- Clothing, Footwear, & Accessories

- PVC Footwear Market

PVC Footwear Market Size, Share, and Growth Forecast 2026 - 2033

PVC Footwear Market by Product Type (PVC Sandals, PVC Slippers, PVC Boots, PVC Shoes, PVC Clogs), by Distribution Channel (Online, Offline), End-User (Men, Women, Children, Unisex), and Regional Analysis, 2026 - 2033

PVC Footwear Market Size and Trend Analysis

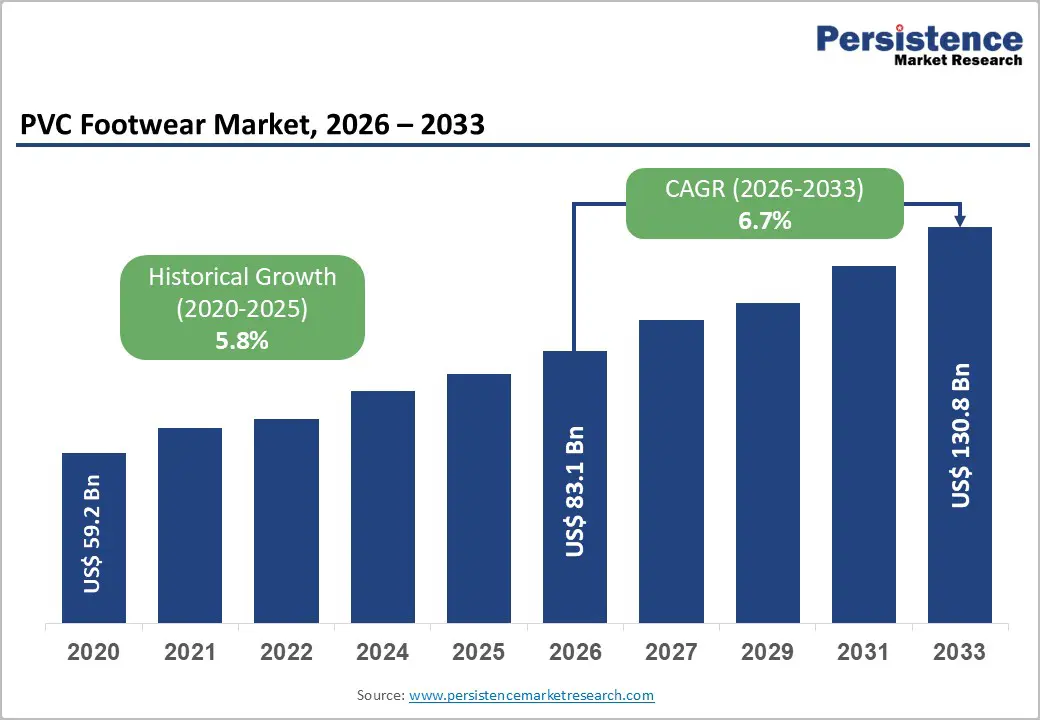

The global PVC Footwear market size is likely to be valued at US$ 83.1 billion in 2026 and is expected to reach US$ 130.8 billion by 2033, growing at a CAGR of 6.7% during the forecast period from 2026 to 2033. The market's strong and sustained growth is primarily driven by the unmatched cost-competitiveness of polyvinyl chloride (PVC) as a raw material relative to natural rubber and leather, widespread urbanization in high-population emerging economies, and rising consumer preference for waterproof, lightweight, and durable everyday footwear.

