- Agrochemicals

- Zinc Carbonate Market

Zinc Carbonate Market Size, Share, and Growth Forecast, 2026-2033

Zinc Carbonate Market by Product Type (Activated Zinc Carbonate, Dense Zinc Carbonate, Others), Application (Paints & Coatings, Medical & Healthcare, Others), Grade (Pharmaceutical Grade, Industrial Grade, Food Grade), and Regional Analysis for 2026 – 2033

Zinc Carbonate Market Size and Trends Analysis

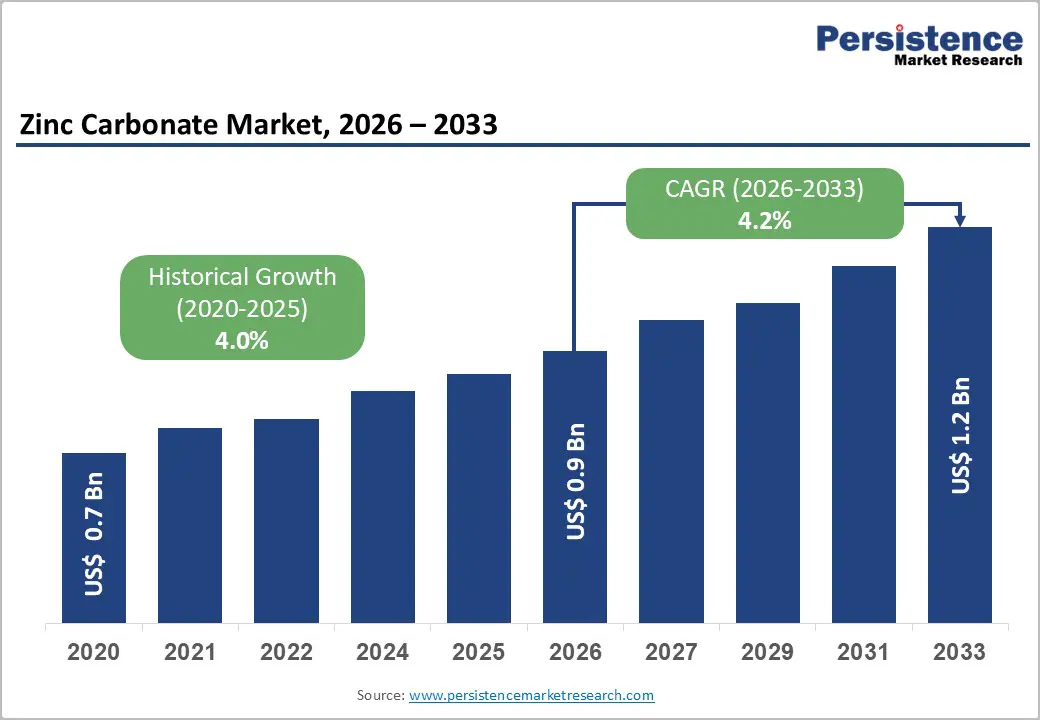

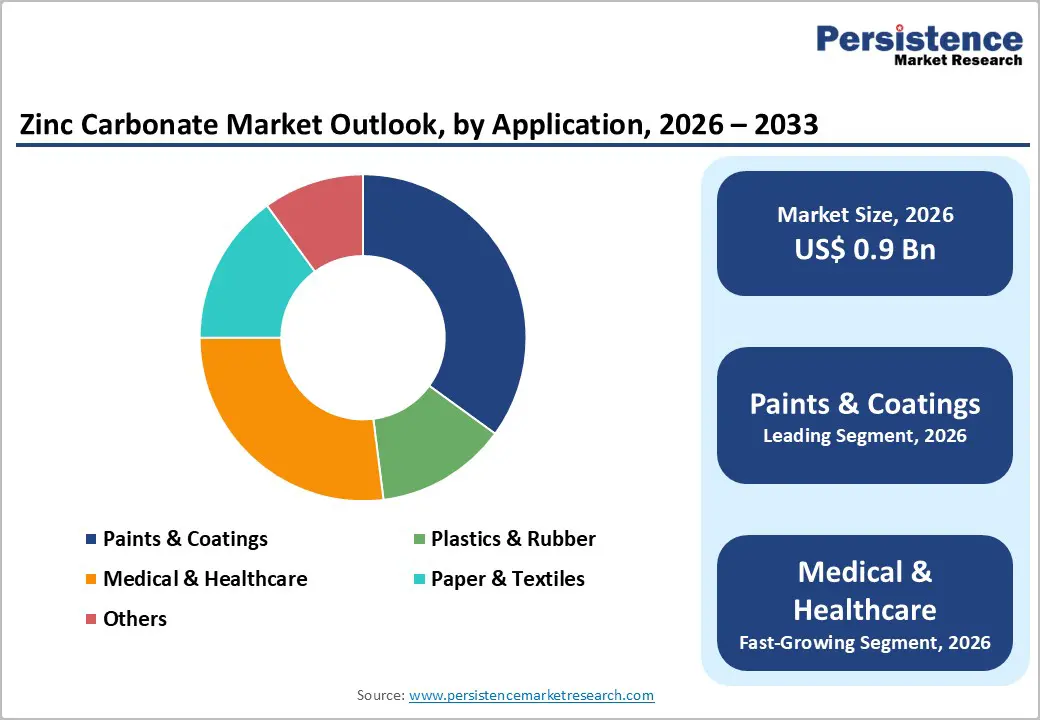

The global zinc carbonate market size is likely to be valued at US$0.9 billion in 2026 and is expected to reach US$1.2 billion by 2033, growing at a CAGR of 4.2% during the forecast period from 2026 to 2033, driven by increasing consumption in paints and coatings, supported by rising construction activity, infrastructure development, and urbanization across emerging economies.

Zinc carbonate is widely used as a functional additive to improve durability, corrosion resistance, and surface performance. Growing applications in pharmaceuticals and medical formulations, including dermatological products and intermediates, are contributing to sustained demand, supported by expanding healthcare expenditure. The market also benefits from rising usage in plastics and rubber, where zinc carbonate serves as a stabilizer and performance enhancer, particularly in formulations aligned with sustainable and lightweight material trends.

Key Industry Highlights:

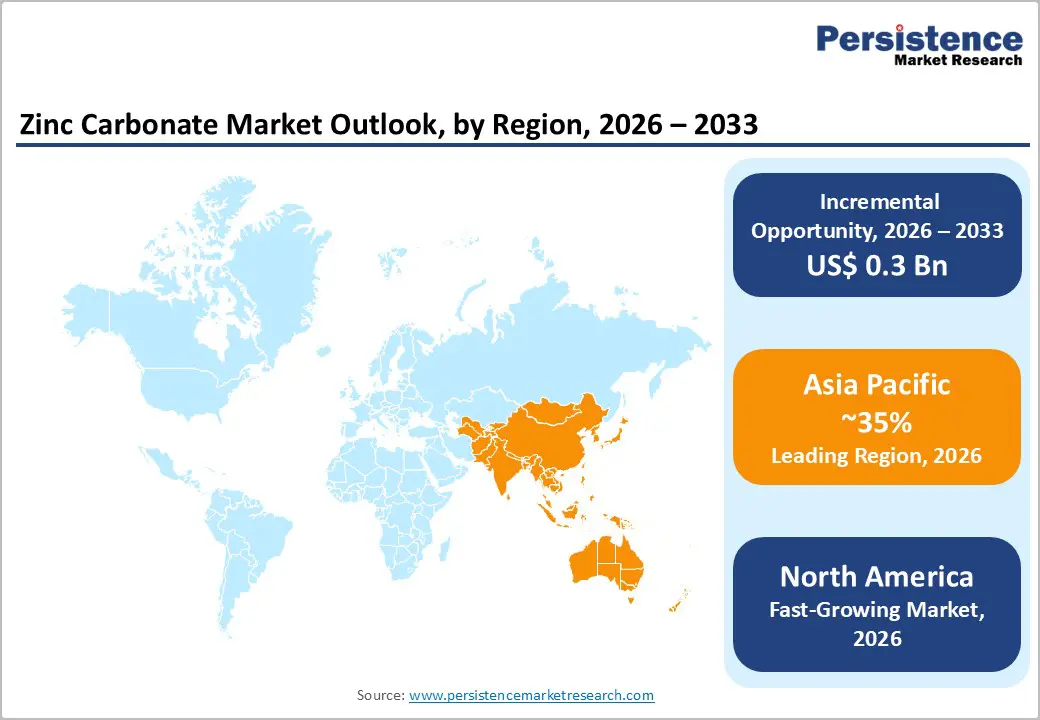

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by strong manufacturing activity, rapid urbanization, expanding construction and coatings demand, and growing pharmaceutical and plastics industries across China, India, and Southeast Asia.

- Fastest-growing Region: North America is likely to be the fastest-growing region for zinc carbonate in 2026, driven by strong manufacturing demand, advanced healthcare applications, innovation in nanobased formulations, and stringent regulatory standards that support high-purity products.

- Leading Product Type: Dense zinc carbonate is projected to be the leading product type in 2026, accounting for 45% of revenue, driven by its cost-effectiveness and suitability for large-scale industrial applications.

- Leading Application: Paints & coatings are projected to be the leading application type, accounting for over 35% of revenue in 2026, supported by strong demand from construction and infrastructure activities.

- Leading Grade Type: Industrial grade is projected to be the leading grade type in 2026, accounting for 55% of revenue, driven by its widespread use in bulk chemical and manufacturing processes.

| Global Market Attributes | Key Insights |

|---|---|

| Zinc Carbonate Market Size (2026E) | US$0.9 Bn |

| Market Value Forecast (2033F) | US$1.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Advancements in Pharmaceutical and Healthcare Applications

Zinc carbonate is commonly used as an intermediate in the production of zinc-based active pharmaceutical ingredients and topical preparations, including calamine formulations, ointments, and skin-protective products. Its mild astringent, anti-inflammatory, and antimicrobial properties make it particularly suitable for treating skin irritations, rashes, wounds, and acne-related conditions. Growing awareness of zinc’s role in immune support and skin health has led to increased incorporation of zinc into dietary supplements and over-the-counter healthcare products.

As healthcare systems expand and access to medicines improves in emerging economies, demand for reliable and high-purity zinc compounds continues to rise. Pharmaceutical manufacturers increasingly prefer zinc carbonate due to its chemical stability, controlled reactivity, and suitability for meeting stringent quality and safety standards. Advancements in pharmaceutical manufacturing and formulation technologies are accelerating the adoption of specialized zinc carbonate grades, particularly pharmaceutical-grade and micro-sized variants.

Improved processing techniques enable better particle size control, enhanced bioavailability, and superior dispersion, which are critical for modern drug formulations and controlled-release applications. The rising focus on preventive healthcare, nutritional supplementation, and dermatological care has strengthened demand for zinc-based ingredients. Zinc carbonate is also gaining traction in pediatric and geriatric healthcare products, where safety, tolerability, and effectiveness are essential. Regulatory emphasis on product purity and traceability has encouraged manufacturers to invest in refined production processes, increasing confidence among pharmaceutical buyers.

Stringent Regulatory Compliance in Pharmaceutical Grades

Pharmaceutical applications demand exceptionally high purity levels, strict control over impurities, and full traceability across the production chain. Regulatory authorities such as the FDA, EMA, and other national drug agencies mandate compliance with pharmacopeial standards, Good Manufacturing Practices (GMP), and the maintenance of detailed documentation for raw materials, processing methods, and quality testing. Meeting these requirements often necessitates advanced purification technologies, specialized production facilities, and frequent audits, which substantially increase operational costs.

