- Sporting Goods & Equipment

- Air Sports Equipment Market

Air Sports Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Air Sports Equipment Market by Product Type (Container/Harness, Protective Gear, Others), Application (Parachuting, Paragliding, Hang Gliding, Base Jumping), and Regional Analysis for 2026 - 2033

Air Sports Equipment Market Size and Trend Analysis

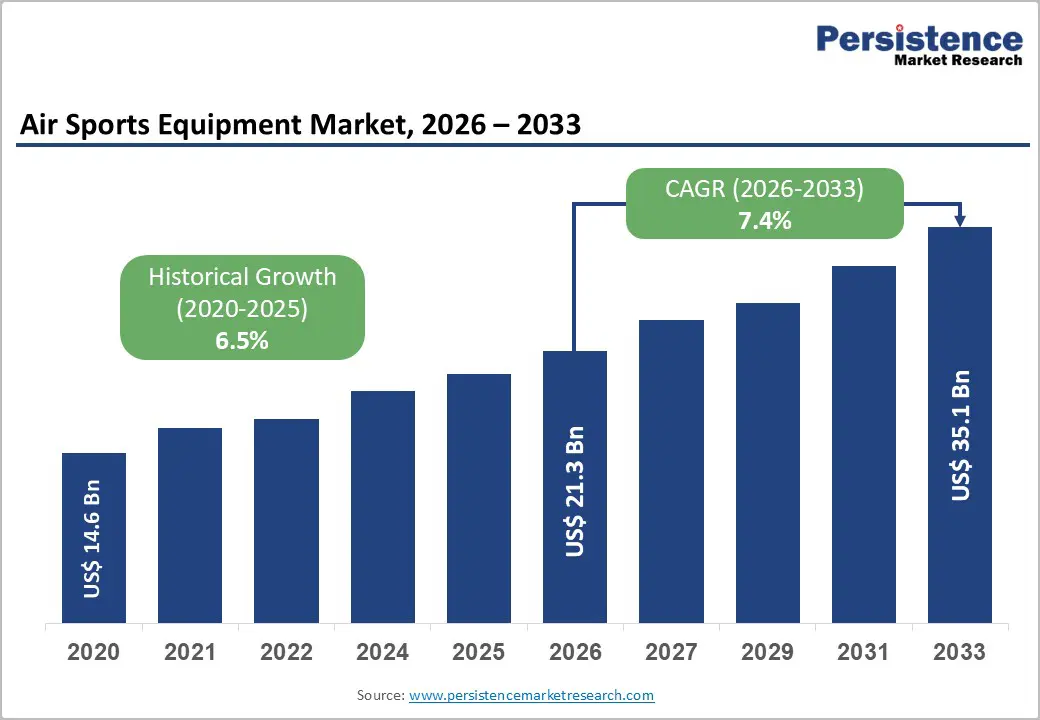

The global air sports equipment market size is valued at US$ 21.5 billion in 2026 and is projected to reach US$ 35.1 billion by 2033, growing at a CAGR of 7.4% between 2026 and 2033.

Rising global participation in aerial recreational activities, particularly paragliding, parachuting, and base jumping, is the primary engine behind this sustained expansion. The broadening of the adventure tourism ecosystem, supported by government-backed initiatives to promote outdoor recreation in key economies such as the United States, Germany, and China, is drawing new participants into the market at a pace.

Simultaneously, continuous breakthroughs in materials science, including lightweight composites, ripstop nylon innovations, and smart equipment integrations, are strengthening demand across both amateur and professional segments globally.

