- Baby Care & Accessories

- Baby Diaper Market

Baby Diaper Market Size, Share, and Growth Forecast, 2025 - 2032

Baby Diaper Market By Product Type (Disposable Diapers, Reusable/Cloth Diapers, Others), Style (Tape Diapers, Pant-Style Diapers (Pull-Ups)), Age Group (Preemie, Newborn, Others), Distribution Channel (Supermarket/Hypermarket, Others), and Regional Analysis for 2025 - 2032

Baby Diaper Market Size and Trends Analysis

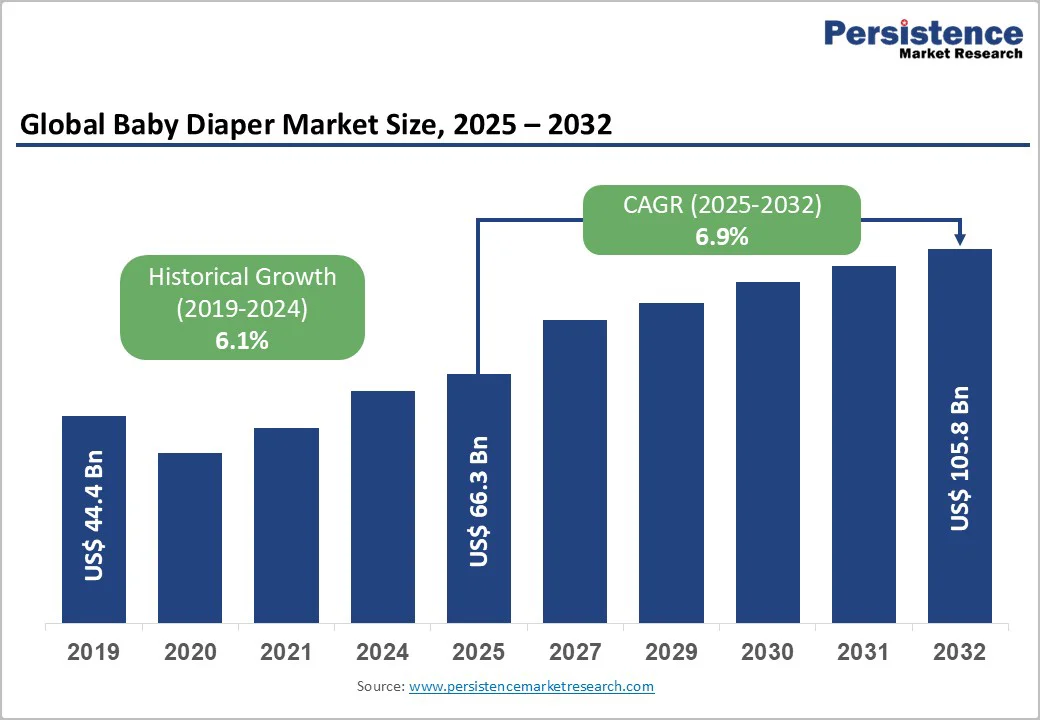

The global baby diaper market is expected to reach US$66.3 billion in 2025. It is expected to reach US$105.8 billion by 2032, growing at a CAGR of 6.9% during the forecast period from 2025 to 2032, driven by rising birth rates in developing regions, higher disposable incomes, and increasing awareness of infant hygiene. Rapid urbanization and expanding female workforce participation have boosted demand for convenient disposable solutions.

According to the Periodic Labour Force Survey, India’s working women ratio rose from 22% in 2017–18 to 40.3% in 2023–24. Innovations in superabsorbent polymers and skin-friendly materials further enhance product performance and adoption globally.

