- Electrical Equipment & Services

- Ultrasonic Level Sensors Market

Ultrasonic Level Sensors Market Size, Share, and Growth Forecast 2026 - 2033

Ultrasonic Level Sensors Market by Product Type (Continuous Ultrasonic Level Sensors, Point Ultrasonic Level Sensors), by Range (Short Range Ultrasonic Level Sensors, Medium Range Ultrasonic Level Sensors, Long Range Ultrasonic Level Sensors), Industry (Medical, Automotive, Industrial, Food & Beverage, Pulp & Paper, Chemical, Oil & Gas, Wastewater Management, and Others), and Regional Analysis 2026 - 2033

Ultrasonic Level Sensors Market Size and Trend Analysis

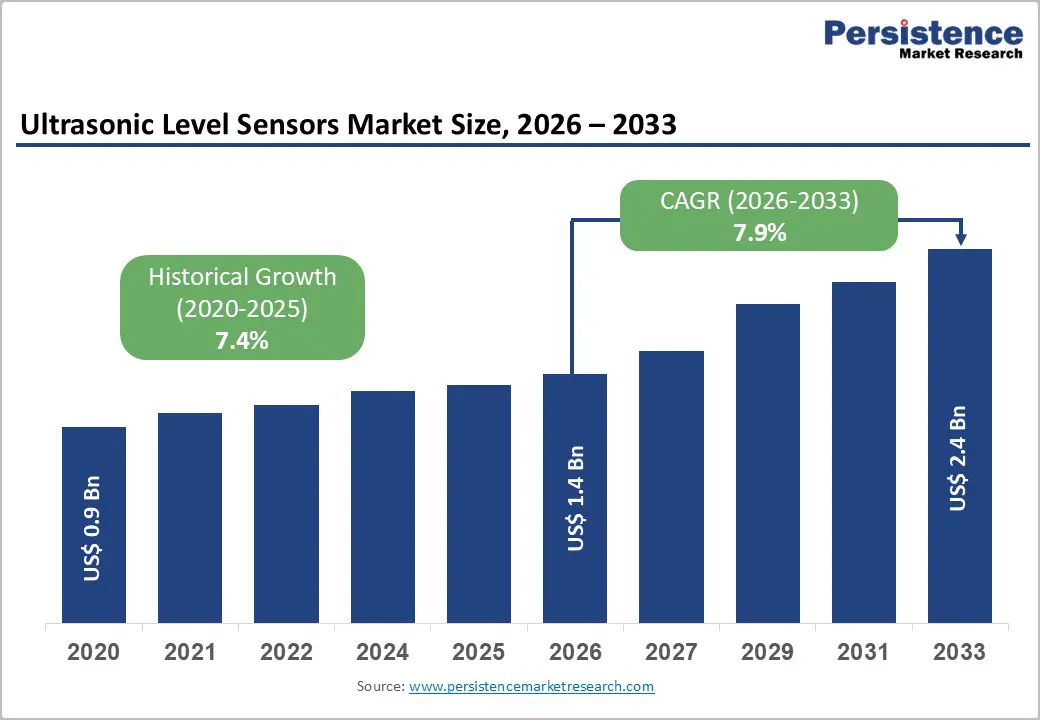

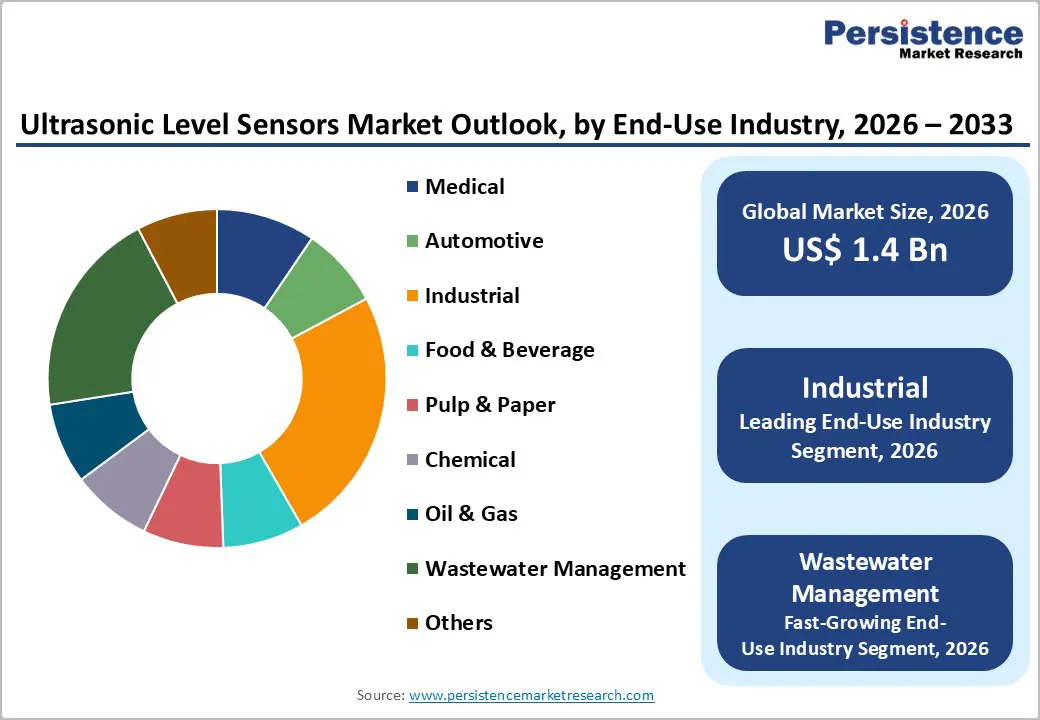

The global ultrasonic level sensors market size is expected to be valued at US$ 1.4 billion in 2026 and projected to reach US$ 2.4 billion by 2033, growing at a CAGR of 7.9% between 2026 and 2033.

