- Plastics, Polymers & Resins

- Bioplastics Market

Bioplastics Market Size, Share, and Growth Forecast, 2025- 2032

Bioplastics Market by Product Type (Bio-Degradable and Non-Biodegradable), by Application (Packaging, Agriculture/Horticulture, Consumer Goods, Automotive, Textiles, Construction, and Other Applications) and Regional Analysis for 2025 - 2032

Bioplastics Market Size and Trends Analysis

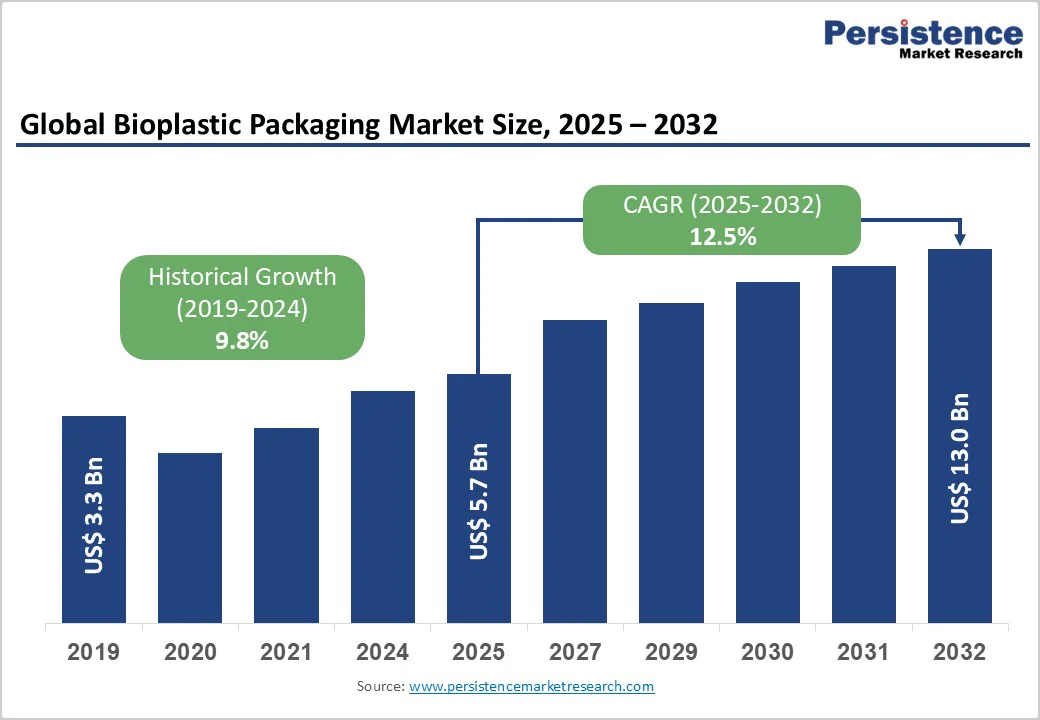

The global bioplastics market was valued at US$ 18.6 Bn in 2025 and is expected to surge to US$ 65.7 Bn by 2032, registering an impressive CAGR of 19.8% during the forecast period. This rapid expansion reflects intensifying global demand driven by stricter environmental regulations, rising corporate sustainability commitments, and continuous technological advancements that are enhancing cost efficiency and material performance.

Key Industry Highlights:

- Biodegradable bioplastics commanding above 60% market revenue share with accelerating growth trajectory driven by EU Single-Use Plastics Directive implementation and corporate sustainability commitments, while non-biodegradable bio-based plastics capture 40% through infrastructure compatibility advantages?

- Packaging applications dominate with above 60% revenue share, while textiles emerge as the fastest-growing segment with CAGR exceeding 16% through 2032, driven by automotive textile integration in electric vehicle platforms and consumer demand for sustainable fashion alternatives?

