- Non-food Packaging

- Fiber Drums Market

Fiber Drums Market Size, Share, and Growth Forecast, 2025 - 2032

Fiber Drums Market By Material Type (Unlined Fiber Drums, Poly-Coated Fiber Drums), Product Type (Lightweight Fiber Drums, Heavy-Duty Fiber Drums), Application, and Regional Analysis for 2025 - 2032

Fiber Drums Market Size and Trends Analysis

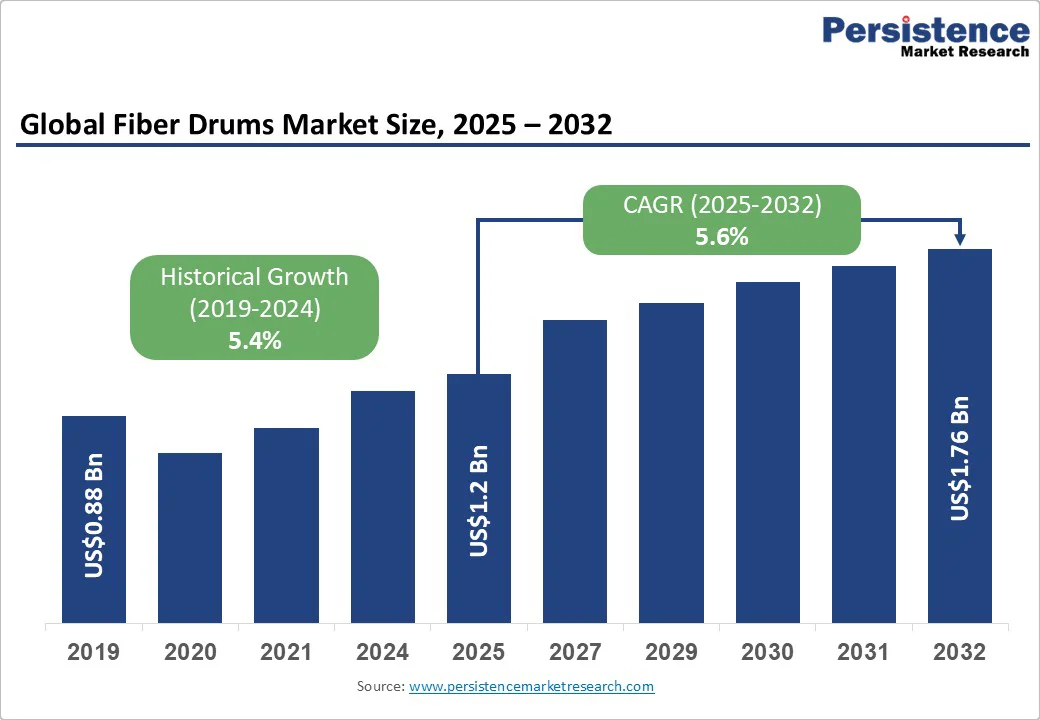

The global fiber drums market size is likely to be valued at US$1.2 Bn in 2025 and is expected to reach US$1.76 Bn by 2032, growing at a CAGR of 5.6% during the forecast period from 2025 to 2032, due to the rising demand for sustainable and recyclable packaging, driven by regulatory mandates and corporate environmental, social, and governance (ESG) commitments.