Key Market Highlights

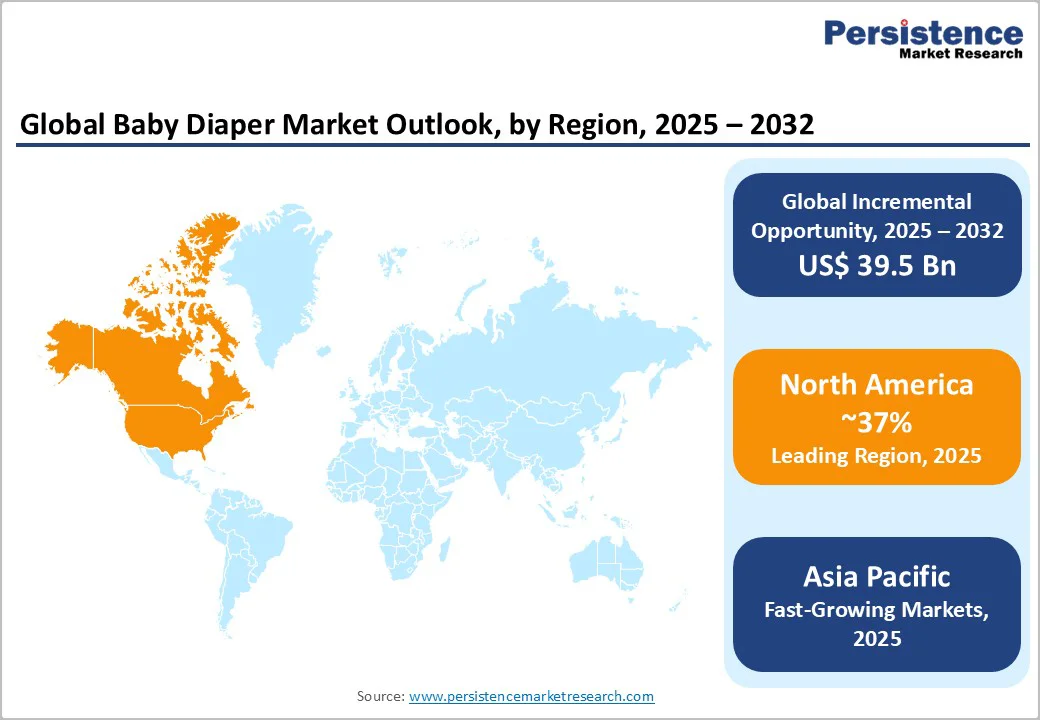

- Leading Region: North America dominates the baby diaper market, holding about 37% share, driven by strong consumer spending power, high brand loyalty, and increasing demand for eco-friendly, premium-quality diapers.

- Fastest Growing Region: Asia Pacific is the fastest-growing market, accounting for nearly 33% share, fueled by high birth rates, rapid urbanization, and rising disposable incomes in countries such as China, India, and Indonesia.

- Dominant Segment: Disposable diapers lead globally with about 65% share, driven by SAP innovation and consumer preference for convenience, especially in urban areas.

- Fastest-growing Segment: Pant-style (pull-up) diapers are expanding rapidly, especially among toddlers and urban households, with adoption rates exceeding 80% in major Asian markets.

- Key Market Opportunity: E-commerce and subscription-based distribution models are emerging as major growth drivers, offering convenience, personalization, and direct brand engagement for digitally active parents.

| Key Insights | Details |

|---|---|

|

Baby Diaper Market Size (2025E) |

US$66.3 Bn |

|

Market Value Forecast (2032F) |

US$105.8 Bn |

|

Projected Growth CAGR (2025-2032) |

6.9% |

|

Historical Market Growth (2019-2024) |

6.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Birth Rates in Emerging Economies Fueling Demand Expansion

The market is experiencing steady growth due to rising birth rates in developing economies across Asia and Africa. Sub-Saharan Africa alone contributed nearly 29% of global births in 2021 and is expected to account for more than half by 2100. Nations such as Niger, Chad, and the Democratic Republic of Congo record fertility rates exceeding five children per woman, creating sustained demand for baby care products. Simultaneously, countries such as India and Indonesia are experiencing stable population growth, boosting demand for infant hygiene solutions.

Government-backed pronatalist initiatives are further driving diaper demand. For example, Hong Kong’s US$20,000 newborn incentive and China’s three-child policy aim to counter declining fertility. Improved healthcare access, rising disposable incomes, and growing urban populations are amplifying the market potential for global and regional diaper manufacturers.

Growing Female Workforce Participation Driving Convenience-Oriented Product Adoption

Increasing female workforce participation is a key catalyst for the adoption of convenient, disposable baby diapers. As more women join formal employment sectors, the need for time-saving and hygienic childcare products has intensified. In India, female labor participation surged from 22% in 2017–18 to 40.3% in 2023–24, reflecting a profound societal shift toward dual-income households and modern parenting lifestyles.

Urbanization and changing family dynamics further reinforce this transition. In China, over 70% of parents now prefer disposable diapers for their ease of use and reliability. Rising living standards and awareness of baby hygiene are encouraging parents to shift from cloth nappies to premium, eco-friendly disposable alternatives. Consequently, convenience, comfort, and skin-friendly innovations are shaping purchasing behavior in both developed and emerging markets.

