- Automation & Robotics

- Phased Array Ultrasonic Testing (PAUT) Market

Phased Array Ultrasonic Testing (PAUT) Market Size, Share, and Growth Forecast, 2026-2033

Phased Array Ultrasonic Testing (PAUT) Market by Technology (Manual, Automatic), Application (Weld Inspection, Crack Detection, Erosion & Corrosion Mapping, Volumetric Inspection, Complex Geometry Scanning), End-Use (Power & Energy, Building & Construction, Oil & Gas, Shipbuilding, Aerospace, Petrochemical, Others), and Regional Analysis for 2026-2033

Phased Array Ultrasonic Testing (PAUT) Market Share and Trends Analysis

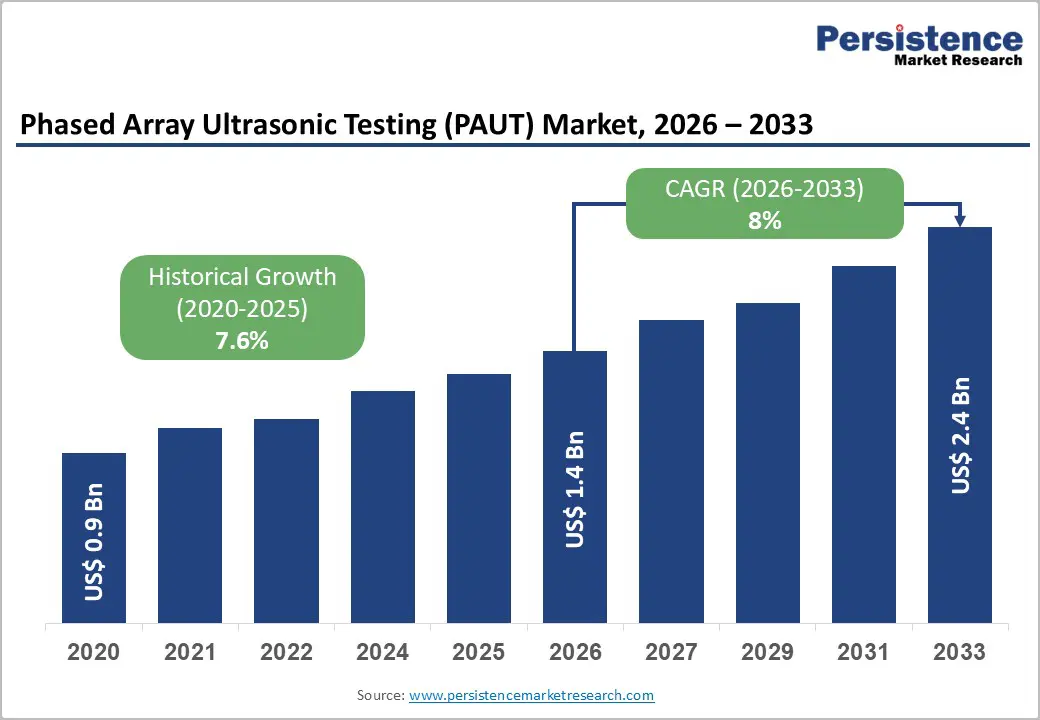

The global phased array ultrasonic testing (PAUT) market size is likely to be valued at US$ 1.4 billion in 2026, and is projected to reach US$ 2.4 billion by 2033, growing at a CAGR of 8% during the forecast period 2026-2033. Market traction is being driven by the increasing reliance on advanced non-destructive testing [NDT] methods that can deliver higher accuracy and faster inspection cycles than conventional techniques. As industrial assets are aging and operating conditions are becoming more demanding, inspection reliability is becoming a core requirement rather than a compliance exercise. Adoption of PAUT is accelerating across energy, aerospace, and infrastructure sectors where asset integrity management and regulatory oversight are intensifying.

Phased array ultrasonic testing is also gaining preference for applications such as complex weld inspection and detailed corrosion mapping, where high resolution imaging and defect characterization are critical for risk mitigation. Digital inspection workflows and data driven maintenance strategies are further reinforcing uptake, as PAUT systems integrate more seamlessly with asset management platforms. For businesses, investing in advanced software analytics, skilled operator training, and industry specific inspection solutions can generate new growth avenues and open up new revenues streams.

