- Electrical Equipment & Services

- Ultrasonic Flow Meter Market

Ultrasonic Flow Meter Market Size, Share, and Growth Forecast 2026 - 2033

Ultrasonic Flow Meter Market by Product Type (Inline Ultrasonic Flow Meters, Clamp-On Ultrasonic Flow Meters, Insertion Ultrasonic Flow Meters), by Output Display (Analog Ultrasonic Flow Meters, Digital Ultrasonic Flow Meters), by Technology, by Application, by Regional Analysis, 2026 - 2033

Ultrasonic Flow Meter Market Size and Trend Analysis

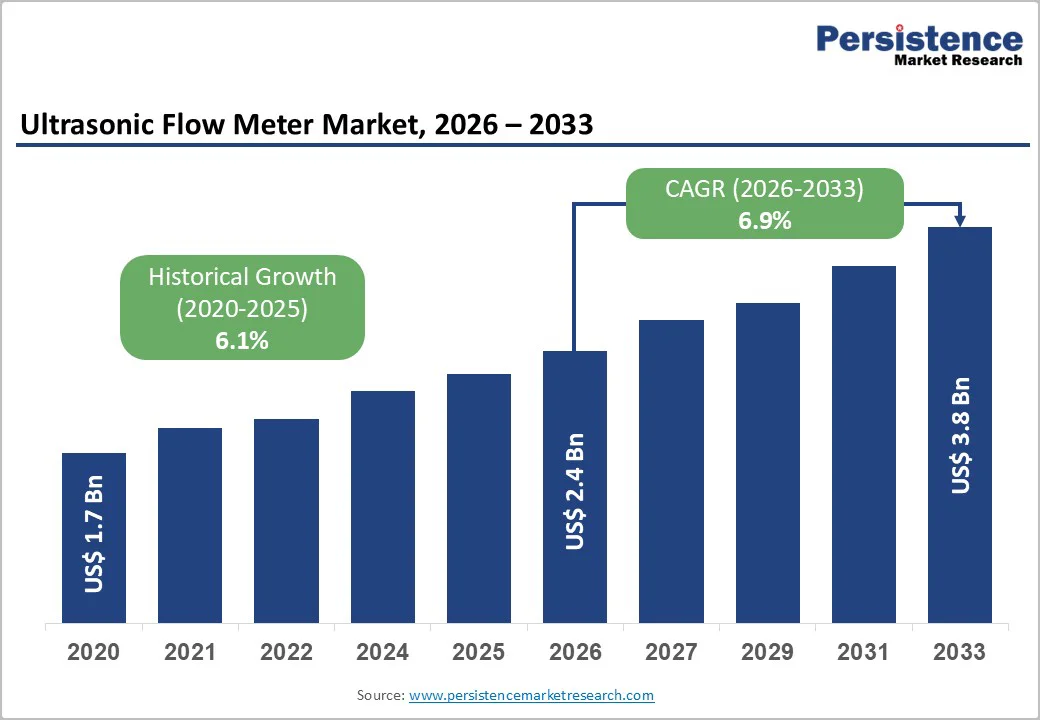

The global ultrasonic flow meter market size is likely to be valued at US$ 2.4 Billion in 2026 and is expected to reach US$ 3.8 Billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 and 2033.

The market is primarily driven by the accelerating adoption of non-intrusive flow measurement technologies in the water and wastewater management sectors. Municipalities and industrial operators are increasingly prioritizing ultrasonic flow meters over mechanical alternatives due to their ability to detect leaks with high precision and their minimal maintenance requirements.

