- Biotechnology

- Clinical Chemistry Market

Clinical Chemistry Market Size, Share, and Growth Forecast 2026 - 2033

Clinical Chemistry Market by Product Type (Clinical Chemistry Analysers, Poc Test Kits, Clinical Chemistry Reagents), by End User (Hospital, Pathology Laboratories, Clinics, Outpatient Centres, Maternity Centres), by Regional Analysis, 2026-2033

Clinical Chemistry Market Size and Trend Analysis

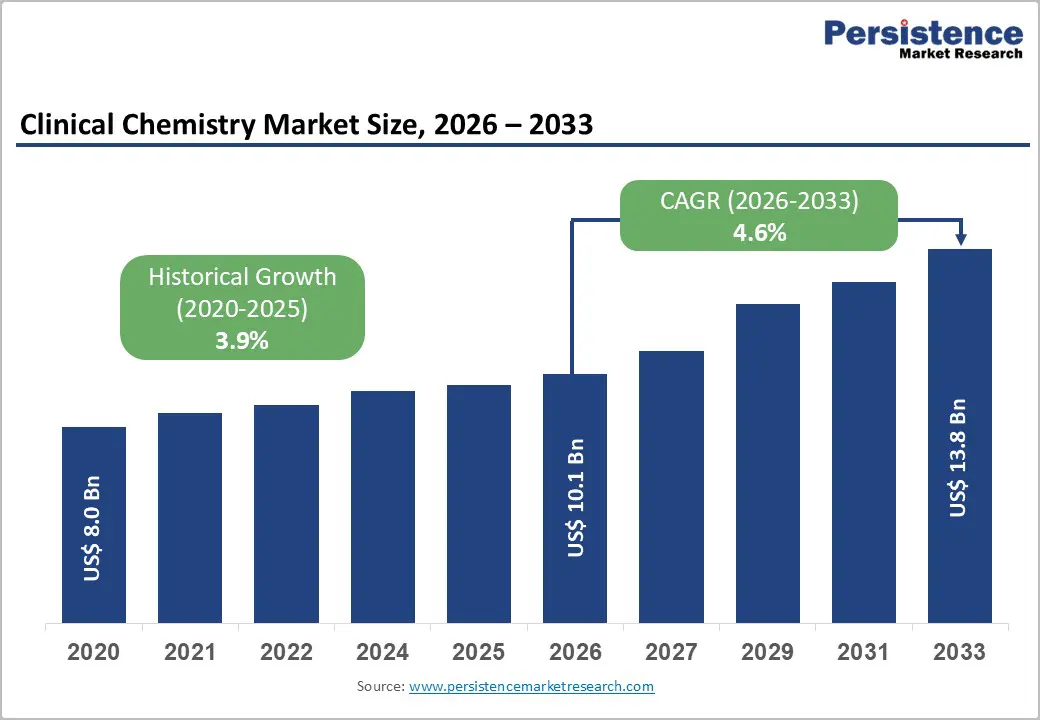

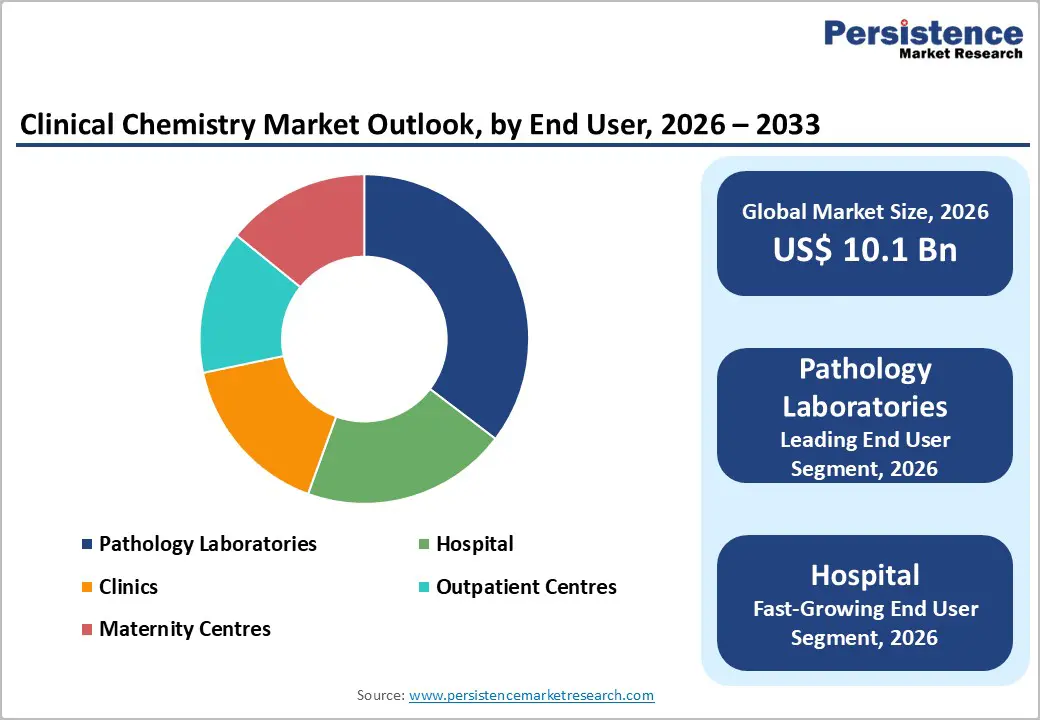

The global clinical chemistry market size is expected to be valued at US$ 10.1 billion in 2026 and is projected to reach US$ 13.8 billion by 2033, growing at a CAGR of 4.6% between 2026 and 2033.

Escalating prevalence of chronic diseases like diabetes and cardiovascular conditions drives this expansion, with CDC estimating 129 million U.S. adults affected by at least one