Key Industry Highlights:

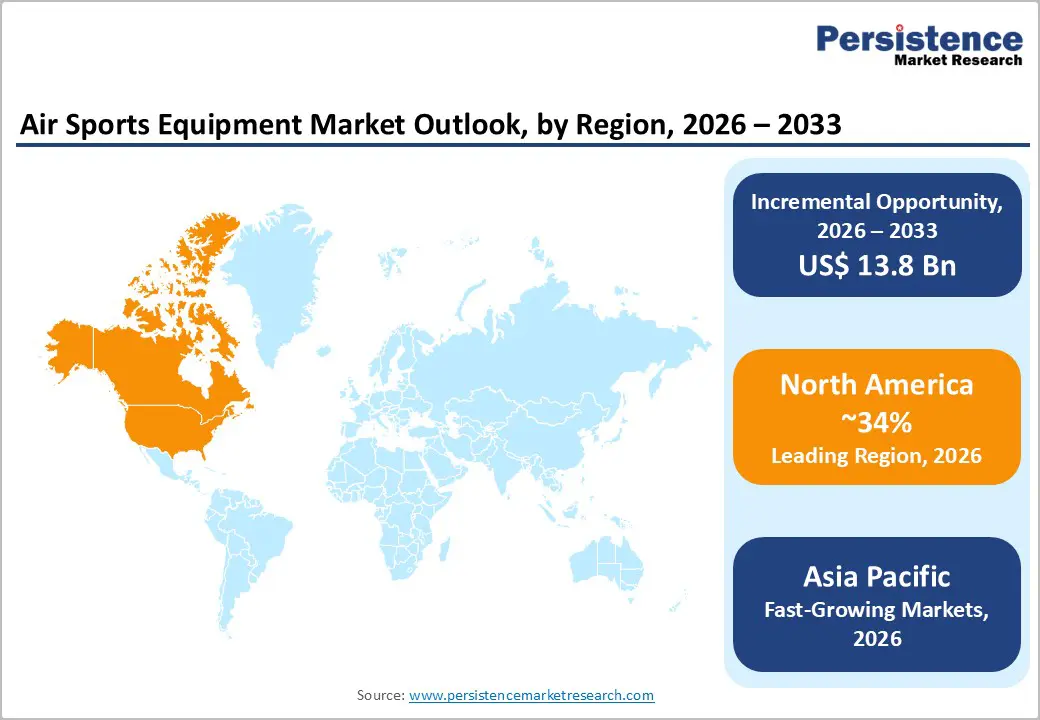

- Leading Region: North America leads the global air sports equipment market with approximately 34% revenue share in 2026, anchored by the United States Parachute Association (USPA) with over 42,400 members, record-low skydiving fatality rates in 2024, and robust government investment in outdoor recreational infrastructure.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR of 9.0% through 2033, powered by China's 2024 Adventure Sports Initiative, rapid expansion of paragliding zones in India and Japan, and rising middle-class disposable incomes.

