- Pharmaceuticals

- Cancer Gene Therapy Market

Cancer Gene Therapy Market Size, Share, and Growth Forecast 2026 - 2033

Cancer Gene Therapy Market by Therapy Type (Immunotherapy, Gene Transfer, Oncolytic Virotherapy, Gene Editing), by Vector (Viral Vectors, Non-Viral Vectors), Cancer Type (Blood Cancers, Solid Tumors), End-user (Hospitals & cancer centers, Research institutes & labs, Specialty clinics, Biopharma & manufacturing companies), and Regional Analysis, 2026 - 2033

Cancer Gene Therapy Market Share and Trends Analysis

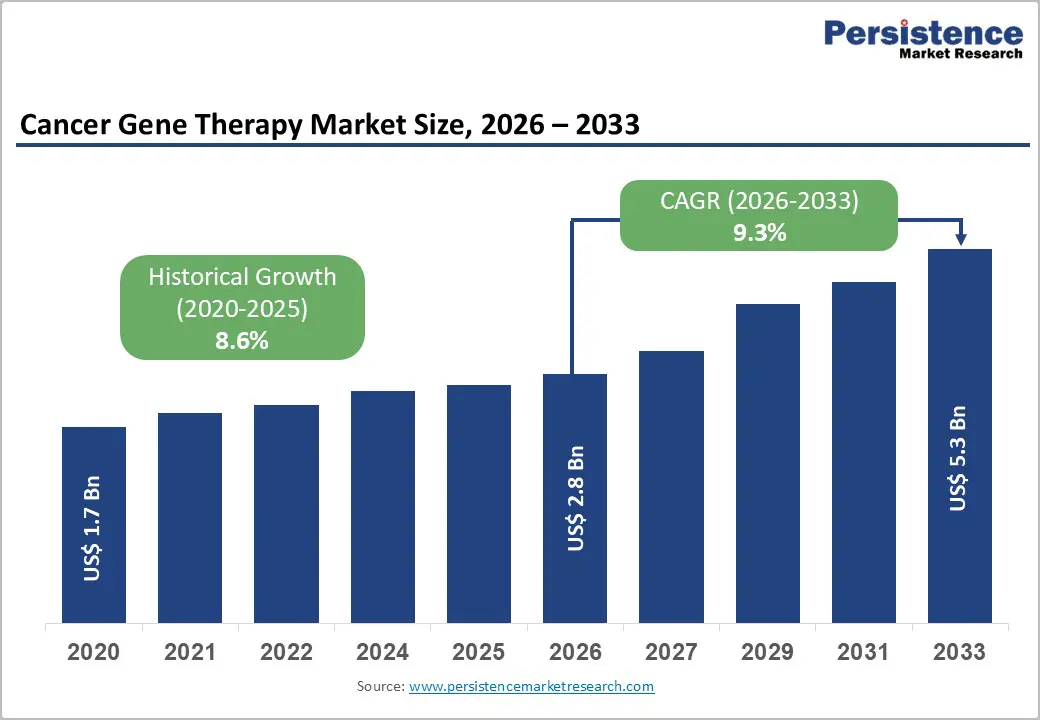

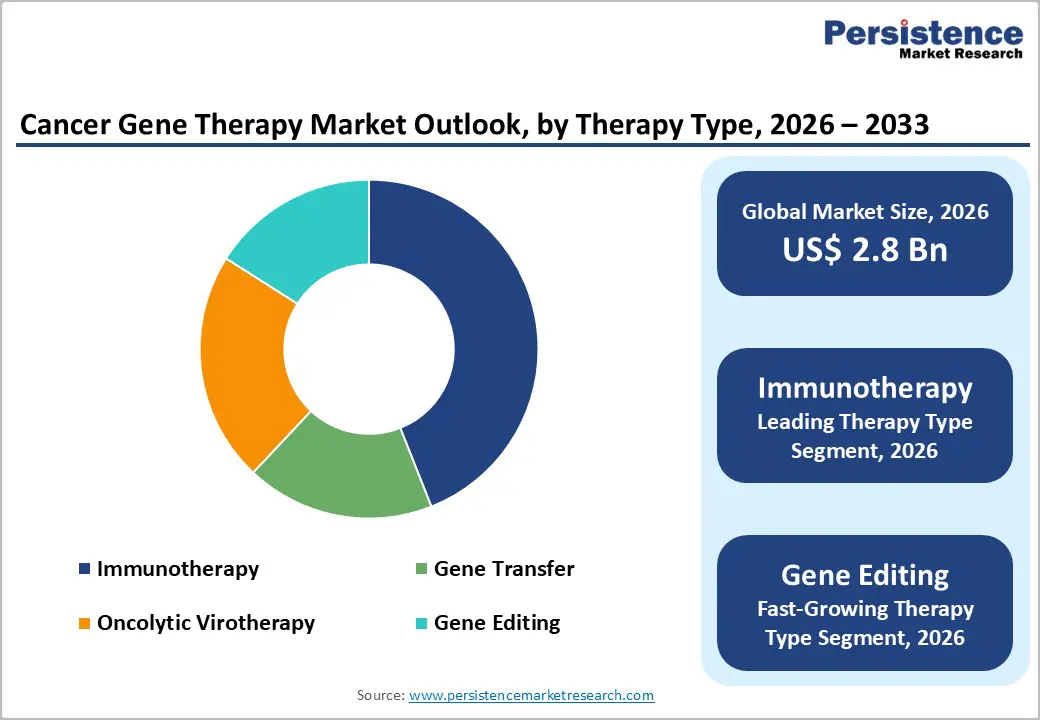

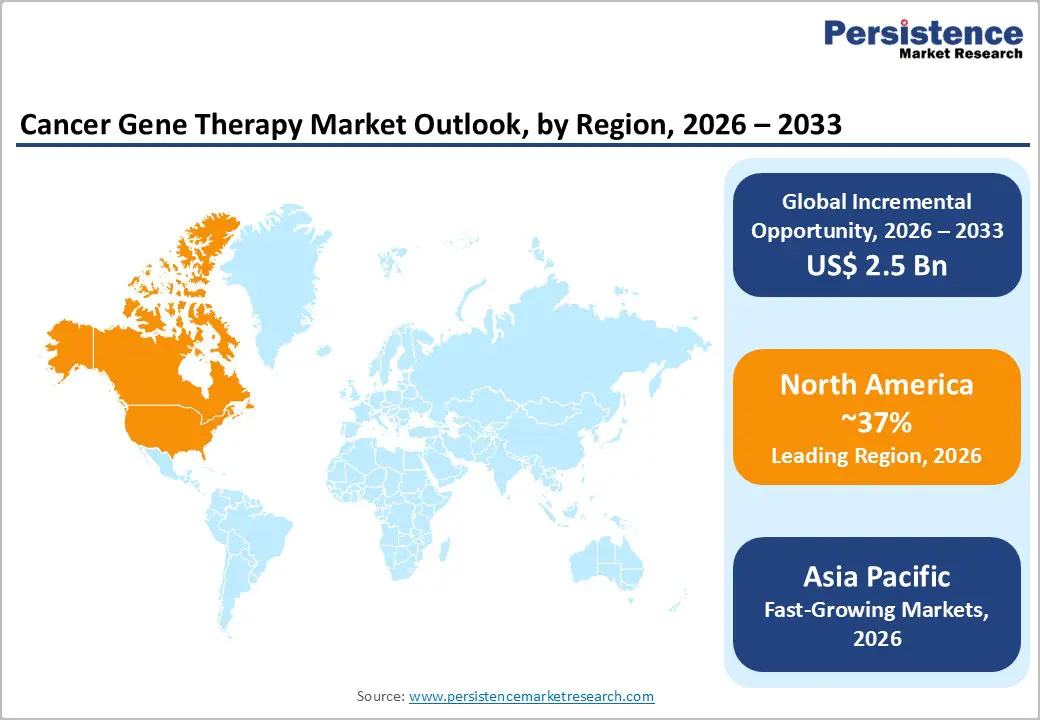

The global cancer gene therapy market size is expected to be valued at US$ 2.8 billion in 2026 and projected to reach US$ 5.3 billion by 2033, growing at a CAGR of 9.3% between 2026 and 2033. The market's robust expansion is primarily driven by transformative regulatory approvals and breakthrough clinical innovations.

