- Metals & Minerals

- Super Alloys Market

Super Alloys Market Size, Share, and Growth Forecast 2026 - 2033

Super Alloys Market by Product Type (Nickel-Based Superalloys, Cobalt-Based Superalloys, Miscellaneous), Application (Turbine Engines, Aircraft Structural Parts, Drilling Tools, Biomedical Devices), Industries (Aerospace, Automotive, Power Generation, Oil & Gas, Medical, Miscellaneous), and Regional Analysis, 2026 - 2033

Super Alloys Market Size and Trend Analysis

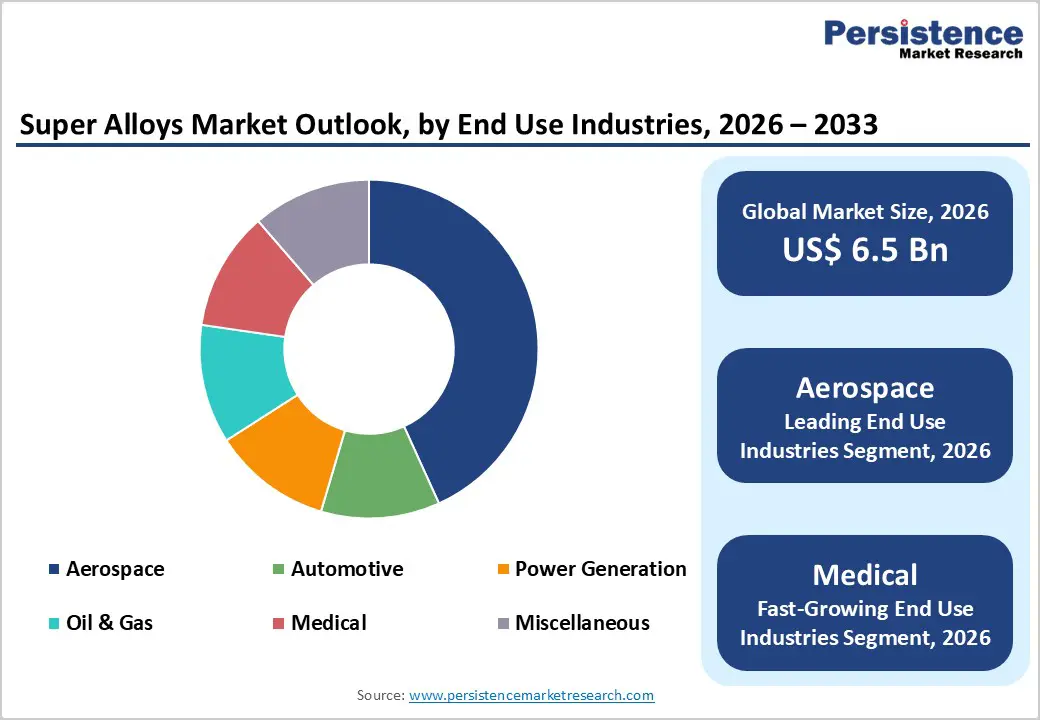

The global super alloys market size is expected to be valued at US$ 6.5 billion in 2026 and projected to reach US$ 11.4 billion by 2033, growing at a CAGR of 8.3% between 2026 and 2033. This robust expansion is primarily driven by the escalating demand from the aerospace industry for high-temperature resistant materials capable of maintaining structural integrity in turbine engines operating above 800°C, coupled with the power generation sector's increasing adoption of advanced gas turbines requiring exceptional creep resistance and oxidation stability.

The market's growth trajectory is further reinforced by technological breakthroughs in additive manufacturing processes that enable the production of complex superalloy components with superior performance characteristics, alongside the automotive industry's growing utilization of these materials in turbocharger applications to meet stringent emission standards and fuel efficiency requirements.

