- Healthcare Services

- Outsourced Clinical Trials & Formulation Market

Outsourced Clinical Trials & Formulation Market Size, Trends, Share, Growth, and Regional Forecast, 2025 to 2032

Outsourced Clinical Trials & Formulation Market by Dosage Form (Oral Dosage, Injectable Dosage, and Others), Application (API Manufacturing, Fill-Finish Product Manufacturing, Drug Product Development, and Packaging/Labeling), End-user, Regional Analysis, 2025 - 2032

Outsourced Clinical Trials & Formulation Market Share and Trends Analysis

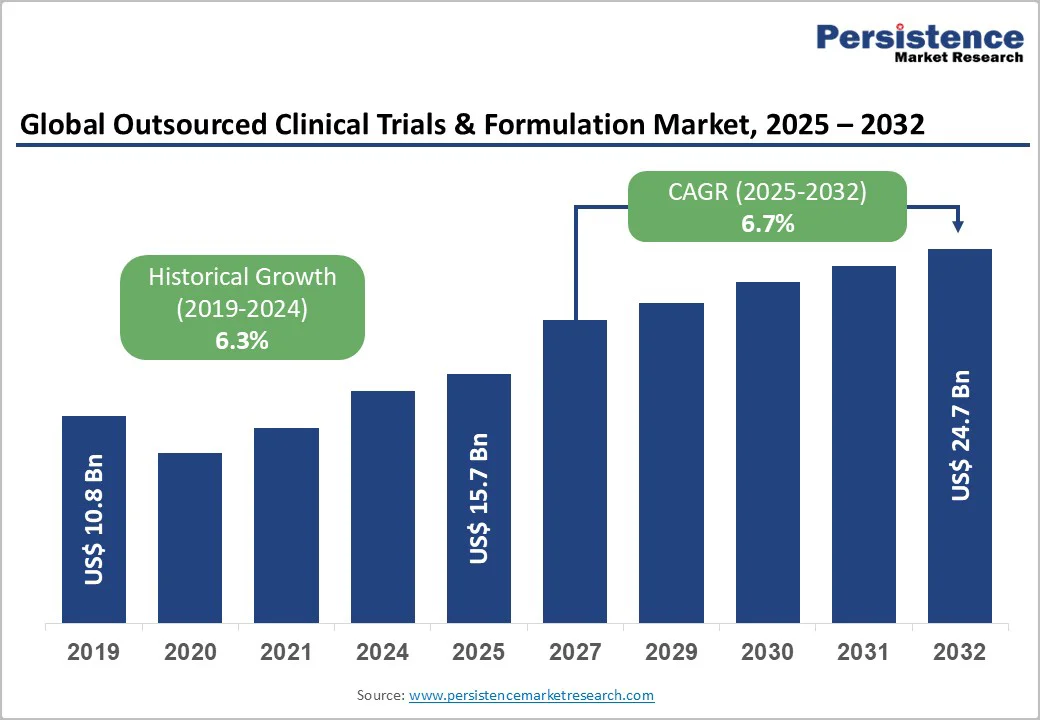

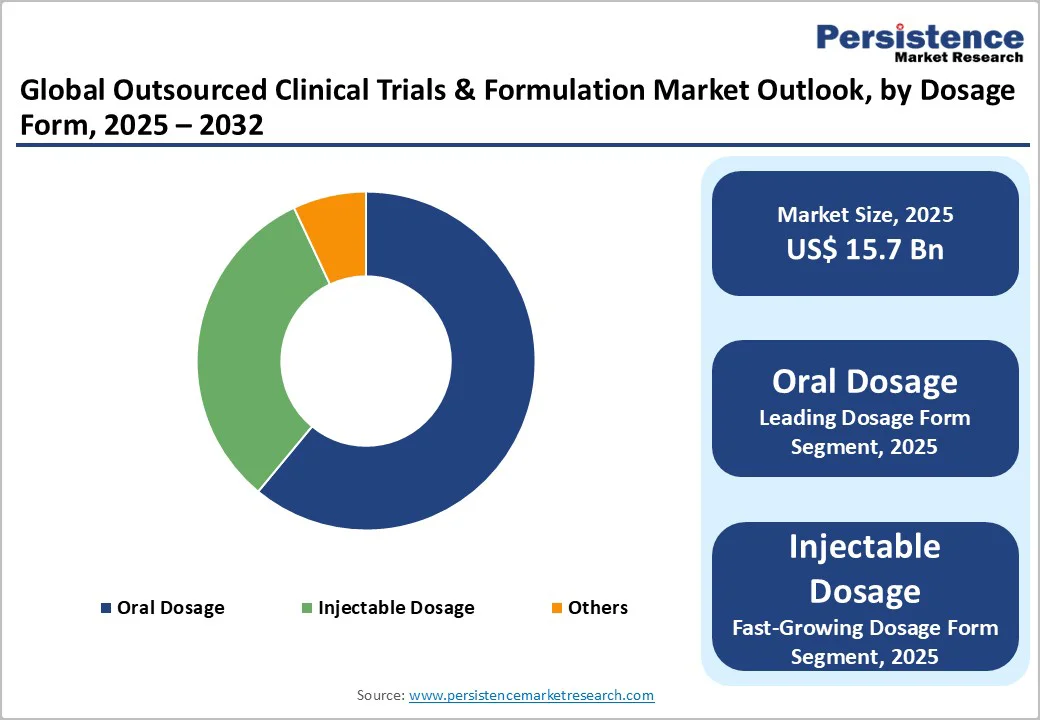

The global outsourced clinical trials & formulation market is valued at US$15.7 billion in 2025 and is projected to reach US$24.7 billion, growing at a CAGR of 6.7% from 2025 to 2032.

The outsourced clinical trials and formulation market is expanding as pharmaceutical companies increasingly rely on external partners due to limited in-house capacity, technology gaps, and the need for flexible backup manufacturing. API production is often outsourced to cost-efficient regions such as Asia and Europe, allowing companies to benefit from CDMOs’ strong CMC expertise, GMP-compliant facilities, and robust quality systems.

Key Industry Highlights:

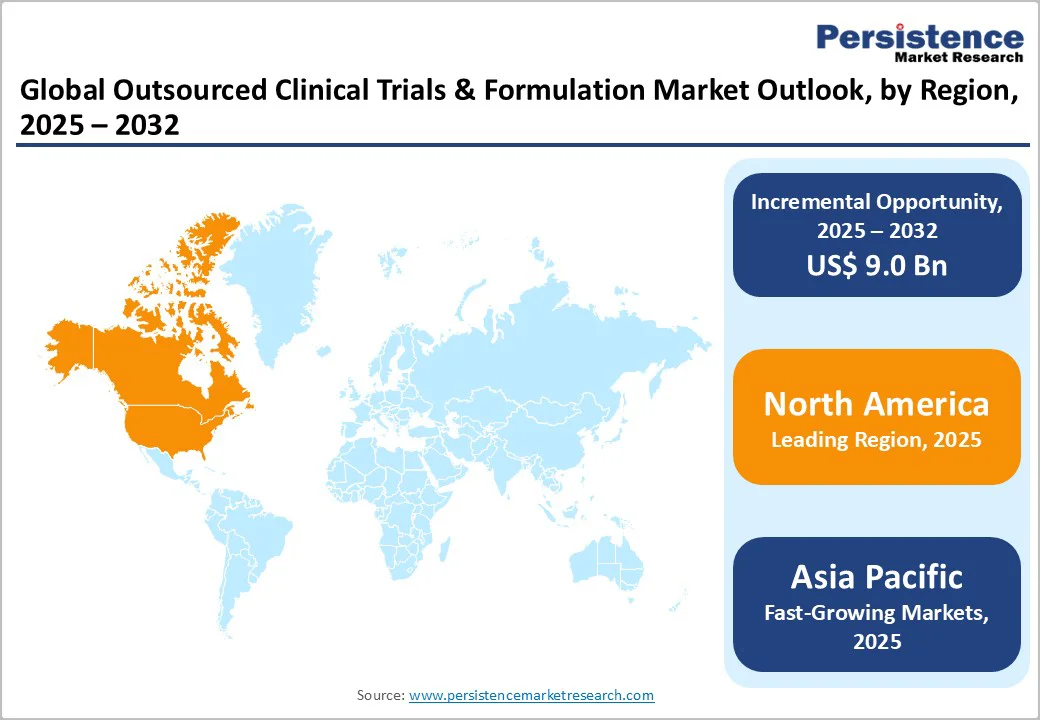

- Leading Region: North America was the leading region in 2024, supported by significant R&D investment, advanced regulatory mechanisms, and a robust CRO/CDMO ecosystem.

- Fastest Growing Region: Asia Pacific is projected as the fastest-growing region, driven by manufacturing growth, policy innovation, and attractive cost dynamics in China and India.

- Dominant Segment: Oral Dosage forms lead with a 61% market share, benefiting from proven technological adoption and demand for patient-friendly formulations.

- Fastest Growing Segment: API Manufacturing emerges as the fastest-growing segment with a 46% share, due to supply chain, cost, and regulatory needs across the industry.

| Key Insights | Details |

|---|---|

| Outsourced Clinical Trials & Formulation Market Size (2025E) | US$15.7 Bn |

| Market Value Forecast (2032F) | US$24.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.3% |

Market Dynamics

Driver - Rising Complexity & Specialization in Drug Development

The growing focus on advanced and specialized therapies is a strong driver for the outsourced clinical trials and formulation market. Pharmaceutical pipelines are shifting toward complex biologics, gene and cell therapies, antibody-drug conjugates, and precision small molecules, all of which require sophisticated development tools, specialized formulation techniques, and rigorous regulatory planning.