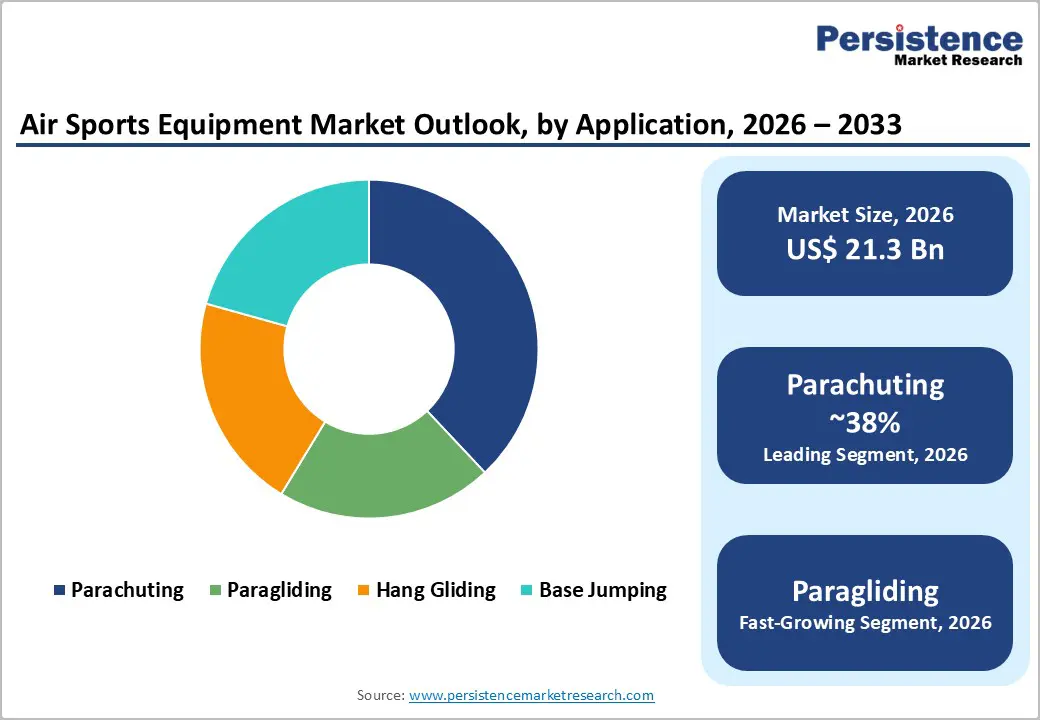

- Dominant Segment: The Container/Harness segment dominates the product type category with approximately 65% market share in 2026, driven by its life-critical role in all air sports disciplines and FAA-mandated safety replacement cycles.

- Fastest Growing Segment: The protective gear segment is the fastest-growing product type, expanding at an estimated CAGR of 8.4%, driven by heightened safety consciousness among paragliding, skydiving, and hang gliding participants and innovations in helmet and protective apparel design.

- Key Opportunity: Smart technology integration, including GPS-enabled flight instruments, AI-powered performance analytics, and ultra-light hybrid wing materials, represents a major product innovation opportunity, particularly in the fast-growing Asia Pacific market, where digitally engaged pilot communities are rapidly expanding.

DRO Analysis

Drivers - Surge in Adventure Tourism Fueling Equipment Demand

The rapid expansion of the global adventure tourism sector has emerged as one of the most potent drivers for the air sports equipment market. According to the United Nations World Tourism Organization (UNWTO), approximately 1.1 billion international tourists traveled in the first nine months of 2024, reaching 98% of pre-pandemic levels, with a notable proportion participating in extreme and adventure activities. The Adventure Travel Trade Association (ATTA) reported a 15% annual growth rate in adventure tourism participation in 2024, encompassing activities such as paragliding and skydiving.

As purpose-built air sports zones proliferate across Switzerland, New Zealand, Turkey, and the United Arab Emirates, and as adventure travel companies expand curated aerial sports packages targeting millennials and Gen Z travelers, demand for premium containers, harnesses, paragliding wings, and protective gear is rising sharply across all market segments.

Rising Skydiving Participation and Safety Investments in North America

North America, led by the United States, represents a mature yet dynamic demand driver for the global air sports equipment market. According to the United States Parachute Association (USPA), 3.88 million skydives were recorded at USPA-affiliated dropzones in 2024, a figure reflecting the extraordinary scale of active participation across the region. The USPA currently maintains a membership base of over 42,400 members, supported by more than 220 affiliated dropzones nationwide.

In 2024, U.S. civilian skydiving fatalities fell to a record low of just nine deaths, the first single-digit fatality year since record-keeping began in 1961, a milestone that materially strengthens public confidence and broadens market accessibility. This combination of high participation volumes, continuously improving safety standards, and government-supported outdoor recreation funding directly stimulates consistent replacement and upgrade cycles for high-value air sports equipment.

Restraints - High Equipment Cost and Maintenance Burden

The high cost of professional air sports equipment continues to act as a structural barrier to market expansion. Premium paragliding kits commonly cost between US$3,000 and US$6,000, while complete skydiving systems, including canopies, containers, altimeters, automatic activation devices, and safety accessories, often exceed US$10,000. Beyond initial purchase prices, owners face recurring expenses linked to inspections, servicing, and compulsory replacement cycles.

In the United States, Federal Aviation Administration regulations require reserve parachutes to be repacked by a certified rigger every 180 days, regardless of usage frequency. Together, these ongoing financial burdens deter an estimated 25% of prospective participants, particularly in developing markets with limited disposable income.