Key Industry Highlights

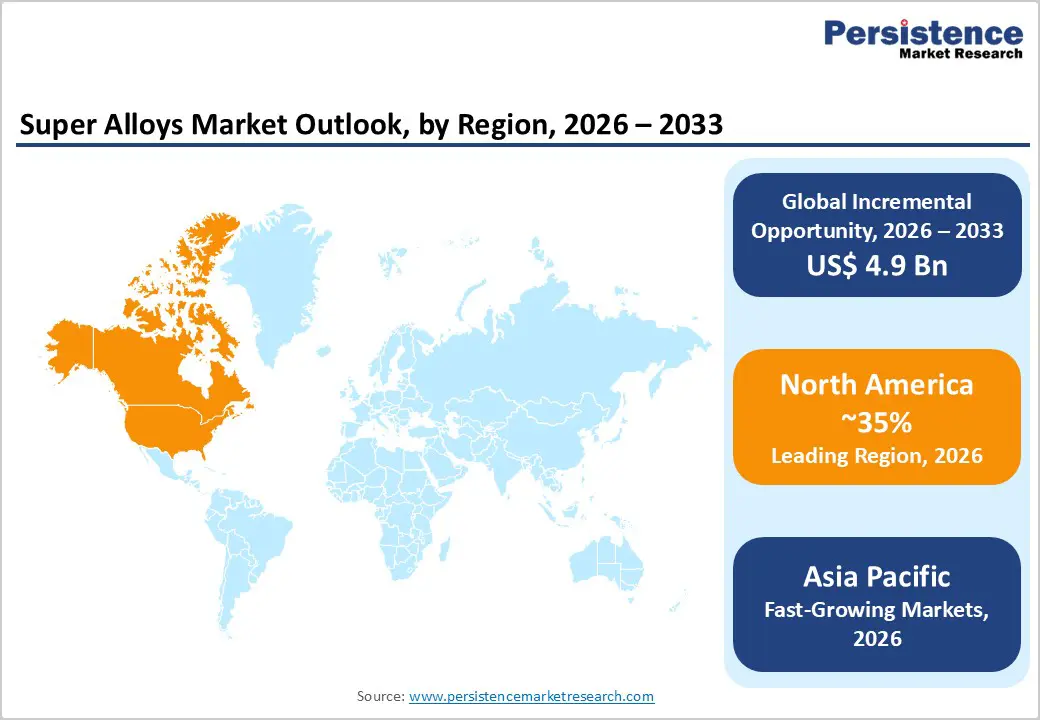

- Leading Region: North America dominates the global super alloys market with approximately 35% market share in 2025, driven by the United States' position as the world's premier aerospace manufacturer, substantial defense spending on advanced aviation technologies, and presence of major superalloy producers including Precision Castparts Corporation, ATI, and Haynes International supporting domestic manufacturing capabilities.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing regional market throughout the forecast period, propelled by rapid industrialization in China, Japan, and India, expanding aerospace manufacturing capabilities, automotive industry adoption of turbocharger superalloys, and substantial government investments in power generation infrastructure requiring advanced gas turbine materials.

- Dominant Product: Nickel-based superalloys represent the leading product type segment with approximately 67% market share in 2025, attributed to their exceptional high-temperature strength, superior creep resistance, and oxidation stability making them indispensable for aerospace turbine blades, industrial gas turbine components, and automotive turbocharger applications operating above 1,000°C.

- Fastest Growing Product: Cobalt-based superalloys emerge as the fastest-growing product type with projected CAGR of 8.9% from 2026 to 2033, driven by expanding biomedical device applications serving the aging global population, including orthopedic implants, cardiovascular stents, and surgical instruments requiring exceptional biocompatibility, fatigue resistance, and corrosion immunity in physiological environments.