Growth is primarily driven by rising adoption of industrial automation and Industry 4.0, which demand accurate, non-contact level measurement solutions. Ultrasonic level sensors support real-time monitoring in harsh and hazardous environments, helping industries reduce maintenance costs while enhancing operational safety. Strong uptake across chemicals, water and wastewater treatment, and process industries is further supported by environmental regulations and smart utility initiatives. Integration with IoT platforms enables predictive maintenance and efficient resource management, accelerating deployment in municipal and industrial infrastructure projects worldwide.

Key Industry Highlights:

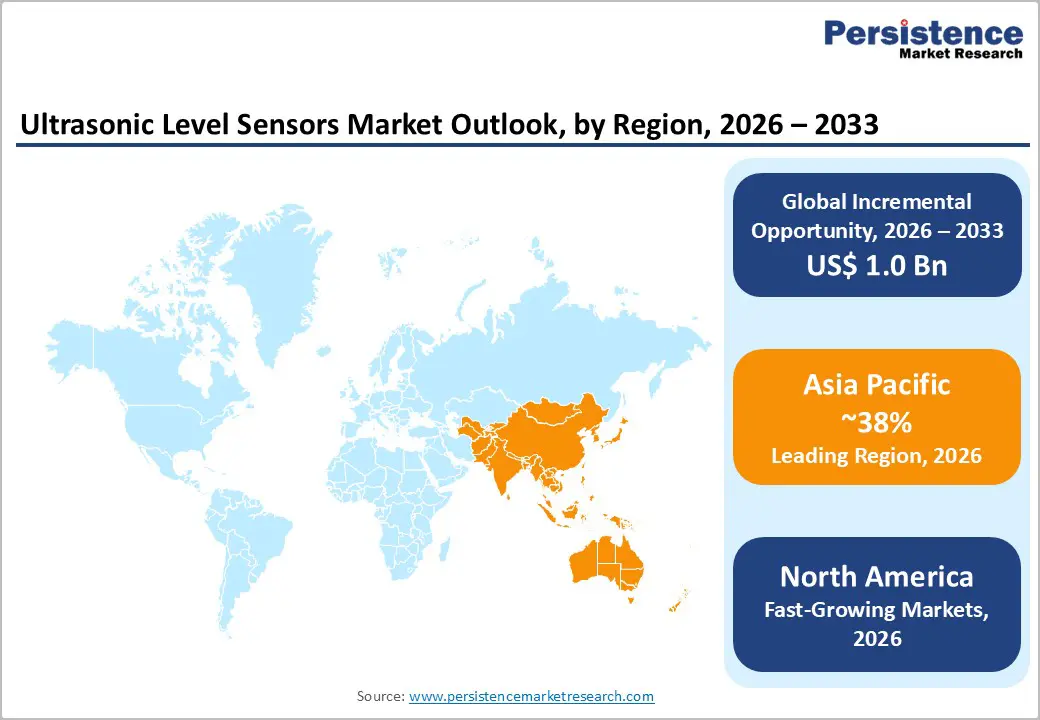

- Leading Region: Asia Pacific leads the Ultrasonic Level Sensors market with ~38% share in 2025, supported by large-scale industrialization in China, strong manufacturing ecosystems in Japan and South Korea, and rising smart water and infrastructure projects across India and Southeast Asia.