Regulatory Complexity and Airspace Restrictions

Evolving regulatory frameworks and complex airspace governance continue to constrain growth in the air sports equipment market. In the United States, parachute demonstration or exhibition jumps at aviation events or public gatherings require prior authorization from the Federal Aviation Administration, while USPA Basic Safety Requirements limit certain advanced jump categories to D-license holders.

Across Europe, strict EN/LTF safety certification standards for paragliders increase compliance costs and extend product development timelines for manufacturers. Meanwhile, fragmented and inconsistent regulations across emerging markets in Southeast Asia, South Asia, and parts of Africa create regulatory uncertainty, hinder the establishment of training institutions, delay infrastructure development, and ultimately restrict market expansion despite strong underlying demand.

Opportunities - Asia Pacific Emerges as the Growth Engine for Air Sports Participation

The Asia Pacific region offers a major growth opportunity for air sports equipment manufacturers, driven by rising disposable incomes, a rapidly expanding middle class, and stronger government support for adventure sports infrastructure. China, India, and Japan are actively investing in dedicated outdoor recreation facilities to encourage participation in aerial sports.

China’s 2024 Adventure Sports Initiative has accelerated the development of new paragliding zones in Yunnan and Sichuan, while India continues to strengthen its adventure tourism sector through national promotion policies. Destinations such as Bir Billing in Himachal Pradesh have gained global recognition as leading paragliding hubs.

Smart Equipment and Lightweight Material Innovation

The integration of digital technologies and advanced materials is creating a high-value growth avenue in the air sports equipment market. Smart variometers, GPS-enabled flight instruments, AI-driven performance analytics, and real-time monitoring systems are increasingly being incorporated into paragliders and skydiving rigs, significantly enhancing pilot safety and performance insights.

Leading manufacturers such as Ozone Paragliders, NOVA Performance Paragliders, and Skywalk GmbH & Co. KG are advancing ultra-light wing designs using hybrid materials, optimized cell structures, and improved collapse resistance to serve the expanding hike-and-fly segment. Electronic instruments and smart accessories remain the fastest-growing product category.

Category-wise Insights

Product Type Insights

The container/Harness segment leads the global air sports equipment market by product type, representing around 65% of total revenue in 2026. Containers and harnesses are essential, life-critical components used across all aerial sports, including parachuting, skydiving, paragliding, and base jumping. They house reserve parachutes and serve as the primary interface between the pilot and equipment during flight.

Regulatory requirements further strengthen this segment’s dominance, as the FAA mandates that reserve parachutes be repacked by certified riggers every 180 days, ensuring steady replacement demand. Ongoing innovations, such as lightweight nylon and ripstop fabrics, ergonomic pod designs, and airbag-integrated cocoon harnesses, continue to drive premium upgrades and repeat purchases among experienced users worldwide.

Application Insights

The parachuting application segment accounts for the largest share of global air sports equipment revenue, contributing roughly 38% of the market in 2026. This leadership is driven by the sport’s long-established institutional foundation and well-organized operational infrastructure, particularly across North America and Europe. Government-affiliated bodies such as the United States Parachute Association and the Canadian Sport Parachuting Association sustain high and consistent participation levels through extensive dropzone networks and standardized safety frameworks.

The USPA alone recorded 3.88 million jumps in 2024, highlighting the scale of commercial and recreational activity. In addition, steady procurement from military and defense organizations across NATO countries provides a stable, non-cyclical demand base for advanced parachuting systems, reinforcing the segment’s durable market position.

Regional Insights

North America Air Sports Equipment Market Trends & Analysis

North America holds the leading position in the global air sports equipment market, contributing an estimated 34% share of total global market revenue in 2026. The region's dominance is underpinned by deep cultural affinity for aerial sports, a robust institutional framework anchored by the United States Parachute Association (USPA), and active government support for outdoor recreational activities.