- Key Opportunity: The convergence of super alloys technology with advanced additive manufacturing represents a transformative growth opportunity, with recent commercialization of optimized superalloy powders for Laser Beam Powder Bed Fusion systems enabling complex component geometries, material waste reduction of 40% to 60%, and democratizing access to customized solutions across aerospace, automotive, and biomedical applications.

| Key Insights | Details |

|---|---|

| Super Alloys Market Size (2026E) | US$ 6.5 billion |

| Market Value Forecast (2033F) | US$ 11.4 billion |

| Projected Growth CAGR (2026 - 2033) | 8.3% |

| Historical Market Growth (2020 - 2025) | 6.4% |

Market Dynamics

Drivers - Surging Aerospace Demand for Next-Generation Turbine Materials

The aerospace industry's relentless pursuit of fuel-efficient aircraft engines is fundamentally transforming the super alloys market landscape. Single-crystal nickel-based superalloys now constitute the primary material choice for turbine blades in modern jet engines, enabling operational temperatures approaching 1,200°C while maintaining creep resistance and mechanical integrity. According to NASA's advanced materials research, contemporary superalloy compositions incorporating titanium, aluminum, and refractory elements such as tungsten and molybdenum deliver temperature capabilities representing 90% of their melting point, a critical advancement that directly translates to improved engine efficiency and reduced carbon dioxide emissions. The global commercial aviation sector's projected fleet expansion, coupled with defense modernization programs across North America, Europe, and Asia Pacific, is generating unprecedented demand for these high-performance materials in both civilian and military aircraft applications.

Accelerating Power Generation Infrastructure Development

The global energy transition is catalyzing substantial investments in advanced power generation technologies that fundamentally depend on superalloy materials for operational efficiency and reliability. Industrial gas turbines utilized in electricity generation now account for approximately 20% of super alloys consumption, with nickel-based compositions dominating applications in turbine blades, vanes, and combustion chambers where temperatures routinely exceed 700°C. Research from the U.S. Department of Energy's Oak Ridge National Laboratory demonstrates that modern superalloy-equipped gas turbines achieve efficiency improvements of 5% to 8% compared to conventional materials, directly supporting grid operators' objectives for reduced fuel consumption and lower emissions. The integration of these materials in supercritical boilers, nuclear reactor systems, and renewable energy infrastructure, particularly in concentrated solar power plants, underscores their expanding role beyond traditional aerospace applications. Government initiatives promoting clean energy across developing economies in Asia Pacific and infrastructure modernization programs in established markets are sustaining robust demand trajectories throughout the forecast period.

Restraints - Elevated Raw Material and Processing Costs

The super alloys market confronts significant cost pressures stemming from the intensive requirements for rare alloying elements and sophisticated manufacturing processes. Nickel-based superalloys typically incorporate expensive constituents including cobalt, chromium, and refractory metals, with raw material costs representing 30% to 50% of total production expenses according to industry analyses. The complexity of processing techniques, particularly for single-crystal directional solidification and powder metallurgy applications achieving grain sizes of ASTM 12, necessitates specialized equipment and energy-intensive operations that substantially elevate manufacturing costs. Geopolitical factors affecting the supply of critical elements like cobalt, primarily sourced from regions with limited diversification, introduce additional volatility into pricing structures that constrain market accessibility for cost-sensitive applications beyond aerospace and power generation sectors.

Extended Development Cycles and Stringent Certification Requirements

Introducing new superalloy compositions to commercial markets involves extraordinarily lengthy qualification processes that impede rapid innovation and market responsiveness. The aerospace industry's rigorous safety and certification standards mandate comprehensive testing protocols that can extend development timelines beyond 10 years from initial alloy concept to full production qualification, as documented in materials science research from leading institutions. These extensive validation requirements encompass mechanical property characterization across temperature ranges, long-term creep and fatigue testing, oxidation resistance evaluation, and compatibility assessments with manufacturing processes. The substantial capital investment required for testing infrastructure, combined with the extended period before revenue realization, creates barriers to entry for smaller manufacturers and potentially delays the commercialization of breakthrough alloy technologies that could offer superior performance characteristics.

Opportunity - Additive Manufacturing Revolution in Complex Component Production

The convergence of super alloys technology with advanced additive manufacturing represents a transformative opportunity reshaping component design and production paradigms. Industry leaders including EOS have recently commercialized nickel-based superalloy powders such as IN738 and K500 specifically optimized for Laser Beam Powder Bed Fusion systems, enabling the fabrication of geometrically complex turbine components with internal cooling channels that would be impossible to produce through conventional casting methods.

