- Healthcare Services

- Clinical Trial Imaging Market

Clinical Trial Imaging Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Clinical Trial Imaging Market by Offering (Services, Software, and Hardware), by Modality (Computed Tomography (CT), Magnetic Resonance Imaging (MRI), Positron Emission Tomography (PET), Ultrasound, and Others), Therapeutic Area (Oncology, Neurology, Cardiovascular Diseases, Infectious Diseases, Endocrinology, and Others) End-user (Pharmaceutical & Biotechnology Companies, Contract Research Organizations (CROs), Medical Device Manufacturers, Academic & Government Research Institutes, and Others), and Regional Analysis from 2026 - 2033

Clinical Trial Imaging Market Share and Trend Analysis

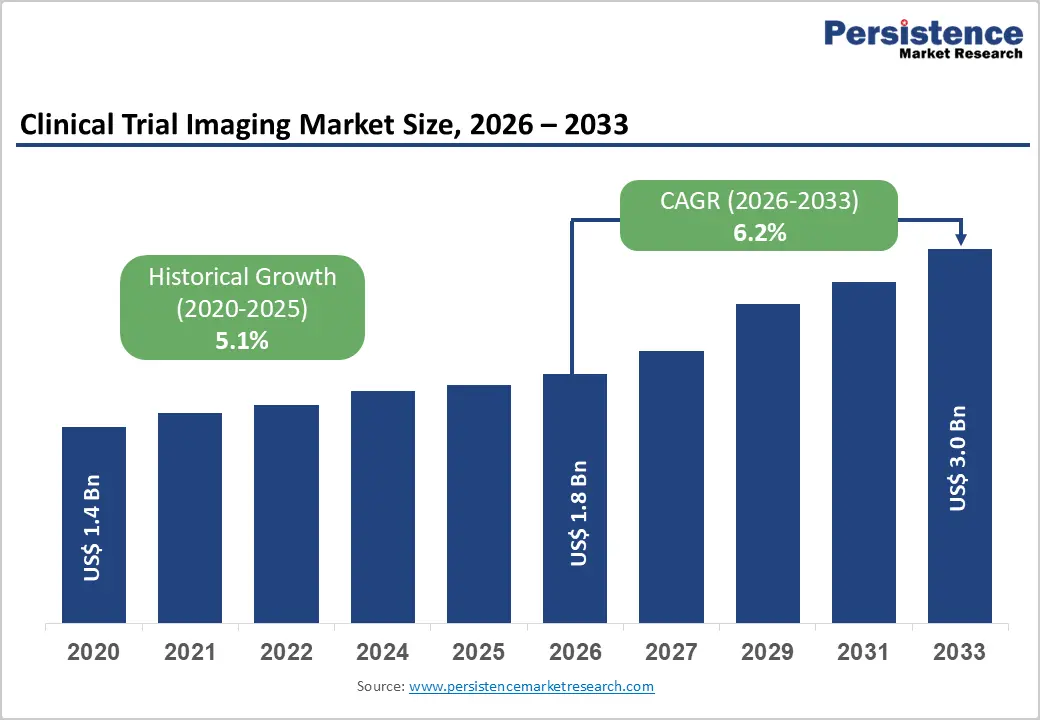

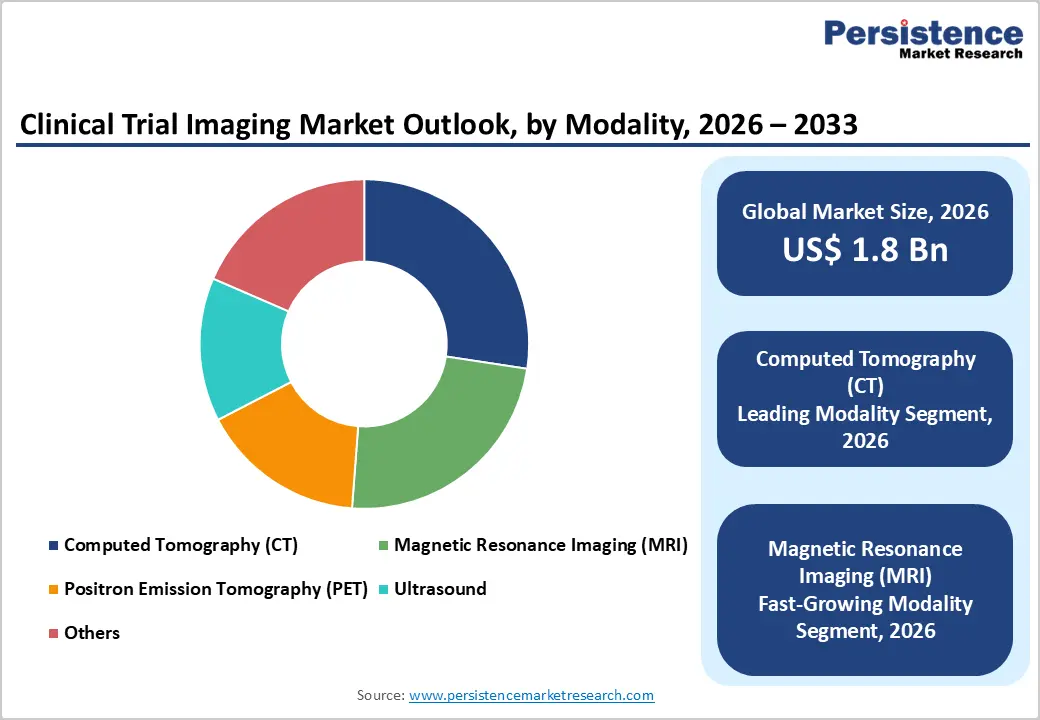

The global clinical trial imaging market size is estimated to grow from US$ 1.8 billion in 2026 to US$ 3.0 billion by 2033. The market is projected to record a CAGR of 6.2% during the forecast period from 2026 to 2033.