major chronic illness. Advancements in automated analyzers and POC testing enhance diagnostic efficiency, supported by rising healthcare spending and early detection initiatives. WHO highlights global CVD burden, necessitating frequent chemistry panels.

Key Market highlights

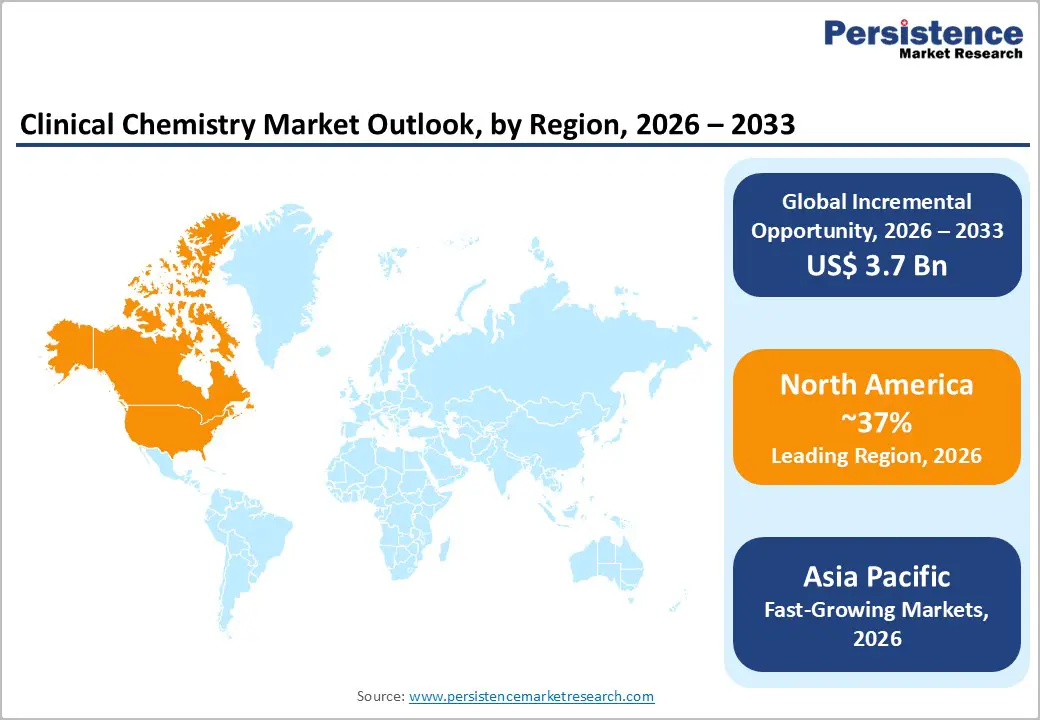

- North America dominates the clinical chemistry market, supported by advanced laboratory infrastructure, high testing volumes, favorable reimbursement policies, and rapid automation adoption.

- Asia Pacific is the fastest-growing region, driven by expanding hospital networks, rising chronic disease burden, national screening programs, and increasing healthcare investments.

- Clinical chemistry reagents account for the largest product share due to recurring consumption in routine metabolic, lipid, renal, and electrolyte testing across care settings.

