- Sporting Goods & Equipment

- Kids Sports Equipment and Accessories Market

Kids Sports Equipment and Accessories Market Size, Share, and Growth Forecast, 2026 - 2033

Kids Sports Equipment and Accessories Market by Equipment Type (Protective gears, Nets & goals, Bats & sticks, Balls, Dumbbells), Accessories (Gloves, Bags & backpacks, Headbands & wristbands, Others), and Regional Analysis for 2026 - 2033

Kids Sports Equipment and Accessories Market Size and Trends Analysis

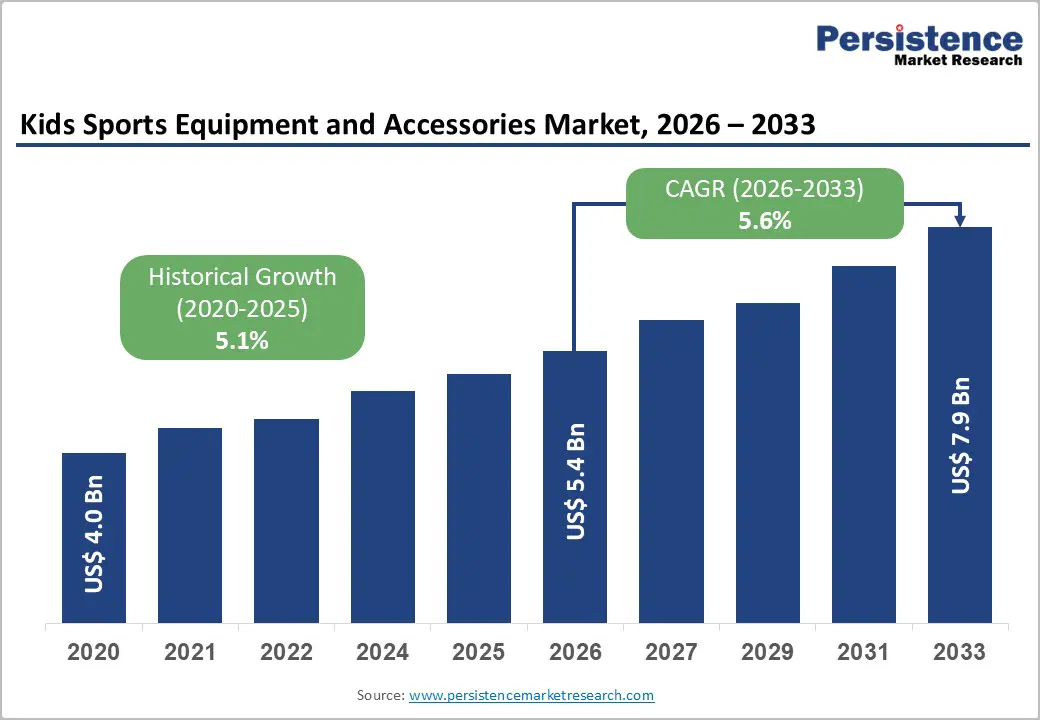

The global kids sports equipment and accessories market size is likely to be valued at US$5.4 billion in 2026 and is expected to reach US$7.9 billion by 2033, growing at a CAGR of 5.6% during the forecast period from 2026 to 2033, driven by structural shifts in consumer behavior and youth engagement in physical activities.

The market is fueled by a rising emphasis from parents on their children's health and the advantages of early sports involvement. Increased participation in school athletics, community leagues, and training programs has led to a surge in demand for child-specific equipment, including protective gear and fitness accessories. Manufacturers are focusing on ergonomic designs, lightweight materials, safety features, and products tailored to children's age groups. The incorporation of technology into wearables and performance trackers appeals to tech-savvy younger consumers, boosting overall engagement.

Key Industry Highlights:

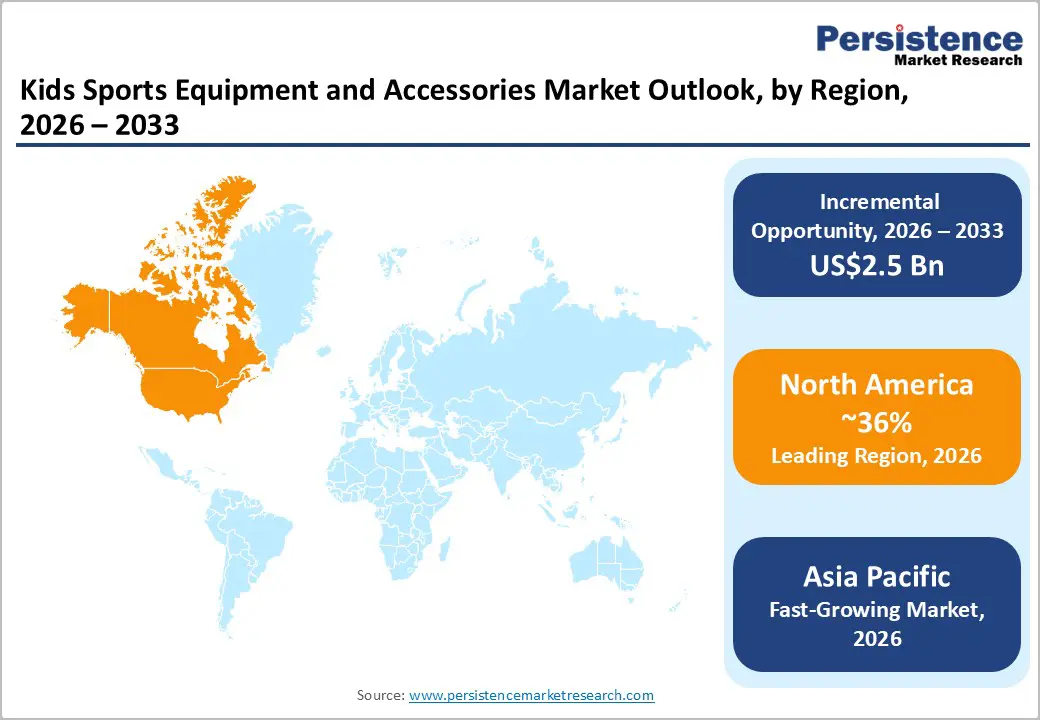

- Leading Region: North America, accounting for a market share of 36% in 2026, driven by strong youth sports participation, advanced infrastructure, and high consumer awareness.

- Fastest-growing Region: Asia Pacific, supported by rising youth participation, expanding middle-class demand, and strong regional manufacturing capabilities.

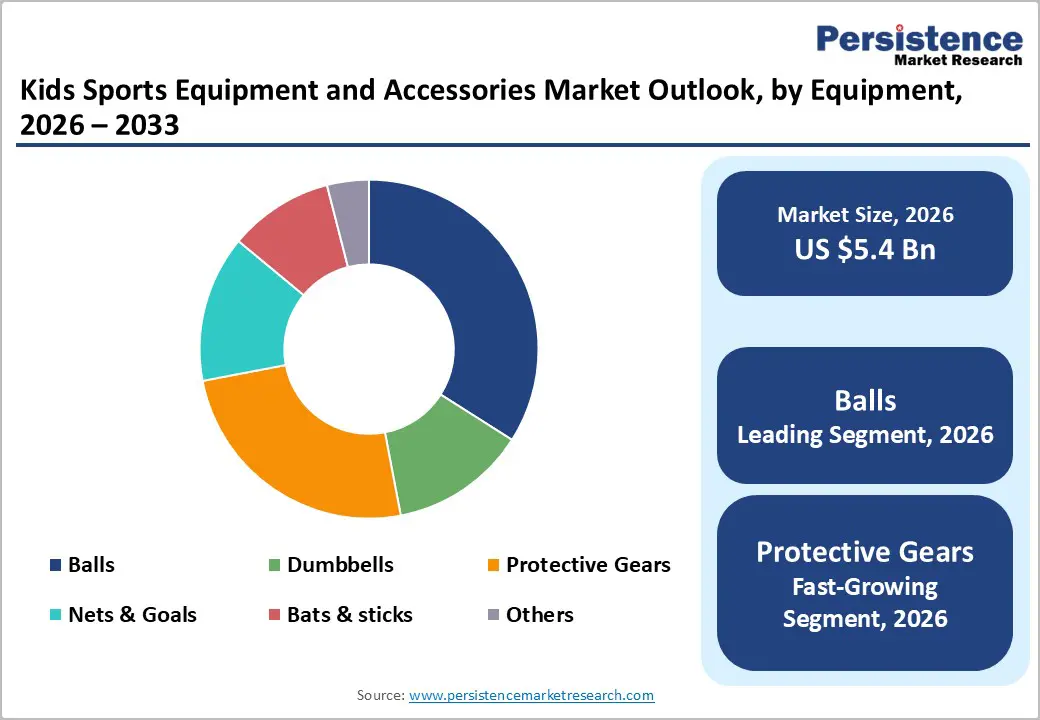

- Leading Equipment Type: Balls, accounting for 38% of the revenue share, driven by their essential use across multiple team sports activities.