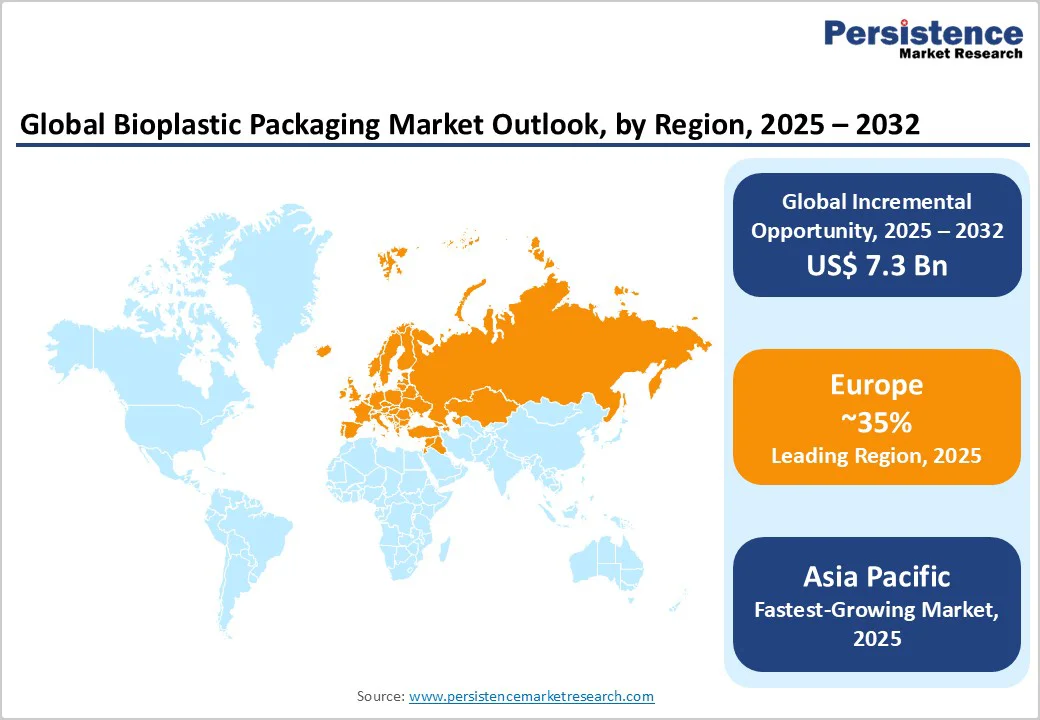

- Europe maintains 45%+ market share as the dominant region with established regulatory frameworks and production infrastructure, while North America expands at 22.5% CAGR, emerging as the fastest-growing region due to the strong corporate sustainability commitments from major packaging and consumer goods manufacturers.

- Market leaders BASF, NatureWorks, TotalEnergies Corbion, Braskem, and Mitsubishi Chemical control approximately 45% market share, with emerging competition from technology-focused startups including Danimer Scientific and Polymateria disrupting incumbent positions through PHA and specialty material innovations

- Strategic market developments in 2024-2025 include Balrampur Bioyug's commercial production validation in India, Horizon Europe GRECO project advances in PLA food packaging technology, and the CSIRO-Murdoch University Bioplastics Innovation Hub, collectively advancing technology capabilities and regional market infrastructure

| Key Insights | Details |

|---|---|

| Bioplastics Market Size (2025E) | US$ 18.6 Bn |

| Market Value Forecast (2032F) | US$ 65.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 19.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 18.5% |

Market Dynamics

Drivers - Environmental Regulations and Single-Use Plastic Bans

Regulatory frameworks have emerged as the primary catalyst for bioplastics adoption, with the European Union's Single-Use Plastics Directive (SUPD) establishing binding market restrictions on conventional plastics and extending producer responsibility schemes to drive material substitutions. The directive mandates that single-use plastic products, including cutlery, plates, and food containers be removed from the market, creating immediate demand displacement toward biodegradable and compostable alternatives.

