market, driven by high per-capita spending and a mature baby hygiene and adult incontinence care ecosystem.

- Fastest-Growing Region: Asia Pacific accounts for nearly 32% share and represents the fastest-growing regional market, supported by high birth rates, rising disposable incomes, and expanding brand awareness.

- Dominant End User: The Infants segment holds around 75% market share, reflecting universal diaper use and high application frequency during the first three years of life.

- Fastest-Growing Ingredient: Conventional formulations retain a leading 62% share, supported by zinc oxide and petrolatum-based products, while the Organic and plant-based segment is expanding rapidly and gaining traction.

- Key Market Opportunity: Developing specialized, high-efficacy barrier creams for the Geriatric/Adult Incontinence population represents a massive, untapped revenue pocket for future expansion.

| Key Insights | Details |

|---|---|

| Diaper Rash Cream Market Size (2026E) | US$ 2.4 Billion |

| Market Value Forecast (2033F) | US$ 3.7 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.5% |

| Historical Market Growth (2020 - 2025) | 5.9% |

Market Dynamics

Drivers - High Clinical Incidence of Diaper Dermatitis and Incontinence-Associated Skin Conditions Driving Sustained Demand

The diaper rash cream market is driven by the widespread clinical occurrence of skin conditions associated with prolonged diaper use across infant and adult populations. Diaper dermatitis remains among the most frequently reported dermatological conditions in infancy, particularly during early developmental stages that require frequent diaper changes. This persistent exposure to moisture and friction necessitates the routine, preventive use of barrier creams as part of daily hygiene.

In parallel, rising cases of incontinence-associated dermatitis among elderly and immobile patients are expanding demand within healthcare and long-term care settings. Hospitals and geriatric facilities increasingly rely on medically validated skin protectants to prevent complications, skin breakdown, and secondary infections. This clinical reliance creates a stable, non-discretionary consumption pattern, ensuring consistent product utilization and long-term revenue continuity for manufacturers.

Accelerating Consumer Shift Toward Organic, Clean-Label, and Ingredient-Safe Formulations

A pronounced shift toward organic and clean-label diaper rash creams is reshaping market dynamics, driven by heightened consumer awareness around ingredient safety. Modern parents are actively avoiding formulations containing parabens, synthetic fragrances, and harsh preservatives, favoring transparency and minimal ingredient lists. This scrutiny has transformed clean-label positioning from a value-add to a core purchasing requirement.

Natural emollients such as shea butter, calendula, beeswax, and plant-derived oils are increasingly preferred over petroleum-based alternatives. This trend is reinforced by advocacy groups and safety-focused organizations highlighting potential chemical exposure risks. As a result, brands offering certified organic, dermatologist-tested, and hypoallergenic formulations are gaining stronger shelf presence, enhanced consumer trust, and improved pricing leverage, collectively supporting premium market growth.

Restraints - Rising Consumer Skepticism Toward Chemical Additives and Increasing Skin Sensitivity Concerns

One of the key restraints on the diaper rash cream market is growing consumer skepticism about the chemical ingredients used in conventional formulations. Despite regulatory approvals, preservatives, synthetic fragrances, and petroleum derivatives are increasingly viewed with caution, especially by parents of infants with sensitive skin. Heightened access to ingredient information has amplified concerns around potential irritation and long-term exposure.

This skepticism often results in reduced product usage or substitution with perceived safer alternatives such as coconut oil, shea butter, or diaper-free time. As a result, established brands face a persistent trust gap rooted in historical reliance on chemical-heavy formulations. Overcoming this restraint requires not only reformulation but also transparent communication, clinical validation, and sustained consumer education to rebuild credibility and consumer confidence in use.

High Price Sensitivity and Strong Competition from Low-Cost and Multi-Purpose Alternatives

Price sensitivity remains a major limiting factor, particularly in emerging and price-conscious markets, where premium diaper-rash creams face adoption barriers. Organic, dermatologist-tested, and therapeutic products typically carry significantly higher price points compared to basic petroleum jelly or generic zinc oxide ointments, limiting affordability for large consumer segments.