Key Market Highlights

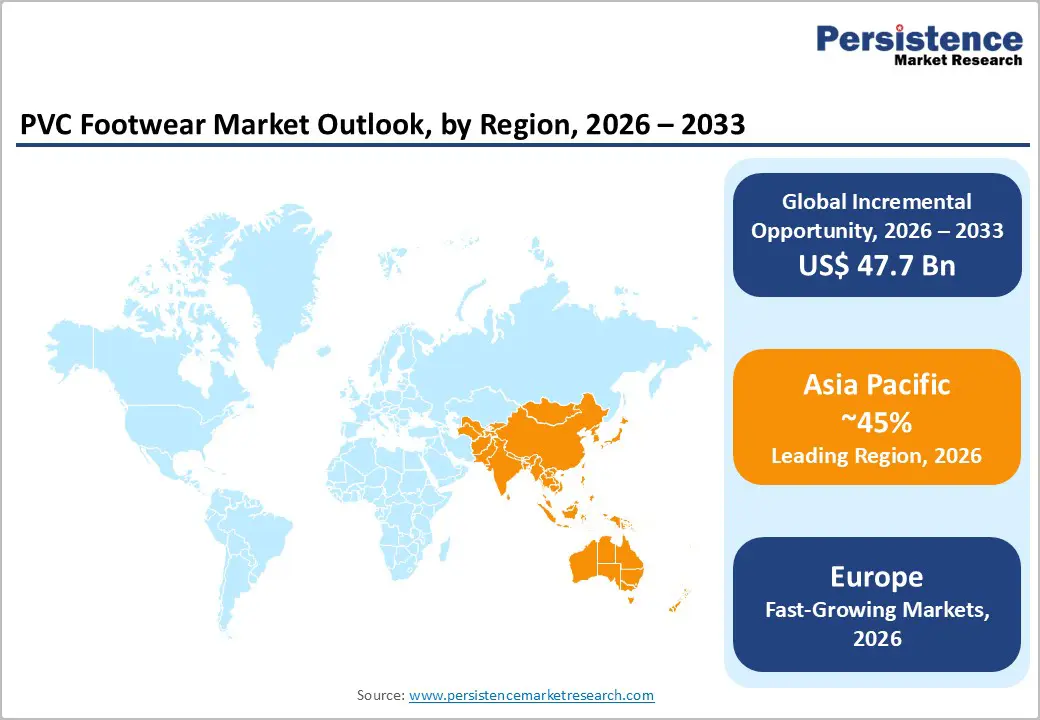

- Leading Region: Asia Pacific dominates the PVC footwear market with 45% share in the marke, led by China’s production share and India’s expanding capacity under government-backed PLI schemes.

- Fastest Growing Region: The fastest growing region in the global PVC footwear market is Europe with rising CAGR of 8.9%, driven by rising disposable incomes, expanding manufacturing capabilities, and increasing retail and e-commerce penetration.

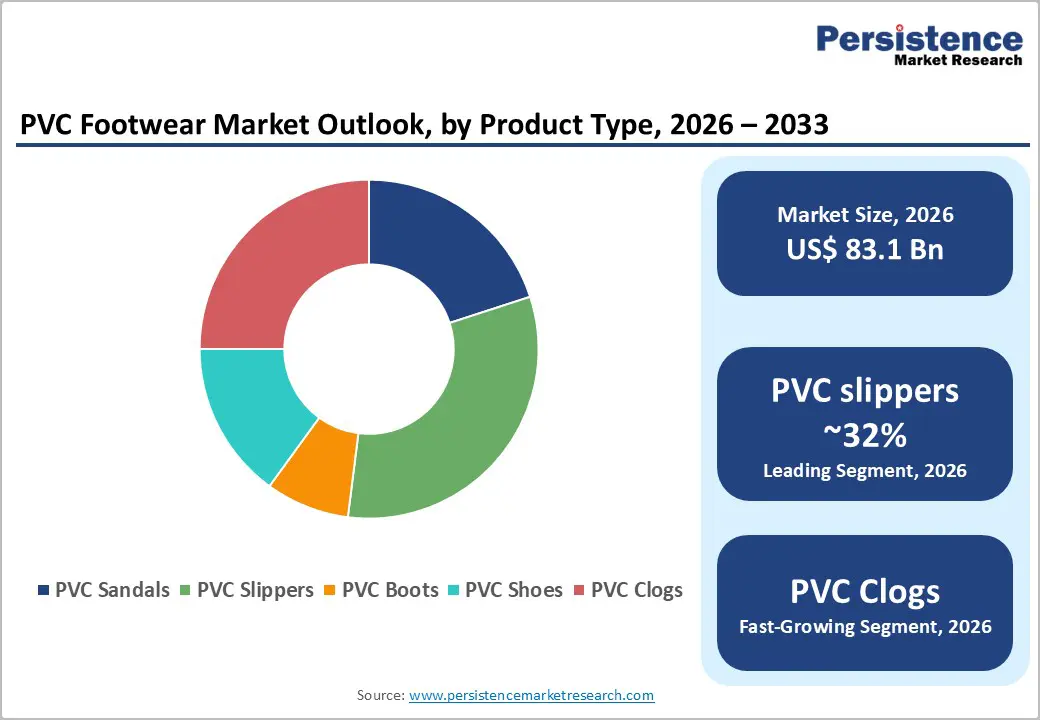

- Dominant Product Segment: PVC slippers hold the largest revenue share at around 32%, driven by affordability, year-round demand, and high-volume production across Asia.

- Fastest Growing DistributionSegment: Online distribution is the fastest growing channel, fueled by e-commerce expansion, smartphone penetration, and digital-focused strategies of brands like Crocs, Inc.

