- Medical Devices

- Non-PVC IV Bags Market

Non-PVC IV Bags Market Size, Share and Growth Forecast, 2026 - 2033

Non-PVC IV Bags Market by Material Type (EVA IV bags, Polypropylene (PP) IV bags, Others), Application (Fluid & Electrolyte Therapy, Chemotherapy, Parenteral Nutrition, Drug Delivery, Blood & Plasma Handling), and Regional Analysis for 2026 - 2033

Non-PVC IV Bags Market Share and Trends Analysis

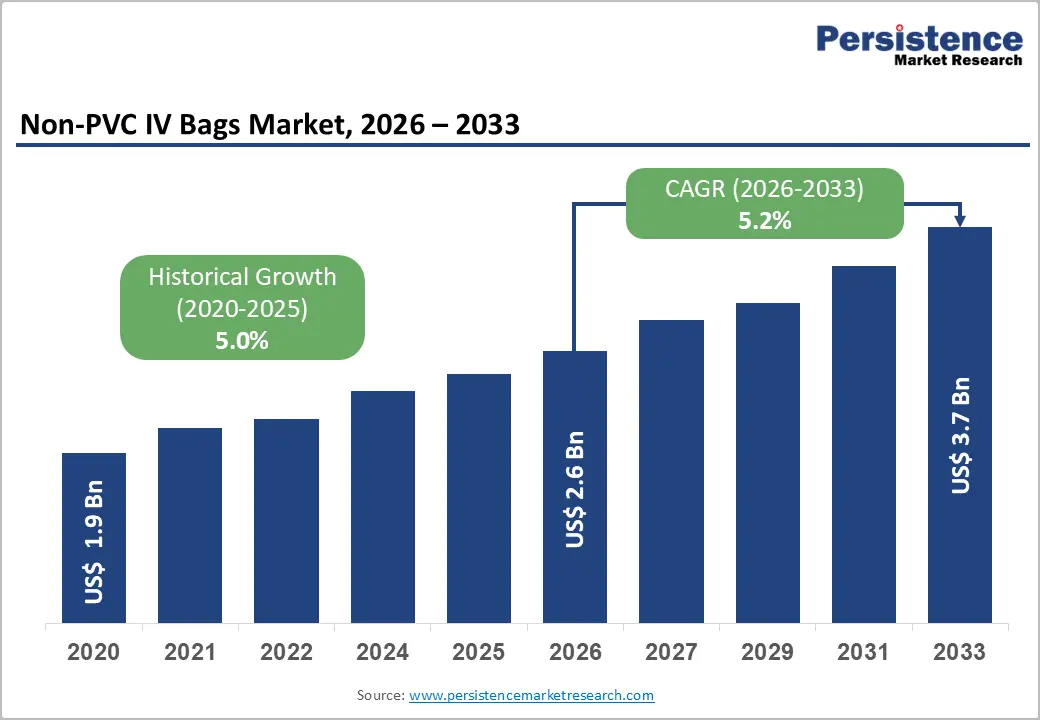

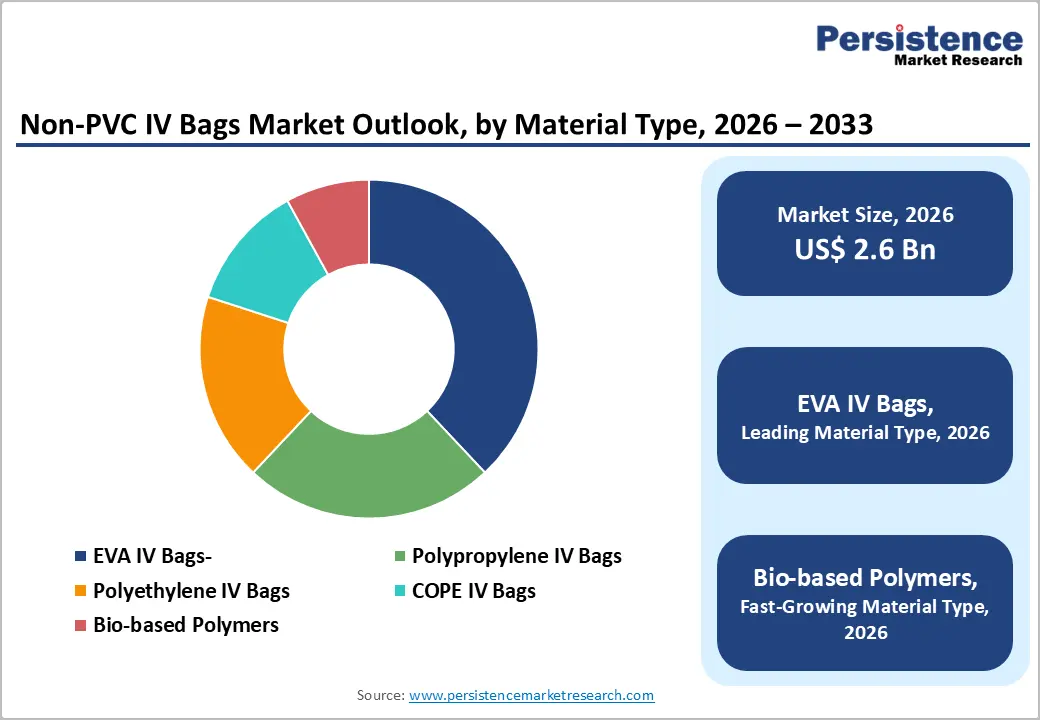

The global non-PVC IV bags market size is likely to be valued at US$ 2.6 billion in 2026 and is projected to reach US$ 3.7 billion by 2033, growing at a CAGR of 5.2% during the forecast period 2026 - 2033, driven by regulatory restrictions on PVC due to phthalate leaching concerns and increasing adoption of biocompatible IV packaging in hospitals and compounding facilities.

Demand is further supported by the rising use of parenteral nutrition bags and chemotherapy applications requiring chemically inert systems. In addition, the FDA and EMA-aligned procurement policies are accelerating the shift toward safer medical fluid delivery bags, especially in oncology and critical care. Growing surgical volumes and infusion-based therapies continue to support steady long-term demand.

Key Industry Highlights:

- Dominant Material Type: Ethylene Vinyl Acetate (EVA) IV infusion bags are expected to lead with around 38% market share in 2026, while bio-based polymers are projected to grow the fastest at 5.8% CAGR through 2033, driven by sustainability mandates and demand for recyclable IV bag materials.

- Leading Application Segment: Fluid & electrolyte therapy is anticipated to dominate with approximately 41% share in 2026, while chemotherapy IV bags are likely to be the fastest-growing segment at 5.4% CAGR, supported by rising global oncology incidence and infusion-based treatment expansion.