- Fastest-Growing Region: North America emerges as the fastest-growing region, driven by stringent U.S. environmental regulations, rapid adoption of industrial automation, and strong integration of ultrasonic sensors across wastewater treatment, oil & gas storage, and smart utility infrastructure.

- Leading Product Category: Continuous ultrasonic level sensors dominate with ~65% share in 2025, owing to their ability to deliver real-time, non-contact monitoring across liquids and bulk solids in industrial tanks, silos, and process vessels.

- Leading Range Category: Medium-range ultrasonic level sensors hold ~50% share in 2025, preferred for their balanced accuracy and coverage in standard industrial tanks across food processing, chemicals, and water treatment applications.

- Key Opportunity Area: Wastewater and municipal water management represent a major opportunity, as utilities increasingly deploy IoT-enabled ultrasonic sensors for overflow prevention, real-time monitoring, and sustainable urban infrastructure development.

| Key Insights | Details |

|---|---|

| Ultrasonic Level Sensors Size (2026E) | US$ 1.4 Billion |

| Market Value Forecast (2033F) | US$ 2.4 Billion |

| Projected Growth CAGR(2026-2033) | 7.9% |

| Historical Market Growth (2020-2025) | 7.4% |

Market Dynamics

Drivers

Growing Demand for Industrial Automation and Smart Manufacturing Systems

The rapid expansion of industrial automation is a key driver for ultrasonic level sensors, as industries increasingly require accurate, non-contact level measurement across manufacturing and process operations. These sensors are widely adopted for their ability to perform reliably in harsh environments involving dust, vapors, and corrosive materials. Real-time level monitoring supports improved process control, inventory management, and flow regulation across automated production lines.

Integration with Industry 4.0 frameworks further strengthens demand, enabling predictive maintenance and reducing unplanned downtime. Advances in digital signal processing allow ultrasonic sensors to compensate for temperature variations and environmental noise, improving measurement accuracy. As global investments in factory automation and smart manufacturing continue to rise, ultrasonic level sensors remain critical components in digitally connected industrial ecosystems.

Increasing Impact of Environmental, Safety, and Regulatory Compliance Requirements

Stringent environmental and safety regulations across the chemical, oil & gas, and wastewater industries are accelerating the adoption of ultrasonic level sensors. Regulatory bodies mandate accurate and continuous monitoring of liquids and hazardous materials to minimize risks related to leaks, overflows, and emissions. Ultrasonic sensors support compliance by enabling remote, non-intrusive measurement, significantly reducing human exposure in dangerous operating zones.

Energy-efficiency and sustainability-focused regulations, particularly in Europe and developed regions, promote the use of advanced monitoring technologies. Ultrasonic level sensors help organizations meet regulatory standards by enhancing process transparency and operational reliability. Growing emphasis on regulatory compliance and risk mitigation positions these sensors as essential tools for safe, environmentally responsible industrial operations.

Restraints

Performance Limitations Due to Environmental Interference and Signal Disturbance

Ultrasonic level sensors are susceptible to performance issues caused by environmental interference, particularly in dense industrial settings with multiple sensing devices operating simultaneously. Signal cross-talk and echo overlap can occur when sensors are installed in close proximity, leading to inaccurate or unstable readings. This challenge is especially common in automated factories, robotics, and automotive assembly lines where space constraints are significant.

Although mitigation techniques such as signal synchronization, filtering algorithms, and controlled installation layouts are available, they increase system complexity and limit flexibility. In highly complex or confined environments, these constraints can restrict broader adoption, as end users may prefer alternative sensing technologies offering more stable performance under crowded operational conditions.

High Initial Investment and Ongoing Calibration Complexity

High upfront costs associated with advanced ultrasonic level sensors, particularly models integrated with internet of things (IoT) and smart monitoring capabilities, act as a restraint for small and mid-sized enterprises. Beyond initial procurement, these sensors often require careful calibration to maintain accuracy in challenging conditions involving foam, vapor, turbulence, or temperature fluctuations.

