- Plastics, Polymers & Resins

- PVC Processing Aids Market

PVC Processing Aids Market Size, Share, and Growth Forecast, 2026 – 2033

PVC Processing Aids Market by Product Type (Acrylic Processing Aids, Methacrylate Processing Aids, Others), Application (Pipes & Fittings, Rigid Sheets & Panels, Wires & Cables, Others), End-User (Building & Construction, Automotive, Electrical & Electronics, Packaging, Others), and Regional Analysis for 2026-2033

PVC Processing Aids Market Share and Trends Analysis

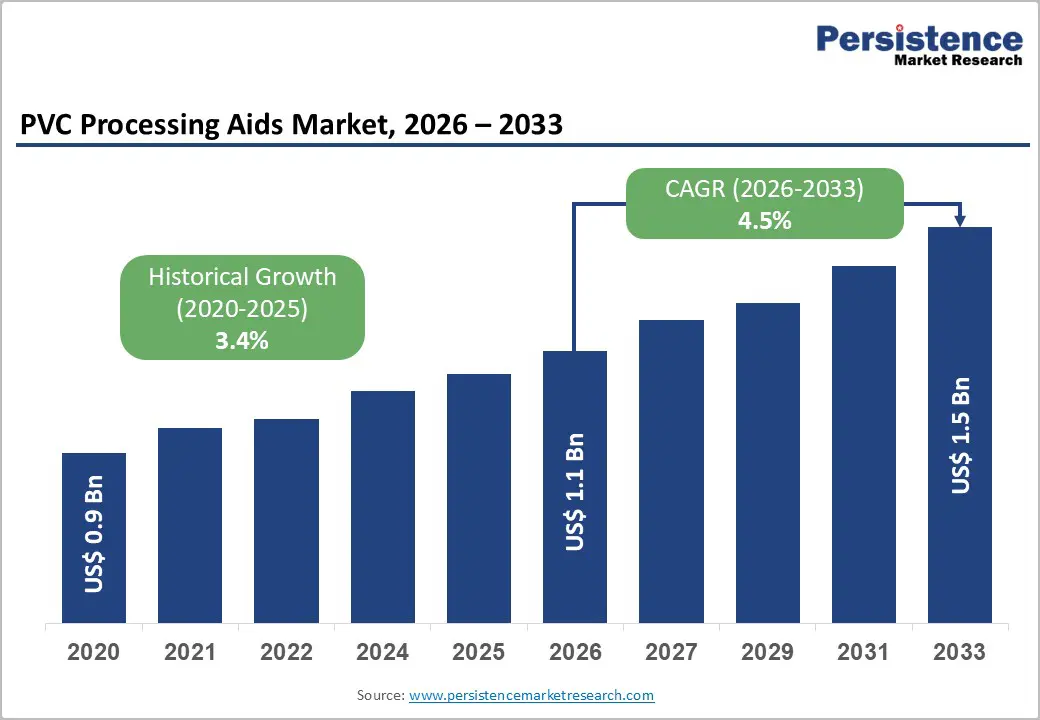

The global PVC processing aids market size is likely to be valued at US$ 1.1 billion in 2026, and is projected to reach US$ 1.5 billion by 2033, growing at a CAGR of 4.5% during the forecast period 2026−2033.

The market is entering a phase of sustained expansion driven by a strengthening demand from construction, infrastructure renewal, and industrial manufacturing value chains. The conclusion remains clear: long-term growth stems from steady expansion of PVC consumption, aligned with urbanization, infrastructure modernization, and manufacturing efficiency imperatives. Rapid urban population growth increases demand for pipes, profiles, and sheets, thereby increasing dependence on additives that enhance melt strength, surface finish, and processing stability.

Industrial users increasingly prioritize consistent output quality and reduced production downtime, creating direct demand for advanced processing aids that improve extrusion and molding performance. Technology integration across polymer processing facilities accelerates the adoption of performance-enhancing additives, as manufacturers seek automation compatibility and defect reduction. Awareness among processors of lifecycle cost optimization strengthens adoption, as processing aids reduce scrap rates and energy intensity.