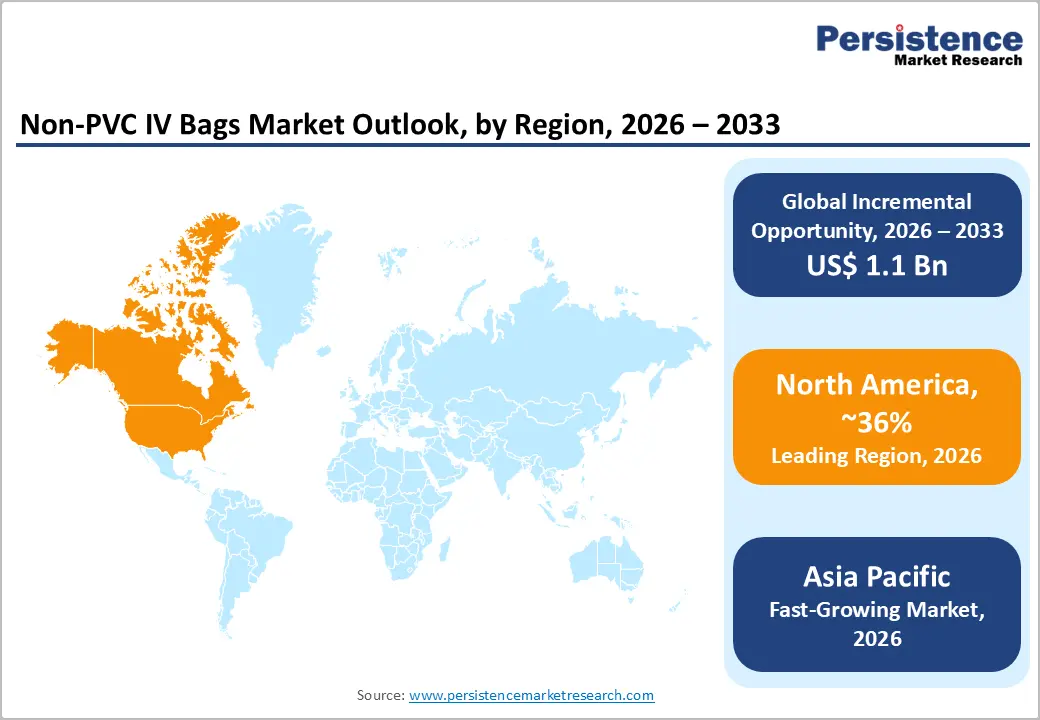

- Regional Leadership: North America is expected to lead with nearly 36% share in 2026, supported by FDA-driven compliance for PVC-free IV containers, while Asia Pacific is projected to be the fastest-growing region, driven by rapid healthcare infrastructure expansion and manufacturing scale-up of hospital infusion systems.

- Competitive & Investment Landscape: Market dynamics are being reshaped by 2025 strategic investments from Baxter, Fresenius Kabi, and B. Braun, focused on expanding production capacity and strengthening global supply chains for biocompatible IV packaging and advanced infusion solutions.

DRO Analysis

Driver - Rising Regulatory Pressure and Expanding Use of Intravenous (IV) Therapies

Global regulatory bodies, including the Food and Drug Administration (FDA, United States), European Medicines Agency (EMA), and European Chemicals Agency (ECHA), are restricting DEHP plasticizers in PVC IV systems due to leaching and long-term safety concerns. ECHA assessments, EU procurement reforms, and 2025 FDA guidance on infusion-related leachables are accelerating the shift toward PVC-free IV containers. Hospitals are increasingly adopting EVA IV infusion bags and polypropylene alternatives. EU Green Deal policies and U.S. state-level restrictions further reinforce this transition. These measures are driving widespread adoption of biocompatible IV packaging.

The rising use of intravenous therapies is expanding market demand across healthcare systems. The increasing prevalence of cancer, diabetes, and renal disorders, along with higher surgical and emergency care volumes, is boosting the consumption of hospital infusion systems. Demand for parenteral nutrition bags and chemotherapy infusions is also rising with aging populations. This is increasing per-patient IV usage intensity globally. Together, regulatory substitution and rising clinical IV adoption are strengthening demand for medical fluid delivery bags and supporting sustained market growth.

Restraint - Higher Production Costs and Complex Manufacturing Transition

A major restraint in the non-PVC IV bags market is the relatively high production cost of alternative polymers such as EVA, COPE, and polypropylene compared to conventional PVC-based systems. According to the U.S. Department of Health and Human Services (HHS) medical device cost assessments, non-PVC materials can increase production costs by 20-35%, depending on sterilization and barrier requirements.

These cost differentials create procurement challenges for public hospitals in cost-sensitive regions such as Latin America, parts of Asia, and Africa. Additionally, switching production lines requires significant capital investment in extrusion, sealing, and sterilization technologies. Smaller manufacturers face barriers in scaling hospital infusion systems compatible with non-PVC formats, limiting competitive participation and slowing adoption in price-sensitive healthcare ecosystems.

Opportunity - Expansion of Biopharmaceutical Infusion Therapies and Personalized Medicine

The expansion of biologics and personalized medicine is creating a strong opportunity for advanced parenteral nutrition bags and drug-specific infusion systems. The biopharmaceutical sector increasingly depends on stable, non-reactive biocompatible IV packaging for biologics and monoclonal antibodies, especially in oncology and immunotherapy, where drug integrity is critical. This is strengthening demand for high-performance PVC-free IV containers across specialty care and hospital infusion systems.

This opportunity is reinforced by the FDA actions tightening expectations on infusion safety and leachable substances in drug delivery systems. Rising biologics approvals and expanding oncology pipelines are increasing infusion volumes globally. The scaling of sterile injectable and oncology manufacturing capacity across the U.S., Europe, India, and China is accelerating demand for chemically inert medical fluid delivery bags. These shifts are creating sustained long-term growth potential for the Non-PVC IV bags market.