In such regions, caregivers often opt for low-cost substitutes, including general moisturizers, antiseptic creams, or home remedies, rather than specialized diaper care products. Private-label offerings from large retailers provide functional alternatives at substantially lower prices. This widespread availability of economical substitutes intensifies market commoditization, compresses margins, and restricts volume growth for established branded manufacturers.

Opportunity - Strategic Expansion into Geriatric Care and Adult Incontinence Skin Protection Solutions

A major growth opportunity for the diaper-rash cream market lies in expanding beyond infant care into the rapidly growing geriatric and adult incontinence segments. Global aging trends and rising life expectancy are increasing the prevalence of incontinence associated with chronic illness, mobility limitations, and post-surgical recovery. Unlike infant care, this segment benefits from a steadily expanding user base driven by demographic aging rather than birth rates.

Manufacturers that successfully reposition diaper rash creams as dignified, medical-grade skin protectants for adults can unlock a largely underpenetrated market. Opportunities are particularly strong in home healthcare and long-term care environments, where caregiver-friendly application, odor control, and prolonged barrier protection are critical. Purpose-built packaging and stigma-free branding will further support adoption and premium positioning.

Product Innovation Through Microbiome-Friendly and Probiotic-Enhanced Skincare Formulations

Innovation centered on microbiome-friendly skincare presents a high-value opportunity for future market expansion. Emerging dermatological research underscores the importance of preserving the skin’s natural microbiome to strengthen barrier function and reduce irritation. This has created demand for advanced diaper-rash creams formulated with prebiotics, probiotics, or skin-conditioning bioactives that support microbial balance, rather than relying solely on physical moisture barriers.

Developing formulations enriched with probiotic ferments, panthenol, or regenerative actives allows brands to position products as therapeutic skin treatments. This “skinification” trend enables meaningful differentiation, supports ultra-premium pricing strategies, and appeals to consumers seeking long-term skin health benefits, thereby elevating both product value perception and brand equity.

Category-wise Analysis

Ingredient Insights

The conventional ingredient segment dominates the diaper rash cream market, accounting for approximately 62% of total revenue. This leadership is supported by the widespread use of clinically proven ingredients, such as zinc oxide and petrolatum, which pediatricians recommend for their effective moisture-barrier properties. Their affordability, mass-market availability, and long-standing consumer trust ensure strong penetration across pharmacies and supermarkets globally.

The Organic and clean-label ingredient segment is emerging as the fastest-growing category. Rising parental awareness around ingredient safety, combined with increasing scrutiny of synthetic additives, is accelerating demand for formulations containing plant-based emollients and non-nano zinc oxide. This shift reflects a broader consumer move toward preventive, skin-friendly, and transparency-driven personal care solutions.

End-user Insights

The Infants segment remains the dominant end-user category, holding approximately 75% of total market share. This is driven by the unavoidable and continuous need for diaper usage during the first few years of life, resulting in frequent product application and high consumption intensity. Parents’ strong emotional focus on infant comfort and skin health further reinforces consistent demand.

The Adults segment represents the fastest-growing end-user category. Aging populations, rising cases of mobility limitations, and increased prevalence of incontinence-related skin conditions are expanding demand beyond infant care. Growing acceptance of home healthcare and improved positioning of adult skin protection products are accelerating adoption across geriatric and assisted-care settings.