The rise in complexity in drug development and increasing reliance on imaging endpoints are significantly strengthening the adoption of clinical trial imaging across global markets. Imaging plays a critical role in disease diagnosis, patient stratification, and therapeutic response evaluation, making it an essential component of modern clinical trials.

Its widespread use in oncology, neurology, and cardiovascular studies supports accurate and reproducible outcome measurement. Growing integration of imaging biomarkers and quantitative analysis is further enhancing trial precision and regulatory acceptance. Additionally, the expansion of precision medicine and targeted therapies is increasing demand for high-resolution imaging modalities such as CT, MRI, and PET. The shift toward decentralized and hybrid clinical trials is also accelerating the use of cloud-based imaging platforms and remote data analysis.

Key Industry Highlights:

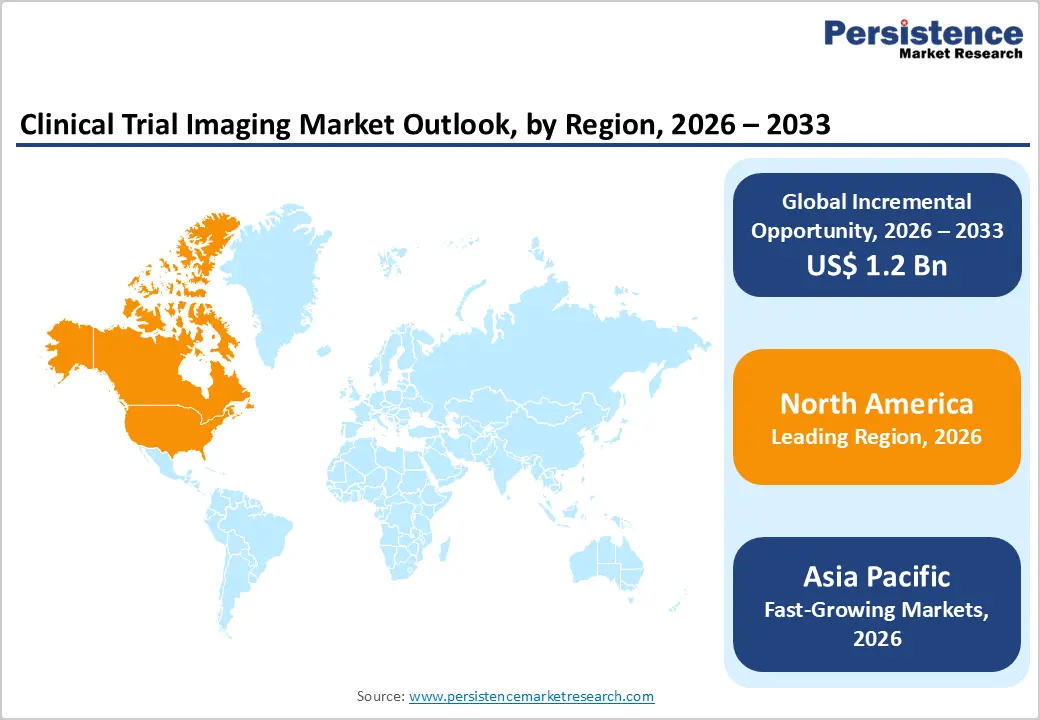

- Leading Region: North America holds 48.5% share, driven by a strong clinical trial ecosystem, high R&D investments, advanced imaging infrastructure, and early adoption of AI-enabled imaging analytics supporting precision medicine initiatives.