Key Industry Highlights

- Dominant Application: Weld inspection is expected to account for around 38% of PAUT market revenue in 2026, while crack detection is projected to be the fastest-growing application at 8.6% CAGR through 2033, driven by preventive maintenance demand.

- Technology Leadership: Manual PAUT systems are projected to lead with approximately 60% share in 2026, while automatic PAUT solutions are expected to grow the fastest at about 9.1% CAGR through 2033, supported by inspection automation.

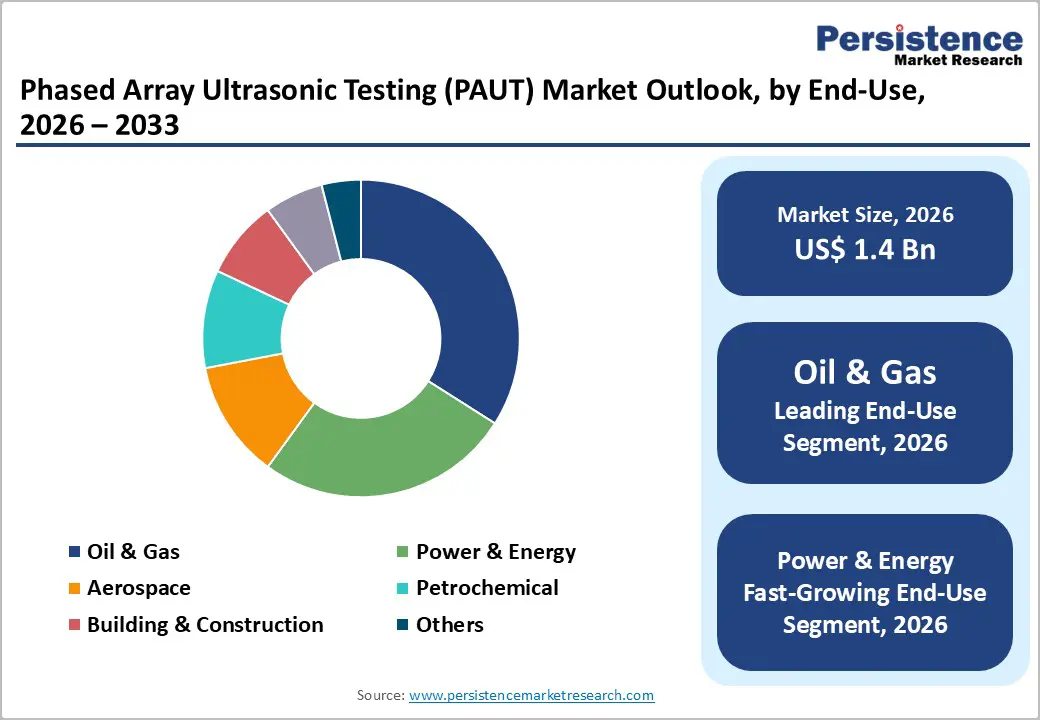

- End-Use Dominance: The oil & gas sector is anticipated to hold nearly 34% share in 2026, while power & energy is forecast to be the fastest-growing end-use segment at 8.8% CAGR, driven by aging assets and safety regulations.