Regular calibration and maintenance increase total cost of ownership, reducing short-term cost attractiveness despite long-term operational benefits. In price-sensitive markets, industries may opt for simpler or lower-cost level measurement technologies, slowing ultrasonic sensor penetration even as awareness of lifecycle efficiency gains continues to grow.

Opportunities

Rising Adoption in Wastewater Treatment and Smart Water Infrastructure

Significant growth opportunities are emerging in wastewater treatment and smart water management systems, where ultrasonic level sensors enable reliable, non-contact monitoring of tanks, reservoirs, and open channels. Municipal utilities increasingly deploy these sensors to optimize pumping, dosing, and overflow prevention through seamless SCADA integration. Real-time level data improves operational efficiency while supporting sustainability and regulatory compliance initiatives.

Rapid urbanization and infrastructure modernization across developing and developed regions are accelerating investments in smart utilities. Advancements in MEMS-based ultrasonic technology have led to compact, energy-efficient sensors suited for dense urban water networks. As cities prioritize digital water management and environmental protection, ultrasonic level sensors are expected to capture substantial revenue opportunities through 2033.

Growth Potential from IoT-Enabled Predictive Maintenance and Connected Industry

The integration of ultrasonic level sensors with IoT platforms presents strong opportunities within Industry 4.0 and connected industrial environments. Smart sensors equipped with wireless communication technologies such as LoRaWAN and industrial IoT protocols enable continuous remote monitoring of storage tanks, chemical vessels, and oil depots. This connectivity supports predictive maintenance strategies by providing real-time analytics and early fault detection.

Edge computing capabilities further enhance data-driven decision-making, helping industries reduce downtime and maintenance costs. Adoption of predictive monitoring solutions is increasing across automation hubs and emerging industrial regions, positioning IoT-enabled ultrasonic level sensors as key components in next-generation industrial monitoring systems.

Category-wise Analysis

Product Type Insights

Continuous ultrasonic level sensors lead the market with approximately 65% share in 2025, driven by their ability to provide real-time, non-contact measurement of both liquids and bulk solids. These sensors are widely deployed in storage tanks, silos, and process vessels where continuous level data is critical for process control and inventory management. Their superior accuracy compared to point-level sensors, along with advancements in signal processing that reduce false echoes, makes them highly suitable for dynamic environments such as wastewater treatment and chemical processing.

Point ultrasonic level sensors represent the fastest-growing product category, supported by increasing demand for cost-effective level detection in discrete applications. Growth is fueled by their simplified installation, compact design, and suitability for alarms, overfill protection, and basic automation tasks. Expanding use in small-scale manufacturing, packaging, and utility infrastructure is accelerating adoption across emerging industrial facilities.

Range Insights

Medium-range ultrasonic level sensors account for around 50% of the market in 2025, as they effectively balance measurement accuracy and coverage for standard industrial tanks and vessels up to moderate heights. These sensors are commonly used across food processing, chemicals, and water treatment applications, where consistent performance, minimized dead zones, and reliable beam focus are essential. Their ability to adapt to temperature variations and maintain accuracy under fluctuating operating conditions supports widespread deployment.

Long-range ultrasonic level sensors are the fastest-growing segment, driven by rising demand in large storage tanks, reservoirs, and open-channel monitoring. Infrastructure expansion, particularly in water management and bulk material handling, is increasing the need for extended measurement capability. Improved transducer power and enhanced echo-processing algorithms enable reliable performance in wide-area and outdoor installations.

Industry Insights

The industrial sector dominates the ultrasonic level sensors market with roughly 40% share in 2025, supported by strong automation requirements across manufacturing, chemicals, pulp and paper, and process industries. Ultrasonic sensors are favored for their ability to operate in harsh conditions involving dust, vapor, and corrosive materials, enabling accurate level control in hoppers, silos, and vessels. Integration with IoT platforms further enhances operational efficiency and process visibility.

Municipal and utilities applications are the fastest-growing end-use categories, driven by smart city initiatives and investments in digital water and wastewater infrastructure. Rising focus on real-time monitoring, leak prevention, and sustainable resource management is expanding sensor deployment. Growing urban populations and infrastructure upgrades continue to support strong adoption across public utility systems.

Regional Insights

North America Ultrasonic Level Sensors Market Trends

North America accounts for approximately 35% of the global ultrasonic level sensors market, driven by strong industrial automation maturity and stringent regulatory frameworks. The United States leads regional demand due to strict EPA regulations requiring precise level monitoring in wastewater treatment, oil & gas storage, and chemical processing. High adoption across utilities and process industries positions ultrasonic sensors as core components for non-contact, safety-critical measurement applications.

