- Advanced Materials

- Superhard Material Market

Superhard Material Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Superhard Material Market by By Type (Extrinsic, and Intrinsic), Cover (Polycrystalline Diamond (PCD), Polycrystalline Cubic Boron Nitride (PCBN), Cubic Boron Nitride (CBN), Micron Diamond), Form (Polycrystalline, Composite, Monocrystalline), Application (Cutting Tools, Diamond Drill Bits, Shipbuilding, Saw Blades, Diamond Disc, and Others), End-user and Regional Analysis for 2025 - 2032

Superhard Material Market Size and Trends Analysis

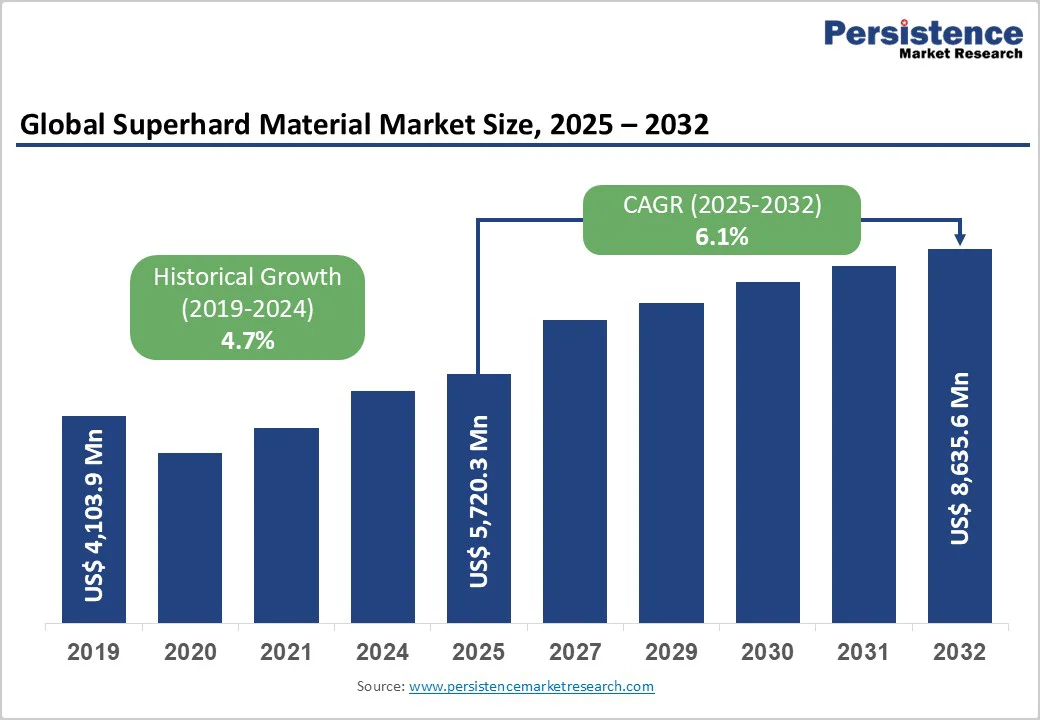

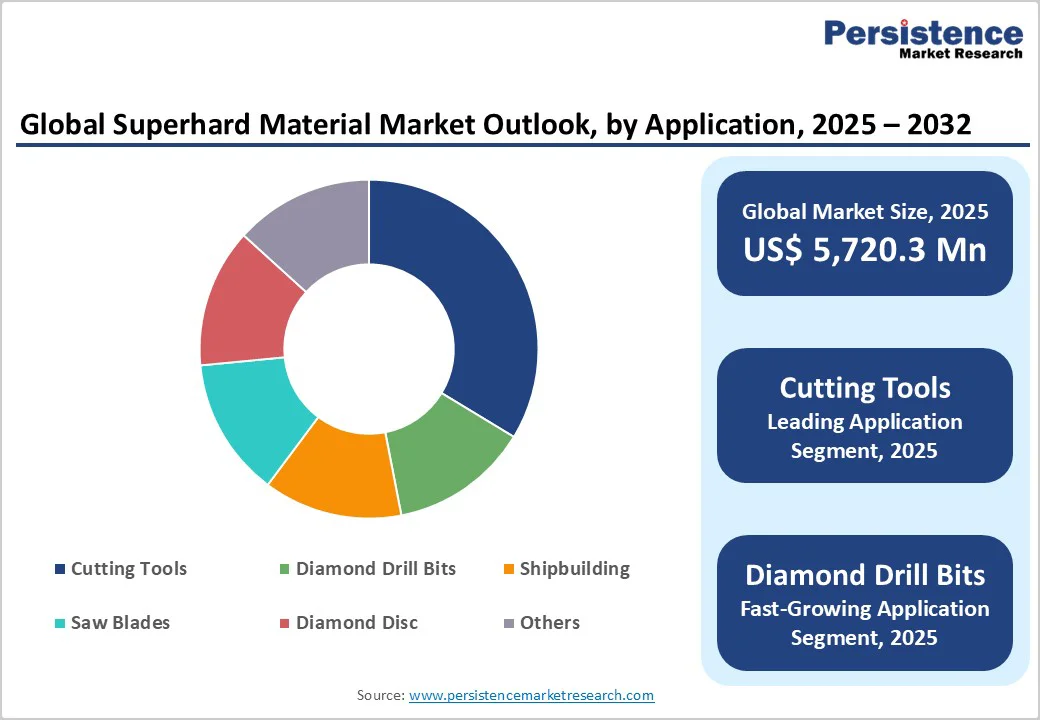

The global superhard material market is valued at US$ 5,720.3 million in 2025, and is expected to reach US$ 8,635.5 million, growing at a CAGR of 6.1% between 2025 and 2032. This trajectory reflects growing demand from automotive, aerospace, construction, and manufacturing sectors, where precision cutting, grinding, and drilling operations require materials with exceptional hardness exceeding 40 gigapascals.

