- Medical Devices

- Intracranial Stents Market

Intracranial Stents Market Size, Share, and Growth Forecast, 2026 - 2033

Intracranial Stents Market by Product Type (Balloon Expanding Stents, Self-Expanding Stents, Others), Disease Indication (Brain Aneurysm, Arteriovenous Malformations, Others), End-user (Ambulatory Surgery Centers, Hospitals, Others), and Regional Analysis 2026 - 2033

Intracranial Stents Market Size and Trends Analysis

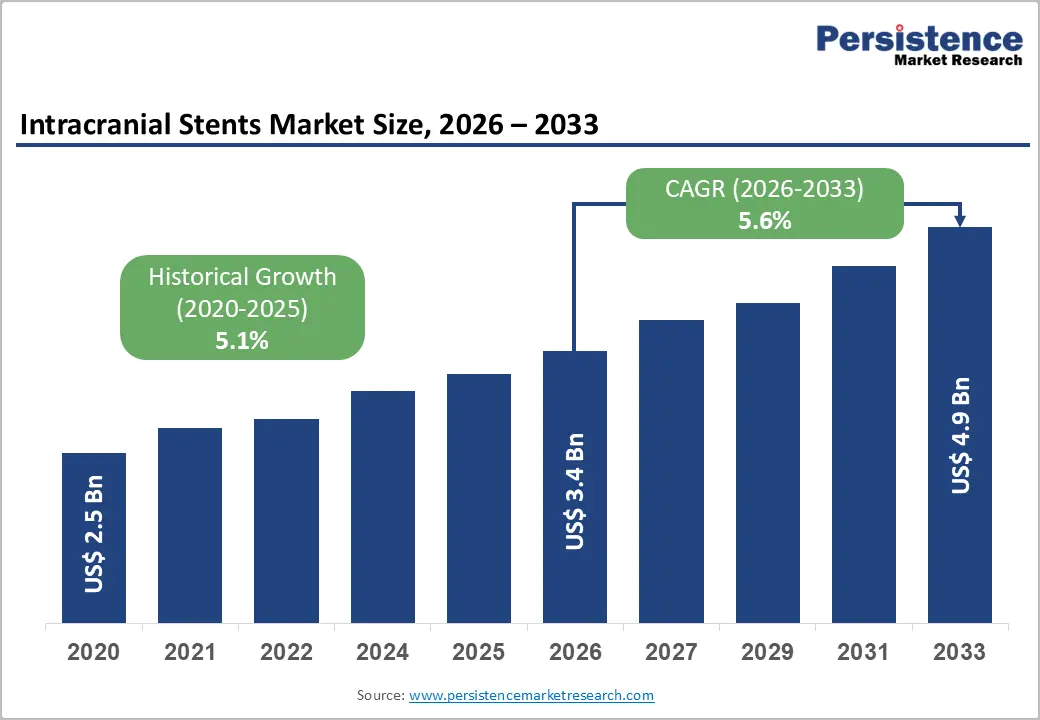

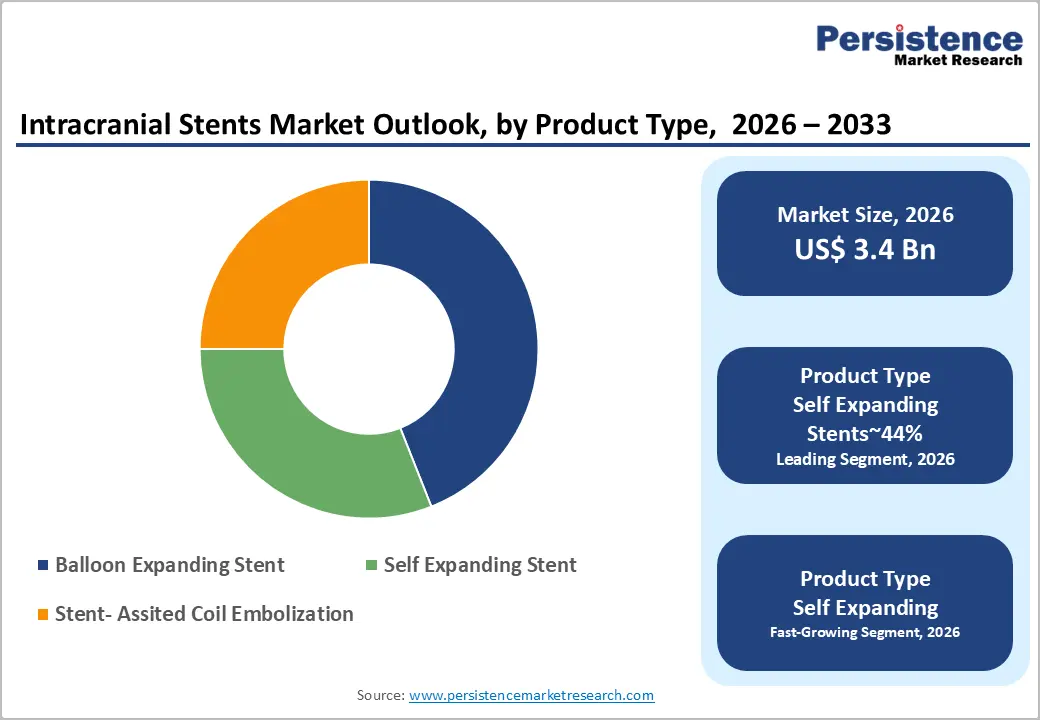

The global intracranial stents market size is likely to be valued at US$3.4 billion in 2026 and is expected to reach US$4.9 billion by 2033, growing at a CAGR of 5.6% during the forecast period from 2026 to 2033, driven by rising incidences of cerebrovascular diseases globally. Technological advancements in minimally invasive neuro-interventions are set to enhance procedural outcomes. Increasing healthcare infrastructure in emerging economies is positioned to drive sustained market demand.

