- Technology

- Cellular IoT Market

Cellular IoT Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Cellular IoT Market by Component Type (Hardware, Software / Platforms, Services), Technology (2G / 3G IoT, 4G LTE IoT, 5G IoT), Connectivity Type (Massive IoT, Broadband IoT, Critical IoT, Industrial Automation IoT), Industry (Automotive & Transportation, Manufacturing & Industrial, Healthcare & Life Sciences, Utilities & Energy, Agriculture & Environment Monitoring, Consumer Electronics, Smart Cities / Public Infrastructure, Misc.), and Regional Analysis for 2026 - 2033

Cellular IoT Market Size and Trends Analysis

The global cellular IoT market size is likely to be valued at US$ 5.2 billion in 2026 and is projected to reach US$ 12.5 billion by 2033, growing at a CAGR of 13.4% between 2026 and 2033. The market's expansion is underpinned by the accelerated adoption of 5G networks, the proliferation of connected devices across industrial and consumer segments, and the widespread integration of IoT solutions in automotive and transportation, manufacturing and industrial, utilities and energy, and healthcare and life sciences sectors.

Regulatory support for smart metering infrastructure, particularly in Europe's binding smart meter deployment roadmap, which targets 95% adoption by 2030, and the deployment of 258 operators across 68 countries offering NB-IoT and LTE-M networks as of April 2024, further catalyzes market penetration. The shift toward cloud-connected, real-time asset tracking and predictive maintenance capabilities is positioning the Cellular IoT Market as a critical enabler of digital transformation across enterprises and critical infrastructure.

Key Industry Highlights:

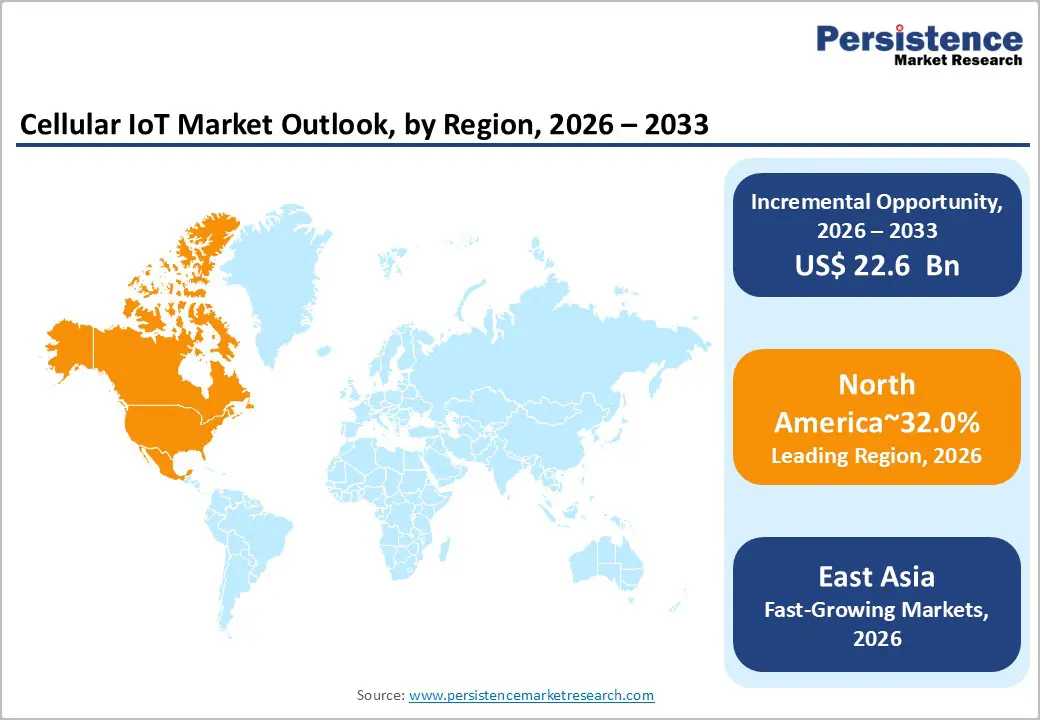

- Regional Leadership: North America dominates the global Cellular IoT Market with a 32% share in 2026, supported by mature 4G/5G infrastructure, enterprise cloud adoption, and the strong presence of major vendors such as Qualcomm, AT&T, Ericsson, and Semtech.