Growth momentum is reinforced by advanced R&D ecosystems and innovation hubs developing IoT-enabled and smart ultrasonic sensors. These technologies support predictive maintenance, reduce operational downtime, and enhance asset reliability. Widespread integration into smart infrastructure and digital utility projects continues to expand deployment, especially across municipal water systems and energy-related industries.

Europe Ultrasonic Level Sensors Market Trends

Europe represents a technologically advanced market, supported by strong engineering capabilities and harmonized regulatory standards. Germany accounts for nearly 30% of regional production, excelling in precision sensor manufacturing for chemical and industrial applications. EU-wide environmental and safety directives are accelerating adoption, particularly in wastewater treatment and emissions-controlled industrial processes.

The European ultrasonic level sensors market is projected to grow at a CAGR of 8.4%, driven by sustainability initiatives and energy-efficiency mandates. Countries such as France, the UK, and Spain are increasingly integrating ultrasonic sensors into predictive maintenance systems and smart utility networks. Focus on green manufacturing, digital transformation, and compliance-driven automation continues to support steady regional growth.

Asia Pacific Ultrasonic Level Sensors Market Trends

Asia Pacific holds approximately 38% share of the global market, making it the largest and fastest-expanding regional contributor. China dominates demand through large-scale industrialization and infrastructure development, while Japan and South Korea lead in high-precision and premium ultrasonic sensor manufacturing. Rapid expansion of manufacturing capacity across ASEAN economies further strengthens regional adoption.

Growth is fueled by rising automation investments, smart city initiatives, and water management projects, particularly in India and Southeast Asia. Local manufacturers are innovating cost-effective ultrasonic solutions tailored to price-sensitive markets, accelerating penetration across industrial and municipal applications. The region’s strong manufacturing base and infrastructure expansion continue to position Asia Pacific as a key growth engine.

Competitive Landscape

The ultrasonic level sensors market is moderately fragmented, characterized by the presence of established players alongside a growing base of agile small and mid-sized manufacturers. Market leaders compete on product reliability, global distribution strength, and long-term performance in harsh industrial environments. Continuous investments in research and development focus on improving signal processing accuracy, durability, and adaptability across diverse applications.

At the same time, emerging players are gaining traction through niche innovations, particularly in AI-driven signal filtering, IoT connectivity, and edge analytics. Strategic partnerships with automation and Industry 4.0 solution providers are increasingly common. Competition is intensifying around wireless capabilities, predictive maintenance features, and value-added digital services that enhance operational efficiency for end users.

Key Developments:

- In May 2025, Endress+Hauser’s development team received the AMA Innovation Award 2025 for the Prosonic Flow P 500 ultrasonic flowmeter, enabling advanced non-contact measurement at temperatures up to 550°C, strengthening performance in extreme industrial process environments.

- In September 2025, VEGA introduced a compact 80 GHz radar sensor series to complement ultrasonic solutions for water and utility applications, improving measurement reliability in harsh operating conditions and expanding monitoring capabilities across challenging wastewater and infrastructure projects.

Companies Covered in Ultrasonic Level Sensors Market

- ABB Limited

- Endress+Hauser Management AG

- Siemens AG

- Krohne

- Pepperl+Fuchs GmbH

- Continental AG

- VEGA Grieshaber KG

- Hans TURCK GmbH & Co. KG

- Gems Sensors, Inc.

- Omega Engineering Inc.

- KEYENCE CORPORATION

- Texas Instruments Incorporated

- MIGATRON CORPORATION

- Honeywell International Inc.

- Ultrasonic Level Sensors Market Size & Growth Insights, 2033

AMETEK.Inc.

Frequently Asked Questions

The global Ultrasonic Level Sensors market is projected to reach US$ 1.4 Billion by 2026, driven by rising adoption across industrial and utility applications.

Rising industrial automation and Industry 4.0 integration drive demand for precise, non-contact level measurement in manufacturing and chemicals.

Asia Pacific leads with ~38% market share in 2025, supported by large-scale industrialization, manufacturing expansion, and smart infrastructure development.

Wastewater treatment and smart water management, leveraging IoT for real-time monitoring and sustainability.

Leading players include Endress+Hauser Management AG, Siemens AG, Krohne, and Pepperl+Fuchs GmbH.