Member States, including Germany, have transposed these regulations into stringent national frameworks requiring multi-use alternatives alongside single-use options at equivalent or lower pricing by 2023, forcing packaging manufacturers to accelerate bioplastics procurement. Extended beyond Europe, regulatory momentum encompasses China's nationwide plastic ban implemented in 2025 and Japan's carbon neutrality targets by 2050, creating binding market incentives for bioplastics adoption across Asia-Pacific's 2.51 million tons of current consumption. The regulatory environment has quantified market impact: compliance-driven procurement is expected to contribute approximately 40-50% of incremental bioplastics demand through 2032, with Extended Producer Responsibility schemes covering waste management costs and awareness measures, directly improving the economic proposition for bioplastics manufacturers.

Corporate Sustainability Commitments: Transforming Procurement Patterns

Major global brands and retailers have established binding corporate decarbonization targets that are now translating into preferential purchasing agreements for bio-based materials, representing a fundamental shift from discretionary to contractual bioplastics demand. With an ever-growing number of big brands turning to bioplastic solutions, the market penetration is well on its way. Brands such as Procter & Gamble, Puma, Samsung, IKEA, Tetra Pak, Heinz, Stella McCartney, Gucci and retail leader Iceland UK have already introduced first large-scale products in Europe. Life-cycle assessments demonstrate that NatureWorks' Ingeo PLA formulations reduce carbon footprints by up to 84% relative to conventional polymers, a differential substantial enough to materially impact corporate scope-3 emissions calculations. This environmental performance quantification has strengthened internal business cases for material transitions, with companies including BMW Group confirming that over 25% of polymer materials in select electric vehicle models are now bio-based formulations, and global FMCG companies increasingly adopting bioplastic packaging to align with net-zero commitments.

The resulting procurement pattern shift has unlocked approximately US$ 350 million in project financing from institutional investors for bioplastics production capacity expansion, with Krungthai Bank providing dedicated financing for NatureWorks' 75,000-ton PLA facility in Thailand. This capital deployment dynamic demonstrates how corporate sustainability mandates have transformed bioplastics from niche alternatives to required supply chain components, creating predictable demand foundations that justify large-scale production investments.

Market Restraining Factors

Production Cost Competitiveness and Capital Intensity Barriers

The regulatory landscape for food enzymes presents significant compliance obstacles, particularly across geographically diverse markets with differing regulatory frameworks. The European Food Safety Authority (EFSA) operates a comprehensive authorization process requiring extensive safety documentation and efficacy data for each enzyme application and source strain. Unlike the United States, where regulatory pathways are more streamlined, the EU maintains distinct regulations governing food enzymes and processing aids, creating market fragmentation and compliance costs.

Different national regulatory standards across the Asia-Pacific, Latin America, and Middle East regions necessitate localized product registration and documentation, extending market entry timelines and increasing costs for manufacturers. These regulatory complexities particularly disadvantage smaller regional players while favoring multinational corporations with established regulatory and quality infrastructure.

Bioplastics Market Trends and Opportunities

Textile and Non-Packaging Application Expansion

Bioplastics textile applications are emerging as the fastest-growing segment within non-packaging applications, with biopolymer fibers and fabrics finding commercial deployment in apparel, home textiles, and industrial applications driven by sustainable fashion alternatives and regulatory mandates, including EU textile strategies. This growth potential encompasses synthetic fiber replacement, particularly polyester and polyamide applications, where bio-based alternatives, including PLA fibers, are establishing market traction through performance improvements addressing durability, elasticity, and dyeability limitations historically constraining adoption.