Key Industry highlights:

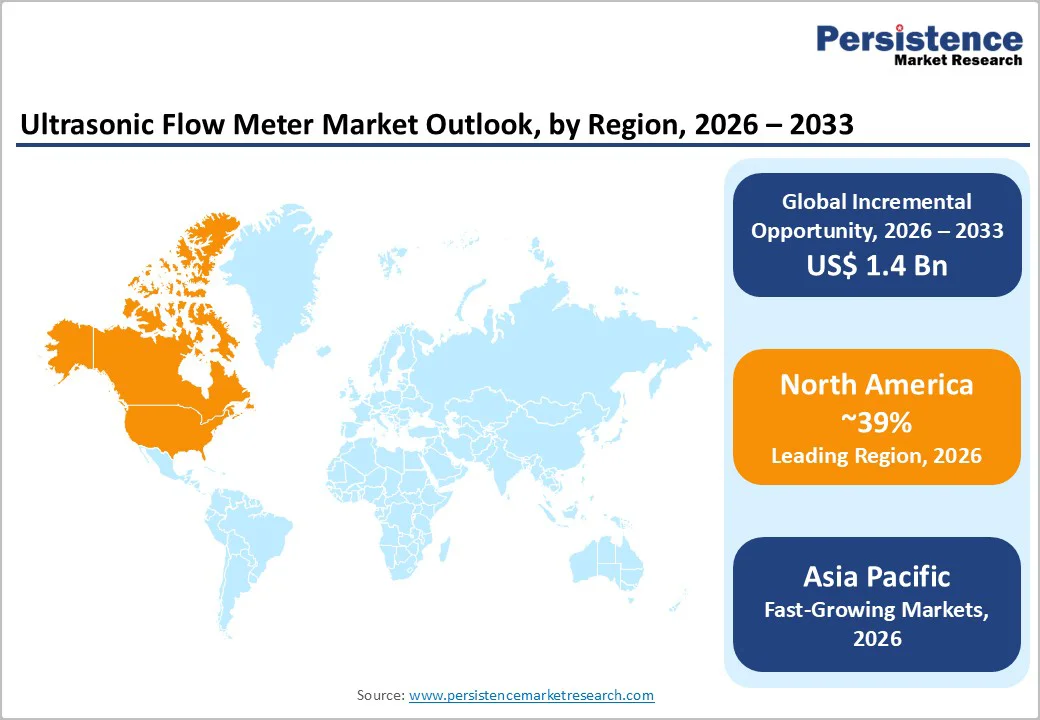

- Leading region: North America dominates the regional category holding 39% share, due to advanced industrial automation and strict regulatory compliance in water and energy sectors.

- Fastest Growing Region: Asia Pacific is expanding rapidly with rising CAGR of 8%, driven by urbanization, smart water infrastructure projects, and industrial growth in China and India.