- Leading Accessories: Bags and backpacks are expected to hold over 32% of the revenue share in 2026, driven by their widespread use in infrastructure development, building renovations, and surface preparation activities.

| Key Insights | Details |

|---|---|

|

Kids Sports Equipment and Accessories Market Size (2026E) |

US$5.4 Bn |

|

Market Value Forecast (2033F) |

US$7.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Awareness of Childhood Health and Fitness

Increasing concerns regarding sedentary lifestyles, obesity, and long-term health complications have encouraged parents to actively involve children in sports and physical activities. Schools and healthcare professionals consistently advocate structured exercise routines to improve cardiovascular strength, coordination, and mental well-being. This shift in mindset has resulted in higher spending on age-appropriate sports equipment, protective gear, and training accessories. Families increasingly prioritize durable, safe, and ergonomically designed products that support physical development while ensuring comfort and injury prevention during regular sports participation.

Public health campaigns, social media awareness, and pediatric recommendations reinforce the importance of early sports engagement. Parents now see sports not just as fun activities, but as important for building discipline, teamwork, and confidence in children. Demand for high-quality balls, bats, protective equipment, and fitness accessories continues to rise steadily. Manufacturers respond by introducing lightweight materials, safety-certified products, and visually appealing designs tailored to younger users.

Growth in Organized Youth Sports Programs

Schools, academies, community clubs, and private training centers increasingly offer structured leagues and competitive tournaments across multiple sports disciplines. These programs require standardized equipment, protective gear, and sport-specific accessories, creating consistent replacement and upgrade demand. Government initiatives promoting grassroots sports development also contribute to higher participation rates among children. Organized sports environments emphasize safety compliance and performance quality, encouraging parents to purchase certified and durable products.

Rising investments in sports infrastructure, including playgrounds, indoor courts, and training facilities, accelerate market momentum. Competitive exposure motivates families to equip children with reliable gear that enhances skill development and safety. Seasonal tournaments and inter-school competitions generate recurring demand cycles for balls, nets, gloves, and other accessories. Sponsorship programs and partnerships between brands and youth leagues enhance product visibility and credibility. The structured nature of organized sports ensures predictable purchasing behavior, supporting steady revenue streams.

Barrier Analysis - Increasing Competition from Digital Alternatives

The growing popularity of video games, streaming platforms, and mobile-based interactive content reduces children’s available time for outdoor play and structured sports. Easy accessibility to digital devices often shifts leisure preferences toward screen-based engagement rather than physical activity. This behavioral shift can weaken demand for traditional sports gear, particularly in urban households where digital infrastructure is widespread. As recreational patterns evolve, manufacturers face challenges in maintaining consistent participation levels, which directly influence the purchasing frequency of sports equipment and accessories.

Parents balancing academic pressures and digital learning environments may also prioritize indoor activities over outdoor sports. The integration of entertainment technology into everyday life creates strong competition for attention, particularly among older children. Reduced participation in physical sports impacts equipment replacement cycles and lowers impulse purchases linked to recreational play. To mitigate this restraint, companies increasingly incorporate interactive and technology-enabled features into sports accessories to maintain relevance.

Declining Interest in Certain Physical Activities

Certain sports categories experience fluctuating popularity due to changing lifestyle preferences, urban space constraints, and evolving recreational trends. As children gravitate toward modern or alternative activities, demand for equipment tied to less popular sports may soften. Limited playground availability in densely populated areas reduces engagement in outdoor team games. This uneven participation pattern affects category-level growth, particularly for equipment linked to sports, facing reduced enrollment in schools or community programs.

Shifting cultural trends and academic pressures also contribute to reduced time allocated for physical recreation. Some families prioritize extracurricular academic training over sports involvement, affecting consistent participation. When fewer children enroll in specific sports, equipment suppliers may experience slower turnover in related product lines. Seasonal demand volatility becomes more pronounced in regions where interest is inconsistent. Although overall youth sports participation remains stable, uneven sport-specific engagement creates segment-level imbalances.

Opportunity Analysis - Technological Convergence and Wearables

The incorporation of sensors, performance tracking tools, and smart wearables enhances engagement by combining physical activity with data-driven insights. Parents increasingly value real-time activity monitoring, step tracking, and performance metrics that encourage consistent exercise routines. These innovations add measurable value to sports participation and differentiate products in competitive markets. Wearables designed specifically for children focus on safety, lightweight construction, and user-friendly interfaces, broadening adoption potential among younger demographics.

Technology-enabled accessories also create cross-selling opportunities alongside traditional sports gear. Integration with mobile applications fosters gamified experiences that motivate children to remain active. Schools and training academies may adopt performance analytics tools to monitor development and improve coaching outcomes. As digital familiarity grows among younger generations, smart sports accessories align naturally with their lifestyle preferences. Manufacturers investing in research and development can capture premium segments while building brand loyalty through innovative ecosystems.