Many drug developers lack the internal expertise, infrastructure, or technology needed to manage these demanding programs, prompting them to rely on experienced outsourcing partners. CROs and CDMOs equipped with high-end analytical platforms, scalable manufacturing systems, and established quality frameworks offer the technical depth needed to navigate complex study protocols and regulatory requirements.

In the U.S., a growing majority of clinical trials, over 75% in 2024, are already conducted through external CROs, demonstrating strong industry dependence on outsourcing. These partners help sponsors reduce timelines, manage operational complexity, and maintain compliance across global studies.

As therapeutic innovation accelerates, the need for specialized capabilities, flexible capacity, and end-to-end development support continues to rise, reinforcing outsourcing as a vital strategy for efficient and compliant drug development.

Restraints - Stringent Formulation Development Outsourcing Regulations

Strict regulatory requirements across major markets pose a significant challenge for the outsourced clinical trials and formulation sector. Regulatory bodies enforce detailed guidelines for formulation development, manufacturing practices, documentation, analytical testing, and quality assurance.

Smaller CDMOs that lack advanced technologies or modernized facilities often struggle to meet these standards, resulting in process deviations, inconsistent product quality, and higher operational costs. These compliance gaps can lead to project delays or failures, discouraging pharmaceutical companies from partnering with less-equipped service providers.

In developed regions, the increasingly stringent scrutiny of small-molecule products has also reduced the number of approvals, further impacting outsourcing demand.

The competitive landscape adds additional pressure, as both emerging and established CDMOs pursue expansion through new facilities, partnerships, and acquisitions to maintain their market position. While these strategies strengthen some players, they create barriers for smaller firms unable to keep pace. Collectively, regulatory complexity and intense competition act as restraints on the overall growth of outsourced clinical trials and formulation services.

Opportunity - Collaboration with Pharma & Biotech Companies

Strategic collaboration with pharmaceutical and biotechnology companies represents a strong opportunity for growth in the outsourced clinical trials and formulation market. As drug developers continue to expand their pipelines and accelerate timelines, they increasingly seek partners that can offer integrated development, analytical, and manufacturing support. This creates room for CDMOs to form long-term alliances, co-development agreements, and technology-driven partnerships that enhance service depth and broaden global reach.

Mergers and acquisitions also allow CDMOs to strengthen capabilities in areas such as complex formulations, biologics, and advanced analytical testing. Technological innovation remains a key focus, with organizations investing in automation, closed-system processing, and next-generation analytical platforms to deliver higher-quality outcomes.

A notable example is the 2021 collaboration between Lonza and Agilent, which aimed to integrate advanced analytical technologies with Lonza’s Cocoon Platform to improve cell therapy workflows. Such partnerships not only expand service offerings but also position CDMOs as essential contributors to modern drug development, creating significant opportunities for market growth.

Category-wise Analysis

By Dosage Form, Oral Dosage Dominate the Global Market

The Oral Dosage segment holds a dominant 61% share in 2024, reaffirming its position as the cornerstone of global pharmaceutical formulations. Tablets, capsules, and other oral solid dosage forms remain highly preferred due to their convenience, dose accuracy, stability, and cost-efficient manufacturing. These attributes make them the leading choice for chronic therapies, pediatric care, and large-volume generic production.

CROs and CDMOs worldwide have built extensive capabilities in oral formulation development, enabling rapid scale-up, technology transfer, and global regulatory support. Advances in controlled-release systems, taste-masking, and bioavailability enhancement technologies are further strengthening demand, particularly for complex generics, poorly soluble molecules, and modified-release therapies.

As emerging markets expand access to affordable medicines and established markets continue to prioritize adherence-focused formulations, the oral dosage category maintains strong momentum. Its broad therapeutic applicability and mature manufacturing ecosystem ensure sustained leadership in outsourced formulation and clinical development services.

By Application, API Manufacturing Leads the Market

API Manufacturing remains the leading application segment, capturing roughly 46% of the market in 2024. Pharmaceutical companies increasingly outsource API production to leverage cost efficiencies, specialized infrastructure, and the robust compliance frameworks of experienced CMOs.

Heightened regulatory scrutiny by agencies such as the FDA, along with evolving environmental and quality requirements, makes in-house API manufacturing challenging for many firms, particularly smaller innovators. Outsourcing enables access to state-of-the-art containment systems, validated processes, and global supply chain networks, supporting uninterrupted production.