Superhard materials are characterized by hardness levels exceeding 40 GPa, making them exceptionally resistant to deformation and wear. Diamond, with a hardness of approximately 90 GPa, ranks as the hardest known material, followed by cubic boron nitride (cBN), which exhibits a hardness of around 50 GPa.

Key Industry Highlights:

- Automotive and aerospace industries are the primary growth drivers, together accounting for over 35% of global demand for superhard materials due to rising use in lightweight and precision component manufacturing.

- PCD and CBN cutting tools enable high-precision machining of aluminum alloys, titanium, and composites, essential for electric vehicles and next-generation aircraft production.

- CBN tools deliver up to 5 times longer tool life than traditional carbide tools when processing hardened steels and cast iron, enhancing manufacturing efficiency and cost-effectiveness.

- High production costs and complex HPHT synthesis processes (exceeding 5 GPa and 1,500°C) remain key barriers to broader market adoption.

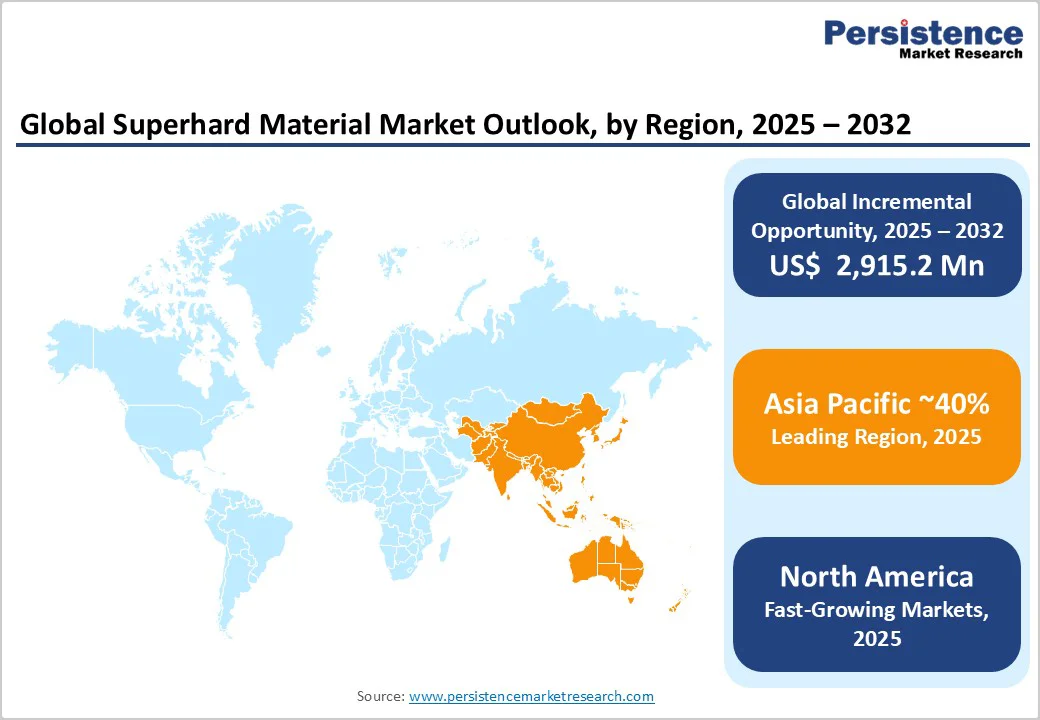

- Asia Pacific dominates with over 40% global market share, led by China’s large-scale synthetic diamond production and robust industrial base.