Category-wise Analysis

Material Type Insights

EVA IV infusion bags are expected to lead the market with an estimated 38% share in 2026, driven by strong adoption in oncology, ICU, and nutrition therapies due to superior drug stability and low extractable risks. Increasing regulatory emphasis on infusion safety and material inertness is steadily shifting hospital preference toward PVC-free IV containers. This is reinforcing demand for biocompatible IV packaging, positioning EVA as the preferred material for critical and high-sensitivity drug delivery applications.

Bio-based polymers are likely to grow at a CAGR of 5.8% during 2026 - 2033, supported by sustainability mandates and healthcare waste reduction initiatives. Hospitals are increasingly evaluating recyclable medical fluid delivery bags to align with green procurement policies and environmental compliance requirements. Early-stage adoption in public healthcare systems is gaining traction, gradually supporting commercial scale-up. This is expected to strengthen their role in next-generation PVC-free IV containers.

Application Insights

Fluid & electrolyte therapy is expected to dominate with an estimated 41% share in 2026, supported by consistently high hospital admissions and emergency care utilization. It continues to form the backbone of hospital infusion systems, widely used in trauma care, surgical recovery, and dehydration management. Rising inpatient volumes and aging populations are likely to sustain steady demand, ensuring continuous consumption of medical fluid delivery bags across global healthcare systems.

Chemotherapy is projected to grow at a CAGR of 5.4% during 2026 - 2033, driven by increasing cancer prevalence and expanding oncology treatment infrastructure. Greater reliance on infusion-based cancer therapies is accelerating demand for specialized chemotherapy IV bags with high chemical resistance and safety standards. Expansion of oncology centers and rising treatment cycles are expected to further strengthen the adoption of biocompatible IV packaging, positioning it as a key growth driver in advanced therapeutic care.

Regional Analysis

North America Non-PVC IV Bags Market Trends

North America is expected to account for approximately 36% share of the global non-PVC IV bags market in 2026, supported by advanced healthcare infrastructure and stringent FDA oversight on infusion safety. The region is expected to witness steady migration toward PVC-free IV containers, driven by high oncology treatment intensity and continuous hospital procurement upgrades. Strengthening regulatory attention on leachable risks in infusion systems will reinforce the adoption of biocompatible IV packaging across acute and critical care settings.

U.S. Non-PVC IV Bags Market Trends

The U.S. is expected to represent nearly 35% of the North America market, driven by high and sustained IV therapy utilization across oncology, ICU, and chronic disease management. In 2025, FDA-linked safety communications on infusion material compatibility will have increased hospital focus on drug-container interaction risks, strengthening demand for medical fluid delivery bags. Expanding standardized procurement across large hospital networks is likely to further support the adoption of EVA IV infusion bags.

Canada Non-PVC IV Bags Market Trends

Canada is anticipated to hold around 10% share of the regional market in 2026, supported by publicly funded healthcare systems emphasizing patient safety and material compliance. In 2026, provincial healthcare upgrades are expected to increasingly prioritize reduced chemical exposure in medical consumables, supporting a gradual shift toward PVC-free IV containers. Rising oncology treatment demand and hospital modernization initiatives are likely to sustain steady growth in hospital infusion systems across tertiary care settings.

Europe Non-PVC IV Bags Market Trends

Europe is set to account for nearly 28% share of the global non-PVC IV bags market in 2026, driven by strict EMA and REACH regulations restricting hazardous plasticizers in medical devices. The region is expected to see steady expansion in demand for PVC-free IV containers, supported by sustainability-focused procurement under EU Green Deal frameworks. Centralized healthcare systems are likely to ensure stable demand for standardized biocompatible IV packaging, particularly in oncology and intensive care applications.

Germany Non-PVC IV Bags Market Trends

Germany is projected to account for approximately 30% of the Europe market in 2026, supported by advanced hospital procurement systems and a strong chemical safety compliance culture. In 2025, hospital procurement updates are expected to have increasingly emphasized low-extractable infusion materials, supporting stronger adoption of EVA IV infusion bags. Expanding oncology infrastructure is likely to continue driving demand for medical fluid delivery bags in high-acuity care environments.