Automotive textile applications including seat fabrics and interior panels have achieved >65% penetration within next-generation electric and hybrid vehicle platforms, with BMW, Volkswagen Group, and other manufacturers specifying bio-based polymer content as part of vehicle sustainability strategies. The global automotive bioplastics market is projected to expand with CAGR of 10.3% through 2035, with bioplastic consumption in automotive reaching approximately 200,000 tons annually by 2032. This application diversification reduces reliance on packaging-centric demand and creates estimated incremental opportunity of US$ 4-6 billion through 2032 from textile and automotive applications alone

Hybrid and Electric Propulsion System Standardization

The convergence toward hybrid propulsion as an industry standard creates substantial opportunities for technology providers, component manufacturers, and innovative shipyards. Current market penetration of hybrid systems remains limited to premium segments, but the declining cost trajectory of lithium iron phosphate battery technology and regulatory pressure for emissions reduction are accelerating mainstream adoption. The December 2024 Wider WiderCat 92 project demonstrates commercial viability of serial hybrid architecture delivering zero-emission cruising capability with practical operational ranges. Market sizing suggests the hybrid Bioplastics segment could expand from current negligible volumes to represent 15-20% of total production by 2032, representing an addressable opportunity of US$ 1.3-1.7 Billion. Opportunities exist for battery manufacturers, electric motor suppliers, and software developers creating integrated propulsion management systems optimizing diesel-electric performance trade-offs.

Bioplastics Market Insights and Trends

Product Type Insights

Biodegradable Bioplastics Lead Global Market Growth Amid Regulatory and Infrastructure Expansion

Biodegradable bioplastics currently dominate the global market with over 60% revenue share and remain the fastest-growing segment, supported by stringent regulations mandating certified compostability and rising consumer demand for materials that break down naturally within controlled timeframes. This category includes PLA, PHA, and starch-based polymers, all capable of achieving industrial compostability within 90–180 days, aligning with emerging standards and public-sector procurement requirements. Growth is further strengthened by rapid infrastructure expansion, with Europe alone set to increase industrial composting capacity by nearly 40% by 2032. Manufacturers such as NatureWorks and TotalEnergies Corbion are expanding PLA output for food packaging, reflecting strong policy-driven momentum, especially across Europe and Asia-Pacific.

In contrast, non-biodegradable bio-based plastics like bio-PET and bio-PE hold under 40% share but benefit from seamless compatibility with existing manufacturing and recycling systems. With materials identical to conventional plastics and offering 30–50% lower emissions, this segment is positioned for steady expansion, particularly in cost-sensitive applications where compostability is not mandatory.

Application Insights

Packaging Dominance and Emerging Textile Applications Driving the Next Growth Wave in the Bioplastics Market