Key Industry Highlights

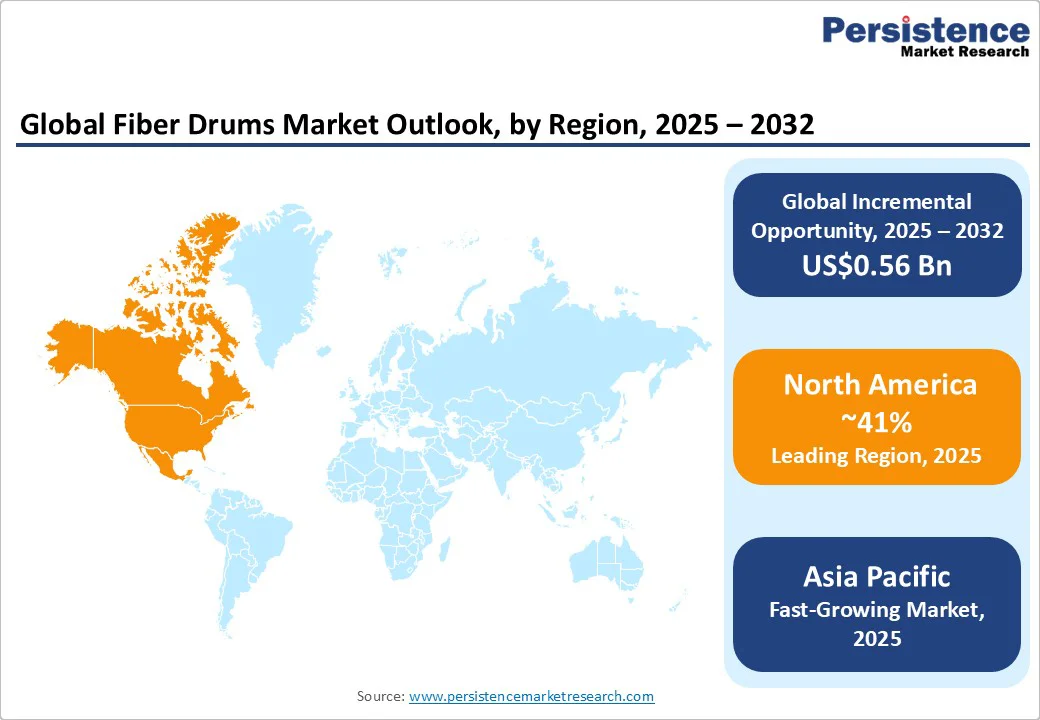

- Leading Region: North America is anticipated to account for 41% share in 2025, driven by strong demand from pharmaceuticals, chemicals, and regulated food packaging.

- Fastest-growing Region: Asia Pacific is projected to grow at a CAGR of 7.4% between 2025 and 2032, fueled by chemical exports, pharmaceutical production, and large-scale manufacturing advantages in China and India.

- Investment Plans: European manufacturers are investing in sustainable and recyclable fiber drum production capacity, particularly in Germany and Eastern Europe, to comply with EU packaging waste directives and capture rising demand.

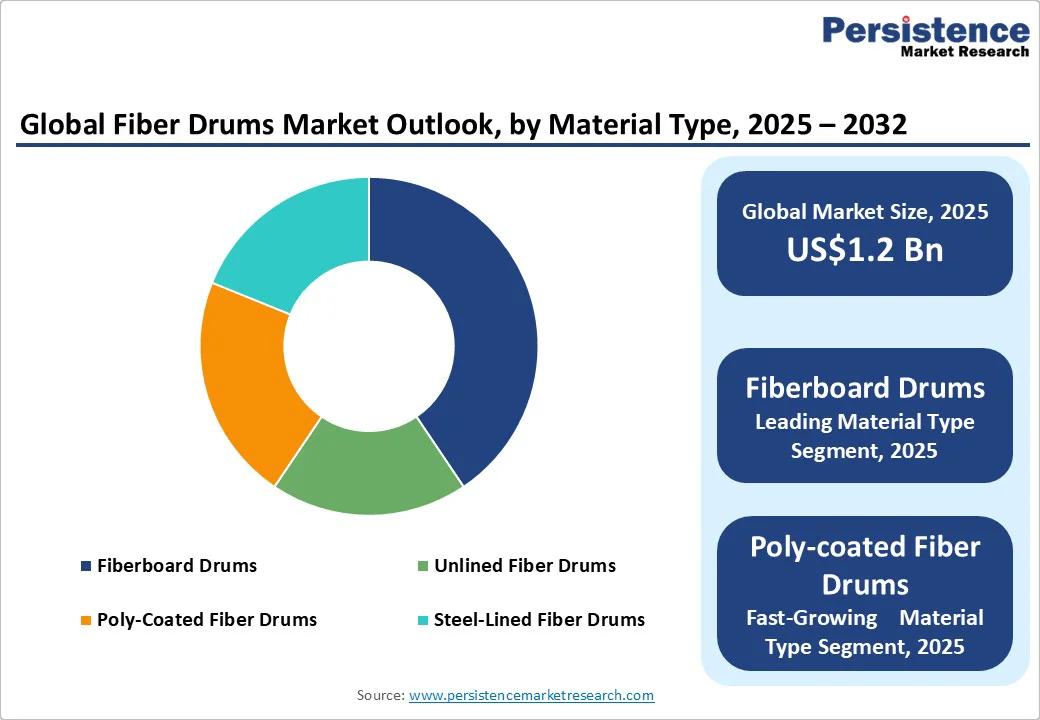

- Dominant Material Type: Fiberboard drums are anticipated to hold 43% of the market share in 2025 due to their cost-effectiveness, recyclability, and regulatory acceptance, making them the largest material segment.