Barrier Analysis - Environmental Concerns and Sustainability Challenges Limiting Market Growth

The baby diaper market faces mounting sustainability challenges due to the enormous environmental footprint of disposable diapers. Over 200 billion diapers are discarded worldwide each year, contributing millions of tons of non-biodegradable waste. In the U.S. alone, nearly 20 billion disposable diapers generate around 3.75 million tons of landfill waste annually, while in India, more than 12 billion are used and discarded each year. Traditional diaper materials can take up to 500 years to decompose, releasing methane and other greenhouse gases in the process.

With regulations such as the European Union’s Deforestation-Free Regulation (EUDR) coming into effect in 2025, manufacturers are under pressure to ensure ethical sourcing of tree-based fibers and sustainable production. This growing regulatory and environmental scrutiny is accelerating the shift toward biodegradable, compostable, and reusable diaper alternatives, challenging the growth of conventional disposable diapers.

Price Sensitivity and Affordability Barriers in Emerging Markets

Affordability remains a major constraint restricting widespread adoption of baby diapers in low- and middle-income regions. Premium products featuring biodegradable materials, organic fabrics, and advanced absorbent technologies often carry higher price tags, putting them beyond the reach of many families in emerging economies. In Sub-Saharan Africa and South Asia, where disposable income levels remain limited, parents continue to rely on traditional cloth nappies as a cost-effective solution.

Volatility in raw material prices, especially for super absorbent polymers (SAPs) and pulp, further intensifies this challenge. Inflationary pressures and limited local manufacturing capacity can raise diaper prices, discouraging consistent use. Consequently, cost sensitivity in developing nations continues to hinder deep market penetration, compelling manufacturers to balance innovation with affordability through localized production and tiered product strategies.

Opportunity Analysis - Expanding E-commerce and Subscription-Based Distribution Models

The rapid expansion of digital retail channels is opening new opportunities for baby diaper manufacturers worldwide. E-commerce platforms now play a central role in product distribution, enabling brands to reach consumers directly and efficiently. The growing popularity of online shopping, especially among tech-savvy and urban parents, has led to strong growth in online diaper sales. Subscription-based models offering doorstep delivery, flexible purchase plans, and automated refills are gaining traction among working parents seeking convenience and cost efficiency.

Direct-to-consumer brands are increasingly leveraging digital marketing, influencer partnerships, and personalized engagement strategies to build strong brand loyalty. These online and subscription-driven models not only improve accessibility but also allow manufacturers to gather valuable consumer insights, optimize inventory, and expand market share across both developed and emerging regions.

Innovation in Sustainable and Biodegradable Diaper Technologies

Rising environmental awareness is creating strong opportunities for innovation in eco-friendly diaper solutions. Manufacturers are increasingly focusing on biodegradable, compostable, and hybrid products that reduce environmental impact while maintaining performance standards. Materials such as bamboo fiber, corn starch-based biopolymers, organic cotton, and biodegradable super absorbent polymers are gaining prominence as sustainable alternatives to conventional plastics.

In regions such as Europe and North America, stringent environmental regulations and consumer demand for ethical products are accelerating the adoption of green diaper technologies. Companies investing in recyclable packaging, plant-based components, and carbon-neutral manufacturing processes are well-positioned to capture environmentally conscious consumers. This growing shift toward sustainable product innovation is expected to redefine long-term market competitiveness.

Category-wise Analysis

Product Type Insights

Disposable diapers dominate the global market, holding around 65% share in 2025, driven by their unmatched convenience, superior absorbency, and comfort-enhancing designs. They account for over 85% of total diaper sales worldwide. Technological advancements in super absorbent polymers (SAPs), along with innovations such as ultra-thin, breathable, and hypoallergenic materials, continue to strengthen the appeal of disposable diapers among modern parents seeking hygiene and reliability.

The reusable or cloth diaper segment is emerging as the fastest-growing category. Increasing environmental awareness, rising adoption of sustainable materials such as organic cotton and bamboo, and supportive government initiatives promoting eco-friendly products are fueling this segment’s expansion. Modern reusable diapers with adjustable fittings and leak-proof layers are helping bridge the gap between convenience and sustainability.

Style Insights

Pant-style diapers lead the market with about 60% share in 2025, favored for their easy pull-up design and superior comfort for toddlers and active babies. In fast-growing urban markets, including China, India, and Southeast Asia, adoption exceeds 80% due to convenience in changing and enhanced mobility. Their ergonomic design and soft waistbands make them the preferred choice for both babies and caregivers.

The tape-style segment, though traditional, is expected to grow steadily as manufacturers innovate to improve fit and skin comfort for newborns. Enhanced adhesive strength, stretchable sides, and gentler materials are making tape-style diapers more appealing for infant use. The segment also benefits from affordability and hospital distribution channels, ensuring continued relevance despite market shifts toward pant-style options.