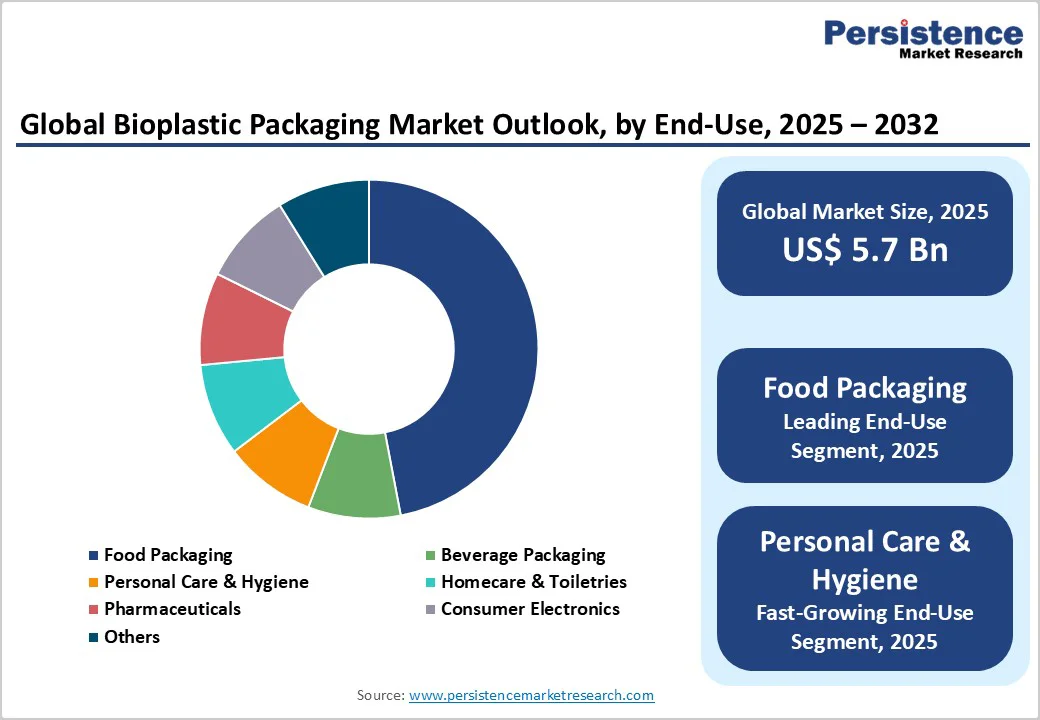

Packaging remains the largest bioplastics application, generating over 60% of global revenue and nearly half of biodegradable plastics consumption. This dominance reflects packaging’s large share of total plastics use and rising regulatory pressure, including the EU Single-Use Plastics Directive, which is accelerating adoption of compostable and bio-based solutions. Demand is further supported by e-commerce and food delivery growth, particularly in developing regions. Rigid bioplastics made from PLA, bio-PE, and bio-PET are increasingly used in cosmetics, beverages, and household products, with major brands such as Coca-Cola, Procter & Gamble, and FMCG leaders adopting plant-based materials at scale. In food packaging, biodegradable films and trays offer strong barrier properties and shelf-life benefits, with ongoing innovations such as antimicrobial coatings making bioplastics performance comparable or superior to conventional plastics.

Textiles are emerging as the fastest-growing bioplastics segment, driven by sustainable fashion trends and policies like the EU Strategy for Sustainable and Circular Textiles. Bio-based polyester and PLA fibers now match conventional polyester performance while offering 40–60% lower emissions. Automotive OEMs are accelerating adoption as well, with more than 65% of next-generation EV platforms specifying bio-based materials for interior fabrics. This segment is expected to reach 150,000–200,000 tons by 2032, growing at a CAGR of 10.3%.

Regional Insights and Trends

Europe Leads the Global Bioplastics Market With Strong Regulations, Advanced Infrastructure, and Innovation Capacity

Europe maintains above 45% of the global bioplastics market revenue share, commanding market leadership through comprehensive regulatory frameworks, established infrastructure, and concentrated production capacity across Germany, the Netherlands, and Italy. Germany alone accounts for over 25% of the European market share and was among the earliest bioplastics adopters, implementing stringent regulations, including single-use shopping bag bans and mandatory compostability certifications, that have created sustained demand growth and attracted significant capital investment.

European government initiatives, including tax exemptions and subsidies for bioplastics manufacturers, combined with a comprehensive recycling infrastructure, have positioned the region as the global bioplastics innovation and production centre, with leading companies, including Novamont (Italy), BASF (Germany), and TotalEnergies Corbion (Netherlands), maintaining substantial production capacity and R&D investments. Germany's well-established recycling systems and the United Kingdom's active investment in eco-friendly packaging infrastructure position these nations as growth engines driving European market expansion through 2032.

North America’s Bioplastics Market Accelerates on Corporate Sustainability Commitments and Expanding State-Level Regulations

North America represents a significant and established bioplastics market characterized by strong corporate sustainability commitments from major packaging and consumer goods manufacturers, though regulatory frameworks remain less comprehensive than European equivalents. The region's bioplastics market is projected to expand at a CAGR of 22.5% through 2032, driven by state-level regulatory initiatives in California, New York, and Washington mandating single-use plastic restrictions and corporate commitments from major retailers, including Walmart, Target, and Amazon, to transition packaging portfolios toward sustainable materials. The United States maintains established production capacity through NatureWorks' facilities in Nebraska and integrated operations across the value chain, positioning the nation as a significant bioplastics manufacturer and consumer.