- Fastest-Growing Region: East Asia captures a 28% share in 2026 and stands as the fastest-growing region, driven by China’s manufacturing scale, rapid 5G deployment, and advanced semiconductor and module ecosystems led by Huawei Technologies and Fibocom.

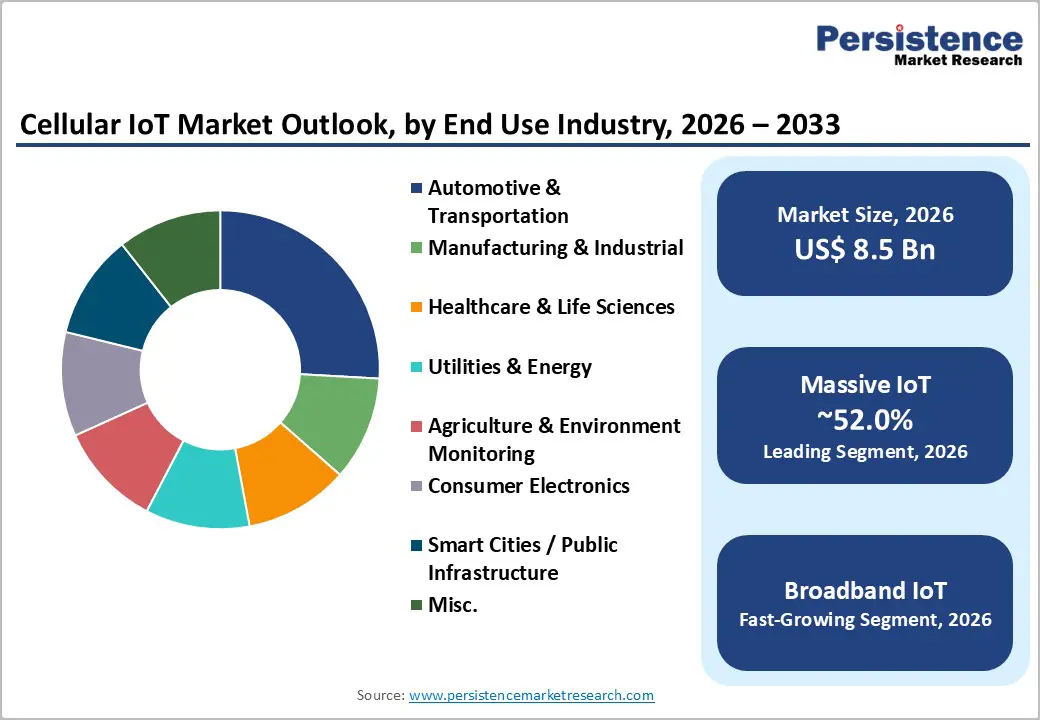

- Connectivity Dominance: Massive IoT (NB-IoT and LTE-M) leads with 54% share in 2026, powered by smart metering, asset tracking, and low-power wide-area IoT applications.

- Rapidly Growing Connectivity: Broadband IoT (LTE Cat. 1/Cat.1bis and entry-level 5G) secures 45% share in 2024 and emerges as the fastest-growing segment, driven by high-data IoT use cases including video-enabled asset tracking, e-mobility, and industrial AR applications.

- Leading End-user: Automotive & Transportation holds 24% share in 2026, supported by connected vehicles, V2X communication, over-the-air (OTA) updates, and smart transport infrastructure integration.

- Fastest-Growing End-user: Manufacturing & Industrial is the fastest-growing segment, fueled by Industry 4.0 adoption, predictive maintenance, AI-powered analytics, and 5G-enabled factory automation.