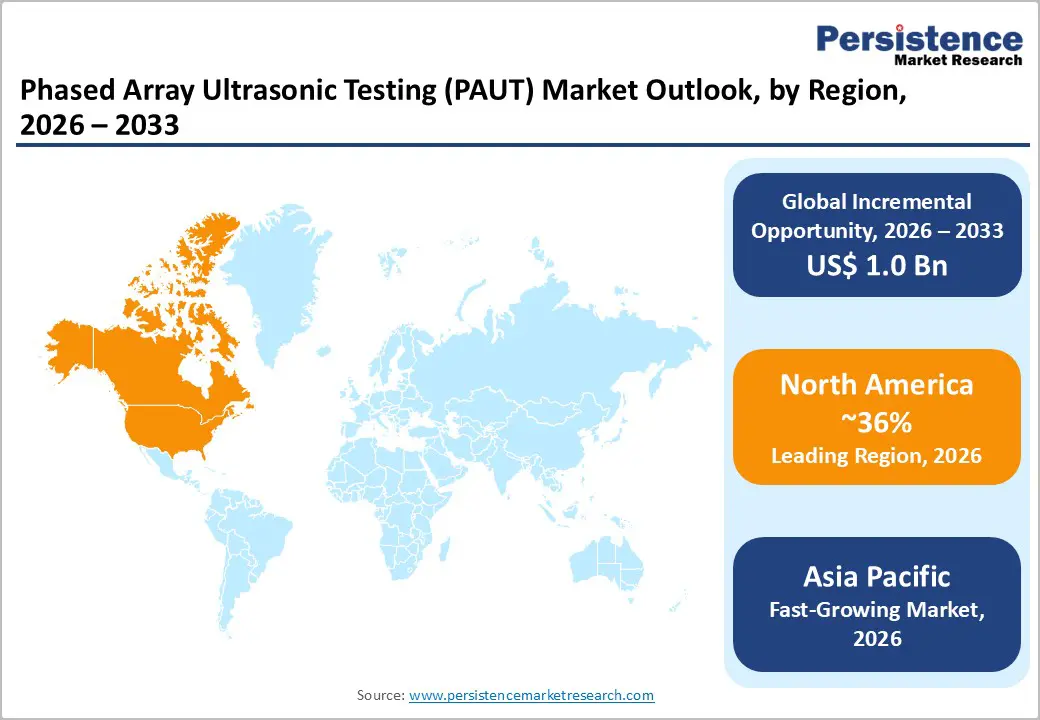

- Regional Leadership: North America is projected to lead with an estimated 36% market share in 2026, while the Asia Pacific market is expected to register the fastest growth at 9.3% CAGR during 2026–2033.

- Competitive & Technology Trends: The market competition is shaped by product launches and acquisitions, alongside rising adoption of AI-driven analytics and automated PAUT platforms to improve inspection accuracy and efficiency.

- January 2025: Mitsubishi Heavy Industries Compressor International integrated a PAUT system into steam turbine maintenance to detect hard-to-find rotor cracks in blade attachment areas non-destructively.

| Key Insights | Details |

|---|---|

| Phased Array Ultrasonic Testing Market Size (2026E) | US$ 1.4 Bn |

| Market Value Forecast (2033F) | US$ 2.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Regulatory Compliance Reinforced by Advanced Inspection Capabilities

The regulatory mandates from bodies such as the U.S. Nuclear Regulatory Commission (NRC) and the Pipeline and Hazardous Materials Safety Administration (PHMSA) require stringent inspection routines to prevent failures in critical infrastructure. Within nuclear power and oil & gas facilities, these requirements drive consistent adoption of phased array ultrasonic testing due to its non-destructive precision and proven ability to detect subsurface flaws that are not visible through conventional inspection methods. As safety standards tighten and enforcement becomes more rigorous, asset owners increasingly rely on PAUT to meet compliance obligations while minimizing operational risk and unplanned downtime. This regulatory reliance ensures recurring inspection cycles and sustained demand for advanced ultrasonic testing solutions.

The technological innovations are strengthening the impact of regulatory-driven demand. Advances such as AI and machine learning integration, cloud-based analytics, and total focusing method (TFM) significantly enhance defect detection accuracy and inspection throughput. These capabilities improve data reliability, reduce interpretation variability, and support faster decision-making in safety-critical environments. Improved imaging resolution and real-time analytics also enable the identification of faults earlier, supporting proactive maintenance strategies. These regulatory pressures and technology-enabled precision are positioning PAUT as a preferred inspection solution for high-risk industrial assets, reinforcing its long-term relevance and adoption across regulated industries.

High Capital Intensity and Skilled Workforce Constraints

Advanced PAUT systems and their accompanying software solutions require sizable upfront capital investment, which continues to limit adoption among small and medium enterprises. Initial acquisition costs can exceed approximately US$ 50,000 per system, depending on configuration and channel count, creating a clear barrier in price-sensitive industrial segments, particularly within developing economies. Budget constraints often delay technology upgrades, even where regulatory or operational needs exist. This cost sensitivity directly contributes to slower year-over-year market growth in emerging regions when compared with North America and Europe. As a result, adoption remains concentrated among large operators with stronger capital expenditure capacity.