- Dominant Product Type: Steel ring-secured fiber drums are anticipated to hold approximately 41% of the market revenue in 2025, favored for strength, reusability, and compliance in chemical and industrial transport applications.

| Key Insights | Details |

|---|---|

| Fiber Drums Market Size (2025E) | US$1.2 Bn |

| Market Value Forecast (2032F) | US$1.76 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Regulatory Push, Sustainability Mandates, and Logistics Efficiency

Governments and regional bodies (EU Packaging and Packaging Waste Directive, U.S. Environmental Protection Agency [EPA], REACH regulations) are increasingly imposing recyclability, minimum recycled content, and waste-reduction requirements.

These policies favor fiber drums over non-recyclable alternatives. Such regulatory pressure is expected to continue, increasing demand, especially in North America and Europe, and driving investments in sustainable materials across supply chains.

The chemical, pharmaceutical, and food & beverage sectors are growing globally, especially in Asia Pacific (China, India, Southeast Asia). These sectors require safe, hygienic, and often bulk packaging. Fiber drums are increasingly replacing plastic and metal drums for packaging dry goods, powders, and certain liquids (when properly lined), due to their lower cost, lighter weight, and environmental benefits.

As fiber drums are lighter than steel or many plastic options, they reduce shipping and handling costs. They are often more economical in large-volume transport of dry or semi-solid goods. The cost advantage, plus the lower environmental disposal or recycling cost, contributes materially.

As transportation costs, such as fuel and emissions, continue to rise, the efficiency gains offered by fiber drums are becoming increasingly valuable. Market reports also indicate that many SMEs are switching to fiber drums to lower their total cost of ownership.

Limitations in Handling Moisture, Hazardous & Corrosive Contents

Fiber drums (especially unlined ones) are susceptible to moisture damage and are less suited for harsh, corrosive, or fully liquid hazardous materials. Many end-users continue to prefer metal or high-grade plastic drums for these applications due to superior chemical resistance, durability under rough handling, or compliance with certain hazardous-goods regulations.

This limits adoption in specialty chemical or petrochemical sectors. Although lining fiber drums mitigates this limitation, adding a liner increases cost and complicates recyclability. The risk here is quantified in some studies as a constraint in high-value segments (pharmaceuticals), reducing potential market share by an estimated 10-20% in these specific sub-applications.

Fiber drum manufacturing depends on fiberboard/paperboard, adhesives, linings, and closure materials (metal or plastic). Fluctuations in pulp/paper prices, energy costs for processing, transportation, and import/export duties for closure components can raise costs.

High initial capital investment, especially for high-barrier lining or for large capacity production (above 75 gallons), limits entry or expansion. Small or midsize firms may find the cost structure less favorable compared to cheaper plastic drums in price-sensitive markets.

Upgraded Lined and Barrier Technologies Driving Growth in Developing Markets

There is a strong demand for fiber drums with enhanced barrier properties (foil, foil-polyethylene, polymer liners) that can safely store semi-liquids, adhesives, food additives, or even mild chemicals. Firms that invest in R&D or partnerships to produce these could capture higher-margin segments.

For example, the market for lined drums in chemical/pharma packaging is estimated to represent a potential incremental value of several hundred million U.S dollars globally by 2030. Asia Pacific (China, India, Southeast Asia) is expected to be the fastest-growing region due to rapid industrialization, growth in export manufacturing, increasing environmental awareness, and regulatory strengthening.

Emerging markets in Latin America and the Middle East & Africa are showing rising demand for packaging for agrochemicals, processed foods, and pharmaceuticals. Companies that localize production or supply chains in these regions may benefit from lower costs, tariff advantages, and proximity to demand.