- North America emerges as the fastest-growing market, supported by aerospace recovery, reshoring initiatives, and adoption of eco-efficient precision tools.

- Extrinsic materials (like PCD and PcBN) lead with over 60% share, driven by engineered composites offering high hardness, toughness, and wear resistance.

- PCBN is the fastest-growing product type, with a strong CAGR driven by demand from hardened metal machining in automotive and aerospace manufacturing.

- Electronics and semiconductor applications are expanding, as CBN’s ultra-wide bandgap and thermal stability support high-performance electronic components.

- Sustainability and digitalization are shaping competitive strategies, with leading manufacturers adopting eco-friendly synthesis, recycling programs, and predictive maintenance through Industry 4.0 integration.

| Key Insights | Details |

|---|---|

|

Superhard Material Market Size (2025E) |

US$ 1,278.5 Mn |

|

Market Value Forecast (2032F) |

US$ 2,405.3 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

9.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

8.1% |

Market Dynamics

Drivers - Expanding Automotive and Aerospace Manufacturing Demands

The automotive and aerospace industries represent critical growth engines for the superhard materials market, with automotive applications alone commanding over 35% of end-user market share. The global automotive sector's transition toward electric vehicles and lightweight component manufacturing has intensified demand for polycrystalline diamond (PCD) and cubic boron nitride (CBN) cutting tools capable of precision machining aluminum alloys, titanium, and composite materials.

According to industry data, the aerospace cutting tools market is expanding at 8.4% CAGR, driven by next-generation aircraft production requiring superhard tools for machining advanced alloys and carbon fiber composites. The automotive industry's focus on fuel efficiency and emission reduction has accelerated adoption of superhard materials for processing hardened steels and cast iron components, where CBN tools demonstrate 3-5 times longer tool life compared to traditional carbide alternatives. Manufacturing automation and Industry 4.0 integration further propel demand, as precision engineering requirements necessitate tools delivering tighter tolerances and superior surface finishes

Technological Advancements in Mining and Drilling Operations

Superhard material technology is transforming modern manufacturing through precise force control, reduced energy use, and adaptive capabilities aligned with Industry 4.0. Supported by initiatives such as the U.S. Department of Energy’s Advanced Manufacturing Office and Japan’s “Connected Industries,” servomotor-driven equipment adoption is accelerating globally. Research from ISO and IEC underscores their advantages in accuracy, speed, and shorter cycle times, fostering widespread adoption across industries.

The rise in local and foreign direct investments in manufacturing particularly in automotive and electronics sectors across Asia Pacific and North America are fueling large-scale plant expansions. Reports by UNCTAD and Invest India highlight multi-billion-dollar inflows into precision stamping and sheet-forming facilities, positioning superhard materials as key productivity enablers for high-volume, high-quality production environments.

Restraint- High Production Costs and Material Limitations Continue to Challenge the Growth of the Superhard Materials Industry

The superhard materials industry faces notable challenges that hinder wider adoption and cost efficiency. Production of synthetic diamond and cubic boron nitride (CBN) involves high-pressure, high-temperature (HPHT) processes exceeding 5 GPa and 1,500°C, demanding advanced equipment and resulting in high capital and operational costs. Price volatility of raw materials such as cobalt binders for PCD and catalytic metals for diamond synthesis further creates pricing instability, limiting competitiveness in cost-sensitive applications. Additionally, strict environmental regulations governing emissions and hazardous waste management increase compliance costs, pushing manufacturers to adopt sustainable production technologies.

Beyond cost factors, material limitations restrict application scope. Diamonds lose thermal stability above 800°C and react chemically with ferrous materials, necessitating the use of CBN for steel and iron machining. Their inherent brittleness makes them prone to chipping in high-impact operations, reducing suitability for interrupted cutting tasks. Moreover, limited technical expertise and supply chain constraints in developing regions further impede market expansion. Together, these factors emphasize the industry’s need for innovation in synthesis methods, durability enhancement, and sustainable manufacturing practices.

Market Opportunities - Emerging Applications in Electronics and Semiconductor Manufacturing

The electronics and semiconductor industries present substantial growth opportunities, with cubic boron nitride's ultra-wide bandgap properties enabling applications in high-power electronics and ultraviolet optoelectronics. CBN's superior thermal conductivity and electrical insulation characteristics make it increasingly valuable for semiconductor fabrication, thermal management substrates, and precision machining of silicon wafers. The global electronics market's 6% CAGR supports expanding CBN utilization in device manufacturing requiring exceptional thermal dissipation and chemical inertness.