- Fastest-Growing Region: Asia Pacific is the most rapidly expanding market, supported by increasing clinical trial outsourcing, improving healthcare infrastructure, rising pharmaceutical investments, and growing adoption of advanced imaging technologies across emerging economies.

- Leading Offering Segment: Services dominate with 66.80% due to its critical role in centralized image reading, protocol standardization, regulatory compliance, and efficient management of multicenter imaging workflows.

- Leading Modality Segment: Computed Tomography (CT) accounts for 27.4%, supported by its widespread use in oncology trials, high imaging accuracy, rapid acquisition capabilities, and strong reliability in assessing disease progression and treatment response.

Market Dynamics

Drivers - Rising Complexity of Clinical Trials and Expanding Use of Imaging Biomarkers Accelerating Demand

Increasing complexity in clinical trial protocols, particularly in oncology and neurology, is a primary force driving demand for advanced imaging solutions. Imaging has become central to endpoint determination, disease progression tracking, and therapeutic response assessment, making it indispensable in modern trial design. The growing adoption of imaging biomarkers enables more precise, quantitative evaluation of treatment efficacy, reducing reliance on subjective clinical measures. Pharmaceutical and biotechnology companies are significantly increasing R&D investments, leading to a higher volume of trials requiring standardized imaging workflows.

Additionally, the shift toward precision medicine and targeted therapies is intensifying the need for high-resolution, multimodal imaging techniques such as CT, MRI, and PET. These modalities support patient stratification and biomarker validation, improving trial success rates. The increasing outsourcing of imaging services to specialized providers and CROs is further streamlining operations and reducing sponsor burden. Technological advancements, including AI-driven image analysis and cloud-based platforms, are enhancing efficiency, scalability, and data consistency. Regulatory emphasis on data integrity and reproducibility is also reinforcing adoption, collectively driving sustained market growth.

Restraints - High Operational Complexity and Regulatory Burden Limiting Scalable Implementation

Operational and regulatory challenges continue to constrain broader adoption of clinical trial imaging solutions. Imaging in multicenter trials requires strict standardization of acquisition protocols, calibration across sites, and consistent interpretation, which significantly increases logistical complexity. Variability in imaging equipment, technician expertise, and site infrastructure often leads to data inconsistencies, potentially affecting trial outcomes. Additionally, the high cost associated with advanced imaging modalities, centralized reading services, and data management platforms creates financial barriers, particularly for smaller sponsors and early-phase trials.

Regulatory compliance adds another layer of complexity, as imaging data must meet stringent standards for accuracy, traceability, and auditability. Requirements for data privacy, especially under frameworks such as GDPR, further complicate cross-border trials. Integration of imaging systems with existing clinical data platforms also poses interoperability challenges. Moreover, the limited availability of skilled radiologists and imaging specialists can delay analysis timelines. These factors collectively increase trial costs and operational risk, restricting scalability despite growing demand for imaging-driven endpoints in clinical research.

Opportunities - AI Integration and Emerging Market Expansion Unlocking Next-Generation Growth Potential

Advancements in artificial intelligence and digital health technologies are creating significant opportunities for innovation in clinical trial imaging. AI-powered image analysis enables automated lesion detection, volumetric assessment, and predictive modeling, improving accuracy while reducing interpretation time. Integration of cloud-based platforms is facilitating real-time data sharing, remote monitoring, and decentralized trial execution, enhancing operational efficiency. These capabilities are particularly valuable as clinical trials become more global and data-intensive.

Emerging markets in Asia-Pacific, Latin America, and the Middle East are presenting untapped growth potential due to expanding clinical trial activity, improving healthcare infrastructure, and cost advantages. Increasing participation of these regions in global multicenter trials is driving demand for standardized imaging solutions. Additionally, the rise of hybrid and decentralized trials is creating opportunities for portable imaging technologies and remote diagnostics. Strategic collaborations between imaging vendors, CROs, and pharmaceutical companies are further accelerating innovation. Continuous advancements in imaging modalities and analytics are expected to broaden the application scope, supporting long-term market expansion.