Research institutions report that additive manufacturing of superalloys reduces material waste by approximately 40% to 60% compared to traditional subtractive machining approaches, while simultaneously accelerating prototyping cycles and enabling on-demand production of spare components. The NASA Glenn Research Center's development of advanced powder metallurgy compositions that inhibit deleterious phase transformations during high-temperature creep demonstrates the technology's potential for next-generation aerospace applications. As manufacturing systems mature and powder production scales increase, additive manufacturing is positioned to democratize access to customized superalloy solutions across industries including automotive turbocharger production, biomedical implant manufacturing, and industrial machinery components.

Expanding Biomedical Device Applications for Aging Global Population

The medical devices sector presents compelling growth opportunities as cobalt-chromium superalloys gain traction in orthopedic implants, cardiovascular stents, and surgical instruments serving the world's aging demographic. These biocompatible alloys, including industry-standard compositions like MP35N, L-605, and Elgiloy, combine exceptional fatigue resistance with corrosion immunity in physiological environments, making them ideally suited for permanent implant applications. Clinical research documents that cobalt-chromium superalloys in hip and knee replacement systems deliver service lifespans exceeding 20 years, addressing the orthopedic biomaterials segment's projected compound annual growth rate driven by rising osteoarthritis and osteoporosis prevalence among elderly populations globally. The Asia Pacific region's expanding healthcare infrastructure, coupled with improving insurance coverage and increasing awareness of advanced medical treatments, positions this geographic market for accelerated adoption of superalloy-based medical devices. Recent innovations in metal injection molding and surface modification techniques are further enhancing the biocompatibility and manufacturing economics of these materials, potentially expanding their utilization into dental applications, spinal fixation systems, and minimally invasive surgical tools.

Category-wise Analysis

Product Type Insights

Nickel-based superalloys remain the most dominant product segment, accounting for nearly two-thirds of the global market in 2025 due to their superior high-temperature strength, creep resistance, and oxidation stability. Their face-centered cubic structure with gamma-prime precipitates enables sustained performance at temperatures exceeding 1,000°C, making them essential for aerospace turbine blades and industrial gas turbines. Alloys such as Inconel 718 and Waspaloy are widely adopted in both commercial and military engines. Continuous advancements in alloy chemistry and processing technologies have further enhanced turbine disc and blade temperature thresholds, reinforcing the segment’s structural importance in high-performance engineering applications.

Application Insights

Turbine engines represent the leading application segment, contributing nearly half of total superalloy demand in 2025 due to their indispensable role in aerospace propulsion and power generation. Superalloys are extensively used in turbine blades, vanes, discs, and combustion chambers that operate under extreme thermal and mechanical stress. Modern aircraft engines incorporate a substantial volume of high-value superalloy components, significantly influencing overall engine manufacturing costs. Advanced directionally solidified and single-crystal blade technologies have extended service life and improved fuel efficiency, providing strong economic justification for adoption and ensuring sustained demand amid global fleet expansion and energy infrastructure development.

Industry Insights

The aerospace sector holds the largest share of 39% of the superalloys market in 2025, driven by its absolute reliance on high-performance materials for aircraft engines and critical structural components. Superalloys are fundamental to ensuring reliability under high-temperature, high-stress flight conditions. Growing global air passenger traffic and fleet expansion programs continue to stimulate demand for new aircraft and replacement engines. Defense modernization initiatives further reinforce consumption through advanced fighter jet and propulsion system development. Stringent aerospace certification standards and long qualification cycles favor established manufacturers, while ongoing innovations in additive manufacturing-grade alloys continue to strengthen this sector’s leadership position.