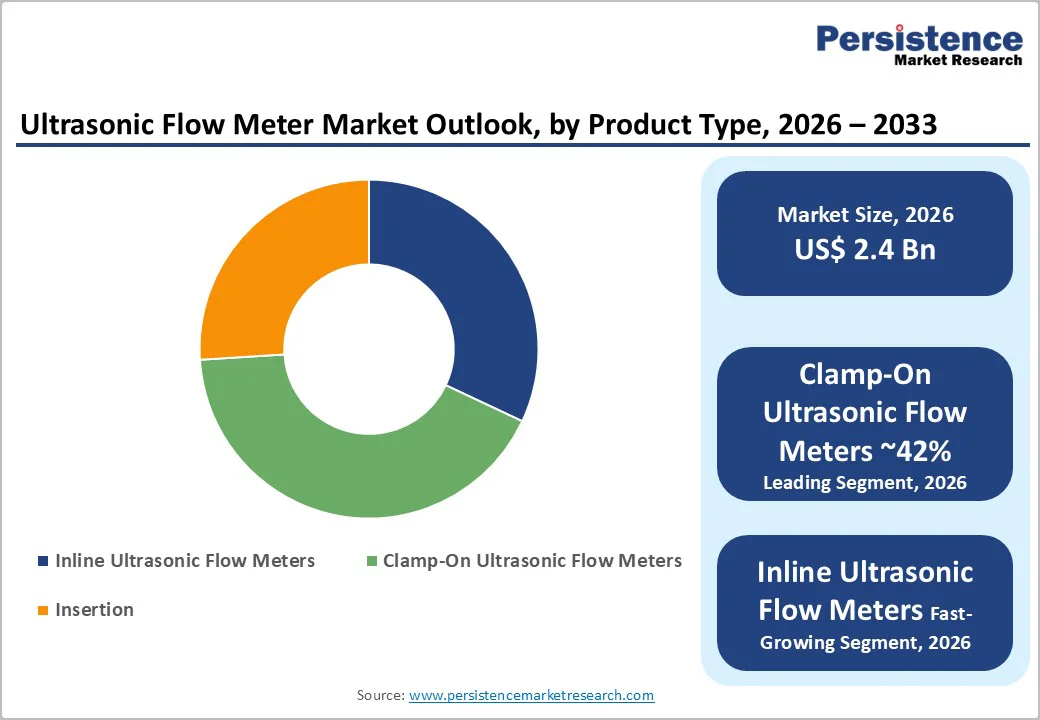

- Dominant Segment: Clamp-On Ultrasonic Flow Meters lead the type category with 42% share, because of their non-intrusive installation and suitability for retrofitting.

- Fastest Growing Segment: Digital Ultrasonic Flow Meters are growing fastest as industries transition to Industry 4.0 and demand IoT-ready measurement devices.

- Key Market Opportunity: Integration of IoT and cloud analytics for remote monitoring and predictive maintenance offers significant revenue potential.

| Key Insights | Details |

|---|---|

| Ultrasonic Flow Meter Market Size (2026E) | US$ 2.4 Billion |

| Market Value Forecast (2033F) | US$ 3.8 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.9% |

| Historical Market Growth (2020 - 2025) | 6.1% |

Market Dynamics

Drivers - Global Demand for Ultrasonic Flow Meters Rises due to Smart City Initiatives, Water Scarcity, and Infrastructure Modernization Efforts

The global movement toward smart cities and intelligent water distribution networks is significantly accelerating the adoption of ultrasonic flow meters. Utilities worldwide are shifting away from older mechanical meters and investing in advanced ultrasonic systems that offer far greater precision, especially at very low flow levels where revenue losses often go unnoticed.

Since ultrasonic meters contain no moving parts, they do not suffer from mechanical wear, enabling them to maintain consistent accuracy throughout their operating life.

This reliability is crucial for utilities facing rising water scarcity pressures and high levels of non-revenue water. In regions such as North America, Europe, and parts of Asia Pacific, governments are heavily funding water infrastructure upgrades, introducing stricter regulatory guidelines, and encouraging digital transformation.

These initiatives are increasing the demand for accurate, maintenance-free flow measurement devices that support leak detection, billing accuracy, and overall water network modernization.

Non-Intrusive Clamp-On Ultrasonic Technology Drives Industrial Adoption by Enabling Precise Flow Measurement without System Disruption or Downtime

Rapid technological improvements, particularly in clamp-on ultrasonic flow meters, have made non-intrusive flow measurement more advanced, precise, and widely accessible. Modern clamp-on systems can measure fluid flow through pipes of varying materials, diameters, and thicknesses without requiring pipe cutting or flow disruption, making them especially beneficial for facilities that cannot afford operational downtime.

This capability is highly valued in sectors such as oil and gas, chemicals, water treatment, and industrial processing, where system integrity and safety are top priorities. The ability to install meters externally and retrofit them onto existing pipelines reduces installation effort and eliminates contamination risks.

These advantages are particularly attractive for brownfield projects aiming to modernize without major structural modifications. As industries continue prioritizing safety, operational continuity, and digital monitoring, non-intrusive ultrasonic technologies are becoming a preferred choice for accurate, dependable, and cost-efficient flow measurement.