- Technology & Market Opportunity: Private 5G networks, and satellite–terrestrial hybrid connectivity offers major growth potential, enabling reliable, low-power, and mission-critical IoT deployments across enterprises and remote locations.

| Key Insights | Details |

|---|---|

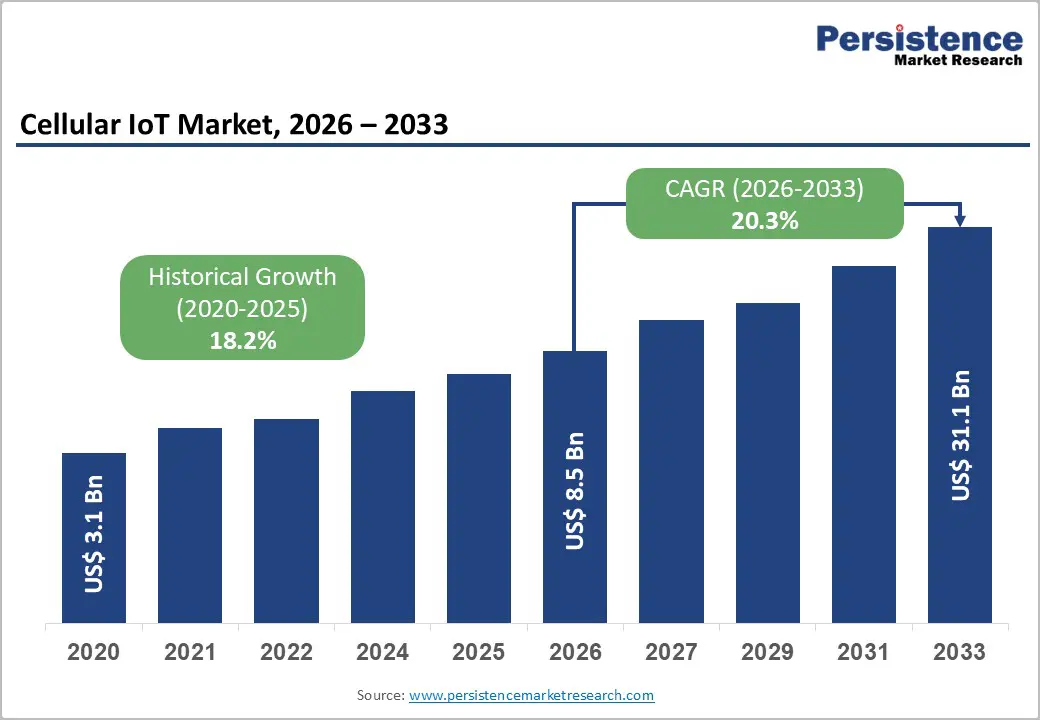

| Cellular IoT Market Size (2026E) | US$ 8.5 Bn |

| Market Value Forecast (2033F) | US$ 31.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 20.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 18.2% |

Market Dynamics

Drivers - Expansion of 5G Infrastructure and Enhanced Connectivity Standards

The rollout of 5G networks, combined with advancements in 3GPP Release 17 standards, is fundamentally transforming the Cellular IoT Market landscape. According to GSA (Global Mobile Suppliers Association) data as of April 2024, 258 operators across 68 countries have deployed or launched NB-IoT and LTE-M networks, with 176 operators actively investing in NB-IoT and 81 operators investing in LTE-M.

The introduction of 3GPP Release 17 brings critical enhancements for massive IoT, including improved uplink coverage via PUSCH/PUCCH repetitions, enhanced NR positioning accuracy targeting less than 1 m for industrial IoT use cases, and extended battery life for low-power devices via extended discontinuous reception (eDRX) mechanisms.

These technical advancements enable organisations to deploy IoT solutions in challenging environments such as remote utility locations and underground infrastructure, where traditional connectivity solutions face limitations. The adoption of these standards across Cellular IoT deployments is creating a unified, globally accessible infrastructure that reduces fragmentation and accelerates time-to-market for IoT applications.

Accelerated Smart Metering and Utilities Infrastructure Modernisation

Smart metering represents a strategic priority for utilities globally, with over 1.06 billion smart meters deployed by the end of 2023 according to IoT Analytics' Global Smart Meter Market Tracker, and projections indicating 54% adoption of the global electricity meter market by 2030.