North American automotive manufacturers are increasingly specifying bioplastic components for vehicle interiors and lightweight structures to achieve fuel efficiency improvements and align with vehicle sustainability targets, with electric vehicle production platforms incorporating bioplastic materials at accelerating rates. This region's growth trajectory reflects commercial rather than regulatory drivers, with market expansion dependent on cost competitiveness improvements and corporate sustainability mandates rather than binding legal requirements

Competitive Landscape

The global bioplastics market exhibits a moderately consolidated competitive structure with five leading companies commanding approximately 45% of market share, while the remaining 55% comprises mid-size manufacturers, regional producers, and emerging technology companies focused on specialized applications and next-generation material formulations. Market leaders including BASF SE, Braskem, Mitsubishi Chemical Corporation, Evonik Industries AG, and TotalEnergies Corbion maintain substantial production capacity, established distribution networks, and integrated supply chains spanning raw material sourcing through end-customer delivery.

This concentrated structure contrasts with conventional plastics markets dominated by petrochemical companies with vastly larger scale, reflecting bioplastics' emerging market status and capital intensity barriers that restrict new entrant participation. The competitive landscape is characterized by differentiation based on raw material sourcing (corn starch, sugarcane, cellulose), polymer chemistry (PLA, PHA, biodegradable polyesters), and application-specific formulations addressing performance requirements across packaging, automotive, textiles, and agriculture sectors. Emerging competitive dynamics include technology-driven startups, including Danimer Scientific, Polymateria, and algae-focused producers, including Notpla and Sway that are challenging incumbent market positions through specialized material innovations and next-generation biodegradable formulations addressing performance gaps and cost competitiveness challenges.

Key Industry Developments

- In May 2025, India marked a major bioplastics milestone with the launch of its first PLA biopolymer brand, Balrampur Bioyug. Developed by Balrampur Chini Mills, the 80,000-tonne renewable-energy-powered plant uses sugarcane feedstock to produce fully biobased, compostable PLA, advancing sustainable plastics and accelerating India’s circular-economy growth.

- In May 2025, the Horizon Europe–funded GRECO project advanced bioplastics by developing innovative PLA-based biodegradable, recyclable food packaging using novel copolymers, green catalysts, and functional coatings. TotalEnergies Corbion’s contribution enhances packaging performance, recyclability, and carbon reduction, supporting sustainable-by-design bioplastic value chains aligned with new EU packaging regulations.

- In 2024, CSIRO and Murdoch University launched an $8 million Bioplastics Innovation Hub to accelerate fully compostable bioplastics. The initiative focuses on creating next-generation, biologically derived plastics that decompose in compost, soil, or water, supporting sustainable packaging innovation and reducing environmental impact across global industries.

Companies Covered in Bioplastics Market

- An Phat Holdings

- Avantium

- BASF

- Braskem S.A.

- ECPlaza Network Inc.

- Futerro

- NatureWorks LLC

- PTT MCC Biochem Co., Ltd.

- SABIC

- Solvay

- Toray Industries, Inc.

- TotalEnergies Corbion

- Toyota Tsusho Corporation

- Trinseo

- TEIJIN LIMITED

- Other Market Players

Frequently Asked Questions

The Bioplastics market is estimated to be valued at US$ 18.6 Bn in 2025

The key demand driver for the global Bioplastics market is the stringent environmental regulations and corporate commitments to reducing plastic waste and carbon emissions.

In 2025, the Europe region will dominate the market with an exceeding 45% revenue share in the global Bioplastics market.

Among applications, packaging has the highest preference, capturing beyond 60% of the market revenue share in 2025, surpassing other applications.

BASF, Solvay, Toray Industries, Inc., Braskem S.A., Futerro, NatureWorks LLC, PTT MCC Biochem Co., Ltd., SABIC are a few leading players in the bioplastics market.