Market Restraints

High Initial Costs and Complex Installation Requirements Limit Adoption of Ultrasonic Flow Meters in Budget-Sensitive Industries

Despite their long-term operational benefits, ultrasonic flow meters require a higher initial investment than traditional mechanical alternatives such as turbine, vortex, or positive displacement meters. Their advanced sensing components, digital signal processing hardware, and calibration mechanisms contribute to a significantly higher upfront cost, often creating hesitation among small and mid-sized utilities and industries with limited budgets.

While ultrasonic meters offer advantages such as reduced maintenance, longer service life, and improved reading accuracy, the initial purchase price remains a critical barrier, especially in cost-sensitive markets. Municipal water authorities in developing regions may delay adoption due to budget constraints or prioritize lower-cost mechanical systems even when long-term costs may be higher.

As a result, although the total cost of ownership favors ultrasonic technology, the immediate capital required for deployment continues to restrict market penetration in price-sensitive segments.

Operational Challenges in Dirty or Variable Fluids Restrict Ultrasonic Flow Meter Performance, Requiring Careful Technology Selection and Calibration

Ultrasonic flow meters perform exceptionally well in applications involving clean or moderately clean liquids, but their effectiveness can decrease in more complex fluid environments.

Transit-time meters, which represent the majority of ultrasonic installations, require relatively clear fluid to transmit sound waves reliably. When liquids contain high levels of suspended solids, heavy aeration, or chemical impurities, signal accuracy can be compromised, leading to measurement deviations.

Doppler ultrasonic meters require suspended particles or bubbles to function correctly, meaning they do not perform well in clean liquid conditions.

These operational dependencies make technology selection highly application-specific and require end-users to thoroughly evaluate fluid characteristics before implementing an ultrasonic solution. Industries with varying or unpredictable fluid compositions may find this requirement challenging, which can limit adoption. Such technical constraints, combined with the need for correct installation and calibration, remain notable limitations to wider ultrasonic flow meter usage.

Market Opportunities

IIot Integration and Remote Monitoring Enable Predictive Maintenance, Operational Efficiency, and New Revenue Streams for Ultrasonic Flow Meters

One of the most promising growth opportunities in the ultrasonic flow meter market lies in its integration with Industrial Internet of Things (IIoT) platforms, automation systems, and digital monitoring tools. Modern ultrasonic meters increasingly feature wireless communication capabilities, cloud connectivity, data analytics functions, and real-time diagnostics that allow operators to monitor performance remotely.

These innovations enable predictive maintenance, early fault detection, and improved asset management, helping industries minimize downtime and optimize operations.

Utility companies and industrial plants are increasingly adopting advanced data-driven systems to streamline resource planning, operational forecasting, and equipment health monitoring. Manufacturers offering complementary software platforms, such as remote monitoring dashboards, automated alerts, and analytics-as-a-service, can establish long-term subscription-based revenue streams.

As digital transformation accelerates across sectors like water management, oil and gas, power generation, and manufacturing, ultrasonic meters equipped with IIoT intelligence are becoming integral to modern smart infrastructure.

Growing District Heating and Energy Efficiency Initiatives Drive Demand for High-Accuracy, Maintenance-Free Ultrasonic Flow Meters Worldwide

Global initiatives to enhance energy efficiency, reduce emissions, and decarbonize heating and cooling systems are significantly boosting demand for ultrasonic flow meters. District heating and cooling networks require highly accurate, maintenance-free meters capable of measuring thermal energy and fluid flow at varying temperatures and pressures.

Ultrasonic meters meet these requirements exceptionally well due to their reliability, stable accuracy, and compatibility with energy management systems.

As European countries expand district heating infrastructure to reduce greenhouse gas emissions and Asia Pacific economies increase investment in energy-efficient building systems, the need for advanced metering technology is rising. Ultrasonic meters are also becoming essential in optimizing energy distribution, improving billing accuracy, and reducing losses from inefficient systems.

Their ability to operate without moving parts and withstand harsh thermal conditions makes them an ideal solution for fast-growing district energy, renewable heating, and industrial thermal applications worldwide.