The European Union's Electricity Directive establishes binding deployment deadlines: 20% rollout by the end of 2025, 50% by the end of 2028, and 95% by the end of 2030 for residential and small business consumers.

Smart metering deployments rely fundamentally on Cellular IoT connectivity to enable real-time data collection, remote meter management, and integration with billing and grid management systems. Utilities leverage Cellular IoT to remotely provision and manage millions of meters over-the-air, reduce field service visits, detect anomalies, and comply with regulatory requirements. This macro-infrastructure trend directly expands the addressable market for the cellular IoT market, particularly for massive IoT (NB-IoT and LTE-M) connectivity solutions designed for low-power, cost-effective deployments across distributed utility networks.

Proliferation of Industrial IoT and Predictive Maintenance Adoption

Manufacturing and industrial enterprises are adopting Cellular IoT technologies at an accelerating pace to enable predictive maintenance, asset tracking, and real-time production optimisation. Industry data indicate that the IoT-based asset tracking and monitoring market is expanding rapidly, driven by the need to reduce unplanned downtime and extend asset lifecycles. In the automotive sector, 5G-enabled IoT applications facilitate vehicle-to-everything (V2X) communication, real-time fleet management, and over-the-air (OTA) software updates, directly supporting manufacturing and logistics optimisation.

The convergence of Cellular IoT with artificial intelligence and edge computing enables automated anomaly detection, demand forecasting, and dynamic asset utilisation optimisation, driving measurable returns on investment and justifying enterprise capital expenditure across industrial segments within the Cellular IoT Market.

Restraint - Integration Complexity and Legacy Infrastructure Incompatibility

The Cellular IoT Market faces structural complexity due to the coexistence of multiple connectivity standards and the slow migration away from legacy technologies. While a large number of operators globally support NB-IoT and LTE-M, adoption rates remain uneven across regions, and many enterprises operate hybrid networks combining LTE Cat. 1/Cat.1bis, LTE-M, and NB-IoT, complicating deployment and vendor selection.

Recent industry observations indicate growing adoption of LTE Cat 1/Cat.1bis alongside a relative slowdown in LPWA standards such as LTE Cat.M and NB-IoT, reflecting regional differences in device economics and network coverage. Integration challenges, legacy infrastructure dependencies, and the need for backward compatibility across older 3GPP releases create friction in Cellular IoT deployments, particularly for SMEs and organisations in emerging markets.

Opportunity - Expansion of 5G Private Networks and Enterprise IoT Deployments

5G private networks represent a high-growth opportunity for Cellular IoT vendors, enabling enterprises across manufacturing, automotive, utilities, and logistics to deploy mission-critical, isolated IoT networks with guaranteed reliability and low latency. In June 2023, partnerships such as Sierra Wireless and Amdocs launched end-to-end solutions for private 4G/5G cellular networks, simplifying deployment across utilities, transportation, smart cities, and robotics. 5G Reduced Capability (5G RedCap) technology offers reduced cost and power consumption compared to full 5G while maintaining higher data transmission speeds than LTE-M and NB-IoT, creating a compelling middle-ground solution for enterprises seeking to upgrade from legacy 3GPP standards. The growing recognition of private cellular as a network-as-a-service model enables new business partnerships between Cellular IoT vendors, infrastructure providers, and industry verticals, unlocking high-margin recurring revenue streams.

The cellular IoT market participants can capture this opportunity by developing vertical-specific solutions, such as ultra-low-latency factory automation modules, secure device management platforms for regulated industries, and integrated software-as-a-service platforms that abstract underlying connectivity complexity for enterprise customers. Organisations investing in regulatory compliance automation, multi-network orchestration, and partner ecosystem development are well-positioned to lead in this expanding segment.

Satellite-Terrestrial Hybrid Connectivity and IoT Coverage Expansion

The emergence of satellite-assisted cellular IoT solutions represents a transformational opportunity to extend connectivity into remote, underserved regions and support global asset tracking scenarios beyond terrestrial network coverage. Qualcomm Technologies introduced the Qualcomm 212S and 9205S modem chipsets in June 2023, integrating satellite IoT capabilities aligned with 3GPP Release 17 standards, enabling hybrid cellular and satellite connectivity for ultra-low-power, off-grid IoT monitoring in remote locations.