The transition toward flow-diverter systems continues to reshape clinical treatment paradigms for aneurysms. Market participants are likely to focus on bioresorbable materials to improve long-term patient health. These innovations are expected to reduce the necessity for long-term antiplatelet medication regimens. Continuous investment in research and development is forecast to drive future market breakthroughs. Procurement volumes rise steadily as providers prioritize compliance and procedural efficiency. This trajectory positions the market for sustained momentum amid evolving clinical guidelines.

Key Industry Highlights:

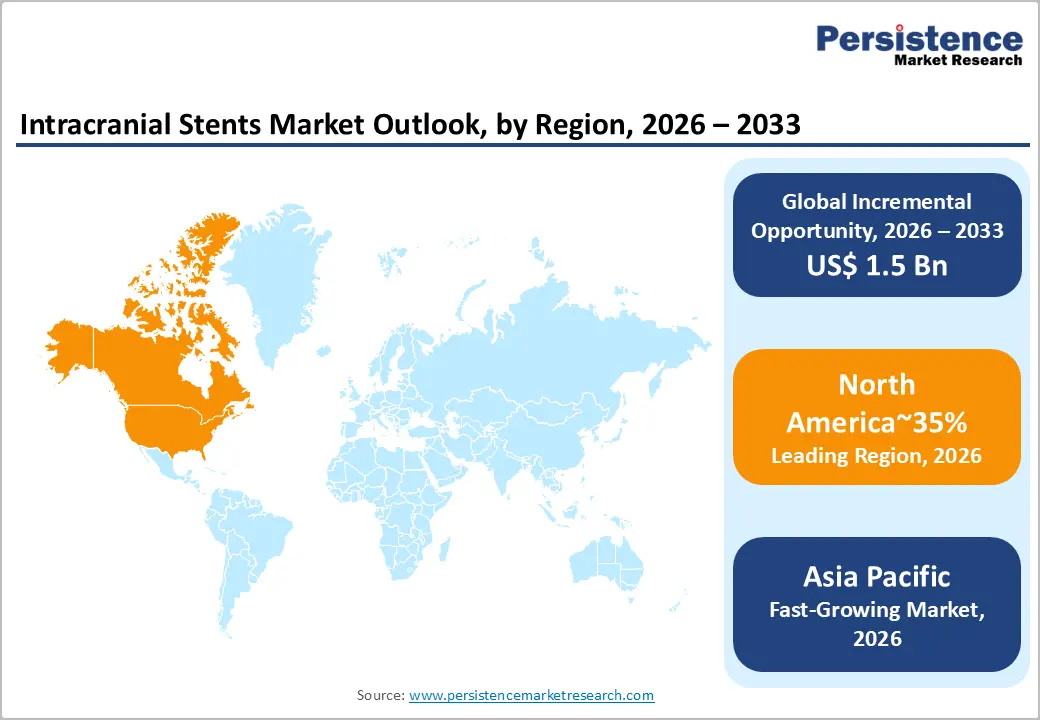

- Leading Region: North America is projected to lead, accounting for approximately 35% share in 2026, supported by high neurovascular disease prevalence and advanced stroke care infrastructure.