Superhard material coatings for cutting tools used in processing printed circuit boards, ceramic components, and glass substrates for display technologies offer differentiation opportunities for manufacturers targeting high-precision electronics applications. The miniaturization trend in consumer electronics and telecommunications equipment demands ultra-precision machining capabilities achievable only through advanced superhard tooling, creating niche markets with premium pricing potential.

Superhard Material Market Insights and Trends

Product Type Insights

Extrinsic Materials Lead Market Share, While Intrinsic Segment Emerges as the Fastest-Growing Category

The extrinsic superhard materials segment dominates the global market, accounting for over 60% of total revenue, driven by strong demand for engineered composites whose exceptional hardness results from microstructural design rather than inherent composition. Materials such as polycrystalline diamond (PCD) and polycrystalline cubic boron nitride (PcBN) are produced through advanced sintering techniques that yield dense, uniform structures with precisely controlled grain sizes. These features optimize hardness, toughness, and wear resistance for critical industrial applications such as cutting, drilling, and grinding. Extrinsic materials also provide consistent quality, scalability, and cost advantages over natural superhard materials while maintaining comparable or superior performance in high-stress environments.

In contrast, the intrinsic superhard materials segment, though smaller in market share, is the fastest-growing category, propelled by breakthroughs in synthesis technologies and growing demand from specialized precision machining sectors. Intrinsic compounds such as single-crystal diamond and cubic boron nitride offer unmatched crystalline hardness and are vital for applications requiring mirror-smooth finishes and sub-micron dimensional accuracy. Ongoing research into advanced materials like boron carbide, carbon nitrides, and B–N–C ternary compounds is expanding this segment’s potential, aiming to surpass natural diamond in hardness while improving thermal stability and minimizing chemical reactivity with ferrous metals.

Cover Insights

Polycrystalline Diamond (PCD) Leads the Market, While PCBN Emerges as the Fastest-Growing Segment

The Polycrystalline Diamond (PCD) segment dominates the market with over 30% share, attributed to its exceptional wear resistance, hardness, and thermal conductivity, making it indispensable for machining non-ferrous metals, composites, and abrasive materials. Produced through high-pressure sintering of diamond particles with a tungsten carbide substrate, PCD tools achieve hardness levels approaching 7,500 Vickers, ensuring extended tool life and superior surface finish in demanding applications.

The automotive and aerospace industries are major end users, employing PCD tools for machining engine components, structural parts, and composite assemblies. Additionally, their use is expanding into woodworking applications, particularly in engineered lumber and laminated flooring production, reinforcing PCD’s market leadership.

Polycrystalline Cubic Boron Nitride (PCBN) represents the fastest-growing segment, driven by its ability to machine hardened ferrous metals where diamond tools are unsuitable. PCBN’s chemical stability and high thermal resistance enable efficient cutting of hardened steels, cast irons, and nickel-based superalloys at elevated speeds without compromising tool integrity. Rising demand from automotive and aerospace manufacturing, where durability and precision are critical, supports a robust 10.5% CAGR. Continuous innovation in CBN content formulations, balancing chemical wear and abrasion resistance further strengthens PCBN’s adoption for both continuous and interrupted machining operations across advanced manufacturing sectors.

Form Insights

Polycrystalline Dominance and Composite Innovation Driving Superhard Material Form Advancements

The polycrystalline form leads the market with over 45% share, owing to its versatility across cutting, grinding, and drilling applications. Its random crystal orientation eliminates the directional weaknesses typical of single-crystal structures, providing isotropic mechanical strength and uniform performance in all cutting directions. Polycrystalline diamond (PCD) and cubic boron nitride (CBN) compacts, when integrated with cemented carbide substrates, deliver an optimal combination of hardness, toughness, and thermal resistance—making them ideal for demanding machining environments in automotive, aerospace, and tooling industries.

Composite forms are the fastest-growing segment, driven by advancements in multi-material engineering and nano-additive technology. These composites feature graded compositions, refined binder systems, and functionally tailored microstructures that enhance impact resistance, thermal stability, and chemical durability. Ongoing innovations in diamond-metal composites and hybrid architectures are enabling next-generation tools optimized for emerging sectors such as additive manufacturing, advanced ceramics processing, and aerospace component machining, where precision, reliability, and durability are critical.