According to industry developments presented at MWC 2025, satellite-driven hybrid connectivity is reshaping the landscape for enterprises in agriculture, utilities, maritime, and energy sectors, where traditional cellular coverage remains sporadic or unavailable. This opportunity enables Cellular IoT vendors to differentiate through non-terrestrial network (NTN) fallback capabilities, as exemplified by Semtech's HL7900 5G LPWA module showcased in April 2025 with integrated Cat-M, NB-IoT, and NTN fallback.

Organisations deploying global supply chain visibility, environmental monitoring in developing regions, and disaster recovery operations increasingly value the resilience provided by hybrid satellite-cellular solutions, justifying investment in specialised modules, managed services, and partner ecosystems that combine telecommunications expertise with space-based connectivity providers.

Category-wise Analysis

Component Type Insights

Hardware components dominate the cellular IoT market, encompassing modems, chipsets, modules, routers, and end devices that form the physical foundation of cellular connectivity solutions. Hardware accounts for approximately 54.7% of market value in 2026, driven by the continued proliferation of connected devices across automotive, manufacturing, utilities, and consumer electronics segments.

Enterprise demand for ruggedised, industrial-grade modules capable of operating in extreme temperature ranges, high-vibration environments, and harsh chemical exposure continues to drive hardware consumption. Strategic developments such as Qualcomm's acquisition of Sequans' 4G IoT technologies in August 2024 strengthened the modem chipset portfolio, while Fibocom's launch of the MC610-GL LTE Cat. 1bis module in June 2024 reinforced competition in cost-effective, compact connectivity solutions. The hardware segment is further supported by ongoing module miniaturisation, integration of security-hardened processors, and adoption of multi-protocol SoCs (systems-on-chip) that reduce bill-of-materials costs while expanding functional capabilities for original equipment manufacturers (OEMs).

Services and software-based offerings represent the fastest-growing component category, encompassing connectivity management platforms, IoT device management, cloud integration services, security services, and professional consulting. This segment is experiencing accelerated adoption driven by enterprises' preference for operational expenditure (OpEx) models over capital expenditure (CapEx), desire to outsource complex IoT deployment and lifecycle management to specialised service providers, and regulatory compliance requirements that necessitate expert guidance.

Connectivity Type Insights

Massive IoT, encompassing NB-IoT and LTE-M (also known as LTE Cat-M), commands the largest market share at approximately 54.0% in 2026, representing the dominant connectivity choice for low-power, wide-area IoT applications.

According to GSA data, 132 operators have deployed NB-IoT networks and 61 have deployed LTE-M networks globally, with 982 documented device types supporting these standards as of April 2024. Massive IoT solutions deliver exceptional battery life, extending device operational periods to 10+ years on standard batteries and low deployment costs by utilising unmodified cellular spectrum and existing carrier infrastructure. Smart metering, asset tracking in utilities, and basic environmental monitoring applications predominantly rely on Massive IoT, driving sustained demand. The continuing refinement of 3GPP Release 17 standards for Massive IoT, including extended uplink coverage mechanisms and enhanced sleep modes, reinforces this segment's dominance and ensures compatibility across multi-generational device deployments throughout the Cellular IoT Market.

Broadband IoT encompasses LTE Cat. 1/Cat.1bis and entry-level 5G connectivity, delivering higher data transmission speeds (10–100 Mbps) than Massive IoT while maintaining reasonable power consumption and cost efficiency. Market data reveals LTE Cat. 1/Cat.1bis expanded to 45% of market share in 2024 from 32% in 2023, demonstrating rapid adoption acceleration. This segment is experiencing the fastest growth rate because it serves emerging use cases, including asset tracking with high-resolution video or image uploads, e-mobility and EV charging infrastructure, remote video surveillance, and augmented reality (AR) in industrial settings.