Certifications such as FSC and PEFC for fiberboard, along with recycled content labeling, are gaining traction among customers, regulators, and end-consumers. The circular economy model, emphasizing reuse, recycling, and reconditioning, is increasingly valued across the supply chain.

Companies that can demonstrate transparent, third-party-audited sustainability metrics are well-positioned to capitalize on this shift. Additionally, the rise in ESG-focused investing is likely to direct capital toward businesses with strong environmental credentials. Regulatory developments, particularly in the EU and U.S., around extended producer responsibility (EPR), are expected to favor recyclable packaging solutions such as fiber drums through incentives such as tax benefits or subsidies.

Category-wise Analysis

Material Type Analysis

Fiberboard drums are anticipated to lead the material-type segment in 2025, account for a share of 43%, due to their balance of cost-effectiveness, durability, and recyclability.

Widely used in chemicals, pharmaceuticals, and food ingredients packaging, these drums meet key safety and transportation standards while offering a sustainable edge over plastic and metal alternatives. Their dominance is reinforced by global adoption across regulated industries and the ability to support bulk handling at competitive costs.

The poly-coated fiber drums category is projected to grow at the fastest rate from 2025 to 2032. These drums provide enhanced moisture and chemical resistance, which extends product shelf life and broadens application in agrochemicals, specialty chemicals, and food exports. Increasing demand for hybrid solutions that combine sustainability with durability makes poly-coated drums the preferred choice for industries seeking reliable long-distance transportation and compliance with stringent global standards.

Product Type Analysis

Steel ring-secured fiber drums are expected to lead with a share of 41% in 2025. Their ability to handle semi-hazardous materials and withstand rigorous handling makes them the preferred choice for chemical, petrochemical, and pharmaceutical industries.

The secure closure system enhances product safety, meeting UN and DOT transportation standards, which strengthens its use in international trade. Their proven track record of reliability positions them as the dominant category over the forecast period.

The lightweight fiber drums segment is expected to expand at the fastest CAGR between 2025 and 2032. Companies are increasingly adopting these drums to optimize logistics, cut transportation costs, and align with carbon footprint reduction targets.

Their growing application in food, nutraceuticals, and dry bulk exports highlights their role in industries where lightweight yet durable packaging is essential. This trend reflects the broader market push toward resource efficiency and circular economy models.

Regional Insights

North America Fiber Drums Market Trends - Regulatory Compliance and Smart Packaging Drive Adoption

North America accounts for a 41% share of the fiber drums market in 2025, with the U.S. leading due to strong demand in pharmaceuticals, chemicals, and food exports. Market growth is supported by the U.S. Food and Drug Administration (FDA) and Department of Transportation (DOT) packaging standards, which drive adoption of compliant containers such as fiber drums.

The region benefits from a robust innovation ecosystem, with packaging manufacturers focusing on sustainable materials and closed-loop recycling. Strategic investments in lightweight drum production and automation are further enhancing competitiveness.

Recent developments in the North America market include the integration of smart packaging technologies such as RFID and barcode tracking, improving traceability and logistics efficiency. U.S.-based companies are increasingly designing hybrid fiber drums that combine sustainability with durability by incorporating plastic or foil linings.

There is also a noticeable trend toward square or space-efficient fiber drum designs to optimize shipping and storage. These innovations are aligned with stricter regulatory frameworks and corporate sustainability goals, further reinforcing North America's leadership in fiber drum innovation and adoption.

Asia Pacific Market Trends - Industrial Growth and Sustainable Production Fuel Expansion

Asia Pacific is the fastest-growing regional market, led by China, India, and Japan. Expansion of the chemical, agrochemical, and pharmaceutical industries is fueling demand for cost-effective and compliant packaging solutions. The region benefits from large-scale manufacturing advantages and rising intra-Asia trade, which drives containerized bulk packaging requirements.

China’s export-driven economy, India’s pharmaceutical production growth, and Japan’s advanced packaging technologies collectively strengthen regional prospects. Supportive government policies encouraging sustainable packaging solutions also contribute to accelerating fiber drum adoption in Asia Pacific.

Recent market dynamics highlight the growing focus on fiber drum sustainability and export readiness. China and India, in particular, are rapidly expanding their fiber drum manufacturing capabilities using locally-sourced recycled paperboard, cutting costs and emissions. Japan continues to lead in innovation, with companies developing high-barrier coatings and drums tailored for cleanroom pharmaceutical applications.