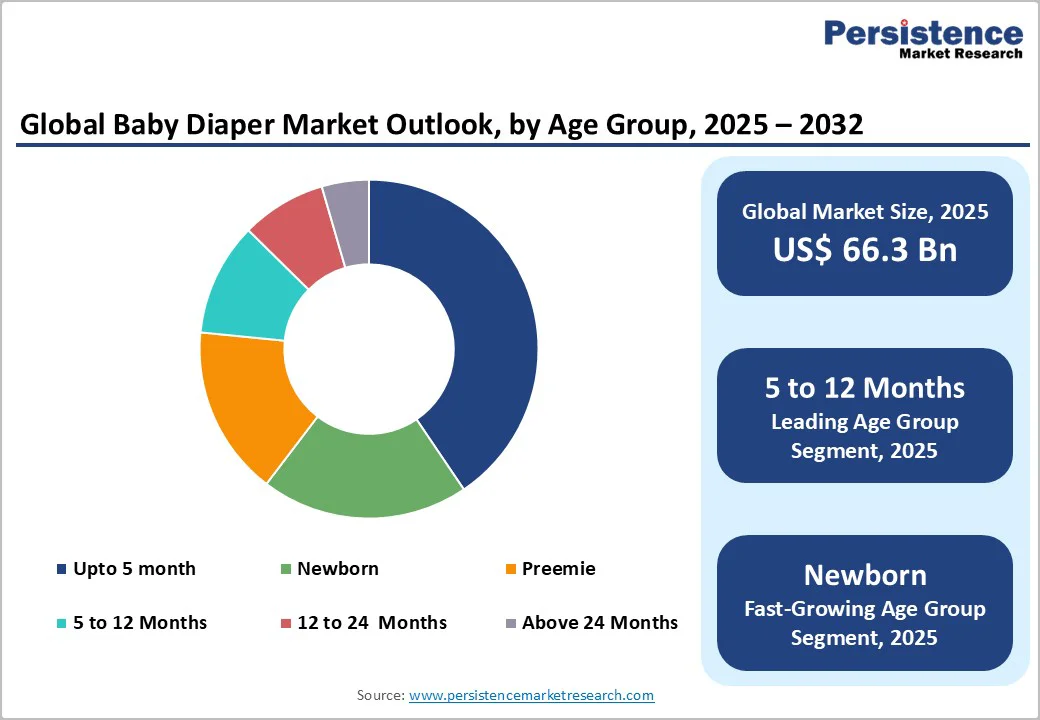

Age Group Insights

The 5- to 12-month age group holds the largest share, around 30%, of the baby diaper market. This dominance is attributed to the high frequency of diaper changes during this active growth phase, where mobility increases, and comfort becomes a top priority. Parents in this category prefer premium, ultra-absorbent, and leak-proof pant-style diapers, ensuring dryness and convenience for longer durations.

The newborn category is the fastest-growing segment, driven by rising hospital births, improved neonatal care, and growing hygiene awareness among new parents. Manufacturers are introducing ultra-soft, breathable, and hypoallergenic diapers tailored for newborns’ sensitive skin, often distributed through hospital and maternity partnerships that enhance brand recognition from birth.

Distribution Channel Insights

Supermarkets and hypermarkets lead global diaper distribution, accounting for roughly 50% of sales. Their dominance stems from extensive product assortments, promotional discounts, and the convenience of bulk purchasing. Strategic shelf placement and cross-category promotions within baby care sections further enhance brand visibility and consumer engagement, sustaining strong retail performance.

E-commerce represents the fastest-growing channel, expanding rapidly as digital retail ecosystems mature. Online platforms and subscription-based services appeal to busy parents through doorstep delivery, competitive pricing, and personalized purchase plans. Direct-to-consumer brands are leveraging social media marketing and targeted campaigns to attract new customers, making digital distribution a critical growth frontier for diaper manufacturers.

Regional Insights

North America Baby Diaper Market Trends

North America is the leading regional market, commanding around 37% of the global baby diaper sales. High consumer spending power, brand loyalty, and demand for premium-quality diapers continue to sustain regional dominance. Parents increasingly prefer eco-friendly, hypoallergenic, and dermatologically tested products, driven by growing awareness of ingredient safety and sustainability. Established brands emphasize innovation in absorbent technology, softness, and breathability, aligning with consumer expectations for comfort and performance.