Regional Insights

North America Super Alloys Market Trends and Insights

North America commands the largest regional market share at approximately 35% in 2025, anchored by the United States' position as the world's leading aerospace manufacturer and home to major superalloy producers including Precision Castparts Corporation, Allegheny Technologies Incorporated, Haynes International, and Carpenter Technology Corporation. The region's dominance is further reinforced by substantial defense expenditures, with military aviation programs requiring advanced superalloy materials for next-generation fighter aircraft, hypersonic vehicle development, and space exploration initiatives supported by NASA's ongoing materials research. According to industry reports, over 68% of aerospace engine components manufactured in the United States utilize nickel-based alloy compositions, reflecting the material's critical importance to national aerospace capabilities.

The region benefits from a comprehensive innovation ecosystem encompassing leading research institutions, advanced manufacturing facilities, and robust supply chain infrastructure supporting rapid technology commercialization. Allegheny Technologies' recent capacity expansion, projected to increase aerospace-grade titanium bar production by 35% above baseline levels by 2025, exemplifies ongoing investments strengthening North American manufacturing competitiveness. The automotive sector's adoption of superalloys in high-performance turbocharger applications, with approximately 38% of manufacturers incorporating these materials in exhaust systems and turbo components according to market analyses, diversifies regional demand beyond traditional aerospace applications. Regulatory frameworks established by the U.S. Food and Drug Administration for medical device applications further position North America as a key market for biomedical-grade superalloy products serving orthopedic implant and cardiovascular device manufacturers.

Europe Super Alloys Market Trends and Insights

Europe represents approximately 24% of global demand, distinguished by advanced aerospace manufacturing capabilities concentrated in Germany, United Kingdom, France, and Spain, where 63% of engine components integrate nickel-based superalloy materials according to regional industry statistics. Major European aerospace programs including Airbus commercial aircraft production and Rolls-Royce engine manufacturing sustain consistent superalloy consumption, with recent announcements of joint ventures between Rolls-Royce and Safran for next-generation low-emission aircraft engines incorporating advanced superalloy materials signaling continued regional innovation. The region's strict environmental regulations and efficiency mandates drive industrial gas turbine applications, with 41% of new installations utilizing nickel alloys to meet stringent emission requirements and operational efficiency targets.

Germany and France collectively account for 48% of European superalloy demand, supported by robust automotive industries where high-performance vehicle manufacturers incorporate these materials in 33% of turbocharger and exhaust components. The successful integration of Haynes International into Acerinox's High-Performance Alloys Division alongside VDM Metals in recent consolidation demonstrates European companies' strategic positioning in global superalloy markets. Regional initiatives promoting sustainable manufacturing, exemplified by Aperam Recycling's collaboration with IperionX Limited to develop 100% closed-loop titanium supply chains using patented low-carbon processing technologies, reflect Europe's commitment to environmentally responsible superalloy production. Chemical processing facilities across Europe utilize nickel alloys in 52% of acid-resistant reactors according to market research, highlighting diversified industrial applications beyond aerospace that stabilize regional demand patterns.

Asia Pacific Super Alloys Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market, propelled by rapid industrialization, expanding aerospace manufacturing capabilities, and substantial government investments in defense modernization across China, Japan, India, and ASEAN nations. The region's automotive industry, representing the world's largest production volume, increasingly adopts superalloy materials in turbocharger applications to comply with stringent emission standards, with 31% of turbocharger components now utilizing nickel alloys for enhanced heat resistance according to industry analyses. China's ambitious aerospace development programs, including domestic commercial aircraft manufacturing and military aviation modernization, generate substantial demand for domestically produced and imported superalloy materials, supported by companies such as Shanghai HY Industry Co., Ltd. and Fushun Special Steel Co., Ltd. expanding production capacities.

Japan's established materials science expertise, embodied by manufacturers including Nippon Yakin Kogyo Co., Ltd., Hitachi Metals, and IHI Corporation, positions the nation as a critical regional supplier of advanced superalloy compositions and manufacturing technologies. India's government-supported aerospace initiatives, including Mishra Dhatu Nigam Limited's role as a strategic materials supplier to defense programs, demonstrate emerging economy participation in high-value superalloy markets. The region's power generation infrastructure expansion, driven by economic growth and electrification objectives requiring efficient gas turbine installations, creates substantial opportunities for superalloy applications in energy sector components. According to market research, Asia Pacific healthcare infrastructure development, coupled with rising medical device adoption rates and improving insurance coverage, positions the region for accelerated growth in biomedical superalloy applications serving orthopedic implant manufacturers and cardiovascular device producers throughout the forecast period.

