ID: PMRREP3034| 192 Pages | 22 Sep 2025 | Format: PDF, Excel, PPT* | Food and Beverages

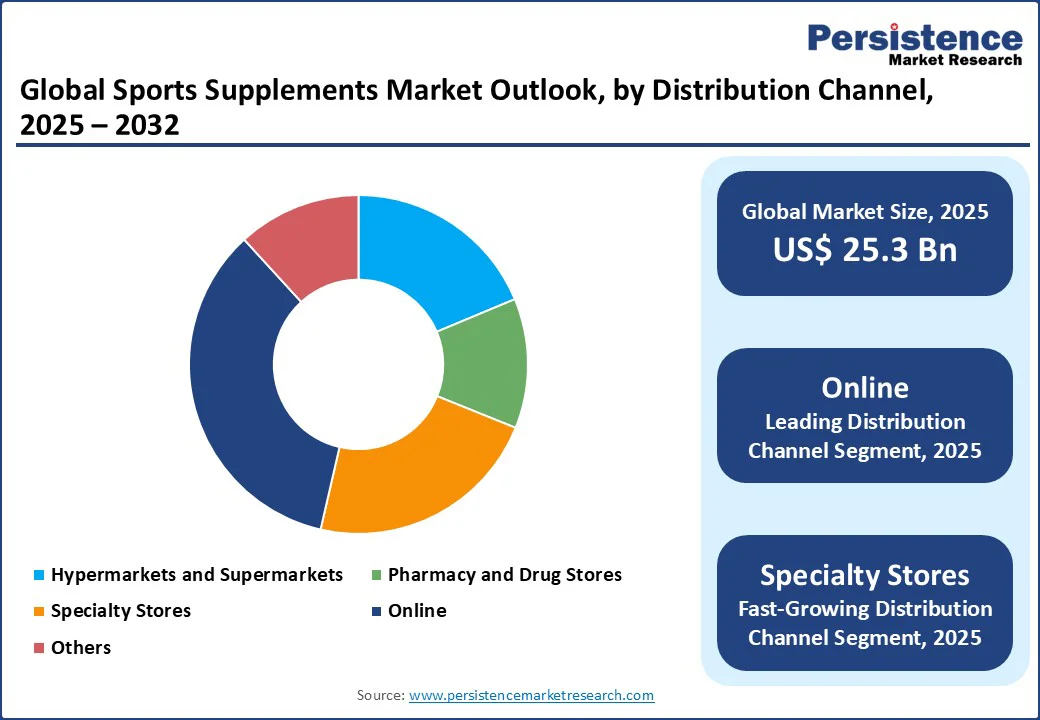

The sports supplements market size is likely to be valued at US$ 25.3 Bn in 2025 and is estimated to reach US$ 43.6 Bn in 2032, growing at a CAGR of 8.1% during the forecast period 2025-2032, fueled by rising consumer interest in preventive health, increased sports and fitness activity participation, and the adoption of personalized nutrition solutions via digital channels.

Key Industry Highlights:

| Key Insights | Details |

|---|---|

|

Sports Supplements Market Size (2025E) |

US$ 25.3 Bn |

|

Market Value Forecast (2032F) |

US$ 43.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.4% |

Global fitness awareness is surging, with more individuals engaged in sports, gymming, and active living. Health campaigns in regions such as the U.S. (Healthy People 2030) and India (Fit India Movement) have spurred demand for nutritional supplements, notably protein powders. According to industry estimates, gym memberships and organized sports participation rose by 18% in key markets from 2020 to 2025, positioning sports supplements as essential performance aids.