Regional Insights and Trends

Asia Pacific Strengthens Its Global Leadership in the Superhard Materials Market through Industrial Expansion and Technological Advancements

Asia Pacific holds over 40% of the global superhard materials market, establishing itself as the dominant production and consumption hub. The region’s leadership is anchored by China, the world’s largest synthetic diamond producer, with major players such as Zhongnan Diamond and Henan Huanghe Whirlwind operating large-scale facilities that supply both domestic and export markets. Regional growth is fueled by rapid urbanization, infrastructure expansion, and robust manufacturing activity in automotive, electronics, and construction sectors.

India is emerging as a high-growth market, supported by pro-manufacturing government policies and increasing foreign investment in industrial sectors. Meanwhile, Japan’s precision engineering expertise sustains strong demand for advanced cutting tools and abrasives, while Southeast Asian nations such as Thailand, Indonesia, and Vietnam continue to attract manufacturing investments, driving derivative demand for superhard tooling and industrial applications. Regional advantages, including cost-competitive production, expanding skilled labor pools, and proximity to key end-user industries, position Asia Pacific for continued market dominance through 2032.

North America Emerges as the Fastest-Growing Market Driven by Technological Innovation and Precision Manufacturing Demand

North America represents a mature yet rapidly advancing market, distinguished by technological innovation, stringent quality standards, and a strong presence of aerospace and advanced manufacturing industries. The United States leads regional demand, supported by established players such as Element Six, Hyperion Materials & Technologies, and specialized tool manufacturers serving the automotive, aerospace, oil and gas, and precision machining sectors. The region is witnessing the fastest growth among developed markets, fueled by reshoring initiatives, domestic oil and gas exploration, and the ongoing recovery of the aerospace industry.

A robust regulatory framework emphasizing worker safety and environmental compliance continues to drive the adoption of advanced, eco-efficient superhard tools that enhance productivity while minimizing waste. North American manufacturers are heavily investing in R&D to develop next-generation cutting geometries, high-performance coatings, and application-specific designs. With a sophisticated distribution network, strong technical support, and growing automation integration, the region is well-positioned for sustained growth in high-value industries such as aerospace, medical devices, and energy applications.

Competitive Landscape

The global superhard materials market is moderately concentrated, with established international players and several regional manufacturers competing across applications and geographies. Market leaders such as Element Six (Luxembourg), a De Beers Group subsidiary, maintain a strong position through extensive synthetic diamond and CBN portfolios catering to cutting, drilling, abrasive, and advanced technology applications. The company operates across the U.K., Ireland, Germany, South Africa, and the U.S., leveraging deep R&D capabilities and vertical integration from synthesis to finished tool production.

Industry leaders emphasize innovation-driven differentiation, investing in advanced manufacturing technologies, materials science, and customized solutions. Vertical integration ensures material quality, supply chain stability, and cost competitiveness, while geographic expansion through localized production and distribution strengthens responsiveness in emerging markets. Sustainability and digitalization are central to strategy, with manufacturers adopting eco-friendly synthesis, tool recycling, and Industry 4.0-enabled predictive maintenance to enhance efficiency and deliver lifecycle value beyond initial tool cost.

Key Industry Developments

- In 2024, Makita U.S.A., Inc. released a comprehensive diamond blade lineup spanning 4.5" to 14" diameters optimized for battery-powered tools, featuring an ultra-thin kerf design delivering 80% more cuts per charge and redesigned cutting surfaces providing faster cutting speeds and extended blade life.

- In 2024, Milwaukee Tool launched Diamond MAX Hole Saws, delivering up to 20X longer life in porcelain and tile applications through higher-grade diamond grit and superior retention technology.

Companies Covered in Superhard Material Market

- Sandvik Element Six

- Zhongnan Diamond

- JINQU Superhard

- Huanghe Whirlwind

- Zhengzhou Zhong Peng

- Yalong Superhard Materials

- Anhui HongJing

- SF-Diamond

- Other Market Players

Frequently Asked Questions

The Superhard Material market is estimated to be valued at US$ 1,278.5 Mn in 2025.

The key demand driver for the superhard materials market is the rising demand for high-precision machining and wear-resistant tooling across industrial sectors such as automotive, electronics, aerospace, and construction

In 2025, the Asia Pacific region will dominate the market with an exceeding 40% revenue share in the global superhard material market.

Among covers, Polycrystalline Diamond (PCD) holds the highest preference, capturing beyond 30% of the market revenue share in 2025, surpassing other covers.

Sandvik Element Six, Zhongnan Diamond, JINQU Superhard, Huanghe Whirlwind, and Zhengzhou Zhong Peng are a few leading players.