Rising Female Participation in Youth Sports

Increasing advocacy for gender inclusivity and equal sports access encourages higher enrollment of girls in organized leagues and school programs. As participation expands, demand grows for sport-specific equipment, protective gear, and accessories tailored to female athletes. Brands are responding by developing ergonomically designed products that address comfort, fit, and performance needs. Government initiatives and educational policies promoting gender equality in sports reinforce this opportunity.

Media visibility of female athletes inspires young participants, driving aspirational demand for quality equipment. Product lines featuring diverse color options, design aesthetics, and safety enhancements enhance brand appeal among female consumers. Retailers increasingly allocate shelf space to girls’ sports gear, reflecting growing market recognition. As participation continues to rise, particularly in emerging regions, expanding female engagement will contribute meaningfully to sustained sales growth and category diversification within the broader kids' sports ecosystem.

Category-wise Analysis

Equipment Type Insights

Balls are expected to lead the kids sports equipment and accessories market, accounting for approximately 38% of revenue in 2026, driven by their universal use across multiple team sports. Their demand remains consistently high because sports such as football, basketball, cricket, and volleyball require balls as the primary playing component. Schools, community leagues, and recreational programs frequently purchase balls in bulk for training sessions and tournaments, ensuring steady replacement demand. For example, junior football programs regularly require size-specific footballs designed for children, creating sustained procurement by schools and sports academies.

The protective gear segment is likely to represent the fastest-growing segment, supported by increasing participation in contact and high-impact sports such as football, hockey, skateboarding, and cycling, which has elevated the importance of helmets, knee pads, shin guards, and mouth guards. Schools and sports authorities emphasize compliance with safety standards, encouraging the adoption of certified protective products. For example, youth cricket leagues increasingly mandate the use of protective helmets and pads during matches, leading to higher sales volumes in this category.

Accessories Type Insights

Bags and backpacks are projected to lead the market, capturing around 32% of the revenue share in 2026, supported by their everyday practicality and cross-sport applicability. Regardless of the sport, children require reliable storage solutions to carry uniforms, shoes, protective gear, and water bottles to practices and games. Their utility extends beyond sports into school and travel use, strengthening repeat purchase behavior. For example, multi-compartment sports backpacks designed for youth athletes allow organized storage of cleats, uniforms, and accessories, making them highly preferred by parents and students. Durability, lightweight construction, and ergonomic shoulder support are key features driving consistent demand.

Fitness trackers and wearables are likely to be the fastest-growing accessory type, as technology becomes increasingly integrated into youth lifestyles. These devices enable step counting, activity tracking, heart rate monitoring, and performance evaluation, aligning with parents' interest in structured fitness monitoring. The growing adoption of digital health tools encourages families to combine physical sports participation with measurable outcomes. For example, child-friendly fitness bands designed with simplified interfaces and parental controls are gaining traction among active families. Integration with mobile applications creates engaging experiences, motivating children to achieve activity goals and maintain consistency.

Regional Insights

North America Kids Sports Equipment and Accessories Market Trends

North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by shifting consumer preferences and broader participation trends among youth athletes. Increasing health consciousness among parents and educators has amplified demand for high-quality, safety-certified gear, especially protective equipment and age-appropriate balls tailored to youth sports such as soccer and basketball. School programs and community leagues remain pivotal, encouraging consistent procurement of essentials such as nets, bats, and ergonomic backpacks. E-commerce channels have strengthened market reach, enabling brands to engage directly with families seeking convenience, customization, and fast delivery.

Companies are introducing smart accessories that integrate sensors and performance tracking, encouraging sustained activity through data and gamification. For example, Nike has expanded its youth lineup with digitally-connected wearables and training tools that sync with apps to monitor performance and progress. Sustainability trends are influencing product design, with eco-friendly materials gaining traction among environmentally conscious consumers. Smaller niche brands also capitalize on specialized segments, such as youth fitness equipment for home training, reflecting broader lifestyle shifts post-pandemic.

Europe Kids Sports Equipment and Accessories Market Trends

Europe is likely to be a significant market for kids sports equipment and accessories in 2026, due to a tradition of youth sports participation and well-established grassroots programs across countries such as the U.K., Germany, France, and the Netherlands. Public and private investments in community sports infrastructure, playgrounds, local pitches, and indoor facilities support consistent engagement in team sports such as football, handball, and basketball. Parents increasingly seek high-quality, safety-tested gear, creating steady demand for protective equipment, ergonomic balls, and durable accessories such as bags and water bottles.