Smaller manufacturers and new entrants may face barriers due to the capital-intensive nature of compliance, limiting competition and slowing capacity expansion. Evolving regulatory frameworks and increasing scrutiny over excipients and inorganic compounds add complexity for pharmaceutical-grade zinc carbonate suppliers. Authorities are progressively tightening limits on heavy metals, residual solvents, and microbiological contamination, requiring continuous upgrades in testing and quality assurance systems.

Suppliers serving multiple regions must also navigate variations in regulatory requirements across countries, increasing administrative burden and compliance costs. These challenges can discourage manufacturers from allocating resources toward pharmaceutical-grade production, shifting focus instead to industrial or technical grades with lower regulatory hurdles.

Technological Convergence with Nano-Materials

Nano-sized and micro-engineered zinc carbonate exhibits a higher surface area, improved dispersion, and superior functional efficiency compared with conventional grades. These properties make it increasingly attractive for advanced applications in the pharmaceutical, healthcare, coatings, plastics, and specialty chemicals sectors. In pharmaceutical formulations, nano-zinc carbonate enhances bioavailability, supports controlled release, and improves therapeutic performance, aligning with the industry’s shift toward precision medicine and targeted drug delivery.

In paints and coatings, nano-enabled zinc carbonate enhances corrosion resistance, UV stability, and durability while reducing material usage, thereby supporting sustainability goals. Increasing investments in nanotechnology research and advanced material science are accelerating the commercialization of nano-grade zinc carbonate. Manufacturers are adopting modern processing techniques, such as controlled precipitation, surface modification, and advanced milling, to achieve consistent nanoscale properties.

This technological progress is opening new opportunities in electronics, medical devices, and high-performance polymers, where precision and material efficiency are critical. Regulatory support for innovative materials that reduce environmental impact also favors nano-enabled zinc carbonate, as smaller quantities can deliver equivalent or superior performance compared to traditional materials. Collaboration among chemical producers, research institutions, and end-use industries is accelerating product development and application testing.

Category-wise Analysis

Product Type Insights

Dense zinc carbonate is expected to lead the market, accounting for approximately 45% of revenue in 2026, driven by its extensive use in large-scale industrial applications where consistency, stability, and cost efficiency are critical. Its chemical robustness makes it suitable for bulk manufacturing processes across plastics, rubber, coatings, and chemical intermediates. Manufacturers favor this product type as it integrates easily into existing production systems without requiring specialized handling or reformulation, ensuring smooth supply chain operations.

For example, it is used in industrial rubber compounding, where manufacturers rely on Dense Zinc Carbonate to ensure uniform curing behavior and material strength across mass-produced automotive components.

The micro- and nano-sized zinc carbonate segment is expected to be the fastest-growing in 2026, driven by the rising demand for high-precision materials in advanced applications. This segment offers enhanced surface activity, better dispersion, and improved functional efficiency, making it ideal for specialized uses that require controlled performance. Industries are increasingly adopting refined material solutions that provide higher effectiveness with lower material input, aligning with both sustainability and innovation goals.

For instance, in pharmaceutical formulation development, micro- and nano-sized zinc carbonate is used to enhance bioavailability and ensure uniformity in both topical and oral healthcare products.

Application Insights

The paints and coatings segment is expected to lead the market, accounting for approximately 35% of the revenue share in 2026. Zinc carbonate is highly valued in coatings for its ability to enhance corrosion resistance, improve surface durability, and provide long-term material protection. Its functional benefits align with the growing needs of urban development and industrial asset maintenance, making it a preferred additive in both decorative and protective coatings.

For example, zinc carbonate is commonly used in infrastructure coatings for bridges and public buildings, where durability and resistance to environmental exposure are crucial. The widespread adoption of zinc carbonate in this segment is further supported by its compatibility with various coating formulations and regulatory acceptance across multiple regions.

The medical and healthcare segment is anticipated to be the fastest-growing application in 2026, driven by the increasing demand for zinc-based therapeutic and preventive solutions. Zinc carbonate plays a key role in dermatological products, wound care formulations, and pharmaceutical intermediates, owing to its soothing, protective, and antimicrobial properties. Healthcare systems are placing a greater emphasis on preventive care, skin health, and nutritional support, which directly fuels demand for zinc-containing compounds.

