- Biotechnology

- Cellular Pathology Market

Cellular Pathology Market Size, Share, and Growth Forecast, 2026 - 2033

Cellular Pathology Market by Product Type (Diagnostic Kits, Others), Technology (Digital Pathology, Immunohistochemistry, Others), Application (Cancer Diagnostics, Infectious Diseases, Others), End-user, and Regional Analysis for 2026 - 2033

Cellular Pathology Market Size and Trends Analysis

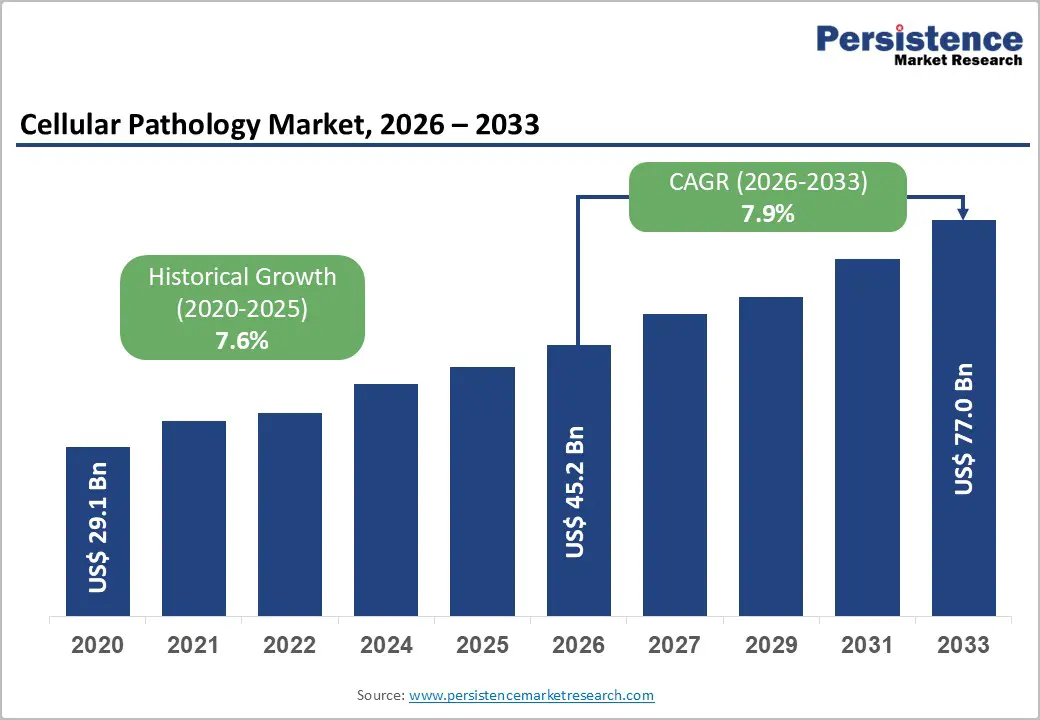

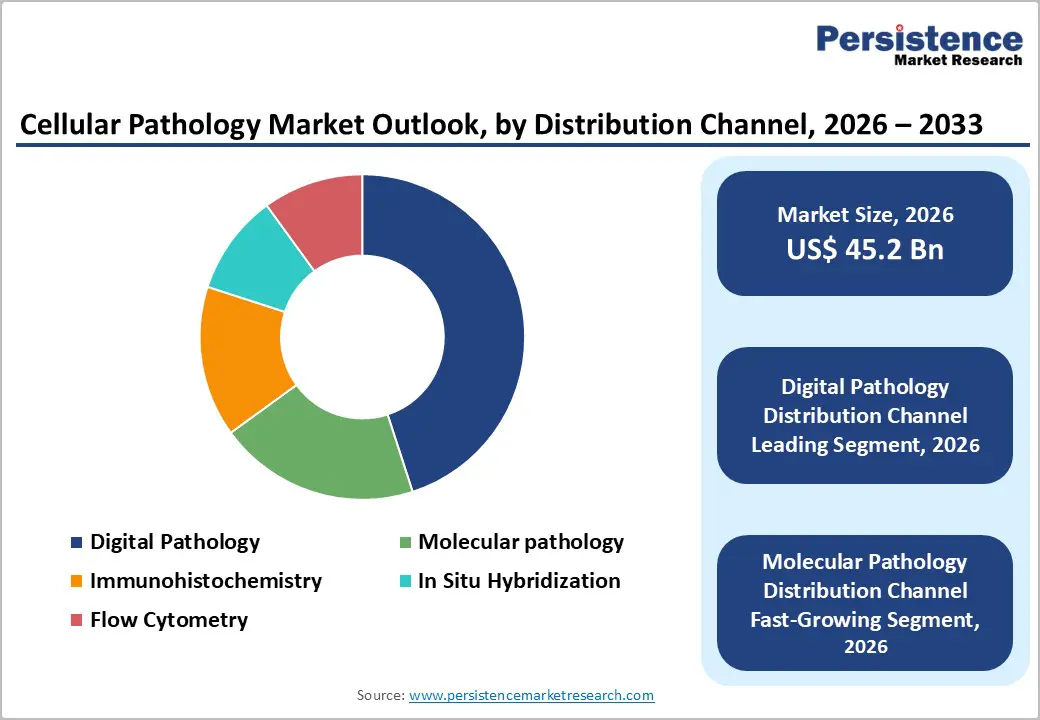

The global cellular pathology market size is likely to be valued at US$45.2 billion in 2026, and is expected to reach US$77.0 billion by 2033, growing at a CAGR of 7.9% during the forecast period from 2026 to 2033, driven by the increasing prevalence of cancer and chronic diseases, rising demand for precise disease diagnosis, and growing adoption of digital pathology and molecular techniques in diagnostic laboratories and hospitals.