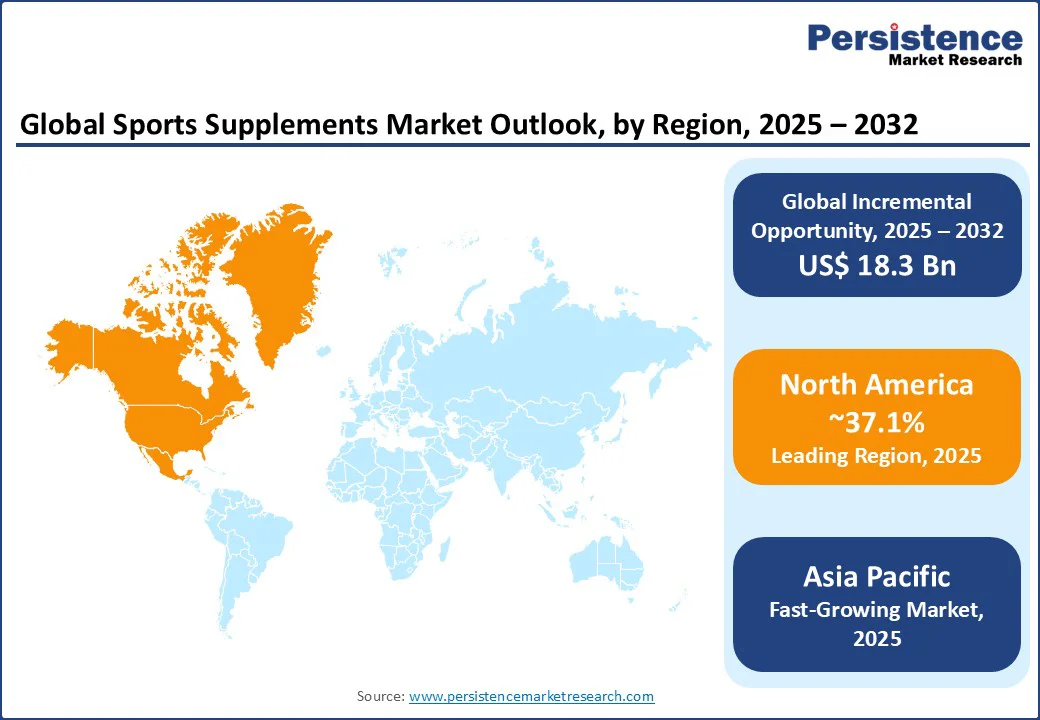

Alongside rising participation, North America continues to dominate the market, supported by superior purchasing power, novel fitness infrastructure, and a deep-rooted gym culture that promotes preventive health practices. In Asia Pacific, steady growth is evident as urbanization and rising disposable income encourage consumers to adopt healthy routines, from yoga and home workouts to structured gym training.

Online retail platforms have lowered entry barriers and broadened product reach. The direct-to-consumer model allows brands to customize product lines and maintain robust consumer engagement. E-commerce ensures rapid expansion, with digital channels reporting a 22% annual increase in purchase frequency since 2022.

E-commerce has fundamentally transformed the sports supplements landscape beyond rapid expansion and increased purchase frequency. Leading online retailers such as Amazon, iHerb, and Flipkart Health+ now carry an extensive portfolio of certified products, increasing accessibility for both mainstream and niche consumer segments.

Sustained growth is stimulated by consumer preferences for clean-label, organic, and plant-based ingredients. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) and European Food Safety Authority as well as industry standards now emphasize transparency and ingredient traceability, fueling investments in product reformulation and certification. As per a new survey, companies allocating over 25% of research and development budgets to clean-label innovation outperformed competitors by 11 to 15% in market growth since 2021.

The shift is not limited to developed markets but is also gaining impetus in Asia Pacific and Latin America, where younger demographics are highly responsive to sustainable and ethical product positioning. Plant-based protein powders, collagen alternatives, and allergen-free formulations are now central to product pipelines, with various brands highlighting non-GMO, gluten-free, and soy-free claims to attract diverse consumer groups.

Complex regulatory frameworks and stringent safety requirements delay product rollouts and raise compliance costs, particularly in Europe and North America. Adverse events linked to substandard ingredients continue to prompt scrutiny, leading to mandatory certifications and recall notices. Approximately 9% of supplement launches in 2024 were delayed based on regulatory findings or incomplete safety documentation.

Sourcing high-quality protein, including dairy and plant-based, and specialty ingredients faces inflationary pressures, with input cost inflation averaging 6.8% annually since 2022. Geopolitical risks and disruptions in global logistics further constrain supply reliability, contributing to product shortages and price volatility. Competitive pricing pressures persist, especially from private labels and new market entrants targeting the budget segment.

Innovations in digital health and wearables facilitate personalized supplement regimens, with over 30% of consumers indicating preference for customized sports nutrition solutions. Companies integrating AI-based recommendation engines and smart packaging are forecast to add US$ 2.1 Bn in revenue by 2028.

Government campaigns promoting physical education and preventive health catalyze market growth. Policy support for research and development grants, flexible import/export policies, and public-private partnerships are creating sustainable growth opportunities that could expand market access by 12 to 18% in target countries through 2028.