Category-wise Analysis

By Product Insights

Clamp-on ultrasonic flow meters remain the fastest-growing type segment, holding a 42% market share, as per the provided dataset. Their strong adoption is mainly due to their non-intrusive design, which allows the device to be mounted externally on pipelines without cutting or interrupting flow.

This capability eliminates any chance of leakage, product contamination, or system shutdown, making these meters highly preferred in sensitive sectors such as Food & Beverages and Pharmaceuticals. Additionally, the ability to retrofit these meters onto existing pipelines reduces installation labor, project delays, and operational losses, which makes them a cost-effective option for facilities looking to upgrade outdated mechanical systems.

By Output Display Analysis

Digital Ultrasonic Flow Meters lead the output display category with a 65% market share, according to the provided dataset. This shift toward digital readouts is accelerated by the growing industry need for precise measurements, stable performance, and reliable data under varying process conditions.

Digital signal processing (DSP) technology helps reduce errors caused by vibration, temperature shifts, or high-noise environments, ensuring consistent performance even in harsh industrial settings. Furthermore, the digital interface supports seamless integration with automation platforms such as SCADA and PLC systems, which are essential for Industry 4.0 upgrades.

These capabilities make digital meters the preferred choice for modern industrial and utility operations.

By Technology Analysis

Transit Time-Single/Dual Path Ultrasonic Flow Meters dominate the technology category with nearly 55% market share, based on the provided dataset. Their popularity comes from their proven accuracy, reliability, and cost-efficiency when measuring clean liquids, including water, refined fuels, and hydrocarbons. These systems are widely accepted across industries because they deliver consistent results for general process monitoring and performance optimization.

While multi-path units are typically chosen for custody-transfer applications, single and dual-path designs strike an ideal balance between affordability and precision. As a result, they remain the primary choice across utility-driven industries such as Water & Wastewater, Power Generation, and general industrial operations.

By Application Insights

The Water and Wastewater segment leads this category with a 38% market share, as stated in the provided dataset. This dominance is driven by increased global pressure to improve water conservation, reduce leakages, and ensure accurate consumption measurement. Ultrasonic flow meters are becoming essential tools for utilities because they can detect leakage, measure low flow rates, and support billing accuracy better than aging mechanical meters.

Their ability to capture a wider flow range helps municipalities minimize revenue losses associated with under-registration. Additionally, regulatory requirements in regions like Europe and the United States emphasize sustainable water management and digital monitoring, further strengthening the segment’s leading position.

Regional Insights

North America Ultrasonic Flow Meter Market Trends

North America holds one of the largest shares in the ultrasonic flow meter market, supported by extensive investment in water infrastructure modernization, industrial automation, and smart metering technologies.

The region’s advanced oil and gas sector, particularly shale exploration, requires high-precision, non-intrusive flow measurement solutions, which strengthens demand for ultrasonic meters. Regulatory agencies enforce stringent monitoring standards, compelling industries to adopt accurate, reliable, and digitally compatible flow measurement systems.

Aging municipal water networks across the United States are undergoing upgrades to reduce leakage, improve billing accuracy, and enhance operational efficiency. Many utilities are transitioning toward remote monitoring and IIoT-enabled flow systems, further boosting adoption.

The presence of leading manufacturers, early technology adoption culture, and strong emphasis on environmental compliance continue to position North America as a key growth hub for ultrasonic metering solutions across both municipal and industrial applications.

Europe Ultrasonic Flow Meter Market Trends

Europe’s ultrasonic flow meter market is strongly influenced by the region’s focus on environmental sustainability, energy efficiency, and strict regulatory compliance. European countries have invested heavily in district heating networks, industrial energy optimization, and wastewater monitoring systems, all of which require highly accurate and maintenance-free flow measurement technologies.

Ultrasonic meters have become essential in these areas due to their reliability, long operational life, and ability to integrate with advanced automation systems.

