- Pharmaceuticals

- Intracranial Therapeutic Delivery Market

Intracranial Therapeutic Delivery Market Size, Trends, Share, Growth, and Regional Forecast, 2025 - 2032

Intracranial Therapeutic Delivery Market by Therapy (Cell-based Therapy, Gene Therapy, Enzyme Replacement Therapy), by Indication (Spinal Muscular Atrophy (SMA), Multiple Sclerosis, Batten Disease, Amyotrophic Lateral Sclerosis), and Regional Analysis from 2025 - 2032

Intracranial Therapeutic Delivery Market Share and Trends Analysis

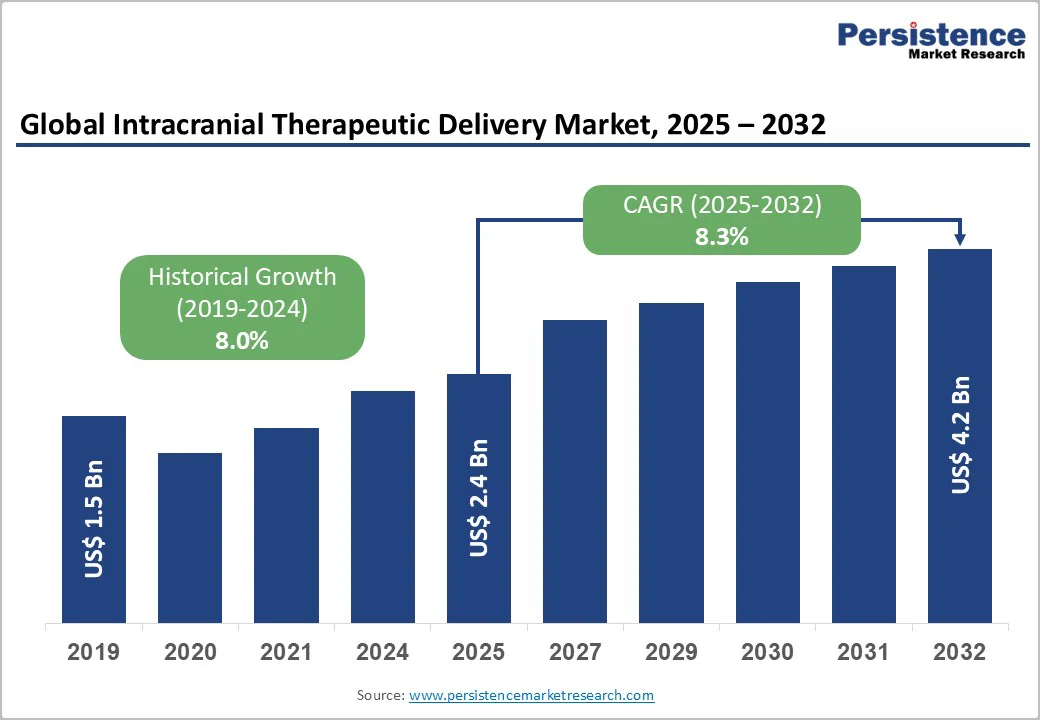

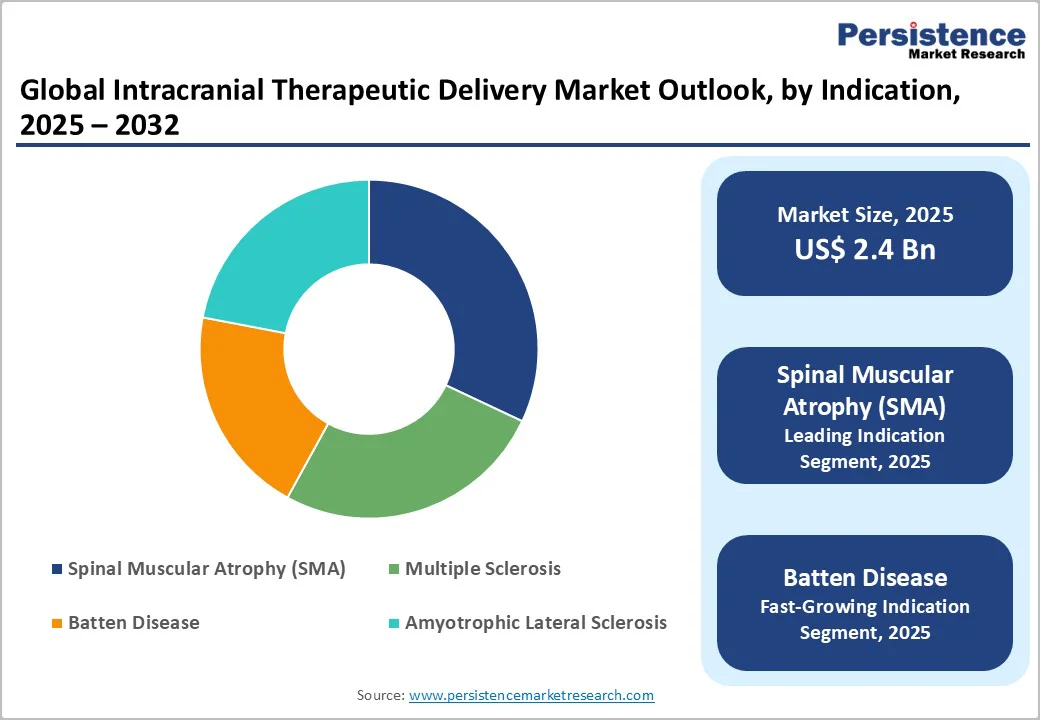

The global intracranial therapeutic delivery market size is valued at US$2.4 billion in 2025 and projected to reach US$4.2 billion, growing at a CAGR of 8.3% during the forecast period from 2025 to 2032.

The intracranial therapeutic delivery industry is growing rapidly as demand for targeted treatments that bypass the blood–brain barrier and deliver drugs directly into the CNS increases. Advances in gene therapy, cell therapy, and biologics are driving the adoption of specialized delivery systems such as intrathecal pumps, catheters, and convection-enhanced delivery devices. The increasing prevalence of neurological disorders, including SMA, Batten disease, multiple sclerosis, and brain cancers, supports market expansion. Improved neurosurgical techniques, strong R&D pipelines, and expanding clinical trials further accelerate adoption.

Key Industry Highlights

- Growing limitations of systemic therapies and the need to bypass the blood–brain barrier are accelerating demand for intracranial delivery approaches.

- Intracranial delivery is becoming essential for administering gene and cell therapies that require precise CNS targeting.

- Gene therapy dominates this market because it requires direct, targeted delivery into the CNS, making intracranial routes essential.