The integration of technology into fitness and nutrition is opening powerful new avenues for sports supplement manufacturers. Wearable devices, AI-based fitness apps, and DNA testing kits are increasingly being paired with supplement recommendations, enabling hyper-personalized regimens that strengthen consumer trust and adherence.

Protein supplements dominate the product type category with a share of nearly 67.4% in 2025. Growth is favored by athletes and fitness enthusiasts for their role in muscle building and repair. The segment enjoys robust consumer trust due to proven efficacy and support for both recreational and competitive sports. Key players invest in whey, casein, and plant protein to cater to specific consumer requirements.

Non-protein products such as amino acids, creatine, and mineral blends are increasingly popular with endurance athletes and broad demographic groups. Segment expansion is fueled by technological development and rising awareness of holistic performance support. It will likely record a CAGR of about 8.9% from 2025 to 2032.

Organic products have surged in popularity, fueled by increasing demand for chemical-free nutritional sources and transparent labeling. Continuous product launches and regulatory endorsements consolidate their appeal and market share. Owing to the aforementioned factors, the segment is poised to account for approximately 58.3% of market share in 2025.

Despite organic’s dominance, conventional supplements retain a substantial segment owing to cost accessibility and evolving formulation improvements. Strategic price positioning by high-volume manufacturers supports their expansion. As per research analysts, the segment is predicted to exhibit nearly 9.2% CAGR through 2032.

Digital or online channels have redefined consumer engagement, delivering product diversity, competitive pricing, and supply chain efficiency. The segment leads, supported by investments in omnichannel strategies and robust logistics. It is anticipated to account for about 34.6% of the global market share in 2025.

Specialty stores garner loyalty among informed consumers seeking expert advice and exclusive products. Improved store formats and targeted marketing fuel above-average segment expansion, particularly in urban centers. These factors are responsible for a CAGR of nearly 8.5% for the segment in the forecast period.

North America holds the most prominent share in the global market, with the U.S. accounting for the majority of revenue. It is due to high consumer awareness, government health campaigns, and unique product innovation ecosystems. The regional market is forecast to account for a market share of nearly 37.1% in 2025, propelled by constant product launches and strategic cross-industry partnerships.

Regulatory rigor by FDA and FTC ensures high standards for product safety and transparency, shaping competitive dynamics in compliance and public trust. Investment trends favor digital initiatives as well as research and development in plant-based and personalized nutrition, with leading companies allocating over 15% of annual budgets to these domains.

Asia Pacific, including China, Japan, India, and the ASEAN region, represents the fastest-growing market zone, propelled by manufacturing advantages, urbanization, and evolving consumer health priorities. The regional market is forecast to rise at a CAGR of 9.5% through 2032, outpacing global averages.

Government health initiatives, rising disposable income, and surging digital access support market formation and expansion. Competitive landscape is fragmented with local and international brands competing for high share through pricing, distribution, and product innovation. Investment flows are increasingly directed to infrastructure and localized branding, especially in China and India.

Europe, led by Germany, the U.K., France, and Spain, represents a mature market for sports supplements, marked by regulatory harmonization and proactive sustainability adoption. The market is distinguished by ongoing adoption of organic and clean-label products, supported by EU-wide policies and rigorous labeling requirements.

Market size is projected to surpass US$ 9.2 Bn by 2032, with competitive intensity propelled by multi-country launches and strategic alliances. Key players prioritize agility and compliance, responding to evolving consumer tastes with local production investments and certified supply chains.

The sports supplements market features a mix of global leaders and specialized niche players, exhibiting moderately consolidated characteristics. Top players collectively hold over 38% of the global market share, with constant portfolio expansion and vertical integration strengthening their positions.

Market leaders prioritize innovation, clean-label transparency, and multi-channel distribution. Strategic elements center on ingredient traceability, cost leadership via supply chain optimization, and digital branding, with emerging trends in direct-to-consumer and subscription models.

The sports supplements market is likely to value at US$ 25.3 Bn in 2025.

Rising health consciousness among millennials and growing participation in professional sports are the key market drivers.

The sports supplements market is poised to witness a CAGR of 8.1% from 2025 to 2032.

Transparency in ingredient sourcing and rising demand from emerging markets are the key market opportunities.

Glanbia plc, Abbott Nutrition (Abbott Laboratories), and PepsiCo, Inc. are a few key market players.

| Report Attribute | Details |

|---|---|

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis |

Value: US$ Bn/Mn, Volume: As Applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

By Product Type

By Nature

By Distribution Channel

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author