The U.S. FDA approved seven new cell and gene therapies in 2024, demonstrating sustained regulatory momentum following 2023's landmark year. Notable approvals include Iovance Biotherapeutics' Amtagvi, the first tumor-infiltrating lymphocyte therapy for solid tumors, and Adaptimmune's Tecelra, the first engineered T-cell receptor therapy for cancer. These regulatory victories validate the therapeutic paradigm shift toward precision oncology, while expanding clinical trial pipelines with over 1,580 CAR-T trials registered globally, and 95% of oncolytic virus trials targeting oncology indications signal accelerating commercialization potential. The convergence of CRISPR-Cas9gene editing breakthroughs with established immunotherapy platforms is unlocking curative possibilities for previously treatment-resistant malignancies, fundamentally reshaping the therapeutic landscape.

Key Market Highlights:

- Leading Region: North America leads the cancer gene therapy market with around 37% share in 2025, supported by the United States’ strong innovation ecosystem, pioneering FDA approvals for multiple oncology gene therapies, and evolving reimbursement models that increasingly recognize the long term value of one-time, potentially curative treatments.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, underpinned by China’s high volume of CAR-T and gene therapy trials, supportive national policies, and expanding manufacturing infrastructure across China, Japan, India, and emerging ASEAN markets, which collectively position the region as both a demand and supply engine.

- Dominant Segment from Therapy Type: Immunotherapy remains the dominant therapy segment with about 44% share in 2025, anchored by approved CAR T products such as Kymriah and Yescarta, which have demonstrated high remission rates in relapsed or refractory blood cancers and established operational and regulatory playbooks for subsequent entrants.

| Key Insights | Details |

|---|---|

|

Cancer Gene Therapy Market Size (2026E) |

US$ 2.8 Bn |

|

Market Value Forecast (2033F) |

US$ 5.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.6% |

Market Dynamics

Drivers - Accelerating Regulatory Momentum and Clinical Trial Expansion

The unprecedented acceleration in regulatory approvals constitutes a foundational growth catalyst for cancer gene therapy commercialization. Between 2023 and 2025, the U.S. FDA greenlit an estimated seventeen novel cell and gene therapies spanning diverse oncological applications, with a substantial share utilizing accelerated pathways for life-threatening conditions. The FDA's Center for Biologics Evaluation and Research (CBER) has explicitly committed to expediting advanced therapy approvals through refined regulatory frameworks and guidance for sponsors. This regulatory tailwind extends globally, with China's NMPA approving multiple CAR-T and gene therapy products, including JW Therapeutics' Carteyva for lymphoma, demonstrating converging global standards. Systematic reviews indicate more than 1,100 CAR T trials initiated between 2020 and 2024, with China leading in trial volume and the U.S. and Europe sustaining robust late-phase pipelines. Strengthening Phase II/III advancement rates and growing real world evidence in hematologic malignancies collectively de risk investment and accelerate time to market trajectories across platforms.

CRISPR Cas9 Integration Revolutionizing Precision Oncology

The integration of CRISPR-Cas9gene editing into oncology is fundamentally transforming therapeutic precision, durability, and personalization. CRISPR technologies allow targeted inactivation of oncogenes, repair of tumor suppressor pathways, and engineering of immune cells with enhanced tumor killing capabilities. Early clinical data from CRISPR-edited T cells in refractory cancer patients have shown encouraging safety and signals of anti-tumor activity, supporting broader investigation in solid and hematologic tumors. Research published through NIH-backed and academic consortia highlights CRISPR’s ability to improve CAR T functionality by knocking out exhaustion-associated receptors and enhancing resistance to immunosuppressive tumor microenvironments. Preclinical work demonstrates effective targeting of mutations such as KRAS and TP53, historically considered difficult to treat, opening new frontiers in precision oncology. Alongside nuclease-based editing, emerging base and prime editing technologies aim to reduce off-target and double-strand break-associated risks, reinforcing CRISPR’s role as a central innovation engine within cancer gene therapy.