- SMA dominates the intracranial therapeutic delivery market because most approved and late-stage therapies for SMA rely on CNS-targeted delivery, making intrathecal or intracranial routes essential.

| Key Insights | Details |

|---|---|

|

Intracranial Therapeutic Delivery Market Size (2025E) |

US$2.4 Bn |

|

Market Value Forecast (2032F) |

US$4.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

8.0% |

Market Dynamics

Driver - Growing Need to Bypass the Blood-Brain Barrier

The growing need to bypass the blood–brain barrier (BBB) is a major driver of the intracranial therapeutic delivery market. Most systemic drugs fail to reach adequate concentrations in the central nervous system because the BBB blocks over 98% of small molecules and nearly all biologics. This limits treatment outcomes for conditions such as gliomas, SMA, and neurodegenerative diseases. Intracranial delivery provides a direct route into the brain or cerebrospinal fluid, ensuring higher bioavailability, precise targeting, and reduced systemic toxicity. As therapies become more complex, especially gene therapies, viral vectors, and large biologics, clinicians increasingly rely on intracranial approaches to achieve meaningful therapeutic effects.

Restraints - High Therapy Costs and Limited Reimbursement Hindering Market Growth

The intracranial therapeutic delivery market faces significant challenges due to the extremely high cost of cell- and gene-based therapies and limited reimbursement pathways available. One-time treatments such as Zolgensma for spinal muscular atrophy are priced in millions, reflecting complex development processes and the substantial clinical benefit they provide. However, such high upfront costs place a heavy financial burden on patients, healthcare providers, and national health systems.