- Fastest Growing Region: Asia Pacific is anticipated to grow the fastest, driven by rapid urbanization and increasing healthcare spending across emerging regional economies.

- Leading Product Type: Self-expanding stents are expected to lead, accounting for approximately 44% share in 2026, anchored by superior flexibility and ease of deployment.

- Leading Disease Indication: Brain aneurysm is expected to dominate, accounting for approximately a 57% share in 2026, driven by high demand for flow-diversion and stent-assisted coiling.

| Key Insights | Details |

|---|---|

|

Intracranial Stents Market Size (2026E) |

US$3.4 Bn |

|

Market Value Forecast (2033F) |

US$4.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.1% |

DRO Analysis

Driver Analysis – Adoption of Minimally Invasive Neuro-Interventional Procedures

Minimally invasive neurovascular procedures are expanding due to superior clinical outcomes and reduced procedural trauma. Patients increasingly prefer these interventions as they significantly shorten recovery durations and hospitalization periods. Lower inpatient burden and reduced complication risks are driving higher procurement volumes across neurosurgical centers globally. Clinicians are shifting toward stenting techniques over traditional open surgical approaches for aneurysm management. This transition is reshaping treatment pathways for stroke and neurovascular disorders within advanced healthcare systems. Healthcare infrastructure continues evolving to support image-guided and catheter-based neuro-interventional procedures effectively.

Medtronic advances Pipeline Vantage Embolic Device, addressing complex aneurysm morphologies with improved deployment precision. Advanced catheter delivery systems enhance intracranial navigation, supporting accurate device placement within tortuous vascular anatomies. Improved stent flexibility strengthens wall apposition, reducing procedural complications and enhancing therapeutic outcomes. These innovations increase procedural success rates, particularly in first-pass treatment scenarios across neurovascular interventions. Regulatory emphasis on safety and efficacy accelerates adoption of next-generation interventional devices. This convergence of clinical demand and device innovation sustains growth across minimally invasive neuro-interventional markets.

Rising Global Geriatric Population and Neurovascular Demand Expansion

Aging population demographics are increasing prevalence of degenerative cerebrovascular conditions across global healthcare systems. Elderly populations exhibit higher incidence of intracranial atherosclerosis and aneurysms requiring sustained clinical intervention. This demographic transition drives demand for long-term vascular scaffolding and neuro-interventional treatment solutions. Healthcare infrastructure continues expanding stroke centers to accommodate rising geriatric patient volumes and specialized care requirements. Increased surgical throughput reinforces consistent utilization of advanced neurovascular devices across institutional settings. These factors collectively strengthen demand for durable and minimally invasive treatment approaches within aging populations.

Stryker Corporation develops Neuro-form Atlas Stent System designed to address anatomical complexities associated with elderly vascular structures. Low-profile configurations improve navigability while reducing procedural risks in fragile and tortuous cerebral vessels. Device innovation increasingly focuses on balancing radial strength with flexibility to enhance clinical safety outcomes. Manufacturers prioritize designs that minimize complications and support predictable deployment within compromised vascular anatomies. Regulatory frameworks emphasize safety validation for devices targeting high-risk geriatric populations globally. This convergence of demographic pressure and device optimization sustains long-term demand across neurovascular intervention markets.

Restraint Analysis – Cost Structure Burdens in Neurovascular Device Adoption

Premium pricing of advanced vascular scaffolds imposes sustained budgetary pressure within constrained reimbursement frameworks globally. High capital requirements for maintaining specialized inventory conflict with volume-driven economics in neurovascular procedural suites. Supply chain dependencies on precision-engineered components further amplify acquisition challenges for mid-tier healthcare facilities. These financial constraints limit accessibility of advanced devices despite their demonstrated clinical effectiveness and procedural advantages. Budget prioritization within hospitals often favors essential services, delaying adoption of high-cost neuro-interventional technologies. Cost-intensive procurement structures continue to restrict widespread integration across resource-constrained clinical environments.

Medtronic operates within premium neurovascular segments where pricing dynamics influence institutional purchasing decisions significantly. Extended procurement cycles emerge due to financing limitations and administrative approval delays across healthcare systems. Operational constraints reduce adoption rates in facilities with limited funding and infrastructure capabilities. Providers navigate complex trade-offs between accessing innovative technologies and maintaining fiscal sustainability within treatment programs. Reimbursement variability across regions further complicates financial planning for advanced neurovascular interventions. These cumulative pressures slow penetration of next-generation devices within fragmented and cost-sensitive healthcare markets.