The effective deployment of phased array ultrasonic testing systems depends heavily on the availability of certified and experienced technicians capable of accurate probe setup and reliable data interpretation. Industry assessments highlight a persistent shortage of qualified non-destructive testing personnel, which limits inspection scalability and increases dependence on external service providers. These workforce gaps often extend project timelines and elevate operational costs for asset owners. In regions facing technician shortages, inspection service lead times can extend beyond 6–8 weeks, directly affecting maintenance planning and project execution. The capital cost barriers and skills constraints form a structural restraint on the PAUT market growth.

Advanced PAUT Adoption Supported by Government and Industry-Led Initiatives

Automation-enabled and advanced PAUT solutions continue to gain traction as inspection requirements become more complex across defense, energy, and industrial infrastructure. The U.S. Naval Surface Warfare Center Carderock Division awarded contracts for advanced PAUT probes and accessories, reflecting direct governmental investment in enhancing ultrasonic inspection capabilities for defense and critical asset applications. This initiative highlights growing reliance on high-precision PAUT hardware to support structural integrity assessment, lifecycle management, and safety assurance in mission-critical environments. Such government-backed procurement validates long-term demand for advanced PAUT technologies and supports expansion of high-value inspection programs.

A prominent example is the launching of the Joint Industry Project by TWI, focused on evaluating advanced ultrasonic array inspection techniques, including phased array ultrasonic testing integrated with TFM and advanced beamforming technologies. This initiative brings together multiple industrial stakeholders to accelerate validation, standardization, and real-world deployment of next-generation ultrasonic inspection methodologies. Increased collaboration at this level reduces technical adoption barriers and accelerates commercialization timelines for advanced PAUT solutions. These government and industry-led initiatives strengthen the foundation for automation-driven PAUT adoption and support the projected expansion of high-precision inspection applications through 2033.

Category-wise Analysis

Technology Insights

Manual phased array ultrasonic testing technology is expected to lead with an estimated 60% of the PAUT market revenue share in 2026 due to lower upfront cost, operational flexibility, and widespread field usability. Manual systems are widely deployed where inspection environments vary by geometry and access, particularly in rail, pipeline, and structural asset inspections. This dominance is reinforced by government?led field trials, such as the Indian Railways RDSO PAUT single rail tester project, which is conducting phased array rail inspection validation under controlled and extended field trials increasing adoption of manual PAUT field workflows. These initiatives demonstrate real?world demand for operator?controlled phased array inspections across critical infrastructure sectors. As regulatory and asset safety requirements expand, manual PAUT systems continue to anchor the baseline technology share.

Automatic PAUT (APAUT) systems are projected to be the fastest?growing technology segment, projected to expand at an estimated 9.1% CAGR from 2026 to 2033, driven by integration with robotics and repeatable inspection workflows. The growth is supported by technologies that enhance data throughput and enable consistent scan coverage across large assets, addressing demand for higher productivity without sacrificing accuracy. The advanced industry research initiatives have systematically explored ultrasonic array inspection techniques, including Total Focusing Method and advanced beamforming, which underpin next?generation automated phased array ultrasonic testing evaluation standards and improve confidence in automated array solutions. These validated research efforts help reduce technical barriers to deployment, accelerating APAUT adoption across manufacturing and large?scale inspection programs where speed and consistency are essential.

Application Insights

Weld inspection is expected to remain the largest application segment, representing approximately 38% of the phased array ultrasonic testing market revenue share in 2026, driven by its essential role in verifying structural integrity across oil & gas, power plants, and infrastructure assets. PAUT’s real?time imaging and quantitative defect sizing enhance quality assurance and compliance with safety standards. This importance is reinforced by industry participation in major forums such as the 2025 Far East Non Destructive Testing New Technology Conference, where Nantong UNION Digital Technology Development Co., Ltd. showcased its latest phased array series instruments, including the MagicScan MS+ fully focused phased array detector, and won technical awards for performance. Such recognition at high?profile industry events validates PAUT tools’ utility in critical weld inspection scenarios and strengthens stakeholder confidence in phased array solutions.

Crack detection is the fastest?growing application segment, forecast to expand at an estimated 8.6% CAGR from 2026 to 2033, supported by increasing emphasis on early flaw identification and proactive maintenance in aging infrastructure programs. PAUT’s precision in detecting subsurface cracks makes it a preferred choice for fatigue?prone structures, pressure vessels, and rotating equipment where failure prevention is imperative. The demonstration of advanced phased array products with fully focused imaging, plane wave imaging, and phase coherent imaging at the Far East NDT Conference underscores industry confidence in phased array ultrasonic testing’s advanced anomaly characterization capabilities. These event?level validations enhance PAUT adoption for crack detection across industrial sectors and reinforce its growth trajectory as inspection precision and reliability needs intensify.