Application Insights

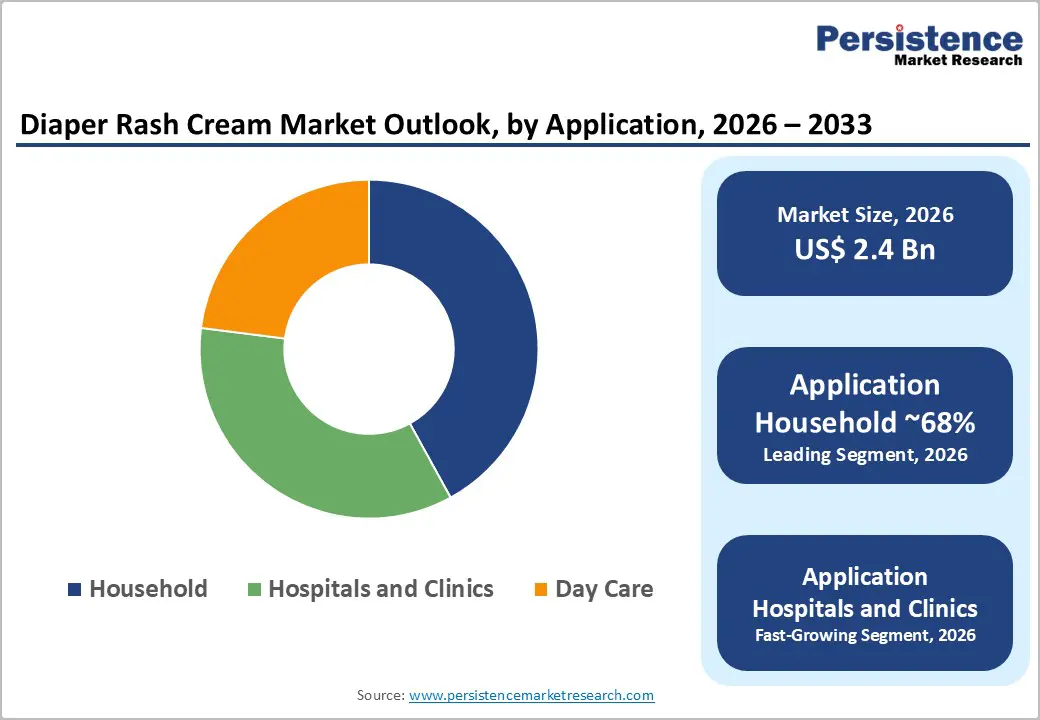

The Household application segment leads the market with an estimated share of 68%, as most diaper rash prevention and treatment occurs in home settings. Daily hygiene routines managed by parents and caregivers drive frequent product usage, while easy retail access through supermarkets and pharmacies sustains high household penetration.

The hospitals and clinics segment is the fastest-growing application area. Increased focus on preventive skin care in neonatal units, elderly care facilities, and post-acute settings is boosting institutional adoption. Clinical validation in healthcare environments also plays a critical role in influencing long-term consumer brand preferences after discharge.

Sales Channel Insights

Hypermarkets and supermarkets dominate the sales channel landscape, accounting for approximately 41% of the total market share. Their leadership is driven by high footfall, convenience-driven purchasing behavior, and extensive shelf presence for established baby care brands, enabling bundled purchases alongside diapers and related essentials.

Online retail is the fastest-growing sales channel, fueled by rising e-commerce adoption, subscription-based purchasing, and access to premium and niche brands. Digital platforms allow consumers to compare ingredients, read reviews, and access specialized formulations, accelerating the shift toward direct-to-consumer and online-first purchasing models.

Regional Insights

North America Diaper Rash Cream Market Trends

North America accounts for approximately 36% of the global diaper rash cream market, led by the United States’ high per-capita spending and well-developed retail and healthcare infrastructure. The region is strongly shaped by clean-label and safety-driven purchasing behavior, with parents prioritizing dermatologist-tested, fragrance-free, and third-party certified products. Established players have responded by reformulating and upgrading their portfolios to align with evolving safety perceptions.

Beyond infant care, North America shows strong traction in the adult incontinence segment, driven by insurance-backed long-term care facilities and the adoption of home healthcare. The region also serves as an innovation hub, where niche and premium brands focused on sustainability, plant-based ingredients, and transparent labeling continue to influence global product trends.