Advances in AI-powered image analysis, multiplex IHC, and next-generation sequencing integration are further boosting uptake by offering faster turnaround, higher accuracy, and personalized insights. Increased recognition of cellular pathology as critical for early cancer detection, treatment selection, and companion diagnostics is a major driver of market growth. It also plays a key role in research for emerging precision oncology and infectious disease markets.

Key Industry Highlights:

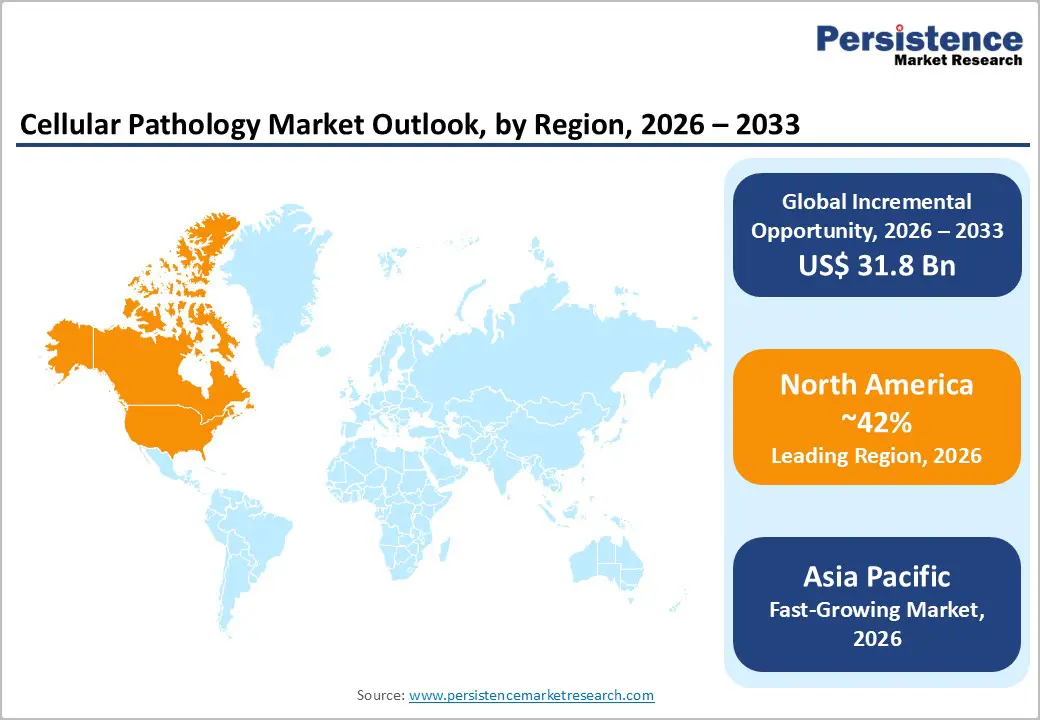

- Leading Region: North America, anticipated to account for a 42% market share in 2026, driven by advanced healthcare infrastructure, high R&D investment, and strong demand in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising cancer incidence, expanding diagnostic capacity, and increasing adoption of digital pathology in China and India.