Industry Insights

Automotive and Transportation represent the dominant end-use industry, commanding approximately 24% of the Cellular IoT Market in 2026, driven by the global automotive industry's strategic shift toward connected, autonomous, and electric vehicles. Connected vehicle deployments leverage Cellular IoT for vehicle-to-everything (V2X) communication, real-time diagnostics, over-the-air (OTA) software updates, and integration with smart transportation infrastructure.

The manufacturing and industrial sectors are the fastest-growing end-use segment, driven by Industry 4.0 transformation initiatives, widespread adoption of predictive maintenance platforms, and competitive pressure to optimise production efficiency and reduce downtime.

Smart factory deployments utilising 5G URLLC (Ultra-Reliable Low-Latency Communication) for human-robot collaboration and wireless manufacturing networks are transitioning from pilot programs to production-scale implementations, as exemplified by Ericsson and Audi's partnership in January 2020, demonstrating 5G-enabled factory automation without wired infrastructure.

Regional Insights and Trends

North America Market Cellular IoT Market Trends

North America commands approximately 32% of the global Cellular IoT Market share, positioning the region as the largest market by revenue and the primary innovation hub for next-generation cellular IoT solutions. The market dominance is underpinned by mature 4G/5G network infrastructure, widespread enterprise cloud adoption, and the concentration of major Cellular IoT vendors, including Qualcomm, AT&T, Ericsson, and Semtech. U.S. telecommunications carriers have invested heavily in 5G standalone (SA) networks with network slicing capabilities, providing enterprises with dedicated, isolated network segments for mission-critical IoT deployments.

AT&T emerged as a global leader in IoT connectivity according to the 2025 Transforma Insights IoT Peer Benchmarking Report, leveraging innovations such as Global SIM Advanced and IoT Console Single Pane of Glass to reduce operational complexity for enterprise customers. The region's regulatory environment, characterised by the FCC's framework for low-power wide-area networks and sector-specific mandates in healthcare and utilities, creates consistent demand for compliant, auditable Cellular IoT solutions. Manufacturing automation adoption, particularly in automotive and aerospace sectors, is driving Broadband IoT demand, while smart city initiatives in municipalities are accelerating Massive IoT deployments for infrastructure monitoring.

East Asia Cellular IoT Market Trends

East Asia accounts for approximately 28% of the market and is the fastest-growing major region, driven by rapid industrialization, aggressive 5G network deployment, and the massive scale of manufacturing and logistics operations across China, Japan, and South Korea.

China's manufacturing sector dominance and ongoing Industry 4.0 transformation initiatives are generating enormous demand for cellular IoT connectivity in factory automation, supply chain visibility, and quality assurance applications. The region's advanced semiconductor and device manufacturing ecosystem, with companies like Fibocom, Huawei Technologies, and China Mobile driving innovation, accelerates the development of cost-competitive Cellular IoT modules and integrated solutions.

Huawei Technologies solidified its position through strategic FRAND patent licensing agreements with Nordic Semiconductor in June 2022 and participation in Sisvel's Cellular IoT patent pool as of September 2023, enabling large-scale NB-IoT and LTE-M deployment across Asia Pacific. Japan's emphasis on ageing infrastructure monitoring and healthcare IoT applications, combined with South Korea's advanced 5G deployment, creates sustained demand for both Massive IoT (utilities and smart metering) and Broadband IoT (healthcare and automotive) connectivity solutions. The region's dominance in electronics manufacturing and export logistics ensures continued investment in Cellular IoT for supply chain optimisation and real-time shipment tracking.

Europe Cellular IoT Market Trends

Europe accounts for approximately 25% of global share, characterised by stringent data protection regulations, advanced industrial automation practices, and ambitious smart metering deployment mandates.

Germany's advanced manufacturing ecosystem, combined with strong Industry 4.0 adoption, drives enterprise investment in Broadband IoT for factory automation and predictive maintenance. GDPR compliance requirements mandate rigorous data governance, encryption, and audit trails within Cellular IoT platforms, increasing deployment complexity but also creating differentiation opportunities for vendors offering privacy-by-design solutions.