U.S. Air Sports Equipment Market Size

The United States is the single largest country market within North America, estimated at approximately US$ 5.2 Bn in 2026. With 3.88 million recorded skydives in 2024, an active USPA membership exceeding 42,400 participants, government-funded expansion of outdoor recreation zones, and the presence of world-class domestic manufacturers, the U.S. market is expected to maintain its dominant position through 2033.

Europe Air Sports Equipment Market Trends, Drivers, & Insights

Europe is the second-largest regional market, holding approximately 30% of the global market share in 2026. The region benefits from world-class paragliding and hang gliding infrastructure across its iconic mountain ranges, including the Alps, Pyrenees, and Dolomites. European nations, including France, Germany, Switzerland, Italy, and the United Kingdom, feature among the highest global penetration markets for aerial sports.

Germany Air Sports Equipment Market Size

Germany represents the largest individual European market for air sports equipment, estimated at approximately US$ 1.5 Bn in 2026, supported by a vibrant paragliding culture concentrated in the Bavarian Alps region and strong domestic manufacturing capabilities across harness, wing, and protective gear categories.

U.K. Air Sports Equipment Market Size

The United Kingdom market is valued at approximately US$ 1.0 Bn in 2026, sustained by a growing network of organized skydiving clubs, increasing recreational participation among millennials and working professionals, and consistent demand for premium containers and canopy systems.

France Air Sports Equipment Market Size

France is estimated at approximately US$ 1.2 Bn in 2026, driven by iconic international paragliding destinations such as Chamonix and Annecy, which attract both domestic pilots and international adventure tourists throughout the year, generating substantial seasonal and year-round equipment demand.

Asia Pacific Air Sports Equipment Market Drivers & Analysis

Asia Pacific is the fastest-growing regional market within the global air sports equipment industry, projected to expand at a CAGR of approximately 9.0% between 2026 and 2033, outpacing all other regions. The combination of rising disposable incomes, rapidly expanding middle-class populations, and government-led adventure sports programs is catalyzing demand at an accelerating pace.

China Air Sports Equipment Market Size

China is estimated at approximately US$ 2.1 Bn in 2026, underpinned by government-driven infrastructure investment, the proliferation of adventure sports zones across southwestern provinces, and the increasing participation of urban middle-class consumers in aerial recreational activities.

India Air Sports Equipment Market Size

India is valued at approximately US$ 0.8 Bn in 2026, with Bir Billing in Himachal Pradesh, recognized as one of Asia's premier paragliding destinations, attracting both domestic enthusiasts and international visiting pilots, while government adventure tourism promotion programs drive increasing market participation.

Japan Air Sports Equipment Market Size

Japan accounts for approximately US$ 0.6 Bn in 2026, driven by growing interest in recreational aerial sports among urban professionals and a culturally embedded preference for high-quality, safety-certified equipment that sustains consistent premium product demand across all air sports categories.

Competitive Landscape

The global air sports equipment market exhibits a moderately fragmented competitive structure, characterized by a diverse mix of specialized manufacturers, niche product innovators, and regional suppliers. Market leaders, including Ozone Paragliders, NOVA Performance Paragliders, and Aerodyne Research LLC, differentiate through continuous R&D investment, safety certification leadership, and broad global dealer network coverage. Emerging business model trends include equipment rental services and subscription-based safety inspection programs designed to broaden participation by reducing barriers to entry.

Key Developments:

- March 2026: France-based Supair announced the launch of its new Strike 3 lightweight paragliding harness, targeting performance-oriented and hike-and-fly pilots in the air sports equipment market. The third-generation harness is designed to deliver an optimal balance between weight, comfort, and performance, eliminating the need for trade-offs across different flying conditions.

- March 2026: Supair unveiled its fifth-generation Delight 5 cross-country paragliding harness, designed to enhance pilot comfort, safety, and long-distance flight performance in the air sports equipment market. The new model is approximately 300 grams lighter, around a 10% reduction compared to its predecessor, while maintaining durability and ergonomic support.