Restraints - Manufacturing Complexity and Scalability Challenges

The autologous, patient-specific manufacturing model of many cancer gene therapies, particularly CAR T and cell-based approaches, creates substantial scalability and cost barriers. Each batch must be produced from an individual patient’s cells under strict GMP conditions, requiring sophisticated facilities, a specialized workforce, and a robust chain of identity tracking. Viral vector production, especially AAV and lentiviral vectors, faces bottlenecks around vector yield, capsid quality, and purification, with several assessments identifying vector supply as one of the most critical constraints for the broader gene therapy industry. Industry analyses and peer-reviewed studies report complex multi-week manufacturing cycles and high failure rates in early implementations, which inflate costs and limit timely access. The resulting therapy prices, often in the hundreds of thousands of dollars per treatment, reflect these underlying operational challenges and remain a hurdle for healthcare systems and payers despite strong clinical value.

Insertional Mutagenesis and Long-Term Safety Concerns

Safety concerns related to insertional mutagenesis and long-term oncogenic risk continue to temper adoption and inform cautious regulatory oversight. Integrating viral vectors, such as gammaretroviral and lentiviral systems, can insert near proto-oncogenes or disrupt tumor suppressor genes, theoretically triggering secondary malignancies. Historical experiences in early gene therapy trials for hematologic and metabolic disorders documented leukemias associated with vector insertion events, which led to revised vector designs and intensified long-term follow-up requirements. More recently, safety reviews of certain gene therapies, such as those using lentiviral vectors in rare disease settings, have reported cases of hematologic cancers emerging years after treatment, prompting label warnings and comprehensive post marketing surveillance. Regulators now typically require 15 year or longer follow-up for many gene therapy products, influencing trial design, sponsor obligations, and risk-benefit assessments in oncology indications where patients may achieve durable remissions.

Opportunities - Gene Editing Expansion into Solid Tumor Applications

Solid tumors represent one of the most compelling expansion opportunities for cancer gene therapy, given their large share of global cancer incidence and mortality. Historically, most approved and late-stage gene-modified cell therapies have focused on blood cancers, where targets such as CD19 and BCMA are well-defined and accessible. However, recent breakthroughs, including the FDA approval of Amtagvi (lifileucel) as the first tumor-infiltrating lymphocyte therapy for advanced melanoma and progress in engineered T cell receptor (TCR) therapies, indicate growing feasibility in solid tumors. Oncolytic virotherapy clinical trials also show that over 90% of ongoing studies are directed at solid tumors such as melanoma, glioblastoma, and pancreatic cancer, leveraging virus-mediated oncolysis and in situ vaccination effects. Gene editing technologies such as CRISPR-Cas9 are increasingly being applied to overcome critical hurdles in solid tumors, such as antigen heterogeneity, immunosuppressive microenvironments, and T cell exhaustion, through multiplexed editing of receptors, checkpoints, and trafficking molecules. As more durable responses are documented and combination strategies with checkpoint inhibitors mature, the solid tumor segment is poised to become a key growth engine for cancer gene therapy.

Category-wise Analysis

Therapy Type Insights

Immunotherapy is the leading therapy type, accounting for about 44% market share in 2025 within cancer gene therapy, driven primarily by CAR T cell therapies and related gene-modified immune cell products. Landmark products such as Kymriah (tisagenlecleucel) from Novartis and Yescarta (axicabtagene ciloleucel) from Gilead/Kite have demonstrated high complete remission rates in relapsed or refractory B-cell malignancies, with trials reporting overall response rates often exceeding 70% in certain indications. These strong outcomes, along with durable responses in subsets of patients, underpin continued uptake in eligible populations. The concentration of clinical activity also reinforces this leadership: comprehensive reviews of CAR T trials show that immunotherapy-based approaches dominate gene-modified cancer therapy pipelines worldwide. At the same time, gene editing-based immunotherapies, including CRISPR-engineered T cells designed to enhance persistence and tumor recognition, are emerging as the fastest-growing therapy type, reflecting intense R&D focus and expanding early phase trial activity.