Innovation focused on performance and comfort is another defining trend in the European market. Companies are leveraging design enhancements to appeal to both children and parents, emphasizing lightweight construction and safety certification. For example, Puma has strengthened its presence with youth-oriented sports lines featuring improved fit and modern aesthetics, appealing to younger demographics while maintaining brand recognition. Local clubs and leagues often partner with regional brands to introduce tailored equipment suited to specific sports preferences within different European regions.

Asia Pacific Kids Sports Equipment and Accessories Market Trends

The Asia Pacific region is likely to be the fastest-growing region in the kids sports equipment and accessories market in 2026, driven by rising youth sports participation, increasing disposable incomes, and expanding middle-class consumer demand. Governments in countries such as China, India, Japan, and South Korea are actively promoting physical education in schools and community sports initiatives to improve children's health and social development. This has led to higher procurement of core sports gear such as balls, bats, nets, and protective equipment at both grassroots and organized levels.

Innovation and product differentiation are becoming increasingly important as brands strive to capture regional preferences and performance requirements. Manufacturers invest in ergonomically designed equipment tailored for children's age groups, using advanced materials that ensure safety, durability, and comfort. For example, Mizuno has expanded its youth sporting goods portfolio in the Asia Pacific with kid-specific cricket and baseball equipment that incorporates lightweight construction and enhanced handling suited to developing athletes.

Competitive Landscape

The global kids sports equipment and accessories market exhibits a moderately fragmented structure, driven by a mix of large multinational brands and agile regional manufacturers addressing varied consumer needs across age groups and sports categories. Established players leverage strong brand equity, extensive distribution networks, and product innovation to capture significant market share, while local and niche companies compete on customization, pricing, and regional relevance.

With key leaders including Nike, Adidas, Puma, Mizuno, and Under Armour, the landscape balances brand strength with regional offerings. These players compete through diversified product portfolios that range from traditional equipment, such as balls and bats, to innovative accessories, including fitness trackers and ergonomic bags. Emphasis on quality certifications, sustainability initiatives, and digital integration enhances differentiation, while competitive pricing and omnichannel retail strategies improve accessibility.

Key Industry Developments:

- In January 2026, NAMU, an athlete-founded recovery footwear brand based in Los Angeles, announced the launch of its SL01 Active Recovery Slide, designed to support post-performance recovery through biomechanical functionality rather than passive cushioning. Developed by a collective of professional athletes, footwear designers, and movement specialists, the SL01 focuses on restoring natural foot movement after intense training or competition. The recovery slide features a zero-drop platform to maintain natural Achilles alignment, a wide toe box to promote forefoot splay, and a SEED™ textured footbed designed to stimulate sensory activation and proprioception.

- In January 2026, Compass Health Brands announced the expansion of its Picklebalm™ line with the launch of a new Pain Relief Spray, developed in response to growing demand from the pickleball community. The spray introduces a new application format to the brand’s topical pain relief range, which is specifically formulated for pickleball players. The new product features the brand’s C.A.L.M. formula, combining Cucumber Seed Extract, Arnica, 4% Lidocaine, and Menthol to provide targeted relief for common strains associated with pickleball play.

- In February 2026, Spin Master unveiled its 2026 toy portfolio, highlighting five major play trends expected to shape the children’s entertainment market: interactive technology, purposeful skill-building play, high-impact action toys, adult-focused games, and shark-themed adventure products. The company emphasized storytelling, innovation, and immersive interactive experiences as core pillars of its upcoming product strategy. Among the key launches are the Peekimo™ Interactive Pet and Bitzee™ Aquarium under the “InterACTION” trend, focusing on responsive, digital-enhanced companionship toys.

Companies Covered in Kids Sports Equipment and Accessories Market

- Adidas

- Amer sports

- Cabela's

- Epic Sports

- Franklin Sports

- JD Sports

- Mizuno

- Nike

- ProMaxima

- Puma

- Sport smith

- Under Armour

Frequently Asked Questions

The global kids sports equipment and accessories market is projected to reach US$5.4 billion in 2026.

The kids sports equipment and accessories market is driven by rising parental awareness of child health and fitness, growing participation in organized youth sports, and increasing demand for safe, age-appropriate gear.

The kids sports equipment and accessories market is expected to grow at a CAGR of 5.6% from 2026 to 2033.

Key market opportunities include the expansion of smart wearables and tech-enabled accessories, rising female participation in youth sports, and growing demand in emerging markets.

Adidas, Amer Sports, Cabela's, Epic Sports, Franklin Sports, and JD Sports are the leading players.