Category-wise Analysis

By Offering Insights

Services are projected to remain the dominant offering in the global clinical trial imaging market in 2026, accounting for 66.80% of total revenue, primarily due to their indispensable role in managing complex imaging workflows across multicenter trials. Their leadership is driven by the need for standardized image acquisition, centralized reading, and consistent interpretation aligned with regulatory requirements. Imaging core labs and service providers ensure protocol adherence, reduce inter-reader variability, and enhance data reliability, which is critical for endpoint validation.

Additionally, sponsors increasingly outsource imaging operations to specialized vendors to optimize costs and streamline trial timelines. The integration of advanced analytics, cloud-based platforms, and AI-assisted interpretation further strengthens service demand. Growing complexity in oncology and neurology trials, coupled with rising global clinical trial volumes, continues to reinforce reliance on comprehensive imaging service models, securing this segment’s leading position.

By Therapeutic Area Insights

Oncology is expected to lead the global clinical trial imaging market with a 38.7% revenue share in 2026, supported by its extensive reliance on imaging for tumor detection, staging, and therapeutic response evaluation. Imaging modalities such as CT, MRI, and PET play a critical role in assessing disease progression and validating clinical endpoints, making them integral to oncology trial design. The increasing shift toward precision medicine and biomarker-driven studies has further elevated the importance of quantitative imaging techniques.

Stringent regulatory requirements for efficacy assessment in cancer trials necessitate high-quality, standardized imaging data. Rising global cancer incidence and growing investment in oncology drug pipelines are significantly increasing trial volumes, thereby driving imaging demand. Continuous advancements in imaging technologies and AI-based analysis are also enhancing diagnostic accuracy, reinforcing oncology’s leadership across both early- and late-phase clinical studies.

By End-user Insights

Pharmaceutical & biotechnology companies are projected to dominate the global clinical trial imaging market in 2026 with a 48.9% share, driven by their central role as primary sponsors of clinical trials. These organizations generate substantial demand for imaging services to support drug development, particularly in therapeutic areas such as oncology, neurology, and cardiovascular diseases. Their reliance on imaging for endpoint evaluation, safety monitoring, and regulatory submissions significantly contributes to segment growth.

Rise in R&D investments and expanding biologics and precision medicine pipelines are driving higher clinical trial activity. Pharma and biotech firms are also adopting advanced imaging analytics and outsourcing imaging operations to CROs and specialized vendors to improve efficiency and reduce operational complexity. Strong partnerships with imaging service providers, along with the need for high-quality, compliant data, continue to reinforce their leadership in the market.

Regional Insights

North America Clinical Trial Imaging Market Trends

North America accounts for 48.5% of the global clinical trial imaging market in 2026, driven by a high concentration of clinical trials, strong presence of pharmaceutical sponsors, and advanced imaging infrastructure. The region benefits from widespread adoption of imaging biomarkers, AI-enabled analysis, and centralized imaging core labs. Growth is further supported by increasing outsourcing to CROs and regulatory standardization. High R&D spending and early adoption of decentralized and hybrid trials continue to reinforce regional dominance.

U.S. Clinical Trial Imaging Market Trends

The U.S. dominates North America with approximately 79.2% regional share, supported by a robust clinical trial ecosystem and strong presence of global sponsors and CROs. Increasing use of imaging endpoints in oncology and neurology trials, alongside rapid adoption of AI-based imaging analytics. Advanced regulatory frameworks, extensive site networks, and high R&D investments continue to strengthen the country’s leadership.

Canada Clinical Trial Imaging Market Trends

Canada holds around 11.4% share in North America, supported by a well-established clinical research environment and strong regulatory standards. Growth is driven by increasing participation in global multicenter trials and rising adoption of advanced imaging modalities. Government support for clinical research and expansion of academic research networks are improving trial efficiency and imaging adoption.

Europe Clinical Trial Imaging Market Trends

Europe represents a highly regulated and quality-driven market, accounting for a significant share of global clinical trial imaging demand. The region emphasizes data standardization, patient safety, and compliance with stringent regulatory frameworks such as GDPR. Increasing adoption of imaging biomarkers in oncology and neurology trials, along with strong CRO presence, supports steady growth. However, regulatory complexity and longer approval timelines slightly moderate expansion compared to emerging regions.