Vector Insights

Viral vectors represent the dominant vector category in cancer gene therapy, with an estimated ~65–70% share in 2025, owing to their high transduction efficiency, established clinical track record, and supportive regulatory precedents. Lentiviral and retroviral vectors remain the backbone for ex vivo modification of T cells and hematopoietic stem cells, enabling stable integration and long term expression of therapeutic constructs. AAV vectors, although more commonly used in in vivo gene therapies for monogenic diseases, also contribute to oncology programs where sustained gene expression or tumor-targeted delivery is advantageous. Several analyses of the viral vector and viral vector manufacturing markets highlight strong growth expectations, reflecting robust demand from approved and pipeline products. Non-viral vectors, including lipid nanoparticles and physical delivery methods, remain a smaller but faster-growing segment, leveraged particularly in mRNA-based immunotherapies and certain gene editing applications where transient expression and favorable safety profiles are desired. Improvements in non-viral delivery efficiency and tissue targeting are expected to gradually diversify vector choices over the forecast period.

Cancer Type Insights

Blood cancers currently account for the largest share of cancer gene therapy usage, with an estimated ~60%+ market share in 2025, reflecting the concentration of current approvals in leukemias, lymphomas, and multiple myelom. Clinical data for CD19-directed CAR T products in acute lymphoblastic leukemia and diffuse large B cell lymphoma demonstrate high response and remission rates in patients who have exhausted conventional options, which have supported favorable health technology assessments and reimbursement decisions in several high-income markets. The clear antigen profiles, accessibility of malignant cells, and well-validated endpoints in hematologic oncology have made blood cancers natural early adopters of gene-modified therapies. In contrast, solid tumors, though historically more challenging due to heterogeneity and hostile microenvironments, are emerging as the fastest-growing cancer type segment. Regulatory approval of TIL therapy for melanoma, expanding TCR T programs targeting solid tumor antigens, and an increasing pipeline of oncolytic virus candidates collectively support double-digit growth prospects for solid tumor applications across the forecast horizon.

End-user Insights

Hospitals and cancer centers are the leading end-user group, accounting for an estimated ~50%+ market share in 2025, reflecting the need for highly specialized infrastructure and multidisciplinary expertise to deliver cancer gene therapies safely. CAR T administration, for example, requires certified centers with capabilities in leukapheresis, intensive monitoring for cytokine release syndrome and neurotoxicity, and access to tocilizumab and critical care support. Major academic medical centers and comprehensive cancer institutes in the U.S., Europe, and Asia have become primary hubs for both clinical trials and commercial administration. Over time, biopharma and specialized manufacturing companies are becoming an increasingly important end user segment from a value chain perspective, as they invest in in-house or partnered production capacity for vectors and cell products. The strong projected growth of the viral vector and vector manufacturing markets underscores this trend, as contract development and manufacturing organizations expand their role in supplying clinical and commercial gene therapy programs worldwide.

Regional Insights

North America Cancer Gene Therapy Market Trends and Insights

North America leads the global cancer gene therapy market with an estimated 37% share in 2025, underpinned by the United States’ unmatched R&D ecosystem, deep venture and biopharma funding, and pioneering regulatory framework. The FDA has approved multiple cell and gene therapies for oncology indications, with agencies projecting that 10–20 such products per year could reach the market in the coming years. The U.S. hosts many of the world’s leading academic centers in this field, including the University of Pennsylvania, Memorial Sloan Kettering Cancer Center, and MD Anderson Cancer Center, which have been central to CAR-T development and early-stage gene-editing trials.

The region also benefits from evolving reimbursement and access models. The Centers for Medicare & Medicaid Services (CMS) has introduced outcome-based and innovative payment mechanisms for high-cost cell and gene therapies, seeking to align one-time therapy costs with long term clinical benefits. Commercial payers are increasingly adopting coverage policies for approved oncology gene therapies, though prior authorization and center-of-excellence models remain common. Parallel expansion of manufacturing capacity by companies such as Novartis and Gilead, along with the growth of U.S.based contract manufacturers, is gradually easing supply constraints. Collectively, these factors reinforce North America’s role as the reference market for new cancer gene therapy launches.