Medicare and private insurers often do not fully cover advanced therapies, leaving hospitals responsible for substantial co-payments. For instance, Medicare covers only 65% of CAR-T therapy costs under NTAP, forcing hospitals to absorb the remaining 35%. Insurers also delay coverage decisions for clinical-stage therapies due to financial risk considerations. Together, these factors, high treatment prices and inadequate reimbursement mechanisms, restrict patient access, discourage hospital adoption, and impede overall market expansion despite strong therapeutic potential.

Opportunity - Next-Generation Convection-Enhanced Delivery (CED) Technologies

Next-generation Convection-Enhanced Delivery (CED) technologies offer significant growth potential by overcoming the limitations of traditional intracranial infusion. Advanced systems now integrate real-time MRI guidance, precision pressure-regulated pumps, and multi-port fiber-based catheters, enhancing control over flow rate and distribution patterns. These improvements ensure deeper, more uniform penetration of therapeutics across brain tissue, particularly benefiting biologics, viral vectors, nanoparticles, and gene therapies that require high-accuracy placement. With rising demand for targeted CNS treatments, CED platforms are increasingly positioned as essential tools for neurosurgeons and biotech developers. Their ability to reduce systemic toxicity and improve therapeutic outcomes creates a substantial commercial opportunity.

Category-wise Analysis

By Therapy Insights

Gene therapy holds the highest share in the intracranial therapeutic delivery market because it relies heavily on direct CNS administration to achieve effective targeting, especially for disorders where the blood–brain barrier limits systemic treatment. Many leading and emerging therapies for SMA, Batten disease, and other genetic neurological disorders use AAV or similar viral vectors, which require intracranial routes. Gene therapies also command premium pricing, significantly boosting revenue contribution compared to cell-based or enzyme replacement therapies. Strong regulatory support, expanding clinical pipelines, and the potential for long-term or one-time disease modification further reinforce gene therapy’s dominance within this market segment.

By Indication Insights

Spinal Muscular Atrophy (SMA) accounts for the largest share of the intracranial therapeutic delivery market because most approved and emerging SMA treatments require direct CNS delivery to effectively target motor neurons. High-value therapies, including gene therapies and antisense oligonucleotides, drive significant revenue due to premium pricing and specialized administration procedures. SMA also has a strong clinical focus, with widespread newborn screening, early diagnosis, and high treatment uptake globally. As a severe pediatric disorder with urgent unmet need, SMA attracts substantial R&D investment and regulatory prioritization, accelerating adoption of intracranial delivery methods. This concentration of advanced, high-cost therapies makes SMA the dominant indication.