- Leading Technology: Digital pathology, contributing nearly 35% of the market revenue, due to the rapid digitization of workflows.

- Leading Application: Cancer diagnostics is expected to dominate the market, contributing nearly 55% of revenue in 2026, driven by rising cancer incidence and the focus on early detection.

- In February, Labcorp announced the clinical availability of Labcorp® Plasma Complete™, a ctDNA-based liquid biopsy test that enabled oncologists to perform comprehensive genomic profiling for advanced solid tumors and inform personalized treatment decisions from a simple blood draw.

| Key Insights | Details |

|---|---|

|

Cellular Pathology Market Size (2026E) |

US$45.2 Bn |

|

Market Value Forecast (2033F) |

US$77.0 Bn |

|

Projected Growth CAGR (2026-2033) |

7.9% |

|

Historical Market Growth (2020-2025) |

7.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Increasing Cancer Burden and Precision Oncology Adoption

The global number of cancer cases continues to rise sharply, placing a growing demand on diagnostic services such as cellular pathology. In 2022, there were an estimated 20 million new cancer cases worldwide and approximately 9.7 million cancer-related deaths, reflecting a substantial public health burden that requires early and accurate diagnosis to improve outcomes. These figures are projected to climb significantly by 2050, with new cases expected to reach over 35 million annually if current trends persist, driven largely by ageing populations and increased exposure to risk factors.

Precision oncology approaches are transforming how cancer is diagnosed and treated by tailoring medical decisions to the molecular and genetic profiles of individual tumors. Programs supported by regulatory bodies such as the U.S. Food and Drug Administration’s Precision Oncology Program focus on advancing methodologies that help match targeted therapies to specific genomic and proteomic characteristics of a patient’s cancer. These advancements increase the clinical utility of pathology tests and reinforce the importance of comprehensive diagnostic workflows in the fight against cancer.

Expanding Digital Pathology and Molecular Techniques

The increasing adoption of digital pathology and molecular techniques is accelerating growth in the cellular pathology market by enabling faster, more precise diagnostics and streamlined laboratory workflows. Government-backed programs such as the CDC’s Electronic Pathology (ePath) Implementation Project have facilitated automated electronic capture and reporting of pathology data across all 50 U.S. states, supporting faster cancer case reporting and public health surveillance. Digital slide scanning, virtual microscopy, and AI-assisted image analytics allow pathologists to view, share, and interpret high-resolution images remotely, improving collaboration and reducing turnaround times. Virtual microscopy supports ultra-high resolution imaging over networks, expanding diagnostic reach and integrity of stored data.

Molecular techniques such as PCR and sequencing are central to identifying genetic variations and infectious agents, offering diagnostic depth beyond traditional histology. Programs such as the U.S. National Institutes of Health’s Cancer Genome Atlas (TCGA) have molecularly characterized over 20,000 cancer samples, demonstrating the critical role of molecular data in disease classification and personalized care. Molecular diagnostics provide detailed genomic insights that guide targeted therapies and improve clinical decision-making.

Barrier Analysis - High Capital Cost of Digital Pathology Systems

The substantial upfront investment required for digital pathology systems poses a significant restraint on the growth of the cellular pathology market. Converting traditional glass slides into whole-slide digital images necessitates purchasing high-resolution scanners, data servers, specialized software, and robust IT infrastructure, which can run into multi-million-dollar expenditures for large clinical labs, as seen in financial analyses of early adopters at tertiary cancer centers. Annual expenditures at large facilities were estimated at over US$5.2 million when accounting for hardware, software, IT, and staffing costs, highlighting the heavy financial burden on institutions aiming to digitize their pathology workflows.