Europe Diaper Rash Cream Market Trends

Europe represents a mature and regulation-intensive market, projected to grow at a CAGR of approximately 5.8% during the forecast period. Stringent European Union cosmetic regulations significantly influence product formulation, favoring dermatologically approved and ingredient-compliant solutions. Countries such as Germany, France, and the U.K. lead demand for pharmacy-grade and organic diaper care products.

A defining characteristic of the region is strong consumer reliance on apothecaries and drugstores for baby skincare purchases, reinforcing trust in clinically positioned brands. Additionally, Europe’s rapidly aging population is driving increased demand for incontinence-related skin protection, prompting manufacturers to expand geriatric-focused and medically positioned product lines.

Asia Pacific Diaper Rash Cream Market Trends

Asia Pacific holds an estimated 32% share of the global market and represents the fastest-expanding regional opportunity. Growth is underpinned by high birth volumes in China and India, alongside rising disposable incomes, which are accelerating the shift from traditional home remedies to branded diaper-rash creams. Premiumization is particularly evident among urban middle-class households.

The region is also witnessing intensifying competition between international and domestic brands, with local players leveraging herbal and culturally familiar ingredients. The rapid expansion of e-commerce platforms has significantly improved product accessibility in tier-2 cities and rural areas, enabling deeper market penetration and sustained volume growth beyond metropolitan centers.

Competitive Landscape

The Diaper Rash Cream Market exhibits a moderately consolidated competitive structure, with a limited number of large multinational players accounting for a significant share of global revenues. These companies benefit from extensive research capabilities, established brand equity, and wide-reaching distribution networks, enabling consistent product availability and strong consumer recall across mass retail and pharmacy channels.

The competitive environment is becoming increasingly fragmented due to the rise of independent and direct-to-consumer brands focused on organic, clean-label, and niche positioning. Competition is shifting toward transparency, ingredient traceability, and third-party certifications as trust becomes a core differentiator. Larger players are responding through strategic acquisitions and portfolio diversification to strengthen credibility in premium and natural segments.

Key Market Developments:

- In November 2025, Johnson & Johnson announced a major brand refresh titled "It's Pure Love," introducing updated, doctor-tested formulations enriched with aloe and Vitamin B5 to better protect baby skin in varying climates.

- In July 2025, The Honest Company launched its new and improved "Clean Conscious Diapers" and associated care products, featuring enhanced breathable layers designed to minimize moisture-related skin irritation.

- In October 2024, Bayer AG officially launched its globally recognized Bepanthen skincare brand in India, backed by a survey revealing a high prevalence of dry skin conditions among the Indian population.

Companies Covered in Diaper Rash Cream Market

- Johnson & Johnson

- Bayer AG

- Beiersdorf AG

- Procter & Gamble

- Unilever

- Himalaya Wellness

- Weleda AG

- Laboratoires Expanscience (Mustela)

- The Honest Company

- Burt’s Bees

- Sebapharma

- Summer Laboratories

- Pigeon Corporation

- Artsana Group (Chicco)

- Earth Mama Organics

Frequently Asked Questions

The global market is forecast to reach a valuation of US$ 3.7 Billion by the end of 2033, expanding from US$ 2.4 Billion in 2026.

Demand is driven by the high prevalence of diaper dermatitis among infants, who account for nearly 75% of total consumption, along with rising cases of incontinence-associated dermatitis in the elderly population and increasing preference for preventive skin protection products.

The Conventional ingredient segment dominates with approximately 62% share, supported by the affordability and widespread use of zinc oxide and petrolatum-based formulations, while organic and plant-based products are gaining momentum.

North America leads the market with around 36% share, supported by high disposable incomes, advanced retail infrastructure, and strong adoption of both infant and adult incontinence skincare products.

A major opportunity lies in targeting the expanding adult incontinence care segment, alongside innovation in clean-label, microbiome-friendly formulations to capture premium demand.

Major players include Johnson & Johnson, Bayer AG, Beiersdorf AG, Procter & Gamble, Weleda AG, and The Honest Company, among others.