U.K. Non-PVC IV Bags Market Trends

The U.K. is expected to represent around 15% share of Europe in 2026, supported by NHS modernization and procurement standardization initiatives. In 2026, NHS sustainability-driven healthcare reforms are expected to further reinforce focus on reducing chemical exposure in medical consumables, supporting a gradual shift toward PVC-free IV containers. Rising cancer care volumes and expansion of outpatient infusion services are likely to strengthen demand for hospital infusion systems across major healthcare trusts.

Asia Pacific Non-PVC IV Bags Market Trends

Asia Pacific is likely to remain the fastest-growing regional market, projected to expand at a CAGR of 6% during 2026 - 2033, driven by rapid hospital infrastructure expansion, pharmaceutical manufacturing growth, and rising infusion therapy adoption. The region is expected to benefit from strong production ecosystems for polypropylene IV bags and cost-efficient infusion solutions. Expanding oncology infrastructure and healthcare access improvements are likely to significantly increase demand for medical fluid delivery bags across emerging economies.

China Non-PVC IV Bags Market Trends

China is likely to account for nearly 35% share of the Asia Pacific market in 2026, supported by large-scale hospital infrastructure expansion and strong domestic manufacturing capacity. In 2025, national healthcare modernization programs are expected to have accelerated upgrades in tertiary hospitals, increasing the adoption of advanced hospital infusion systems. Growth in sterile injectable production and oncology care expansion is likely to further strengthen demand for PVC-free IV containers in high-volume urban hospitals.

India Non-PVC IV Bags Market Trends

India is likely to represent around 20% share of the regional market, supported by expanding healthcare access and rising pharmaceutical exports. In 2026, hospital capacity expansion initiatives and oncology infrastructure development are expected to accelerate the adoption of EVA IV infusion bags in tertiary care centers. Growing sterile manufacturing clusters and rising infusion therapy penetration are likely to reinforce demand for biocompatible IV packaging, improving the availability of cost-efficient medical fluid delivery bags across healthcare systems.

Competitive Landscape

The global non-PVC IV bags market is likely to remain moderately consolidated, with leading players such as Baxter International, Fresenius Kabi, B. Braun Melsungen AG, and ICU Medical accounting for a significant share of global revenue. These companies are leveraging strong hospital relationships, regulatory expertise, and integrated infusion therapy portfolios to strengthen market positioning. Investments in biocompatible IV packaging and sustainable PVC-free IV containers are expected to remain key competitive priorities.

Regional manufacturers and specialized medical packaging firms are increasingly focusing on cost-efficient production of EVA IV infusion bags and recyclable infusion materials to expand their presence in emerging healthcare markets. High regulatory compliance requirements and sterile manufacturing standards are likely to continue limiting new entrants. However, rising demand for oncology therapies and advanced medical fluid delivery bags is expected to create opportunities for niche innovators and strategic supply chain partnerships.

Key Industry Developments:

- In March 2025, Fresenius Kabi expanded its Generic IV Drugs portfolio in the U.S., including launches of potassium phosphate bags and injectable formulations requiring advanced sterile infusion packaging systems.

- In January 2025, B. Braun reported continued expansion of its Hospital Care division, supported by rising demand for infusion therapy consumables and advanced IV systems across Asia Pacific and Europe.

Companies Covered in Non-PVC IV Bags Market

- Baxter International Inc.

- Fresenius Kabi AG

- B. Braun Melsungen AG

- ICU Medical Inc.

- Terumo Corporation

- Smiths Medical

- Hospira

- Grifols S.A.

- Sippex IV Bag Systems

- JW Life Science

- Sichuan Kelun Pharmaceutical

- Otsuka Pharmaceutical Factory

- Technoflex

- Kraton Corporation

- Wipak Group

Frequently Asked Questions

The global non-PVC IV bags market is projected to reach US$ 2.6 billion in 2026.

Rising regulatory restrictions on PVC materials, growing IV therapy volumes, and increasing demand for safer biocompatible IV packaging drive the market.

The market is expected to grow at a CAGR of 5.2% from 2026 to 2033.

Growth opportunities lie in biologics infusion therapies, oncology treatment expansion, and the rising adoption of sustainable PVC-free IV containers.

Baxter International, Fresenius Kabi, B. Braun Melsungen AG, and ICU Medical are the key players in the market.