Implantation Complexity and Procedural Risk Constraints

Steep learning curves associated with flow diversion techniques limit widespread integration across neurovascular treatment protocols globally. Procedural variability introduces elevated thrombosis risks, particularly when combined with adjunctive pharmacological therapies during interventions. These complexities require high operator proficiency, increasing dependency on specialized training and experienced clinical teams. Skill gaps across intervention units prolong competency development and reduce procedural standardization within healthcare systems. Variability in technique execution impacts clinical outcomes, creating uncertainty in broader adoption across diverse treatment settings. This technical burden constrains consistent utilization of advanced neuro-interventional devices within routine clinical practice.

Stryker Corporation operates within complex neurovascular intervention segments where precision deployment significantly influences procedural success rates. Downstream effects limit scalability across decentralized care networks lacking specialized expertise and infrastructure capabilities. Healthcare centers balance risk mitigation with efficiency requirements, influencing adoption decisions for advanced techniques. Training investments increase operational costs, further constraining expansion within resource-limited environments globally. Regulatory scrutiny emphasizes procedural safety, reinforcing the need for standardized training and validated clinical outcomes. These dynamics collectively temper expansion pace within emerging neurovascular practice environments.

Opportunity Analysis – AI-Driven Procedural Planning and Simulation in Neurovascular Interventions

Artificial intelligence is transforming pre-operative planning for intracranial stenting procedures within advanced neurovascular treatment environments. Machine learning algorithms enable prediction of optimal stent sizing and placement tailored to individual vascular anatomies. These capabilities reduce procedural complications by simulating hemodynamic changes prior to actual clinical intervention. Clinicians increasingly utilize digital twin models to visualize outcomes and refine surgical strategies before execution. Integration of predictive analytics enhances decision-making accuracy across complex neurovascular cases requiring high precision. This technological evolution strengthens procedural reliability and improves clinical success rates across specialized intervention centers.

Rapid medical advancements are transforming the Comaneci embolization assist device through the integration of artificial intelligence–driven procedural planning. Software-guided platforms improve stent selection by matching device characteristics with patient-specific vascular conditions. The incorporation of digital imaging enables real-time procedural adjustments, enhancing precision and significantly reducing intraoperative risks. Manufacturers are increasingly partnering with software developers to create proprietary planning ecosystems that combine imaging, advanced analytics, and simulation tools. Regulatory frameworks are also placing greater emphasis on algorithm reliability, data integrity, and the clinical validation of AI-assisted systems. Collectively, these developments are driving the next wave of innovation in neurovascular intervention technologies.

Hybrid Therapy Convergence in Neurovascular Treatment Strategies

The convergence of coil and stent technologies enables treatment of wide-neck aneurysms previously unsuitable for standalone interventions. Multimodal therapeutic approaches improve occlusion stability across complex and irregular vascular geometries within neurovascular procedures. This integration expands clinical indications, supporting broader utilization of combined device strategies in challenging anatomical conditions. Enhanced structural support and flow modulation improve long-term durability of treatment outcomes across diverse patient profiles. Clinical adoption increases as hybrid techniques demonstrate improved efficacy compared to traditional single-modality interventions. This trend sustains momentum for device pairing across advanced neuro-interventional treatment frameworks.

Terumo Corporation develops complementary neurovascular solutions supporting combined deployment strategies across coil and stent systems. Integrated device architectures improve procedural flexibility and enable tailored treatment approaches for complex aneurysm morphologies. Healthcare centers leverage these synergies to optimize occlusion success and reduce retreatment rates across patient populations. Technological alignment between device categories strengthens interoperability and procedural efficiency within interventional suites. Regulatory pathways increasingly recognize combined modality approaches, supporting broader clinical acceptance across global markets. This convergence reinforces utilization growth within advanced neurovascular intervention ecosystems.

Category–wise Analysis

Product Type Insights

Self-expanding stents are expected to lead, accounting for approximately 44% share in 2026, underpinned by superior vessel conformability. High-flexibility nitinol architectures enable these devices to navigate the complex turns of the cerebral vasculature. Adoption remains anchored in the ease of deployment compared to balloon-expandable alternatives in tortuous anatomy. Clinicians prioritize self-expanding designs for wide-neck aneurysms to ensure stable and secure wall apposition. Ongoing enhancements in delivery sheath technology further strengthen the utilization of these flexible stent systems. Medtronic with Pipeline Vantage Embolic Device and Stryker with Neuro-form Atlas Stent System exemplify this category leadership. This convergence of mechanical reliability and clinical versatility sustains the segment's dominance in neurovascular interventions.