Smaller hospitals, community labs, and facilities in lower-resource regions often lack the capital to justify such investments, slowing market penetration. The cost per digital slide scan varies widely and depends on scanner utilization, indicating that high fixed costs must be offset by large volumes of testing to become economically viable.

Reimbursement Challenges and Regulatory Complexity

Reimbursement challenges and regulatory complexity pose significant hurdles for the cellular pathology market’s growth and adoption. Securing reimbursement for advanced diagnostic tests, especially those involving molecular assays, digital pathology workflows, or AI-assisted tools, is difficult because many payers have limited historical frameworks for covering novel technologies. Pathology providers often face lengthy review processes to demonstrate clinical utility, cost-effectiveness, and improved patient outcomes.

Regulatory pathways for cellular pathology technologies are complex and evolving. Diagnostic systems that combine hardware, software, and AI algorithms fall under multiple regulatory categories in different countries, requiring comprehensive evidence for safety, performance, and interoperability. Regulatory bodies may require extensive validation studies, real-world performance data, and post-market surveillance, which extend development timelines and increase costs.

Opportunity Analysis - Innovations in AI-Powered Digital Pathology and Companion Diagnostics

The integration of AI into digital pathology opens significant opportunities for the cellular pathology market by enhancing diagnostic precision and operational efficiency. Government-linked scientific efforts, including a virtual workshop hosted by the U.S. National Cancer Institute (NCI), highlight how digital pathology combined with artificial intelligence (AI) can support large-scale image analysis, standardize data handling, and improve infrastructure for cancer research and clinical trials, guiding future advancements in precision diagnostics. Such initiatives are shaping standards for data quality assurance and scalable digital platforms that accelerate disease characterization and decision support.

Government regulatory science programs such as the U.S. Food and Drug Administration’s (FDA) Digital Pathology Program focus on enabling safe and effective digital pathology devices, laying the groundwork for broader AI adoption in clinical settings. These programs address technical challenges and help ensure interoperability and reliable performance of AI-augmented diagnostic tools, creating a more conducive regulatory environment.

Expansion in Infectious Disease Testing

The expansion in infectious disease testing is being driven by rising global awareness of emerging pathogens, pandemics, and antimicrobial resistance. Hospitals, public health agencies, and diagnostic laboratories are increasingly prioritizing rapid, accurate, and high-throughput testing to manage outbreaks and routine surveillance. Advances in molecular pathology, including PCR, next-generation sequencing (NGS), and point-of-care assays, allow early detection of bacterial, viral, and fungal infections, supporting timely treatment and containment strategies. Digital pathology and automated laboratory platforms further enhance efficiency, reducing turnaround times and minimizing human errors.

The integration of AI-driven analytics enables rapid interpretation of complex datasets, improving diagnostic precision and supporting epidemiological monitoring. The growth of decentralized and point-of-care testing in remote or resource-limited areas expands accessibility, ensuring that timely diagnostics reach wider populations. Government initiatives for public health preparedness and investment in diagnostic infrastructure also contribute to market growth. Increased collaboration between diagnostic companies, hospitals, and research institutions accelerates innovation, allowing new assays and platforms to reach the market faster.

Category-wise Analysis

Technology Insights

Digital pathology is expected to dominate the market, contributing nearly 35% of revenue in 2026, propelled by its ability to transform traditional workflows through high-resolution imaging, remote access, and AI-assisted analysis. By converting glass slides into digital images, laboratories can store, share, and analyze samples more efficiently, reducing turnaround times and human errors. Integration with AI and machine learning enhances diagnostic accuracy, particularly in complex cancer and infectious disease cases. Hospitals and research centers benefit from streamlined collaboration across locations, enabling faster decision-making and improved patient care. Sectra AB’s digital pathology solution used with Leica Biosystems’ Aperio GT 450 DX scanner, which received FDA 510(k) clearance, allowing the use of standardized DICOM images for primary pathology diagnostics in the U.S. This approval enables labs to digitize tissue slides, access and review high-resolution images remotely, and streamline workflows, improving efficiency and collaboration in cancer diagnosis.

