- Agrochemicals

- Zinc Sulfate Market

Zinc Sulfate Market Size, Share, and Growth Forecast 2026 - 2033

Zinc Sulfate Market by Product Type (Anhydrous, Hexahydrate, Monohydrate, Heptahydrate), Application (Chemicals, Pharmaceuticals, Synthetic Fibers, Water Treatment, Agrochemical, Others), and Regional Analysis, 2026 - 2033

Zinc Sulfate Market Size and Trend Analysis

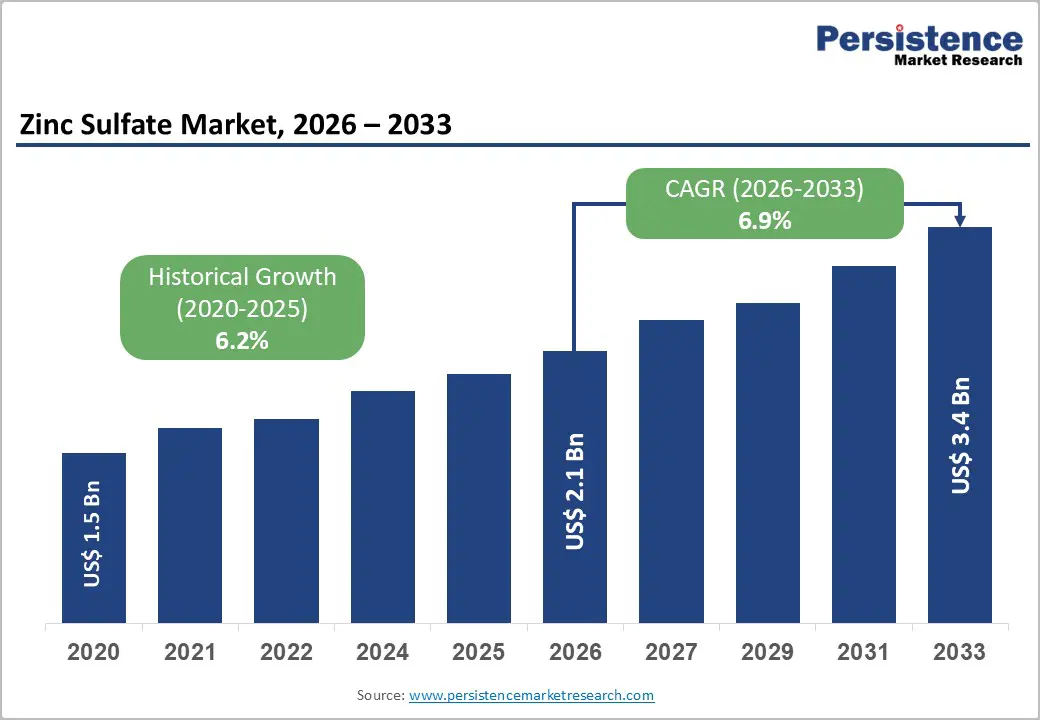

The global zinc sulfate market size is likely to be valued at US$ 2.1 billion in 2026 and is expected to reach US$ 3.4 billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 and 2033.

The market growth is primarily driven by the critical role of zinc sulfate in the agricultural sector, particularly in addressing widespread zinc deficiency in soils, which affects nearly half of the world's cereal-growing regions.