The rising demand for complex and high-potency APIs (HPAPIs) is also accelerating partnerships with CMOs equipped with advanced technologies and high-containment facilities. As drug pipelines shift toward more potent and targeted molecules, companies rely on outsourcing partners to ensure scalable, compliant, and efficient production.

Growing emphasis on supply chain resilience, quality assurance, and rapid development timelines continues to reinforce API Manufacturing as the dominant application in the outsourced clinical trials and formulation market.

Region-wise Insights

North America Outsourced Clinical Trials & Formulation Market Trends

North America continues to dominate the outsourced clinical trials and formulation market, with the U.S. capturing nearly 91.7% of the regional share. This leadership is supported by a strong base of API manufacturing, advanced healthcare accessibility, and a well-established network of CROs and CDMOs capable of handling complex development programs.

The region benefits from a favorable regulatory environment, consistent R&D investment, and one of the world’s most extensive pharmaceutical pipelines.

The U.S. also offers exceptional clinical research infrastructure, including specialized trial sites, experienced investigators, and the widespread use of advanced electronic data capture and compliance systems. Government incentives and funding aimed at accelerating innovation in biotech and novel therapies further enhance outsourcing demand.

Companies such as Velesco, which operate out of a former Pfizer analytical facility in Michigan, reflect the region’s focus on strengthening drug development efficiency. With over 39% of global market share in 2024 concentrated in North America, the region’s continued emphasis on quality, regulatory alignment, and technology-driven development is expected to sustain its dominance in outsourced clinical trials and formulation services.

Asia and Pacific Outsourced Clinical Trials & Formulation Market Trends

Asia Pacific has emerged as the fastest-growing region for outsourced clinical trials and formulation services, driven by increasing activity in China, Japan, and India. The region offers a strong combination of cost-effective operations, expanding manufacturing capacity, and growing alignment with international regulatory standards.

China leads with nearly 59% of East Asia’s share, supported by rapid expansion of clinical trials, large patient pools, and government initiatives to upgrade biopharmaceutical manufacturing and research capabilities.

India is strengthening its position through regulatory reforms led by the CDSCO, which continue to streamline ethics approvals, registration processes, and compensation frameworks for global trial sponsors.

Japan’s mature scientific environment and rising biologics focus add further momentum. Collectively, these factors are attracting global pharmaceutical and biotechnology companies seeking efficient development timelines, technical expertise, and flexible production capacity. As regional infrastructure continues to advance, the Asia Pacific is expected to maintain its strong growth trajectory in outsourced clinical and formulation services.

Competitive Landscape

The outsourced clinical trials and formulation market is highly competitive, driven by the growing demand for integrated development solutions from global pharma and biotech companies.

Leading providers are expanding their end-to-end service portfolios, covering early formulation, clinical manufacturing, trial management, and global supply logistics. Strategic collaborations are becoming central to strengthening technical depth, geographic reach, and specialty service offerings.

Companies are also actively acquiring innovative start-ups to enhance formulation technologies, analytical capabilities, and clinical operations efficiency. This consolidation is enabling providers to deliver faster turnaround times, higher-quality outputs, and improved regulatory compliance.

As competition intensifies, firms are prioritizing differentiated scientific expertise, flexible manufacturing capacity, and strong client relationships to capture a larger share of development outsourcing budgets.

Key Industry Developments:

- In May 2024, AGC Biologics and BioConnection a CMO specializing in aseptic vial and syringe filling for clinical and commercial use, announced the formation of a new strategic partnership.

- In January 2023, WuXi STA, a subsidiary of WuXi AppTec, announced that its first continuous manufacturing (CM) line for oral solid drug products had become operational at its facility in Wuxi, China.

Companies Covered in Outsourced Clinical Trials & Formulation Market

- Quotient Sciences

- SGS S.A.

- Catalent, Inc.

- Piramal Pharma Solutions

- Thermo Fisher Scientific / Patheon

- BioXcellence (Boehringer Ingelheim)

- Siegfried Holding AG

- Adare Pharmaceuticals, Inc.

- KP Pharmaceutical Technology Inc.

- Hermes Pharma GmbH,

- Eurofins Scientific SE,

- Glatt GmbH,

- Pharmaceutics International, Inc.,

- Rottendorf Pharma GmbH.

- Others

Frequently Asked Questions

The global market is projected to be valued at US$ 15.7 Bn in 2025.

Increased complexity in drug development, stringent global regulations, and emphasis on cost-efficiency and accelerated time-to-market are primary demand drivers.

The global market is poised to witness a CAGR of 6.7% between 2025 and 2032.

Adoption of digital platforms and decentralized clinical trial models offers significant future growth potential for market participants.

Key companies include Quotient Sciences, SGS S.A., Catalent, Inc., Piramal Pharma Solutions, Thermo Fisher Scientific/Patheon, BioXcellence (Boehringer Ingelheim), Siegfried Holding AG, and others.