The region’s robust chemical, pharmaceutical, and food processing industries also require hygienic, contamination-free measurement solutions, making clamp-on ultrasonic technology particularly attractive.

Additionally, the European Union’s regulatory framework emphasizes water conservation, emission reduction, and efficient resource usage, further accelerating the demand for digital ultrasonic meters. As industrial plants and utilities continue modernizing systems and adopting smart infrastructure solutions, Europe maintains strong momentum in ultrasonic flow meter deployment.

Asia Pacific Ultrasonic Flow Meter Market Trends

Asia Pacific is the fastest-growing region in the global ultrasonic flow meter market, driven by rapid industrialization, urban expansion, and widespread investment in water and energy infrastructure. Countries such as China, India, Japan, and those in Southeast Asia are actively upgrading water treatment plants, developing smart city initiatives, and expanding manufacturing operations, all of which require accurate and efficient flow measurement technologies.

Ultrasonic meters are becoming a preferred choice due to their low maintenance requirements, high accuracy, and flexibility in both new and retrofit installations. The region’s booming energy demand, expansion of power generation facilities, and growth in refining and petrochemical industries further support market growth.

Additionally, government programs targeting water resource efficiency, leakage control, and digital utility management are accelerating the adoption of smart ultrasonic metering systems across both municipal and industrial environments.

Competitive Landscape

The global ultrasonic flow meter market is moderately consolidated, with a few major multinational corporations dominating the high-end and custody transfer segments, while numerous regional players compete in the standard utility segments. Market leaders like Emerson Electric Co. and Siemens AG focus on strategic partnerships and acquisitions to expand their technology portfolios.

A key differentiator for these leaders is their heavy investment in Research and Development (R&D) to enhance digital signal processing and diagnostic capabilities. Emerging business models are increasingly service-oriented, with companies offering "metering as a service" or data analytics packages alongside hardware sales to lock in long-term customer value.

Key Market Developments:

- In April, 2025: Emerson Electric Co. launched the FLUXUS / PIOX 731 clamp-on meter series, offering high-performance, non-intrusive measurement for both liquids and gases. The new range enhances accuracy, reduces installation complexity, and supports advanced industrial monitoring.

- In October, 2024: Endress+Hauser updated its Prosonic clamp-on flowmeter line with FlowDC technology, enabling precise measurement even with limited straight-pipe lengths. This innovation improves installation flexibility and ensures reliable performance in space-constrained industrial environments.

- In May, 2023: Siemens introduced the Ultrasonic Gas FS-DSL, a digital, low-power flow measurement system engineered for gas applications. The device is optimized for solar-powered remote sites, providing continuous, reliable operation in off-grid and long-distance monitoring environments.

Companies Covered in Ultrasonic Flow Meter Market

- General Electric

- Emerson Electric Co.

- Greyline Instruments

- Honeywell International Inc.

- OMEGA Engineering Inc.

- Proflow

- Siemens AG

- Endress+Hauser Management AG

- Hontzsch GmbH & Co. KG

- KRONE Group

- UFM

- FLEXIM

- MIB GmbH

- Pietro Fiorentini S.p.A

- KOBOLD Messring GmbH

Frequently Asked Questions

The market is projected to reach a valuation of US$ 3.8 Billion by the end of 2033, driven by increasing industrial automation.

The primary driver is the need for accurate, non-intrusive flow measurement in water management and leak detection applications to conserve resources.

The Transit Time-Single/Dual Path Ultrasonic Flow Meters segment leads the market due to its high accuracy in measuring clean liquids across various industries.

North America is the leading region, supported by established infrastructure, technological advancements, and a strong oil and gas sector.

A key opportunity lies in the integration of IoT connectivity and smart diagnostics into flow meters to enable remote monitoring and predictive maintenance.

Key players include Emerson Electric Co., Siemens AG, Endress+Hauser Management AG, General Electric, and Honeywell International Inc. among others.