- High-throughput automated analyzers and digital laboratory systems represent the fastest-growing technology segment, driven by workforce shortages, laboratory consolidation, and efficiency demands.

| Key Insights | Details |

|---|---|

| Clinical Chemistry Market Size (2026E) | US$ 10.1 Bn |

| Market Value Forecast (2033F) | US$ 13.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.9% |

Market Dynamics

Driver: Increasing elderly population and an increase in the incidences of chronic disorders.

The increasing elderly population will drive the clinical chemistry market going forward due to the increasing incidences of age-related disorders such as hypertension, diabetes, cardiovascular, liver, and kidney problems. As the prevalence of chronic diseases rises, the demand for tests used in their diagnosis and treatment is also increasing significantly. These factors, along with the rising preventive care, are expected to drive the growth of the clinical chemistry market throughout the forecast period.

Increasing adoption of Point of Care Testing Kits (POCT) and Analyzers

Point-of-care testing is useful for detecting analytes for improved diagnosis, treatment, and monitoring. It allows for the diagnosis of illnesses at an early stage. The increasing adoption of POCT kits and analyzers for the detection and treatment of diseases is one of the major factors driving the growth of the Clinical Chemistry Market.

Increasing adoption of fully automated clinical chemistry systems

Many healthcare institutions around the world are acquiring the fully automated clinical chemistry systems with built-in quality-assurance capabilities. These fully automated systems can process many samples at a time and can also perform tasks like tube sampling, cap piercing, dilution, and much more. The increasing adoption of these systems is fostering improved healthcare diagnostic facilities, and it is also expected to drive the growth of the Clinical Chemistry Market throughout the forecast period.

Restraint: High Capital Investments and Lack of Skilled Professionals

Due to the requirement of high capital investments, only big hospitals and labs with a huge capital budget can acquire the clinical chemistry analyzers. Many small laboratories and sole practitioners cannot afford these analyzers due to the high-cost requirements. As such, the requirement for high capital investments is one of the major restraints to the growth of the global clinical chemistry market.

Another factor that can hinder market growth is the lack of skilled professionals in both - developed and emerging nations. There is a global scarcity of lab technicians due to the rising patient population and a small number of fresh graduates due to the low availability of clinical lab programs. The lack of skilled pathologists and lab technicians is projected to stifle market growth.

Opportunity: Expansion in Hospital Settings

Hospitals are emerging as the fastest-growing end-user segment within the clinical chemistry market, driven by increasing patient admissions linked to cardiovascular disease, diabetes, kidney disorders, and aging populations. The growing need for rapid diagnostic decision-making in emergency rooms, intensive care units, and inpatient wards is accelerating adoption of integrated chemistry analyzers and high throughput testing platforms. Large-scale infrastructure programs are further strengthening demand; for example, the U.K.’s New Hospital Programme aims to deliver dozens of new and refurbished facilities by 2030, expanding laboratory capacity and routine testing volumes. Similar public-sector investments across Europe and Asia are supporting modernization of hospital laboratories and replacement of legacy equipment.

To manage rising sample loads efficiently, hospitals are prioritizing automated workflow solutions, track-based systems, and consolidated analyzers that reduce turnaround time while maintaining accuracy. Integration with electronic medical records and centralized laboratory networks is improving operational efficiency and clinician access to results. These trends create sustained opportunities for manufacturers supplying scalable instruments, reagents, and service contracts tailored to high-volume hospital environments.

Category-wise Insights

Product Type Analysis

Clinical chemistry reagents continue to represent the largest product category, capturing roughly 57% of market revenues in recent years because of their indispensable role in routine, high-volume diagnostic testing. Electrolyte panels, liver function tests,lipid profiles, renal markers, and glucose assays are performed daily across hospitals and laboratories, creating sustained demand for consumables that must be replenished continuously. Their recurring-use nature makes reagents a predictable revenue stream compared with capital equipment, especially when proprietary formulations are optimized for specific automated analyzer platforms. Laboratories favor validated reagent systems that deliver consistent performance, short turnaround times, and minimal calibration variability, particularly in large, centralized facilities processing thousands of samples daily.

The global rise in chronic disorders such as diabetes, cardiovascular disease, and kidney dysfunction further amplifies routine chemistry testing volumes, reinforcing reagent dominance. Ongoing innovation in assay stability, shelf life, multiplexing capability, and sensitivity is strengthening this segment’s leadership while supporting standardized metabolic panels across diverse healthcare settings.