- Key Opportunity: Certified industrial PVC safety boots offer strong B2B growth potential, supported by workplace safety standards and rapid industrialization across emerging economies.

| Key Insights | Details |

|---|---|

|

PVC Footwear Market Size (2026E) |

US$ 83.1 Billion |

|

Market Value Forecast (2033F) |

US$ 130.8 Billion |

|

Projected Growth CAGR (2026–2033) |

6.7% |

|

Historical Market Growth (2020–2025) |

5.8% |

Market Dynamics

Drivers - Low-Cost PVC Material Continues to Drive High-Volume Footwear Production Across Developing and Price-Sensitive Global Markets

PVC (polyvinyl chloride) continues to be one of the most cost-effective synthetic materials used in footwear manufacturing, making it highly preferred in mass-market and value segments, especially across developing economies. The relatively low cost of PVC resin, compared to natural rubber or genuine leather, allows manufacturers to price products competitively for price-sensitive consumers. According to the World Footwear Yearbook 2024 published by APICCAPS, global footwear production reached 22.4 billion pairs in 2023, with Asia contributing 87.1% of total output.

Countries such as China, India, and Brazil, which dominate global footwear production, rely heavily on PVC due to its durability, water resistance, and chemical stability. These properties make PVC ideal for everyday casual and work footwear. Its strong cost advantage ensures continued adoption by both organized manufacturers and the unorganized sector, firmly establishing PVC as a backbone material in the global footwear supply chain.

Urban Population Growth and Rising Middle-Class Incomes Fuel Expanding Demand for Affordable and Stylish PVC Footwear

Rapid urbanization across the Asia Pacific, Latin America, and Sub-Saharan Africa is steadily expanding the consumer base for affordable synthetic footwear. The United Nations Department of Economic and Social Affairs projects that the global urban population will approach 5 billion by 2030, with developing regions contributing significantly to this growth. Urban consumers increasingly seek functional, stylish, and waterproof footwear at accessible price points, and PVC products meet these needs effectively.

In India, the footwear industry directly employs over 1.1 million people and accounts for 11.6% of global production volume, according to the World Footwear Yearbook 2024. Rising middle-class incomes in Southeast Asia and Latin America are also driving gradual premiumization within PVC categories, including fashionable sandals and designer-style clogs. This combination of expanding urban populations and improving purchasing power continues to create strong and sustainable demand momentum for PVC footwear globally.

Restraints - Stringent Environmental Regulations and Growing Sustainability Concerns Create Compliance Pressures for PVC Footwear Manufacturers Globally

PVC footwear faces growing regulatory pressure due to concerns regarding plasticizers, particularly phthalates, used to enhance flexibility and softness during production. The European Chemicals Agency enforces strict limits under the REACH Regulation, restricting certain phthalates such as DEHP, DBP, and BBP to 0.1% by weight in consumer products. Compliance with these regulations increases manufacturing costs, especially for companies targeting premium markets such as the European Union and North America.

Producers are often required to reformulate raw materials to meet safety standards, which adds operational complexity. In addition, rising consumer awareness about microplastic pollution, plastic waste disposal challenges, and carbon emissions is negatively impacting the perception of PVC-based products in environmentally conscious markets. This shift in consumer preference, particularly in Western economies, is moderating demand growth in higher-income segments and creating long-term sustainability challenges for PVC footwear manufacturers.

Rising Adoption of EVA and Other Advanced Materials Intensifies Competitive Pressure on Traditional PVC Footwear Segments

PVC footwear is facing increasing competition from alternative materials such as ethylene-vinyl acetate (EVA), thermoplastic polyurethane (TPU), and thermoplastic rubber (TPR). These materials offer benefits such as lighter weight, better cushioning, improved flexibility, and, in some cases, a more favorable environmental profile. EVA has gained strong popularity in casual and sports-inspired footwear categories due to its comfort and lightweight characteristics.

A well-known example is the global success of Crocs, Inc., which has popularized EVA-based clog designs worldwide. Industry data indicates that EVA products are gradually replacing PVC in children’s footwear, sports-adjacent styles, and premium casual categories. This shift limits PVC’s growth potential in higher-margin product segments, particularly in developed markets where consumers are willing to pay slightly higher prices for improved comfort and sustainability features.