Region-wise Insights

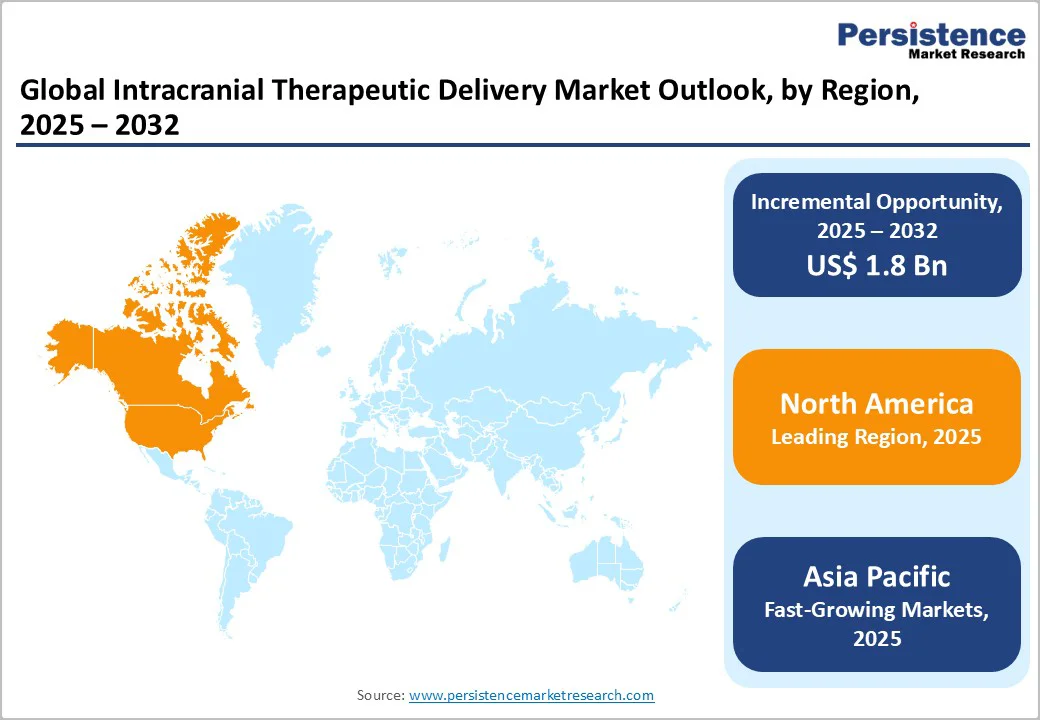

North America Intracranial Therapeutic Delivery Market Trends and Analysis

North America leads the intracranial therapeutic delivery market due to its strong neurology research ecosystem, early adoption of advanced drug-delivery technologies, and extensive availability of specialized neurosurgical infrastructure. The region benefits from high investment in gene and cell therapy programs, a robust clinical trial pipeline, and strong collaboration between biotech companies and academic medical centers. The U.S. drives most regional growth, with rapid uptake of intracranial delivery tools for SMA, Batten disease, brain tumors, and emerging gene-editing therapies. Favorable FDA pathways, strong reimbursement support for rare-disease treatments, and the presence of leading innovators further reinforce North America’s dominance in this highly specialized market.

Asia Pacific Intracranial Therapeutic Delivery Market Share Analysis

Asia Pacific intracranial therapeutic delivery market is emerging rapidly as countries invest in advanced neurology care, gene therapy research, and modern neurosurgical infrastructure. Growing diagnoses of pediatric neurodegenerative disorders, rising awareness of targeted CNS treatments, and improved access to specialized hospitals are accelerating adoption.

Japan, South Korea, China, and India are expanding clinical trial participation, particularly for gene and cell therapies requiring intracranial administration. Increasing healthcare spending, supportive regulatory reforms, and collaborations with global biotech firms further strengthen regional growth. As demand for precision CNS therapies increases, the Asia Pacific is becoming a key hub for innovation, clinical development, and future market expansion.

Competitive Landscape

Through different market consolidation initiatives, major firms in the intracranial therapeutic delivery sector are collaborating on research, production, and distribution of intracranial therapeutic delivery products. It is anticipated that cooperative business strategies will help secure future growth and market position.

Mergers and acquisitions are also anticipated to support the research and development of potent therapeutic lines for the management of severe diseases. Additionally, leading firms in the intracranial therapeutic delivery market are concentrating on winning approvals, launching new products, and making acquisitions to increase their market revenue.

Key Industry Developments:

- In July 2025, Sironax, a clinical-stage biotech company focused on developing transformational therapies for age-related diseases, announced that it had entered into a strategic agreement with Novartis. Under this agreement, Sironax granted Novartis an exclusive option to acquire its proprietary Brain Delivery Module (BDM) platform, a differentiated BBB-crossing technology designed to enhance brain delivery of multiple therapeutic modalities. Sironax retained the right to continue developing selected therapeutic assets using the platform.

Companies Covered in Intracranial Therapeutic Delivery Market

- Novartis AG

- BioMarin

- CORESTEM Inc.

- Alaunos Therapeutics, Inc.

- Apic Bio

- Stemedica Cell Technologies, Inc.

- Voyager Therapeutics

- Bayer AG

- Abeona Therapeutics

- Spark Therapeutics

- Other

Frequently Asked Questions

The global market is projected to be valued at US$2.4 Bn in 2025.

The Global Intracranial Therapeutic Delivery Market is driven by the rising prevalence of neurological disorders such as SMA, Batten disease, gliomas, and neurodegenerative conditions that require targeted CNS treatment.

The global market is poised to witness a CAGR of 8.3% between 2025 and 2032.

Innovation in real-time imaging, pressure-controlled pumps, and multi-port catheters offers significant commercial potential for safer and uniform drug distribution.

Novartis AG, BioMarin, CORESTEM Inc., Alaunos Therapeutics, Inc., and others.