Self-expanding stents are anticipated to be the fastest growing segment by the expansion of the Flow-diverter systems, driven by the increasing clinical preference for reconstructive aneurysm treatments. Advanced braided designs enable the redirection of blood flow away from the aneurysm sac to promote healing. This structural shift reduces the risk of rupture without requiring dense coiling of the internal cavity. Terumo Neuro with FRED X Flow Diverter and Micro Port with Tubridge Flow Diverter are accelerating the transition toward these devices. Integration of anti-thrombogenic coatings supports the reduction of post-operative complications and improves long-term patient outcomes. As neurosurgeons seek more durable solutions for complex lesions, flow-diversion is gaining significant momentum globally. This shift toward biological remodeling over mechanical filling is reshaping the future of intracranial therapy.

Disease Indication Insights

Brain aneurysm is projected to lead, accounting for approximately 57% share in 2026, reinforced by high procedural volumes globally. The growing adoption of stent-assisted coiling techniques remains a primary driver for market leadership in this segment. Health systems prioritize early intervention for unruptured aneurysms to prevent catastrophic hemorrhagic stroke events in patients. Balt with LEO+ Self-Expandable Braided Stent and Phenox with p64 MW Flow Diverter support these critical treatments. Ongoing improvements in microcatheter navigation enhance the success rates of stenting in distal vascular locations. This combination of preventive screening and reliable device performance sustains the segment's high market share.

Arteriovenous malformations (AVM) is expected to be the fastest growing segment, driven by advancements in hybrid neuro-interventional treatment strategies. Complex vascular lesions require precise scaffolding to manage high-pressure blood flow during curative embolization procedures. Rapid Medical with Comaneci Embolization Assist Device and Cerenovus with BRAVO Flow Diverter address these intricate anatomical challenges. Surgeons are increasingly utilizing stents to provide structural stability in the parent vessel during nidus destruction. The emergence of more flexible micro-stents is expanding the treatable range of small-vessel malformations. As clinical expertise in managing vascular anomalies grows, the demand for specialized stents is accelerating rapidly.

Regional Insights

North America Intracranial Stents Market Trends

North America is expected to remain the leading regional market, accounting for approximately 35% share in 2026, supported by dense neuro-interventional networks. The region's dominance is anchored in high healthcare expenditures and a robust infrastructure for acute stroke management and preventive care. Comprehensive stroke centers prioritize the early adoption of advanced flow-diversion and stent-assisted coiling technologies to improve patient survival. Regulatory alignment and favorable reimbursement policies for minimally invasive procedures continue to reinforce the concentration of leading vendors.

The U.S. is expected to anchor regional momentum through sustained investments in advanced neurovascular centers and specialized physician training programs. High prevalence of hypertension and related cerebrovascular conditions is anticipated to drive consistent demand for intracranial scaffolding solutions. Medtronic with Pipeline Vantage Embolic Device is expected to benefit from established procurement contracts across major hospital networks. Strategic focus on reducing long-term disability through rapid stroke intervention is projected to sustain high procedural volumes.

Europe Intracranial Stents Market Trends

Europe is expected to remain a mature and structurally stable regional market, with demand primarily anchored in replacement cycles. The region's market is supported by progressive clinical guidelines and well-established public healthcare systems that provide broad access to neuro-interventions. Market stability is reinforced by the presence of numerous domestic manufacturers and a strong tradition of neurovascular research and development. Standardized regulatory frameworks under the Medical Device Regulation (MDR) ensure high safety standards across the diverse regional markets.

Germany is expected to lead regional activity due to its advanced hospital infrastructure and high concentration of specialized neurosurgery clinics. Robust insurance coverage for neurovascular implants is anticipated to support the steady adoption of premium flow-diverter technologies. Balt’s Silk Vista Flow Diverter is expected to maintain a strong presence through localized distribution and clinical partnerships. Increasing focus on elderly care and stroke prevention is projected to drive consistent procurement of intracranial stents.

Asia Pacific Intracranial Stents Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as rapid healthcare infrastructure buildout and rising clinical awareness accelerate market expansion. The region's acceleration is anchored in the expansion of specialty hospitals and the growing middle-class population's access to modern neuro-interventions. Increasing government initiatives to improve stroke response times are anticipated to drive the procurement of advanced stenting technologies. Local manufacturing and favorable investment climates are attracting global players to establish regional production hubs and clinical trial sites.