Opportunity - Rapid Expansion of E-Commerce Platforms Unlocks New Direct-to-Consumer Growth Opportunities for PVC Footwear Brands

The rapid growth of e-commerce across Asia, Latin America, and the Middle East & Africa presents a major opportunity for PVC footwear manufacturers. Online marketplaces such as Alibaba, Flipkart, Mercado Libre, and Amazon have significantly expanded consumer access to affordable footwear in regions where organized retail penetration remains limited. Improved digital infrastructure in developing countries is enabling even small and mid-sized PVC brands to participate in cross-border trade. Notably, Crocs, Inc. reported that digital sales accounted for 37.2% of its consolidated revenues in 2024, highlighting the structural shift toward online purchasing. Brands investing in mobile-friendly platforms, influencer-driven marketing, and efficient last-mile delivery networks are well positioned to capture expanding online demand and strengthen direct-to-consumer relationships in the coming years.

Increasing Industrial Safety Regulations Strengthen Institutional Demand for Certified and Durable PVC Safety Boots Worldwide

PVC boots hold a strong position in industrial and occupational safety footwear, where waterproofing, chemical resistance, durability, and affordability are critical requirements. The global safety footwear market continues to expand as governments enforce stricter workplace safety regulations. The International Labour Organization estimates that occupational accidents and diseases cost nearly 3.94% of global GDP annually, reinforcing the need for protective equipment such as certified safety footwear.

Regulatory frameworks such as the EU Personal Protective Equipment Directive and ASTM standards in North America mandate compliance for workplace footwear, creating consistent institutional demand. Industries including agriculture, construction, food processing, chemical manufacturing, and healthcare rely heavily on PVC safety boots for operational safety. Manufacturers focusing on B2B procurement channels, especially in rapidly industrializing regions, can benefit from stable, high-volume contracts and relatively stronger margins compared to highly competitive consumer retail segments.

Category-wise Analysis

By Product Type Insights

PVC slippers hold the leading share in the global PVC footwear market, accounting for approximately 32% of total revenue. Their dominance is driven by consistent year-round demand for affordable indoor and outdoor casual footwear across South Asia, Southeast Asia, Sub-Saharan Africa, and Latin America. Slippers represent the most basic and widely purchased footwear category, with typical retail prices ranging from USD 1 to USD 8 in mass-market channels.

Asia Pacific remains the primary production hub, with China manufacturing 12.3 billion pairs of footwear in 2023, capturing nearly 55% of global production. A significant portion of this output consists of slippers and flip-flops. The segment’s leadership is supported by frequent replacement cycles due to regular wear and tear, combined with limited seasonal dependency. These factors ensure steady, high-volume demand, reinforcing slippers as the backbone of the global PVC footwear market.

By Distribution Channel Insights

The offline distribution channel continues to dominate the PVC footwear market, accounting for nearly 65% of total revenue. In price-sensitive and high-volume markets across Asia Pacific, Africa, and Latin America, most purchases occur through traditional retail outlets such as local footwear shops, general stores, bazaars, and specialty chains. Consumers prefer physical stores because they can check product quality, comfort, and fit before purchase.

Large retail networks operated by companies such as Bata Corporation, Decathlon, and Shoe Carnival, Inc. further strengthen offline sales presence. However, online sales are growing at a faster pace, driven by increasing internet penetration and digital payment adoption. The steady expansion of e-commerce platforms is gradually narrowing the gap between offline and online channels.

By End-user Insights

The women’s segment leads the global PVC footwear market, accounting for approximately 38% of total revenue share. Women’s footwear typically demonstrates higher purchase frequency, greater style diversity, and stronger demand across casual, formal, and seasonal categories compared to men’s and children’s segments. PVC sandals and fashion-oriented shoes targeting women benefit from continuous design innovation, including metallic finishes, textured patterns, platform soles, and ergonomic footbeds.

In many markets, women play a primary role in household purchasing decisions related to apparel and footwear, reinforcing structural demand strength. Additionally, rising female workforce participation across South and Southeast Asia is increasing demand for practical yet stylish footwear suitable for both workplace and everyday use. These factors collectively position the women’s segment as the most influential and revenue-generating category within the global PVC footwear market.

Regional Insights

North America PVC Footwear Market Trends

The North American PVC footwear market is primarily driven by the United States, one of the largest footwear consumer markets globally. According to the American Apparel and Footwear Association (AAFA), Americans purchase nearly 2.5 billion pairs of footwear each year, with most products imported from countries such as China and Vietnam. In this region, PVC footwear ranges from affordable private-label offerings sold through mass retailers like Walmart and Target to premium designer PVC clogs and fashion sandals distributed through specialty stores.

Product safety and quality standards are regulated by the U.S. Consumer Product Safety Commission (CPSC) and ASTM International, creating a structured, compliance-driven market environment. Brand innovation plays a crucial role, with Crocs, Inc. significantly shaping the global PVC clog segment through consistent growth and strong consumer demand for casual, waterproof, and easy-to-maintain footwear.