Tightening environmental regulations and ingredient transparency requirements are reshaping product portfolios. Manufacturers are transitioning toward biodegradable components, recyclable packaging, and sustainable production methods. These factors, combined with consistent product innovation and mature retail infrastructure, reinforce North America’s leadership in the global baby diaper landscape.

Europe Baby Diaper Market Trends

Europe represents a highly regulated and sustainability-focused market through the forecast period. Countries such as Germany, France, the U.K., and Spain drive regional demand, supported by a growing preference for biodegradable, organic, and chemical-free diaper products. The EU Ecolabel and Deforestation-Free Regulation (EUDR) are compelling producers to adopt eco-friendly materials and ensure transparent supply chains.

European consumers increasingly favor subscription-based and online diaper delivery models for convenience and cost efficiency. Heightened regulatory scrutiny, combined with consumer awareness, continues to steer innovation toward sustainability, solidifying Europe’s role as a benchmark for green diaper manufacturing practices worldwide.

Asia Pacific Baby Diaper Market Trends

Asia Pacific is the fastest-growing region, accounting for nearly 33% of the global market share. The region’s growth is powered by high birth rates, rapid urbanization, and increasing disposable incomes. With over 60% of the world’s infant population, countries such as China, India, and Indonesia are key consumption hubs. In China, diaper penetration exceeds 70% in cities, while India’s market continues expanding as awareness of hygiene and convenience grows among new parents.

Local innovation, competitive pricing, and expanding e-commerce access are accelerating adoption across both urban and semi-urban areas. Leading brands such as Unicharm and Kao leverage regional manufacturing and tailored marketing strategies to meet consumer needs. As sustainable and premium diaper options gain popularity, the Asia Pacific region remains the strongest engine of global market expansion.

Competitive Landscape

The global baby diaper market is moderately consolidated, with a few major multinational players dominating overall sales through strong brand recognition, large-scale production, and continuous product innovation. These leading companies leverage advanced materials, high-performance absorbent technologies, and robust marketing networks to maintain competitive positioning across diverse regional markets.

Emerging regional and direct-to-consumer brands are disrupting the landscape by targeting eco-conscious and digitally active consumers. Innovation in biodegradable materials, smart sensor-integrated diapers, and sustainable packaging, combined with strong online distribution and subscription-based models, is intensifying competition and reshaping long-term market dynamics.

Key Industry Developments

- In January 2025, Unicharm India launched the #HarBabyKaPehlaDiaper campaign to connect with new-age mothers through digital platforms and influencer marketing. The initiative highlighted MamyPoko Pants’ superior absorption, long-lasting dryness, and gentle skin protection, reinforcing the brand’s trust among modern, health-conscious parents.

- In February 2025, Ontex Group introduced Dreamshields technology diapers across Europe, offering advanced leakage protection, improved comfort, and a reduced carbon footprint. The product emphasizes sustainability through eco-friendly materials and manufacturing processes, aligning with Europe’s growing demand for environmentally responsible baby care solutions.

- In January 2024, Procter & Gamble expanded its premium product line with Pampers Premium Care Diapers, enriched with anti-rash properties and aloe vera lotion. Designed for sensitive baby skin, these diapers enhance softness, breathability, and all-day protection for improved infant comfort and hygiene.

Companies Covered in Baby Diaper Market

- The Procter & Gamble Company (P&G)

- Kimberly-Clark Corporation

- Hengan International

- Unicharm Corporation

- Johnson & Johnson

- First Quality Enterprises

- Ontex Group

- The Hain Celestial Group Inc

- The Honest Company, Inc.

- Essity AB

- Kao Corporation

- Bambo Nature USA

- Paul Hartmann AG

- Bambina Mio Ltd.

- Daio Paper Corporation

- Domtar Corporation

- Svenska Cellulosa Aktiebolaget (SCA)

- Nobel Hygiene

- Wipro Enterprises Private Limited

Frequently Asked Questions

The baby diaper market is projected to reach US$105.8 Billion by 2032, growing at a CAGR of 6.9% from 2025 to 2032.

Market growth is driven by rising birth rates, expanding female workforce participation, and technological innovation in absorbent and skin-friendly materials.

Disposable diapers dominate the market with about a 65% share, owing to superior convenience, absorbency, and hygiene features.

Asia Pacific is the fastest-growing region, supported by high birth rates, urbanization, and rising disposable incomes.

Key opportunities lie in e-commerce expansion, subscription-based models, and innovation in biodegradable and eco-friendly diapers.

Major players include The Procter & Gamble Company (Pampers), Kimberly-Clark Corporation (Huggies), Unicharm Corporation (MamyPoko), Hengan International, Kao Corporation, and Essity AB.