- April 2026: Skywalk GmbH & Co. KG announced the Fly Jacket Design 2026, developed in collaboration with Salewa, targeting performance-oriented paragliding pilots in the air sports equipment market. The high-performance insulation jacket is specifically engineered for cold-weather flying, long cross-country (XC) missions, and off-season conditions.

Top Companies in Air Sports Equipment Market

- Ozone Paragliders (United Kingdom) is one of the world's foremost paraglider manufacturers, renowned for competition-grade wings and a culture of innovation embedded since the company's founding in 1998. The company commands a strong global distribution network spanning over 60 countries and maintains one of the broadest portfolios across EN certification levels, from beginner to expert, encompassing cross-country wings, paramotors, and hike-and-fly solutions.

- Aerodyne Research LLC (United States) is a premier U.S.-based manufacturer of high-performance parachute systems, specializing in canopies and container systems for the skydiving segment. The company is a key supplier to both commercial dropzones and institutional military customers, leveraging deep materials engineering expertise and rigorous compliance with FAA and USPA safety standards.

- NOVA Performance Paragliders (Austria) is a highly regarded Austrian paraglider manufacturer with over three decades of design heritage, recognized internationally for engineering excellence across recreational and competitive product lines. The company has consistently pioneered safety-first design philosophies, including advanced reserve parachute integration and sophisticated cell structure engineering, along with material innovations that have set benchmarks for the European market.

Companies Covered in Air Sports Equipment Market

- Ozone Paragliders

- SUP'AIR

- Velocity Sports Equipment

- Aerodyne Research LLC

- Advance Paragliders

- Skywalk GmbH & Co. KG

- NOVA Performance Paragliders

- Niviuk Paragliders

- Dudek Paragliders

- Sun Path Products, Inc.

- Peregrine Manufacturing, Inc.

- Gin Gliders Inc.

- Performance Designs Inc.

- BGD (Bruce Goldsmith Design)

- Apco Aviation Ltd.

Frequently Asked Questions

The global Air Sports Equipment Market is valued at US$ 21.5 Bn in 2026 and is projected to reach US$ 35.1 Bn by 2033, expanding at a CAGR of 7.4% during the 2026 - 2033 forecast period. This growth is driven by rising adventure tourism participation, increasing skydiving and paragliding activity globally, and continuous innovation in equipment technology and materials.

The primary demand drivers include the rapid expansion of global adventure tourism, with the United Nations World Tourism Organization (UNWTO) recording 1.1 billion international tourist arrivals in the first nine months of 2024, rising skydiving participation (3.88 million USPA jumps in 2024), government investment in outdoor recreation infrastructure, and accelerating innovation in lightweight materials, smart variometers, and GPS-integrated flight systems.

The Container/Harness segment dominates the Product Type category, holding approximately 65% of total market revenue in 2026. Its dominance is driven by the segment's life-critical role across all air sports disciplines and mandatory regulatory replacement cycles, including the FAA requirement for certified parachute riggers to repack reserve parachutes every 180 days in the United States.

North America is the leading regional market, accounting for approximately 34% of global market revenue in 2026. The region's dominance is supported by robust institutional infrastructure from the United States Parachute Association (USPA), government-funded outdoor recreation programs, record participation levels, and the presence of leading manufacturers such as Aerodyne Research LLC and Sun Path Products, Inc.

The integration of smart technologies, including GPS-enabled flight instruments, AI-powered performance analytics, and ultra-light hybrid wing materials, represents the most significant forward-looking opportunity for market participants. Combined with the rapid expansion of air sports adoption across the Asia Pacific (projected 9.0% CAGR through 2033), manufacturers prioritizing R&D investment in next-generation connected and lightweight products are positioned to capture high-value, first-mover growth.

Key players in the global Air Sports Equipment Market include Ozone Paragliders, SUP'AIR, Aerodyne Research LLC, NOVA Performance Paragliders, Skywalk GmbH & Co. KG, Niviuk Paragliders, Advance Paragliders, Dudek Paragliders, Sun Path Products, Inc., Peregrine Manufacturing, Inc., and Gin Gliders Inc.