Asia Pacific Cancer Gene Therapy Market Trends and Insights

Asia Pacific is the fastest-growing market for cancer gene therapy, for broader gene therapy markets through the early 2030s. China has emerged as a global leader in clinical trial volume for CAR-T and other cell-based therapies, with hundreds of registered studies across hematologic and solid tumors. Supportive government policies, high disease burden, and growing biotech clusters have fostered a vibrant ecosystem of domestic developers and manufacturing facilities. Regulatory authorities such as the National Medical Products Administration (NMPA) have granted approvals for locally developed CAR-T therapies, signaling increasing maturity and confidence in advanced therapy oversight.

Beyond China, Japan leverages its regenerative medicine laws, which allow conditional early approvals for advanced therapies, and hosts a growing number of oncology-focused cell and gene therapy projects. India and several ASEAN markets are progressively building capacity in biologics and viral vector production, often at cost structures favorable compared with Western facilities, which can attract global outsourcing and technology transfer. Rising healthcare expenditure, expanding cancer screening programs, and broader insurance coverage in middle-income Asian economies will further support demand for innovative oncology treatments. As global developers increasingly prefer Asia Pacific for both trial enrollment and manufacturing partnerships, the region’s role in the cancer gene therapy value chain is expected to deepen substantially.

Competitive Landscape

The cancer gene therapy market is highly competitive and innovation-driven, characterized by rapid technological advancements and expanding clinical pipelines. Competition is centered on developing safer and more effective viral and non-viral delivery systems, improving manufacturing scalability, and achieving durable treatment responses. Companies are focusing on next-generation platforms such as gene editing and enhanced immune-cell engineering to differentiate their portfolios. Strategic collaborations, licensing agreements, and research partnerships are common to accelerate product development and regulatory approvals. The market also faces challenges related to high therapy costs, complex production processes, and stringent regulatory requirements, pushing players to invest heavily in R&D and advanced manufacturing capabilities.

Key Developments:

- In February 2026, a first-of-its-kind inhalable gene therapy for lung cancer received fast-track designation from the U.S. Food and Drug Administration (FDA) after demonstrating encouraging early clinical results. The therapy was administered as an inhaled mist, using a modified harmless virus to deliver immune-stimulating genes directly into lung cells to enhance the body’s ability to fight tumors.

Companies Covered in Cancer Gene Therapy Market

- Novartis AG

- Gilead Sciences, Inc.

- Bristol‑Myers Squibb Company

- Amgen Inc.

- bluebird bio, Inc.

- Adaptimmune Therapeutics

- CRISPR Therapeutics AG

- Legend Biotech

- Cellectis

- Spark Therapeutics (Roche)

- Sangamo Therapeutics

- Astellas Pharma

- Others

Frequently Asked Questions

The global cancer gene therapy market is expected to be valued at US$ 2.8 billion in 2026, supported by accelerating regulatory approvals, a rapidly expanding CAR-T and cell therapy clinical pipeline, and the first wave of solid tumor‑focused gene‑modified therapies reaching commercialization.

Key demand drivers include strong clinical efficacy of CAR‑T and related immunotherapies in relapsed or refractory blood cancers, rapid progress in CRISPR‑Cas9 and other gene editing technologies, growing regulatory support for advanced therapies, and increasing incidence of cancers where conventional treatments have limited curative potential.

North America, led by the United States, is the leading region, benefiting from early-mover regulatory approvals, dense clusters of academic and industry innovators, high healthcare spending, and relatively advanced reimbursement frameworks for high-cost, high-value cell and gene therapies.

The most significant opportunity lies in extending gene-based and cell-based therapies into solid tumors, leveraging TIL and TCR-T platforms, oncolytic virotherapy, and gene editing senhanced constructs to address high-mortality cancers such as melanoma, lung, pancreatic, and certain sarcomas, where unmet need remains substantial.

Major players include Novartis AG, Gilead Sciences, Inc., Bristol-Myers Squibb Company, Amgen Inc., bluebird bio, Inc., Adaptimmune Therapeutics, CRISPR Therapeutics AG, Legend Biotech, Cellectis, Spark Therapeutics, Sangamo Therapeutics, Astellas Pharma, and an expanding group of specialized biotechs and regional developers in North America, Europe, and Asia Pacific.