For example, zinc carbonate is widely used in topical treatments for skin irritation and minor wounds, where both safety and effectiveness are paramount. As healthcare manufacturers continue to prioritize high-quality, biocompatible ingredients, zinc carbonate is gaining traction in this segment, supported by advancements in formulation technologies and broader access to healthcare products in developed markets.

Grade Type Insights

The industrial-grade segment is expected to lead the market, accounting for approximately 55% of revenue in 2026, driven by its extensive use in bulk manufacturing. This grade is preferred for its affordability, availability, and suitability for high-volume applications in plastics, rubber, paper, and chemical processing. Industrial users prioritize consistent quality and reliable supply over ultra-high purity, making industrial-grade zinc carbonate the preferred choice for large-scale production.

For example, its use in polymer stabilization processes, where manufacturers require dependable performance without the added costs associated with refined grades. The dominance of industrial grade zinc carbonate reflects the strong influence of volume-driven industries on overall market demand, particularly in regions with expanding manufacturing bases and infrastructure development.

Pharmaceutical-grade is likely to be the fastest-growing segment in 2026, driven by increasing demand for high-purity materials in regulated healthcare applications. This grade is essential for pharmaceutical formulations, dermatological products, and nutraceuticals, where strict quality standards and safety requirements apply. Growing awareness of zinc’s role in immune health, skin care, and treatments has strengthened demand for pharmaceutical-grade inputs.

For example, it is used in medicated creams and ointments, where purity and consistency are critical to product safety and regulatory approval. Pharmaceutical-grade zinc carbonate is widely used in medicated creams, ointments, and dietary supplements, with manufacturers adhering to stringent quality standards to ensure purity and safety, highlighting its strategic role in the market.

Regional Insights

North America Zinc Carbonate Market Trends

North America is likely to be the fastest-growing region for zinc carbonate in 2026, driven by steady demand across industrial, pharmaceutical, and specialty chemical applications, supported by established manufacturing infrastructure and diversified end use industries. In the U.S. and Canada, zinc carbonate is widely used in coatings, adhesives, rubber compounding, and personal care products due to its chemical stability and functional versatility, ensuring broad industry relevance.

For example, Zochem Inc., a leading North American producer, has expanded its high purity zinc carbonate and related zinc compound offerings specifically for applications in pharmaceuticals and cosmetics, reflecting the region’s focus on value added materials that meet stringent quality specs.

Emerging patterns in the North American zinc carbonate market include heightened emphasis on sustainability, recycling, and supply chain resilience as buyers seek environmentally responsible sources and reliable regional supply. Recycled and secondary zinc streams are particularly valued for lowering lifecycle impacts and aligning with corporate-level sustainability targets, especially in coatings, plastics, and agricultural sector applications. Performance requirements in specialized end uses such as dermatological products and precision industrial chemicals are encouraging product innovation around finer particle size distributions and tailored grade control.

For example, American Zinc Recycling has been increasing facility capacity to recover zinc from industrial by products and deliver consistent quality zinc carbonate feedstock into North American supply chains.

Europe Zinc Carbonate Market Trends

Europe is likely to be a significant market for zinc carbonate in 2026, owing to strong industrial demand, sustainability priorities, and regulatory compliance, which influence purchasing patterns and product applications. In several major European economies, zinc carbonate is widely used in paints, coatings, ceramics, and chemical processing sectors as it enhances corrosion resistance, durability, and functional performance in finished goods.

A valid example of European involvement at the intersection of specialty chemicals and zinc compounds is Coventya, a France-based chemical company that develops and supplies surface finishing and corrosion protection solutions across multiple industries, illustrating the linkage between local chemical expertise and zinc compound utilization in value-added applications. Sustainability and innovation are central trends shaping the European zinc carbonate market, as manufacturers and end users increasingly adopt eco-friendly materials and refined product grades that support regulatory compliance and performance goals.