The region's sustainability agenda, including mandates for renewable energy grid integration, electric vehicle charging infrastructure, and building energy efficiency, creates cross-cutting demand for Cellular IoT connectivity in smart grid, smart buildings, and transportation electrification initiatives. Regional vendors such as Semtech expanded production capabilities through new Canadian manufacturing facilities in February 2025, signalling investment in European and North American supply chain resilience and supporting the region's continued technological leadership in cellular IoT.

Competitive Landscape

The global cellular IoT market exhibits an oligopolistic-to-moderately consolidated structure, characterised by the dominance of a limited number of large chipset vendors, module suppliers, and connectivity providers that control core technologies, standards alignment, and large-scale deployments.

Companies such as Qualcomm Technologies, Inc., Huawei Technologies Co., Ltd., and MediaTek Inc. lead at the chipset level, driving innovation across NB-IoT, LTE-M, and 5G IoT standards. On the module side, Quectel Wireless Solutions, Fibocom Wireless Inc., Telit Cinterion, and Sierra Wireless (Semtech) hold strong positions due to their broad portfolios, global certifications, and deep integration with device manufacturers.

Network and platform players, including Ericsson AB, AT&T Inc., and Verizon Communications Inc., strengthen market consolidation through end-to-end IoT connectivity, device management, and enterprise-grade solutions. High entry barriers related to spectrum access, standard compliance, certification costs, and ecosystem partnerships limit new entrants, reinforcing market concentration. Ongoing demand from smart cities, automotive, utilities, and industrial IoT continues to create selective opportunities for niche players, preventing full monopolisation.

Key Industry Developments

- Sep 30, 2024 - Qualcomm Technologies, Inc. and Sequans Communications S.A. completed the acquisition of Sequans’ 4G IoT technology by Qualcomm, enhancing Qualcomm’s low-power cellular IoT portfolio with LTE-M, NB-IoT, and upcoming 5G Redcap solutions, strengthening its position in industrial and embedded IoT connectivity.

- October 30, 2025, AT&T and Thales launched a next-generation eSIM solution powered by GSMA SGP.32, enabling enterprises to remotely and securely manage IoT subscriptions at scale, while ensuring device integrity, advanced automation, and compliance with global cybersecurity standards, supporting diverse industries including automotive, smart cities, healthcare, and utilities.

Companies Covered in Cellular IoT Market

- Qualcomm Technologies, Inc.

- Huawei Technologies Co., Ltd.

- Quectel Wireless Solutions Co., Ltd.

- Fibocom Wireless Inc.

- Telit Communications / Telit Cinterion

- Sierra Wireless (Semtech)

- u‑blox Holding AG

- Ericsson AB

- Cisco Systems, Inc.

- AT&T Inc.

- Verizon Communications Inc.

- ZTE Corporation

- Texas Instruments Incorporated

Frequently Asked Questions

The global Cellular IoT market is projected to be valued at US$ 8.5 Bn in 2026.

The Massive IoT segment is expected to account for approximately 54.0% of the global Cellular IoT market by Connectivity Type in 2026.

The market is expected to witness a CAGR of 20.3% from 2026 to 2033.

The Global Cellular IoT market growth is driven by the global rollout of 5G and advanced connectivity standards, large-scale smart metering and utilities infrastructure modernisation, and accelerating adoption of industrial IoT solutions for predictive maintenance, asset tracking, and real-time operational optimisation.

Key opportunities in the global Cellular IoT market include the expansion of private 5G enterprise networks, satellite terrestrial hybrid connectivity for global and remote IoT coverage, and the growing demand for AI- and edge-enabled, vertical-specific Cellular IoT platforms delivering real-time analytics and mission-critical intelligence.

The key players in the Cellular IoT market include Qualcomm Technologies, Inc., Huawei Technologies Co., Ltd., Quectel Wireless Solutions Co., Ltd., Fibocom Wireless Inc., Telit Communications / Telit Cinterion, and Sierra Wireless (Semtech), which collectively lead the market through strong cellular chipset portfolios, extensive IoT module offerings, global connectivity platforms, and deep integration across industrial, automotive, utilities, and enterprise IoT ecosystems.