End-Use Insights

The oil & gas sector is expected to maintain the largest end?use revenue share 34% in 2026 due to extensive pipelines, refineries, and offshore facilities requiring frequent non?destructive inspections. PAUT systems are widely applied for internal defect detection and integrity verification without disrupting operations. The U.S. Naval Sea Systems Command (NAVSEA) Portsmouth Naval Shipyard awarded a federal contract to Evident Scientific, Inc. for phased array ultrasonic testing machines to support inspection programs. This confirmed award underscores the strategic importance and validated demand for phased array ultrasonic testing hardware in critical asset inspection for capital-intensive industries. The contract also highlights ongoing investment in advanced phased array equipment to ensure reliability, precision, and compliance with stringent safety standards across high-risk infrastructures.

The power & energy sector is projected to be the fastest?growing end?use segment, with an estimated 8.8% CAGR between 2026 and 2033, driven by increasing inspection requirements for aging thermal, nuclear, and renewable energy assets. PAUT’s high-resolution imaging supports precise inspections of turbines, boilers, pressure vessels, and other complex components to ensure safety and reliability. As energy infrastructure expands and modernizes, PAUT adoption is expected to accelerate, with both hardware and expertise playing a critical role in maintaining asset integrity. Regulatory emphasis on periodic inspection cycles and technological upgrades in inspection equipment further reinforce the sector’s rapid adoption of advanced phased array ultrasonic testing solutions.

Regional Insights

North America Phased Array Ultrasonic Testing (PAUT) Market Trends

North America is expected to account for approximately 36% of the phased array ultrasonic testing market share in 2026, supported by mature industrial sectors and strong regulatory frameworks that enforce rigorous inspection protocols. According to recent regional activity data, the region executed over 50,000 PAUT inspections in 2025 across energy, aerospace, automotive, and infrastructure sectors, illustrating broad application integration. Canada and the U.S. lead in pipeline integrity, refinery, and critical infrastructure inspections. The advanced NDT ecosystem accelerates digital analytics adoption and automated inspection solutions, improving operational efficiency. Regulatory enforcement, quality assurance programs, and recurring maintenance cycles sustain North America’s dominant market position.

The growth is driven by investments in advanced inspection technology and workforce development programs that enhance deployment capabilities. Centralized reporting and digital workflow management platforms enable consolidated PAUT data analysis across enterprise asset management systems. The U.S. leads adoption due to extensive oil & gas networks, aerospace quality assurance mandates, and energy infrastructure inspections. Multi-sector collaboration and industry accreditation programs strengthen the region’s position as a global PAUT leader. Modernization initiatives and infrastructure upgrades further increase recurring demand for manual and automated phased array ultrasonic testing solutions.

Europe Phased Array Ultrasonic Testing (PAUT) Market Trends

Europe holds a significant share of the global PAUT market, with recent regional analyses indicating a strong presence across Germany, the U.K., France, and Spain due to harmonized safety standards and proactive industrial integrity programs. European industries such as petrochemical, transportation, energy, and aerospace continue to adopt phased array ultrasonic testing to comply with safety directives and ensure long?term asset reliability. Regulatory convergence across the European Union (EU) reduces compliance barriers and encourages broader adoption of advanced inspection techniques. Germany’s manufacturing and industrial inspection budgets, the U.K.’s energy infrastructure maintenance programs, and France’s aerospace quality assurance initiatives collectively sustain regional demand for phased array ultrasonic testing equipment and services.

The investments in renewable energy infrastructure, such as wind turbine farms and nuclear power plants, which require periodic, high?accuracy structural evaluations, supports the regional growth. Service networks across major European countries are expanding to support both manual and automated phased array workflows, enabling comprehensive coverage of inspection needs. Continued emphasis on digital data integration and predictive maintenance reinforces the role of phased array ultrasonic testing technology in Europe’s quality assurance frameworks. Ongoing modernization of industrial assets and compliance with emerging inspection mandates contribute to steady expansion of the phased array ultrasonic testing market across the region.