European buyers are placing greater emphasis on material traceability and reduced environmental impact, which stimulates interest in zinc carbonate used in premium applications such as high-performance coatings for infrastructure, specialty chemicals for personal care, and micronutrient supplements in agriculture. The region’s stringent environmental guidelines encourage the development of zinc compounds with lower ecological footprints and enhanced functionality, aligning with circular economy objectives and waste minimization strategies.

Asia Pacific Zinc Carbonate Market Trends

Asia Pacific is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by rapid industrialization, expanding manufacturing sectors, and wide adoption in multiple end-use industries across China, India, Japan, and Southeast Asia. This region leads zinc compound consumption due to strong activity in coatings, rubber compounding, plastics, and agrochemical formulations, where zinc carbonate serves as a functional additive for corrosion resistance, stabilization, and micronutrient supply.

For example, Pan Continental Chemical Co., Ltd. is a Taiwanese chemical manufacturer that produces zinc carbonate and other zinc compounds, supplying industrial and specialty markets with high purity materials.

Asia Pacific zinc carbonate market is witnessing increased uptake in higher value and specialty applications that reflect broader consumption patterns in the region. End use industries such as paints and coatings, personal care, pharmaceuticals, and specialty chemicals are increasingly integrating zinc carbonate for performance enhancements, regulatory compliance, and formulation innovation. This trend aligns with regional emphasis on quality improvement and product differentiation in consumer and industrial segments, where formulations require additives that balance efficacy with safety and environmental standards. Beyond traditional uses, zinc carbonate also plays a role in specialty agricultural inputs and micronutrient products, where its chemical characteristics support soil health and crop productivity.

Competitive Landscape

The global zinc carbonate market exhibits a moderately fragmented structure, driven by the presence of a mix of large multinational producers, regional manufacturers, and specialty chemical companies competing across product quality, geographic reach, and application focus. Established players often integrate upstream zinc sourcing with downstream carbonate production to secure raw material supply and cost advantages, and they serve a diversified set of end use industries such as pharmaceuticals, coatings, rubber, and agriculture.

With key leaders including Zochem Inc., a major producer of high purity zinc carbonate products used in pharmaceuticals and cosmetics, the competitive landscape emphasizes product differentiation through quality and technical support to meet stringent industry requirements. These players compete through strategic initiatives such as portfolio diversification, capacity expansion, sustainable manufacturing, and enhanced distribution networks. Many companies engage in collaborative ventures, acquisitions, and R&D partnerships to broaden their product offerings and strengthen market positions.

Key Industry Developments:

- In January 2026, Hindustan Zinc Limited, a Vedanta Group company and the world’s largest integrated zinc producer, strengthened its partnership with Silox India, a leading specialty chemicals manufacturer, through the adoption of Hindustan Zinc’s low-carbon zinc brand, EcoZen, across Silox’s manufacturing operations. EcoZen is produced entirely using renewable energy and has a verified carbon footprint of around 75% lower than the industry average, producing less than one tonne of CO2 per tonne of zinc. When used in downstream applications such as galvanizing, EcoZen can help avoid approximately 400 kilograms of CO2 emissions per tonne of steel compared to conventional zinc.

Companies Covered in Zinc Carbonate Market

- Zinc Nacional

- American Zinc Recycling

- Hindustan Zinc Limited

- Mitsui Mining and Smelting Co.

- Zinc Oxide LLC

- Korea Zinc Co Ltd.

- Nyrstar

- Teck Resources Limited

Frequently Asked Questions

The global zinc carbonate market is projected to reach US$0.9 billion in 2026.

The zinc carbonate market is driven by growing demand from paints & coatings, pharmaceuticals, and rubber/plastics industries for corrosion resistance, stability, and functional performance.

The zinc carbonate market is expected to grow at a CAGR of 4.2% from 2026 to 2033.

Key market opportunities in zinc carbonate lie in nano- and micro-sized variants for pharmaceuticals, healthcare, and high-performance industrial applications.

Zinc Nacional, American Zinc Recycling, Hindustan Zinc Limited, Mitsui Mining and Smelting Co., and Zinc Oxide LLC are the leading players.