Molecular pathology represents the fastest-growing technology, due to its ability to analyze genes, proteins, and molecular markers with high precision. Techniques such as PCR, next-generation sequencing (NGS), and in-situ hybridization enable early detection of diseases, personalized treatment planning, and monitoring of therapy response. Laboratories are increasingly adopting automated and high-throughput molecular platforms to handle complex diagnostic workloads efficiently. Integration with digital pathology and AI-driven analytics enhances accuracy and reduces turnaround times. Thermo Fisher Scientific, Inc. offers molecular pathology platforms such as the Ion-Proton System, enabling rapid, high-precision genetic analysis for oncology, inherited disorders, and infectious diseases, supporting early detection and personalized treatment.

Application Insights

Cancer diagnostics is expected to dominate the market, contributing nearly 55% of revenue in 2026, fueled by increasing global incidence of various cancers and the growing emphasis on early detection. Advanced immunohistochemistry (IHC), molecular testing, and digital pathology solutions enable precise tumor profiling, guiding personalized treatment strategies and improving patient outcomes. Hospitals and diagnostic laboratories are adopting automated platforms that allow high-throughput analysis, reducing errors and turnaround times. Integration of AI-driven image analysis further enhances accuracy and efficiency in identifying malignant tissues. F. Hoffmann-La Roche Ltd. leverages its Ventana BenchMark IHC and digital pathology systems to help labs accurately identify tumor types, guide targeted therapies, and support companion diagnostics, driving significant cancer diagnostics revenue.

Infectious diseases represent the fastest-growing application, driven by rising global prevalence and the need for rapid, accurate diagnosis. Advances in molecular assays, immunohistochemistry, and digital pathology allow precise detection of bacterial, viral, and fungal pathogens, supporting timely treatment decisions. Hospitals and diagnostic laboratories increasingly adopt automated and high-throughput platforms to manage outbreaks and routine testing efficiently. Integration with digital systems enables faster data analysis, reducing diagnostic errors and turnaround times. bioMérieux launched EPISEQ-SARS-CoV-2, a cloud-based application for surveillance of SARS-CoV-2 variants that helps laboratories detect and monitor emerging viral strains using genomic data. This digital and molecular pathology-linked tool supports public health responses by providing accurate, high-throughput infectious disease analysis globally.

Regional Insights

North America Cellular Pathology Market Trends

North America is projected to dominate, accounting for nearly 42% of the share in 2026, driven by the region’s advanced diagnostic infrastructure, high R&D investment, and strong public awareness of precision oncology benefits. Distribution systems in the U.S. and Canada provide extensive support for cellular pathology programs, ensuring wide accessibility across reagents, digital pathology, and diagnostic laboratory populations. Increasing demand for AI-assisted, convenient, and easy-to-integrate forms is further accelerating adoption, as these formats improve accuracy and reduce barriers associated with conventional microscopy.

Innovation in cellular pathology technology, including stable molecular panels, improved AI interpretation delivery, and targeted cancer enhancement, is attracting significant investments from both public and private sectors. Government initiatives and NCI campaigns continue to promote use against diagnostic risks, treatment concerns, and emerging companion diagnostic threats, creating sustained market demand. The growing focus on infectious disease grades and specialty uses, particularly for cancer diagnostics and others, is expanding the target applications for cellular pathology.

Europe Cellular Pathology Market Trends

Europe shows significant growth by increasing awareness of precision medicine benefits, strong regulatory systems, and government-led biobanking programs. Countries, such as Germany, the U.K., France, and the Netherlands, have well-established pathology frameworks that support routine cellular pathology use and encourage adoption of innovative digital and molecular delivery methods. These high-precision formulations are particularly appealing for cancer diagnostics populations, regulation-conscious labs, and research users, improving outcomes and coverage rates.

Technological advancements in cellular pathology development, such as enhanced multiplex IHC, application-targeted delivery, and improved software grades, are further boosting market potential. European authorities are increasingly supporting research and trials for pathology against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, accurate options is aligned with the region’s focus on preventive disease management and reducing misdiagnosis. Public awareness campaigns and promotion drives are expanding reach in both diagnostic laboratories and hospital segments, while suppliers are investing in AI and novel variants to increase efficacy.