Key Market Highlights

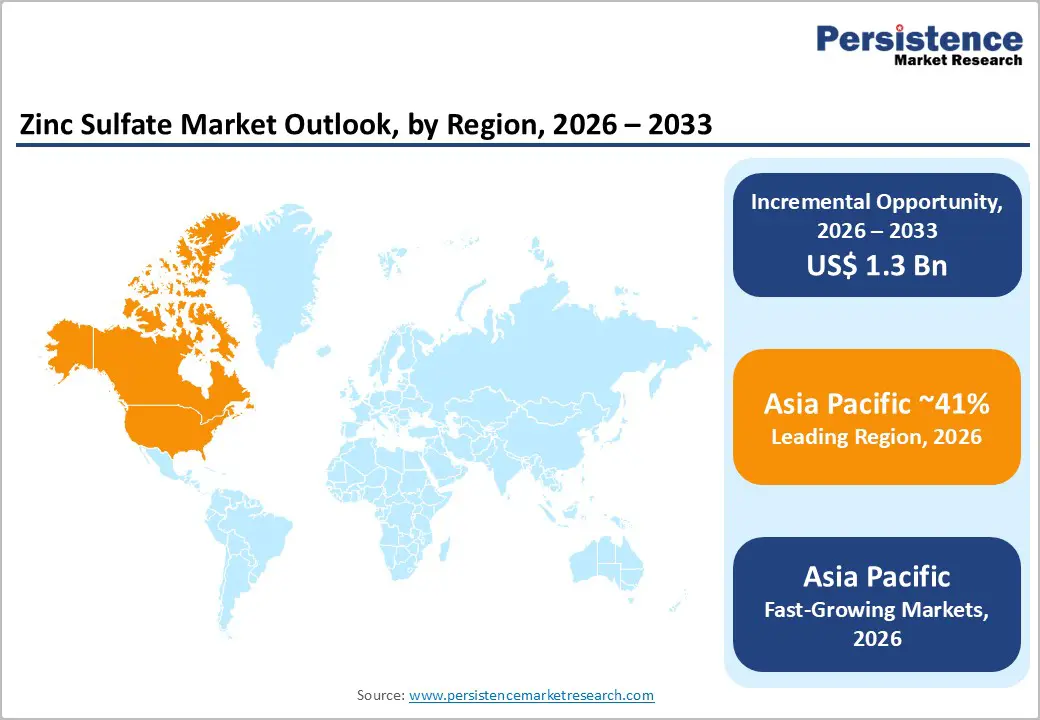

- Leading Region: Asia Pacific dominates the market share with 41%, due to extensive agricultural usage in China and India and a robust textile manufacturing base.

- Fastest Growing Region: Asia Pacific is also the fastest-growing region with a rising CAGR of 8.2%, driven by government subsidies for micronutrients and rising industrialization in ASEAN nations.

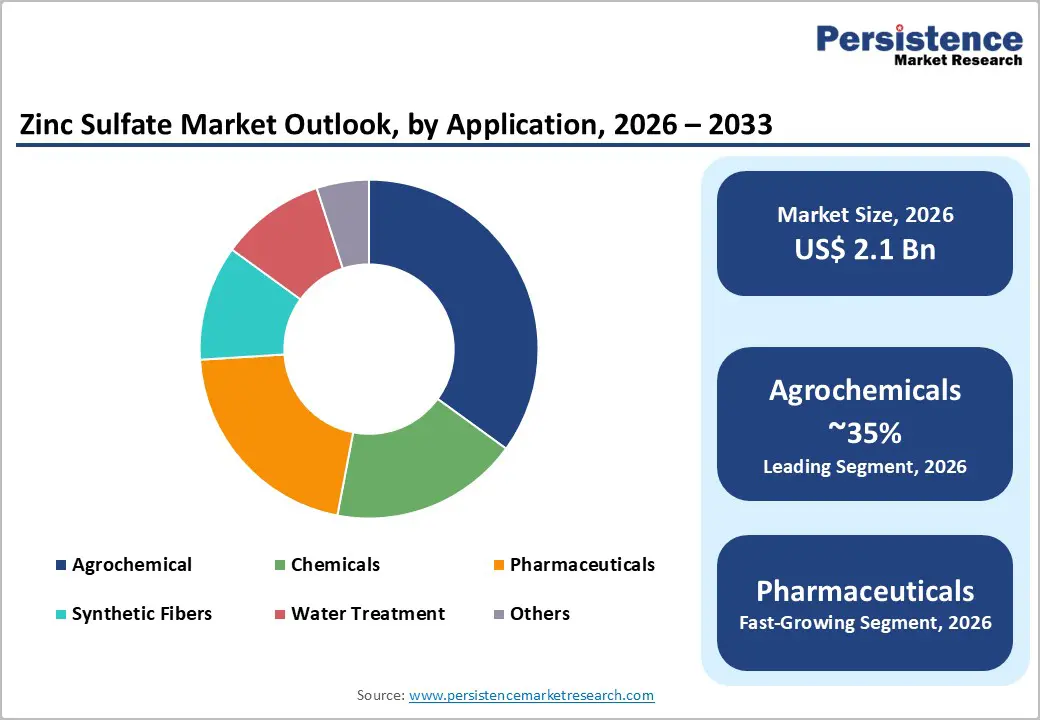

- Dominant Segment: Agrochemicals remain the largest segment in the Application category, holding 35% share, consuming nearly half of global production for fertilizer and soil amendment use.