Germany Clinical Trial Imaging Market Trends

Germany leads Europe with approximately 24.6% regional share, driven by a strong pharmaceutical industry and advanced imaging infrastructure. Growth is supported by increasing use of imaging endpoints in clinical trials and strong emphasis on precision medicine. The country’s robust R&D ecosystem and presence of leading research institutions continue to enhance its position in clinical trial imaging.

United Kingdom Clinical Trial Imaging Market Trends

The UK accounts for nearly 15.3% of the European market, supported by a mature clinical research ecosystem and strong adoption of advanced imaging technologies. Growth is driven by increasing outsourcing to CROs and rising use of AI in imaging analysis. Government-backed clinical research initiatives and strong academic collaborations further contribute to steady market expansion.

Asia Pacific Clinical Trial Imaging Market Trends

Asia Pacific is the fastest-growing region, driven by expanding clinical trial activity, cost advantages, and increasing pharmaceutical outsourcing. The region benefits from a large patient pool, improving healthcare infrastructure, and growing adoption of advanced imaging technologies. Rising investments by global sponsors and CROs, along with regulatory improvements, are accelerating market growth. Rapid digitization and increasing use of cloud-based imaging platforms further enhance regional penetration.

China Clinical Trial Imaging Market Trends

China dominates Asia Pacific with approximately 38.7% regional share, supported by a large clinical trial base and strong government support for pharmaceutical innovation. Growth is driven by increasing adoption of imaging biomarkers and expansion of domestic CRO capabilities. Advancements in imaging infrastructure and rising participation in global trials continue to strengthen market development.

India Clinical Trial Imaging Market Trends

India accounts for around 12.9% share of the Asia Pacific market, driven by rapid growth in clinical trial outsourcing and cost-efficient research capabilities. Increasing adoption of advanced imaging modalities and expansion of CRO networks are supporting growth. A large patient population, improving regulatory landscape, and rising investments in clinical research infrastructure further contribute to market expansion.

Competitive Landscape

The global clinical trial imaging market is highly competitive, with strong participation from Ixico PLC, Navitas Life Sciences, Resonance Health, Radiant Sage LLC, Medpace, and WCG Clinical. These companies leverage advanced imaging analytics, centralized reading capabilities, and integrated clinical trial workflows to enhance data accuracy and efficiency. Rising demand for imaging biomarkers in oncology and neurology trials is driving innovation in AI-based analysis and cloud platforms. Market players are expanding partnerships, global site networks, and R&D investments to deliver scalable, regulatory-compliant imaging solutions.

Key Industry Developments:

- In May 2026, TriSalus Life Sciences, Inc. announced the initiation of patient enrollment for the PREDICTT clinical trial (NCT07444645), a prospective study evaluating its Pressure-Enabled Drug Delivery™ (PEDD™) technology in patients with primary and metastatic liver tumors, aiming to enhance therapeutic delivery alongside standard oncology treatments.

- In January 2026, Flywheel announced major milestones from 2025, alongside the successful closure of an oversubscribed $25 million funding round led by Novalis Lifesciences and 8VC. The funding is expected to accelerate expansion of its imaging data management and AI-driven analytics capabilities for clinical research. It also supports scaling of cloud-based infrastructure and strengthens partnerships with pharmaceutical companies and CROs to enhance clinical trial imaging workflows.

Companies Covered in Clinical Trial Imaging Market

- Ixico PLC

- Navitas Life Sciences

- Resonance Health

- Radiant Sage LLC

- Medpace

- WCG Clinical

- Icon PLC

- Voiant

- Clario

- Parexel International Corporation

- Anagram

- Calyx

- Invicro

- BioTelemetry, Inc.

- Intrinsic Imaging LLC

- Others

Frequently Asked Questions

The global clinical trial imaging market is projected to be valued at US$ 1.8 Bn in 2026.

Rising complexity of oncology and neurology trials, increasing reliance on imaging biomarkers, and growing outsourcing to CROs drive the global clinical trial imaging market.

The global Clinical Trial Imaging Market is poised to witness a CAGR of 6.2% between 2026 and 2033.

Expansion of AI-powered imaging analytics and increased clinical trial activity in emerging markets present key growth opportunities.

from Ixico PLC, Navitas Life Sciences, Resonance Health, Radiant Sage LLC, Medpace, and WCG Clinical are some of the key players in the clinical trial imaging market.