Competitive Landscape

The global super alloys market exhibits moderate consolidation with a competitive landscape characterized by established multinational corporations possessing advanced manufacturing capabilities, extensive intellectual property portfolios, and longstanding relationships with aerospace and power generation original equipment manufacturers. Market leaders including Precision Castparts Corporation, Allegheny Technologies Incorporated, Haynes International, and Carpenter Technology Corporation command significant market share through continuous research and development investments targeting next-generation alloy compositions with enhanced high-temperature performance, improved creep resistance, and superior oxidation stability.

Industry consolidation trends are evidenced by Acerinox's strategic acquisition of Haynes International and integration with VDM Metals to form a comprehensive High-Performance Alloys Division, reflecting broader market dynamics favoring scale and technological capabilities. Companies differentiate through specialized manufacturing processes including single-crystal directional solidification, powder metallurgy techniques, and additive manufacturing expertise, with market participants increasingly forming strategic partnerships with aerospace firms for customized superalloy applications in advanced propulsion systems.

Key Developments:

- July, 2024: Aubert & Duval in collaboration with Alloyed launched ABD-1000 AM, a state-of-the-art superalloy developed using the Alloys-by-Design platform for additive manufacturing applications, exhibiting outstanding environmental resistance and high-temperature performance exceeding 1,000°C while maintaining stress rupture capabilities comparable to Ni247LC cast alloy, targeting aerospace, power generation, and defense sectors.

- November, 2024: EOS expanded its additive manufacturing material portfolio by introducing nickel-based EOS IN738 and EOS K500 superalloy powders specifically optimized for Laser Beam Powder Bed Fusion systems, with commercial availability commencing for EOS M 290 machine families in December 2024 and EOS M 400-4 systems in early 2025, enabling advanced aerospace component manufacturing.

- August, 2025: International Advanced Research Centre for Powder Metallurgy and New Materials (ARCI) unveiled a new laser-assisted turning technology to machine tough super-alloys like Inconel 625, significantly improving precision and efficiency for aerospace, power and nuclear applications.

- September, 2025: Aerolloy Technologies unveiled a state-of-the-art vacuum induction melting facility for superalloys and large investment castings, boosting its position in the global superalloy market and strengthening India’s aerospace and defence materials manufacturing capabilities.

Companies Covered in Super Alloys Market

- Aperam S.A.

- AMG Superalloys

- Special Metal Corporation

- Haynes International

- Nippon Yakin Kogyo Co., Ltd.

- Special Metals Corporation

- Universal Stainless

- Superalloy International Co. Ltd.

- VDM Metals

- Precision Castparts Corporation

- Allegheny Technologies Incorporated (ATI)

- Carpenter Technology Corporation

- Doncasters Group

- Hitachi Metals

- IHI Corporation

- Eramet Group

- Arconic Corporation

- Aubert & Duval

- Mishra Dhatu Nigam Limited

- ThyssenKrupp AG

Frequently Asked Questions

The global super alloys market is projected to reach US$ 6.5 billion in 2026, driven by strong demand from aerospace, power generation, and automotive sectors.

The market is driven by rising aerospace turbine requirements, expanding gas-based power generation capacity, and advancements in additive manufacturing technologies.

North America leads the market with around 35% share in 2025, supported by strong aerospace manufacturing and defense investments in the United States.

The integration of super alloys with advanced additive manufacturing offers major growth potential through complex part production and significant material waste reduction.

Key players include Precision Castparts Corporation, Allegheny Technologies Incorporated, Haynes International, Carpenter Technology Corporation, Aperam S.A., VDM Metals, Special Metals Corporation, Nippon Yakin Kogyo Co., Ltd., AMG Superalloys, and Doncasters Group.