- Fastest Growing Segment: Pharmaceuticals is the fastest-growing application segment, fueled by increasing global demand for immunity supplements and fortified functional foods.

- Key Market Opportunity: Bio-fortification of staple crops presents a massive untapped avenue, allowing companies to develop premium, high-efficiency zinc formulations for food security programs.

| Key Insights | Details |

|---|---|

| Zinc Sulfate Market Size (2026E) | US$ 2.1 billion |

| Market Value Forecast (2033F) | US$ 3.4 billion |

| Projected Growth CAGR (2026 - 2033) | 6.9% |

| Historical Market Growth (2020 - 2025) | 6.2% |

Market Dynamics

Drivers - Rising Soil Zinc Deficiency Worldwide Is Significantly Increasing Demand for Zinc Sulfate-Based Agrochemical Solutions Across Major Farming Regions

One of the most significant drivers supporting the global market is the growing need to address zinc deficiency in agricultural soils. According to the Food and Agriculture Organization (FAO), nearly 50% of cereal-cultivated soils worldwide lack adequate zinc levels, which directly reduces crop yield, grain quality, and overall plant health. As a result, farmers and agricultural companies are increasingly adopting zinc sulfate because it offers a highly soluble, cost-effective, and reliable source of zinc.

This trend is especially strong in high-intensity farming regions where continuous crop cycles rapidly deplete micronutrients. Moreover, the rise of precision agriculture and the growing inclusion of micronutrients in NPK blends have made zinc sulfate a standard component of modern fertilizer programs. These developments ensure consistent, long-term demand for zinc sulfate, regardless of broader economic fluctuations, making it a stable contributor to market growth.

Growing Pharmaceutical and Dietary Supplement Consumption is Strongly Boosting Demand For High-Purity Zinc Sulfate For Health Applications

The pharmaceutical industry has become a powerful growth driver for zinc sulfate due to rising global awareness of immunity and preventive healthcare. Zinc sulfate is widely used in several essential medical products, including oral rehydration solutions recommended by the World Health Organization (WHO) for treating diarrhea in children, immune-support supplements, and a variety of dermatology formulations.

Following recent global health concerns, consumer spending on zinc-based dietary supplements has grown substantially, creating strong demand for high-purity pharmaceutical-grade zinc sulfate. In addition, the compound is frequently used in topical treatments and skin therapies, ensuring steady adoption across dermatology applications. The increasing focus on wellness, combined with an aging population seeking immunity support, further strengthens this demand. As a result, the pharmaceutical and nutraceutical sectors represent a high-value and consistently growing market segment for zinc sulfate.

Restraints - Volatile Zinc and Sulfuric Acid Prices, Combined With Supply Disruptions, Continue To Constrain Zinc Sulfate Manufacturing Stability

A major challenge for the zinc sulfate market is the price volatility of raw materials such as zinc and sulfuric acid. Zinc prices, which are heavily influenced by London Metal Exchange (LME) trends, fluctuate due to changes in mining output, geopolitical uncertainties, and global energy costs. Since raw materials account for a large share of production expenses, sudden price increases significantly reduce profit margins, especially for producers serving the fertilizer-grade segment where pricing is highly competitive. Additionally

Disruptions such as smelter shutdowns, mining delays, or transportation bottlenecks can lead to supply shortages, forcing manufacturers to increase prices. This often impacts agricultural customers, who are highly price-sensitive and may temporarily shift to cheaper alternatives. Such conditions create short-term demand instability and highlight the market’s dependence on a steady and affordable raw material supply chain.

Strict Global Environmental Regulations on Chemical Production are Creating Major Compliance Challenges for Zinc Sulfate Manufacturers

Zinc sulfate production involves chemical processes that generate waste streams requiring strict environmental management. Regulatory bodies in regions such as the European Union and North America have implemented rigorous guidelines on handling heavy metal waste, emissions, and effluents, particularly under frameworks like REACH. Complying with these rules demands significant investment in waste treatment systems, filtration units, and pollution control technologies.

For many small and mid-sized manufacturers, especially in developing economies, the associated costs can be prohibitive, limiting expansion opportunities or forcing facility upgrades. Moreover, the classification of certain zinc compounds as environmental hazards in some regions increases restrictions on their storage, transportation, and disposal. These regulatory pressures add operational complexity, raise compliance costs, and create uneven competition between global producers and smaller local firms, ultimately shaping the competitive landscape of the zinc sulfate market.