Asia Pacific Cellular Pathology Market Trends

Asia Pacific is likely to be the fastest-growing market for cellular pathology in 2026, driven by rising cancer incidence, increasing government initiatives, and expanding diagnostic programs across the region. Countries such as China, India, Japan, and South Korea are actively promoting pathology campaigns to address oncology growth and emerging precision needs. Cellular pathology is particularly attractive in these regions due to its scalable administration, ease of adoption, and suitability for large-scale diagnostic laboratory and hospital drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-deploy cellular pathology, which can withstand challenging infrastructure conditions and minimize cost dependence. These innovations are critical for reaching domestic labs and improving overall diagnostic coverage. Growing demand for reagents, digital pathology, and cancer diagnostics applications is contributing to market expansion. Public-private partnerships, increased healthcare expenditure, and rising investments in pathology research and capacity are further accelerating growth. The convenience of pathology delivery, combined with improved accuracy and reduced risk of late diagnosis, positions it as a preferred choice.

Competitive Landscape

The global cellular pathology market is marked by intense competition between established diagnostic leaders and emerging digital-pathology specialists. In North America and Europe, companies such as Leica Biosystems and F. Hoffmann-La Roche Ltd. dominate through robust R&D pipelines, extensive global laboratory networks, and strong hospital affiliations, supported by advanced digital pathology platforms and immunohistochemistry (IHC) innovations.

In Asia Pacific, local players are gaining traction with cost-effective solutions that improve accessibility for hospitals and diagnostic centers. The adoption of digital pathology enhances laboratory workflow efficiency, reduces turnaround time risks, and allows large-scale integration across multiple labs. Strategic partnerships, collaborations, and acquisitions combine technical expertise, broaden product portfolios, and accelerate commercialization. Advanced molecular formulations address precision challenges, driving adoption in oncology-focused segments and further expanding market penetration across diagnostic and research applications worldwide.

Key Industry Developments:

- In July 2025, Labcorp launched two innovative liquid biopsy tests, Labcorp Plasma Detect and PGDx Elio Plasma Focus Dx, to advance cancer detection and treatment. Plasma Detect used whole-genome sequencing to identify molecular residual disease (MRD) in stage III colon cancer patients, while the FDA-authorized Elio Plasma Focus Dx provided rapid, pan-solid tumor profiling to guide targeted therapies.

- In May 2025, Labcorp, a global leader in innovative and comprehensive laboratory services, expanded its precision oncology portfolio. The company added new test offerings for solid tumors and hematologic malignancies and enhanced its biopharma solutions to accelerate clinical trials and support companion diagnostic development.

Top Regional Markets

By Product Type

- Diagnostic Kits

- Reagents

- Instruments

- Consumables

- Software

By Technology

- Digital Pathology

- Immunohistochemistry

- In Situ Hybridization

- Flow Cytometry

- Molecular Pathology

By Application

- Cancer Diagnostics

- Infectious Diseases

- Genetic Testing

- Drug Discovery

- Toxicology

By End-user

- Hospitals

- Diagnostic Laboratories

- Research Institutes

- Pharmaceutical Companies

- Academic Centers

By Region

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

Companies Covered in Cellular Pathology Market

- Leica Biosystems Nussloch GmbH

- BioGenex.

- Hologic, Inc.

- Epredia

- Sakura Finetek

- F. Hoffmann-La Roche Ltd.

- Merck KGaA

- Gestalt Diagnostics

- Carl Zeiss AG

- Olympus Corporation

- Abbott Laboratories Inc.

- NeoGenomics Laboratories

Frequently Asked Questions

The global cellular pathology market is projected to reach US$45.2 billion in 2026.

Adoption of advanced technologies such as immunohistochemistry, molecular testing, digital pathology, and AI-driven analysis for precise tumor profiling.

Adoption of advanced technologies such as immunohistochemistry, molecular testing, digital pathology, and AI-driven analysis for precise tumor profiling.

The cellular pathology market is poised to witness a CAGR of 7.9% from 2026 to 2033.

Expansion of liquid biopsy and molecular residual disease (MRD) testing for personalized cancer treatment.