Europe PVC Footwear Market Trends

Europe represents a mature and highly regulated PVC footwear market, with strong demand across Germany, the United Kingdom, France, Spain, and Italy. Regulatory frameworks such as the European Commission’s REACH Regulation and the EU Green Deal are influencing product development by encouraging the use of phthalate-free plasticizers and recyclable or bio-based PVC materials. The European Footwear Confederation (CEC) plays an important role in supporting industry stakeholders while ensuring compliance with environmental standards.

In countries such as the United Kingdom and Germany, PVC rain boots and garden footwear remain consistent consumer essentials due to long wet seasons and strong outdoor lifestyles. Meanwhile, Spain and France experience high seasonal demand for PVC sandals during summers. Sustainability is becoming a key purchasing factor, with consumers increasingly preferring eco-labeled products and transparent supply chains. Companies such as Bata Corporation have adopted recycled PVC materials in gumboot production, demonstrating measurable carbon emission reductions in sustainability reports.

Asia Pacific PVC Footwear Market Trends

Asia Pacific leads the global PVC footwear market as both the largest manufacturing hub and the fastest-growing consumption region. China remains the dominant producer, accounting for nearly 35% of global footwear production, with PVC slippers, sandals, and boots forming a major share of exports. India has also strengthened its position in global footwear manufacturing, supported by government initiatives such as the Production Linked Incentive (PLI) Scheme introduced by the Ministry of Commerce and Industry to boost domestic production and exports.

Emerging manufacturing destinations, including Vietnam, Indonesia, Bangladesh, and Cambodia, are gaining importance as global brands diversify supply chains to reduce overdependence on China. Companies such as Crocs, Inc. are expanding partnerships in Vietnam and Indonesia while increasing retail presence across China, India, and Southeast Asia. In Japan and South Korea, consumers are shifting toward premium and ergonomic PVC footwear, supporting regional value growth. Overall, the Asia Pacific is expected to maintain strong growth leadership throughout the forecast period.

Competitive Landscape

The global PVC footwear market is highly fragmented, consisting of multinational corporations, strong regional players, and numerous small and medium-sized local manufacturers, particularly concentrated in Asia. Leading global companies such as Bata Corporation, Crocs, Inc., Skechers USA, Inc., and VF Corporation compete through brand recognition, product innovation, and extensive global distribution networks.

At the regional level, players including VKC Group, Grendene S.A., and Fujian Jinyang Group Co., Ltd. leverage cost advantages and a strong understanding of local consumer preferences. Key strategic priorities across the industry include expanding product portfolios, investing in sustainable material sourcing and eco-certifications, strengthening digital sales channels, and entering high-growth emerging markets through partnerships, licensing agreements, and franchise expansion models.

Key Developments:

- In March 2024, Crocs, Inc. strengthened its Southeast Asian supply chain by expanding sourcing partnerships in Vietnam and Indonesia, aiming to reduce dependence on single-country manufacturing, improve cost flexibility, and enhance operational resilience amid global trade uncertainties and shifting tariff dynamics.

- In November 2024, Bata Corporation introduced an eco-conscious PVC footwear collection using phthalate-free plasticizers and recycled PVC materials in gumboots, aligning product innovation with European Union sustainability regulations and advancing circular economy commitments across its global manufacturing and retail network.

- In February 2025, Grendene S.A. reported record export volumes of PVC sandals under its Havaianas brand to North America and Europe, driven by favorable currency movements and strong international demand for premium casual flip-flops and fashion-oriented PVC footwear products.

Companies Covered in PVC Footwear Market

- Ansell Limited

- Bata Shoe Organization

- Crocs, Inc.

- Fujian Jinyang Group Co., Ltd.

- Inter Rubber Products, Inc.

- Keds Corporation

- Skechers USA, Inc.

- Shoe Carnival, Inc.

- VF Corporation

- Dr. Martens plc

- Decathlon

- VKC Group

- Havaianas (Alpargatas S.A.)

- Bata Corporation

- Grendene S.A.

- Relaxo Footwears Limited

- Liberty Shoes Limited

- Action Shoes

- Lotto Sport Italia

- Rubber Band Co. Ltd.

Frequently Asked Questions

The market is projected to reach US$ 130.8 billion by 2033, growing at a 6.7% CAGR.

Key drivers include cost advantage over leather, urbanization, rising incomes, and growing demand for certified safety footwear.

PVC slippers dominate with about 32% revenue share due to affordability and strong year-round consumer demand.

Asia Pacific leads, driven by China’s large-scale production and India’s rapidly expanding footwear manufacturing capacity.

E-commerce expansion and rising institutional demand for industrial PVC safety boots present strong growth opportunities.