Opportunities - Bio-fortification Programs and Advanced Micronutrient-Enriched Fertilizers Are Creating Large Growth Opportunities for Zinc Sulfate Producers

A major market opportunity lies in the growing global focus on bio-fortification, which aims to enhance the nutritional value of staple food crops. Governments across the Asia Pacific and Africa are actively promoting zinc-enriched crops to tackle micronutrient deficiencies and childhood malnutrition. This shift opens new avenues for zinc sulfate producers to collaborate with fertilizer companies and agricultural agencies to develop advanced, slow-release, and highly efficient zinc formulations.

Innovations such as chelated zinc sulfate, nano-zinc solutions, and customized micronutrient blends offer higher absorption rates and are expected to command premium pricing. As food systems increasingly prioritize nutrition and crop quality over simple yield growth, companies offering specialized agricultural formulations stand to gain substantial market share. The rising importance of soil health and plant nutrition further strengthens this long-term opportunity for zinc sulfate manufacturers.

Rapid Expansion of Water Treatment Infrastructure in Emerging Economies is Driving Strong Industrial Demand for Zinc Sulfate

The water treatment industry represents another promising growth area, driven by rapid urbanization and industrial expansion in emerging economies. Zinc sulfate is used effectively as a corrosion inhibitor in cooling systems and as a coagulant in wastewater treatment, especially for removing heavy metals. Countries such as China, India, and Brazil are enforcing stricter discharge regulations and investing heavily in municipal and industrial water treatment facilities. Unlike mature Western markets, these regions are still building essential water infrastructure, creating large, recurring demand for industrial-grade zinc sulfate. Manufacturers that can supply competitive, high-volume products are well-positioned to secure long-term contracts with utilities and industrial players. This opportunity also enables producers to diversify beyond the seasonal agricultural sector and tap into a more stable, infrastructure-driven demand cycle.

Category-wise Analysis

Product Type Insights

Zinc sulfate monohydrate holds a dominant 43% share in the market’s product type segment due to its advantageous physical and chemical properties. Its low moisture content ensures better stability during storage and transportation, making it easier to handle compared to the heptahydrate form. With a zinc concentration of approximately 33-35%, monohydrate provides high nutrient value, which is essential for agricultural applications seeking efficient micronutrient delivery. It also blends smoothly with granular fertilizers without causing caking or operational issues in fertilizer plants. Manufacturers prefer producing monohydrate because its high purity and consistent quality support strong demand from both the fertilizer and animal feed industries. The steady and large-scale requirement from these sectors ensures monohydrate remains the primary revenue-generating product for most zinc sulfate producers worldwide.

Application Analysis

The agrochemicals market segment leads the application category with nearly 35% market share, supported by the essential role of zinc in plant growth and metabolic activity. Zinc influences hormone formation, enzyme activation, and internode elongation, functions that are critical for crops such as rice, wheat, and corn. Modern intensive farming practices have depleted naturally occurring zinc in soils, making external supplementation through zinc sulfate a necessary practice rather than an optional input. Government initiatives and subsidy programs in major agricultural regions, including China and India, further promote the adoption of micronutrient-enriched fertilizers. As global food production systems focus on improving crop quality, yield, and soil health, zinc sulfate continues to be a vital micronutrient. This strong agricultural dependence ensures that the segment remains the largest consumer of zinc sulfate worldwide.

Regional Insights

North America Zinc Sulfate Market Trends

The North American market, led by the United States, is highly mature and regulated, with strong emphasis on efficient agricultural practices and animal nutrition. Precision farming technologies are widely adopted, boosting demand for high-quality granular zinc sulfate monohydrate that integrates easily with NPK blends. Domestic manufacturers such as Old Bridge Chemical play a major role by offering reliable, high-purity products for agriculture, feed, and pharmaceutical applications.

In the animal nutrition sector, zinc sulfate is a standard additive used to prevent mineral deficiencies in poultry, cattle, and swine. Strict regulatory frameworks such as AAFCO guidelines further ensure that only safe, high-grade material is allowed in feed products. The U.S. pharmaceutical industry also contributes significantly by requiring USP-grade zinc sulfate for medical and supplement applications. These combined factors create a stable, value-driven market environment in North America.

Europe Zinc Sulfate Market Trends

Europe presents a complex and highly regulated market shaped by strong environmental policies and significant industry shifts. The region operates under strict REACH regulations, which require detailed safety and environmental data for all chemical substances, pushing manufacturers toward cleaner technologies and compliance-focused production systems. Recent closures of major local zinc sulfate facilities have created supply gaps, increasing reliance on imports for industrial demand.