End User Analysis

Pathology laboratories account for about 35% of the clinical chemistry market in 2025, reflecting their central role in high-complexity diagnostic workflows and population-scale screening programs. These facilities are typically equipped with advanced automation systems, high-throughput analyzers, and rigorous quality-control frameworks, enabling accurate and reproducible testing across broad menus that include metabolic panels, cardiac markers, tumor indicators, and endocrine assays. Hospitals and physician networks increasingly outsource specialized or large-volume testing to accredited pathology labs to manage capacity constraints while maintaining regulatory compliance. Their strong adoption of in vitro diagnostics platforms and data-management systems also supports standardized reporting and epidemiological monitoring. Rising screening initiatives for chronic diseases and oncology, coupled with preventive health programs, continue to shift testing volumes toward centralized laboratory networks. As a result, pathology laboratories remain a critical demand center for reagents, service contracts, and next-generation chemistry analyzers

Regional Insights

North America Clinical Chemistry Market Trends and Insights

North America remains one of the most established clinical chemistry markets, supported by advanced healthcare infrastructure, high diagnostic test volumes, and strong adoption of automated laboratory systems. The United States accounts for most regional demand, driven by widespread chronic disease prevalence, preventive screening programs, and well-developed hospital laboratory networks. Laboratories increasingly invest in high-throughput analyzers, integrated tracks, and digital connectivity to improve turnaround times and workforce efficiency. Replacement demand for aging instruments and expansion of outpatient diagnostic centers further sustain market momentum. In addition, reimbursement systems and regulatory frameworks encourage the use of standardized chemistry panels for cardiovascular, renal, and metabolic disorders, supporting consistent reagent consumption.

Looking forward, the region continues to focus on laboratory consolidation and precision medicine initiatives, which are driving purchases of advanced analyzers and specialized assays. Growing home-based testing referrals, centralized laboratory hubs, and partnerships between hospital networks and diagnostic service providers are shaping future demand, reinforcing North America’s stable yet innovation-driven growth profile.

Asia Pacific Clinical Chemistry Market Trends and Insights

Asia Pacific represents the fastest-expanding region in the clinical chemistry market, propelled by rapid healthcare infrastructure development, rising diagnostic awareness, and expanding access to routine laboratory testing. Countries such as China, India, Japan, and South Korea are investing heavily in hospital construction, laboratory modernization, and national screening programs for diabetes, cardiovascular disorders, and kidney disease. Urbanization and aging populations are increasing outpatient and inpatient testing volumes, while public insurance expansion in several markets is improving affordability of diagnostic services.

Manufacturers are responding with locally produced analyzers and reagent kits tailored to regional price sensitivities, supporting broader penetration beyond major metropolitan centers. Growth of private diagnostic chains and reference laboratories is further centralizing testing volumes and accelerating automation adoption. Cross-border partnerships, technology transfers, and government-backed healthcare initiatives continue to reshape the competitive landscape, positioning Asia Pacific as a long-term engine of demand for clinical chemistry instruments, consumables, and service contracts.

Competitive Landscape

Market Structure Analysis

The global clinical chemistry market is moderately consolidated, with a limited number of multinational players accounting for a significant share of revenues. These companies increasingly pursue mergers, acquisitions, and strategic alliances to strengthen technology capabilities, broaden assay menus, and expand geographic reach. Alongside inorganic growth, manufacturers invest heavily in organic strategies such as new product launches, automation upgrades, and digital laboratory solutions to enhance competitiveness. Portfolio expansion into integrated analyzer systems, high-throughput platforms, and specialized reagents remain a priority. Partnerships with hospital networks, reference laboratories, and regional distributors further support market penetration, enabling leading firms to defend market share while capturing emerging opportunities across developing healthcare markets.?

Key Market Developments

- In May 2023, Siemens Healthineers announced the launch of two new high-volume hematology testing systems: the Atellica HEMA 570 Analyzer and the Atellica HEMA 580 Analyzer.

Companies Covered in Clinical Chemistry Market

- Danaher corporation

- Abbott

- F. Hoffmann-La Roche Ltd

- Siemens AG

- Thermo Fisher Scientific Inc.

- bioMérieux SA

- Bio-Rad Laboratories Inc.

- Cardinal Health, Inc.

- Mindray Medical International Limited

- Hitachi, Ltd.

- Hologic Inc.

- Others

Frequently Asked Questions

The global clinical chemistry market is valued at US$ 10.1 billion in 2026.

Rising chronic diseases, aging populations, preventive screening programs, automation adoption, laboratory consolidation, outpatient testing growth, and reimbursement support worldwide.

North America leads with 37% share in 2025.

Hospital expansion, emerging-market penetration, reagent rental models, digital connectivity, AI-driven workflows, point-of-care chemistry, and subscription service contracts.

Leaders include Danaher corporation, Abbott, F. Hoffmann-La Roche Ltd, iemens AG, and Thermo Fisher Scientific Inc.