China is expected to be the primary growth driver through massive investments in domestic neuro-interventional device development and healthcare facility expansion. Government-led reforms aimed at reducing the burden of stroke are anticipated to accelerate the adoption of intracranial stents. MicroPort with Tubridge Flow Diverter is expected to leverage strong local presence to capture expanding market opportunities. Rapidly increasing neuro-interventional training programs are projected to expand the pool of surgeons capable of performing complex procedures.

Competitive Landscape

The intracranial stents market is moderately consolidated, with leadership concentrated among medical device firms such as Medtronic, Stryker, and Terumo Neuro. These companies exert influence through integrated neurovascular platforms combining stents with adjunctive delivery and embolization systems. Their technologies establish benchmarks for deployment precision, safety outcomes, and procedural efficiency across clinical settings. Strong physician training programs and clinical support frameworks reinforce procurement preferences within specialized neurovascular centers. Their global regulatory expertise and supply chain capabilities sustain adoption across both developed and emerging healthcare systems. This structure reflects high entry barriers driven by stringent validation requirements and advanced engineering complexity.

Competitive positioning reflects vertical differentiation through material innovation, retrievability features, and biologically adaptive surface engineering. Premium participants emphasize anti-thrombogenic coatings and low-profile systems enhancing navigation in complex vascular anatomies. Companies such as Cerenovus and Acandis advance specialized solutions targeting high-risk and technically demanding procedures. Industry dynamics include selective acquisitions and collaborations integrating imaging and planning technologies into procedural workflows. Platform evolution increasingly incorporates bioresorbable materials and data-assisted deployment techniques improving clinical precision. Forward-looking strategies prioritize evidence-based outcomes and value-driven pricing models aligned with evolving hospital procurement frameworks.

Key Industry Developments:

- In March 2026, MicroPort Scientific's APOLLO Dream® Sirolimus Target Eluting Stent System was granted FDA Breakthrough Device Designation. This status accelerates the regulatory pathway for the first targeted eluting stent specifically designed for intracranial atherosclerotic disease (ICAD), potentially setting a new standard for preventing restenosis.

- In March 2026, Medtronic announced a definitive agreement to acquire Scientia Vascular to integrate its access and therapeutic neurovascular portfolios. This merger allows Medtronic to offer a "complete system" solution (access wires + therapeutic stents), streamlining surgical workflows and consolidating its lead in the stroke care market.

- In February 2025, Stryker completed the US$4.9 billion acquisition of Inari Medical, providing a significant entry into the high-growth peripheral and neurovascular segments. The acquisition integrates Inari’s mechanical thrombectomy technologies with Stryker’s existing stent-retriever business, creating a dominant global force in clot-management.

Companies Covered in Intracranial Stents Market

- Medtronic

- Stryker

- Johnson & Johnson

- Terumo

- MicroVention

- Penumbra

- Boston Scientific

- Balt

- Acandis

- MicroPort Scientific

- Phenox

- Rapid Medical

- Cerenovus

- Codman Neuro

- Lepu Medical

- Sano

Frequently Asked Questions

The global intracranial stents market is projected to be valued at US$3.4 billion in 2026 and is expected to reach US$4.9 billion by 2033, driven by the increasing prevalence of cerebrovascular diseases and rising adoption of minimally invasive neuro-interventional procedures across advanced healthcare systems.

The shift toward minimally invasive techniques is accelerating market growth due to reduced procedural trauma, shorter hospital stays, and improved clinical outcomes, while advanced catheter-based technologies and imaging integration enable higher procedural precision and increased success rates in complex neurovascular interventions.

The intracranial stents market is forecast to grow at a CAGR of 5.6% from 2026 to 2033, reflecting sustained demand driven by aging populations, technological advancements in flow-diverter systems, and expanding neurovascular treatment infrastructure globally.

North America is the leading regional market, accounting for approximately 35% share, supported by advanced stroke care infrastructure, high healthcare expenditure, strong reimbursement frameworks, and early adoption of next-generation neurovascular devices.

The intracranial stents market is moderately consolidated, with key players including Medtronic, Stryker Corporation, Terumo Corporation, Johnson & Johnson, and Boston Scientific, competing through innovation in flow-diversion technologies, material science, and integrated neurovascular platforms.