Asia Pacific Phased Array Ultrasonic Testing (PAUT) Market Trends

Asia Pacific is the fastest?growing regional PAUT market, with an approximate 2026-2033 CAGR of 9.3%, driven by rapid industrialization, large infrastructure investments, and expanding manufacturing bases in China, India, Japan, and ASEAN states. The enormous demand for precision inspection solutions in the region continues to increase as asset owners prioritize proactive quality assurance and compliance with evolving safety standards. Government programs promoting industrial modernization, smart manufacturing, and energy corridor development are creating supportive environments for advanced non?destructive testing technologies such as phased array ultrasonic testing. Regulatory alignment with international inspection standards further encourages adoption, particularly in sectors where asset integrity is mission?critical.

Industry collaboration and technology dissemination efforts are contributing to regional momentum. The 5th Singapore International Non?Destructive Testing Conference & Exhibition was successfully held in Singapore, organized by the Non?Destructive Testing Society Singapore (NDTSS). The event featured technical sessions on advanced NDT technologies, including phased array ultrasonic testing, and brought together international delegates to discuss research, practical applications, and emerging inspection techniques. Such initiatives highlight regional innovation, knowledge sharing, and the growing emphasis on advanced PAUT capabilities across Asia Pacific. These confirmed developments reinforce the region’s trajectory as the most dynamic phased array ultrasonic testing market.

Competitive Landscape

The global phased array ultrasonic testing market structure is moderately consolidated, with leading players such as Olympus Corporation, GE Inspection Technologies, Eddyfi/NDT, Sonatest, and Mistras Group controlling a significant share. These companies leverage strong industrial relationships and integrated hardware-software platforms. Heavy R&D investments in AI-enabled defect detection, automated scanning, and advanced imaging maintain their technological leadership. They serve key sectors including oil & gas, aerospace, and power generation. The focus on innovation ensures continued differentiation in complex inspection applications.

Regional and niche players, including Nantong UNION Digital Technology, Proceq, and Krautkramer, target specialized applications and localized markets. High equipment costs, technician training requirements, and regulatory compliance remain barriers for new entrants. Digitalized inspection platforms and cloud-based data analytics allow smaller firms to participate via integration partnerships. Market consolidation is expected as leaders acquire regional specialists. Software and analytics collaborations further enhance the PAUT service ecosystem.

Key Industry Developments

- In July 2025, Wabtec Corporation acquired Evident’s Inspection Technologies division, formerly part of Olympus NDT, in a deal valued at approximately US$ 1.78 billion. The acquisition expands Wabtec’s Digital Intelligence portfolio, integrating advanced PAUT and non?destructive testing solutions and strengthening Wabtec’s capabilities in data acquisition, analytics, and automated inspection workflows.

- In June 2025, Eddyfi Technologies launched the Cypher® portable ultrasonic inspection platform, optimized for PAUT and advanced imaging applications. The system improves inspection speed, clarity, and repeatability for complex geometries in sectors such as energy, petrochemicals, and industrial manufacturing.

- In April 2025, Evident introduced the OmniScan X4, a portable phased array flaw detector integrating PAUT, TFM, PCI, and PWI technologies. The device provides fast, precise, and versatile defect detection in demanding field environments. Enhanced processing power and data storage enable longer and more complex inspections.

Companies Covered in Phased Array Ultrasonic Testing (PAUT) Market

- Olympus Corporation

- GE Inspection Technologies

- Zetec Inc.

- Sonatest Ltd.

- Eddyfi Technologies

- Waygate Technologies

- MISTRAS Group

- Siemens AG

- TechnoLogix

- NDT Global

- Fujifilm

- SGS SA

- Acuren

- Applied Technical Services

- Insight NDT

Frequently Asked Questions

The global phased array ultrasonic testing (PAUT) market is projected to reach US$ 1.4 billion in 2026.

Tightening industrial inspection mandates, aging infrastructure, preventive maintenance programs, and increasing adoption of automated and AI-enabled ultrasonic testing across oil & gas, power, aerospace, and construction sectors are driving the market.

The market is poised to witness a CAGR of 8% between 2026 and 2033.

Lucrative opportunities are emerging in in automated high-throughput PAUT systems, service and rental models, and expansion in developing markets with growing energy, manufacturing, and infrastructure projects.

Evident, Eddyfi Technologies, GE Inspection Technologies, Sonatest, and Olympus Corporation are some of the key players in the market.