Additionally, governments across the region are incentivizing green packaging through subsidies and policy reforms, accelerating private-sector investment in biodegradable and recyclable drum formats. Smart manufacturing practices, including automation and digital monitoring systems, are also being adopted to increase production efficiency and meet rising regional demand.

Europe Fiber Drums Market Trends - Circular Economy and Eco-Innovation Shape Demand

Europe remains a key market, supported by regulatory harmonization under EU waste management and packaging directives. Countries, including Germany, France, and the U.K., are central to demand, with strong consumption from the chemical and specialty food sectors.

The European Green Deal and circular economy policies are accelerating the adoption of recyclable packaging formats such as fiber drums. Investment trends point toward the expansion of fiber drum manufacturing capacity in Eastern Europe, where cost advantages and proximity to industrial hubs provide strategic opportunities for market participants.

In 2025, the Europe fiber drums market is expected to be shaped by innovations in coatings and linings that meet EU standards for moisture resistance, chemical safety, and food-grade compliance. Manufacturers are increasingly using recycled and bio-based materials in production, responding to extended producer responsibility (EPR) regulations and consumer pressure.

Smart packaging solutions are also gaining traction in Europe, particularly in Western European economies, where high-tech integration into logistics and supply chains is more advanced. Additionally, Eastern Europe is emerging as a production hub and also as a growing market itself, driven by industrial expansion and rising intra-regional trade.

Competitive Landscape

The global fiber drums market is moderately consolidated, with several large global players commanding significant shares, especially in developed regions, but also numerous smaller regional/local firms, especially in Asia Pacific and emerging markets.

Key leading players include Greif Inc., Sonoco Products Company, Mauser Group, Schutz Container Systems, C.L. Smith Company, Orlando Drum & Container, Industrial Container Services, Fibrestar Drums Limited, Great Western Containers, etc. These firms often control a large proportion of volume in high-specification products (lined, barrier closures) and in regions with stringent regulation.

Leading firms are focused on differentiation via product quality (lining, barrier, closure performance), cost leadership (scale, efficient supply chain, localization), and market expansion (geographic and end-use diversification: e.g., moving into pharmaceuticals or specialty chemicals). An emerging business model is offering “circular service?packages” that cover drum return, reuse, or recycling, giving an end-to-end sustainability offering.

Key Industry Developments

- In April 2024, Greif, Inc. announced expanded production capacity for fiber drums in North America, aiming to meet rising demand from the chemical and pharmaceutical sectors. The move strengthened its leadership in sustainable industrial packaging solutions.

- In January 2024, Mauser Packaging Solutions launched a new line of lightweight fiber drums with enhanced recyclability, designed to reduce logistics costs and align with circular economy targets. This product innovation targeted food and agrochemical applications.

Companies Covered in Fiber Drums Market

- Greif, Inc.

- Mauser Packaging Solutions

- Sonoco Products Company

- Schutz Container Systems

- Enviro-Pak

- Berry Global, Inc.

- Time Technoplast Limited

- SIG Combibloc Group

- Pactiv Evergreen, Inc.

- Mondi Group

- Smurfit Kappa Group

- U.S. Corrugated, Inc.

- Pratt Industries

- WestRock Company

- Inteplast Group

- Nefab Group

- DS Smith Plc

- Amcor Limited

- Rexam Plc

- Ball Corporation

Frequently Asked Questions

The fiber drums market size was valued at US$1.2 Bn in 2025.

By 2032, the fiber drums market is projected to reach US$1.76 Bn.

Key trends include the rising demand for sustainable and recyclable packaging solutions, increased adoption of poly-coated fiber drums for chemical and food applications, and growing preference for lightweight drums to reduce logistics costs and carbon footprint.

By material type, fiberboard drums dominate due to cost-effectiveness and recyclability. By product type, steel ring-secured drums lead, driven by strong adoption in chemical and pharmaceutical transport.

The fiber drums market is projected to grow at a CAGR of 5.6% between 2025 and 2032.

Leading companies include Greif, Inc., Mauser Packaging Solutions, Sonoco Products Company, Schutz Container Systems, and Enviro-Pak.