Despite these disruptions, countries like Germany, Spain, and Italy remain key centers for chemical manufacturing, textile processing, and high-value agriculture. The European Green Deal and sustainability initiatives encourage reduced nitrogen usage and increased adoption of micronutrient-rich fertilizers, indirectly supporting zinc sulfate consumption. Additionally, the region’s strong water treatment sector continues to utilize zinc sulfate for heavy metal removal and industrial effluent purification. These factors combined shape Europe into a high-compliance, moderate-growth, but strategically important market.

Asia Pacific Zinc Sulfate Market Trends

Asia Pacific is the largest and fastest-growing region for zinc sulfate, driven primarily by expansive agricultural activity in China and India. China’s “Zero Growth in Chemical Fertilizers” policy, which focuses on improving nutrient efficiency rather than increasing fertilizer volume, has increased the use of micronutrient-fortified formulations, including zinc sulfate. India, with its historically low micronutrient usage, is rapidly increasing adoption thanks to government programs like the Soil Health Card Scheme that raise farmer awareness of zinc deficiency. The region is also a global hub for textile manufacturing, especially rayon and viscose fiber production, which generates sustained industrial demand.

Competitive pricing and the presence of numerous regional manufacturers make the market highly dynamic. However, environmental inspections and stricter compliance requirements are gradually consolidating the industry, pushing smaller producers out and strengthening the position of established companies. Asia Pacific’s strong agricultural base and industrial growth ensure long-term market expansion.

Competitive Landscape

The global zinc sulfate market operates with a fragmented structure, characterized by a mix of a few large-scale multinational producers and a multitude of regional manufacturers, particularly in China. The market concentration is low, with no single player holding a dominant global monopoly. Leading companies compete primarily on product purity, particle size consistency (for fertilizer blending), and supply chain reliability. A key differentiator for market leaders is vertical integration; companies that have access to their own zinc mining or recycling operations can better manage raw material price volatility. In recent years, business models have shifted towards "solution selling," where manufacturers offer customized blends or chelated formulations to agricultural clients rather than just selling commodity chemicals. Research and development is increasingly focused on nano-technology and slow-release formulations to improve the bioavailability of zinc in soil applications.

Key Market Developments:

- In September 2024: GRILLO-Werke AG announced it would not rebuild its zinc sulfate plant. This permanent exit of a major European producer has tightened regional supply significantly, opening market share opportunities for competitors.

- In June 2024: Bohigh Group introduced a new nano-zinc sulfate formulation designed for high-efficiency foliar application. The product claims to improve zinc absorption in crops by 30% compared to traditional sulfates, targeting the premium agrochemical segment.

- In November 2024: Changsha Haolin Chemicals Co., Ltd. completed the expansion of its production line for feed-grade zinc sulfate. The upgrade focuses on reducing heavy metal impurities to meet stricter export standards for the European and North American animal nutrition markets.

Companies Covered in Zinc Sulfate Market

- Midsouth Chemicals

- Gupta Agricare

- China Bohigh

- Rongqing Chemical Co. Ltd

- Clean Agro

- Oasis Fine Chem

- Saba Chemical GmbH

- Redox

- Balaji Industries

- Changsha Haolin Chemicals Co., Ltd

- Old Bridge Chemical

- Tianjin Topfert Agrochemical Co

- FUJI KASEI CO., LTD.

- GRILLO-Werke AG

- Prakash Chemicals

- Zinc Nacional

- Sulfozyme Agro

- Rech Chemical Co. Ltd

Frequently Asked Questions

The global market is projected to reach a valuation of US$ 3.4 billion by the end of 2033, driven by steady demand from the agriculture and pharmaceutical sectors.

The widespread prevalence of zinc deficiency in soils across major agricultural regions is the primary driver, necessitating the use of zinc sulfate as a critical fertilizer additive to ensure crop health and yield.

The Agrochemical segment is the dominant application, accounting for the largest market share as zinc sulfate is the standard solution for correcting micronutrient deficiencies in staple crops worldwide.

Asia Pacific is expected to remain the leading region, supported by the massive agricultural sectors in China and India, along with significant industrial manufacturing capacities for textiles and chemicals.

Bio-fortification of crops represents a significant opportunity, where manufacturers can develop advanced, high-bioavailability zinc formulations to support global initiatives aimed at improving human nutrition through.