Key Industry Highlights

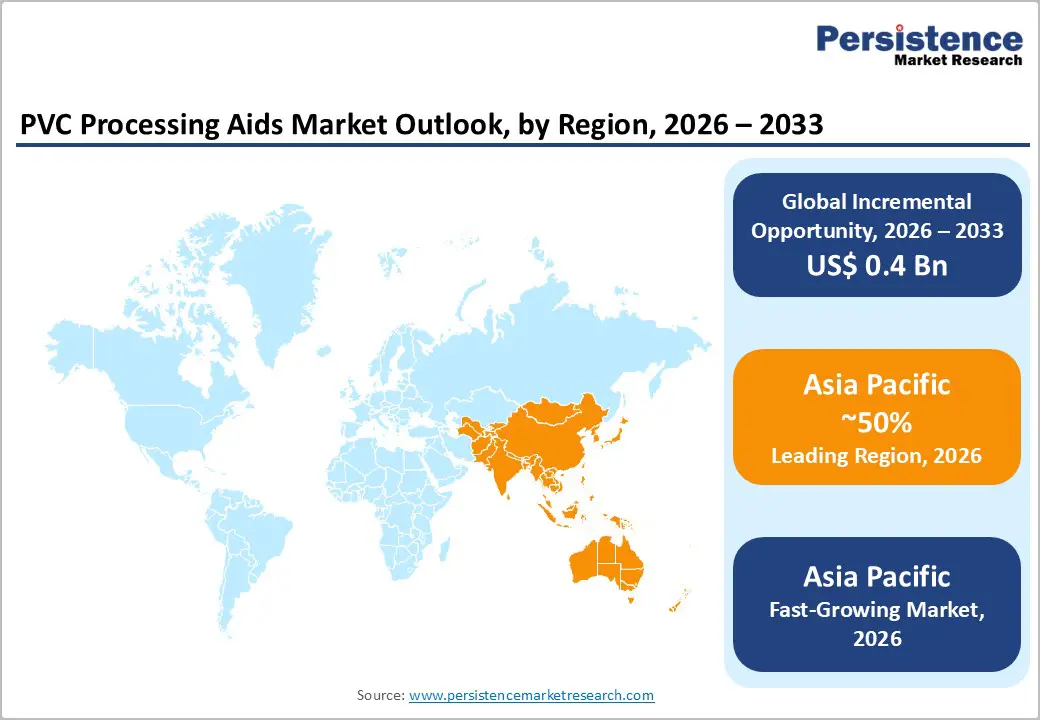

- Dominant Region: Asia-Pacific is expected to lead, with an estimated 50% market share, driven by high-volume manufacturing and infrastructure expansion.

- Fastest-growing Regional Market: Asia Pacific is also forecasted to be the fastest-growing market through 2033, propelled by industrial modernization and increasingly supportive policies.

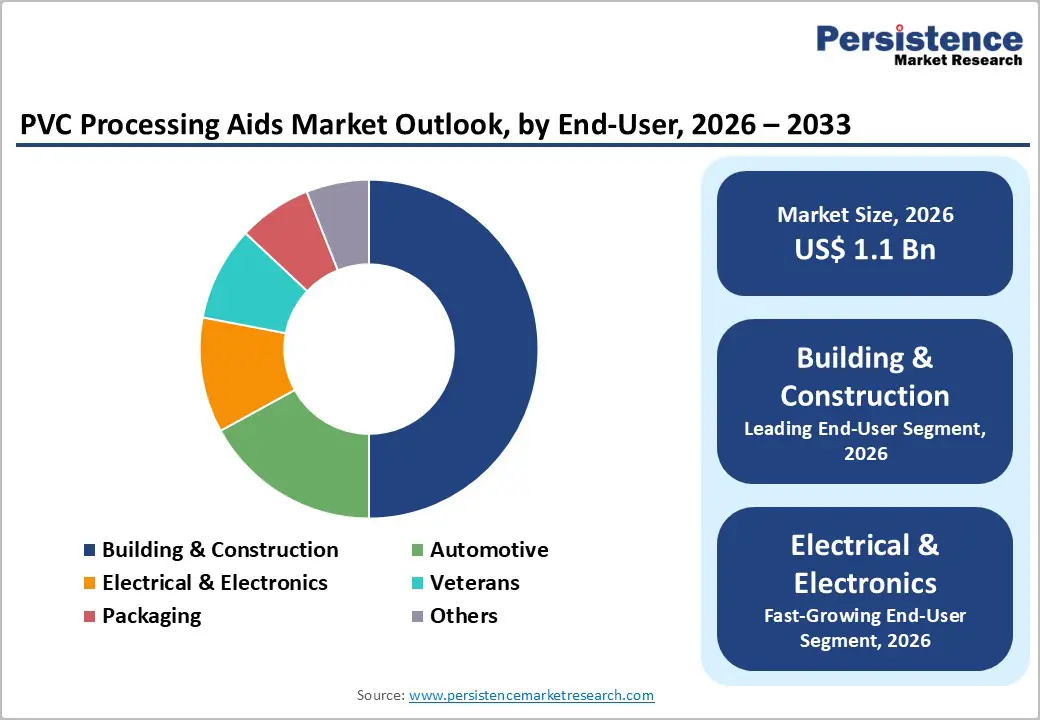

- Leading End-User: Building and construction activities are likely to lead the market with a projected 50% revenue share, fueled by extensive PVC use, quality requirements, and regulatory compliance.

- Fastest-growing End-User: Electrical & electronics are expected to be the fastest-growing segment through 2033, powered by electrification, insulation requirements, and advanced manufacturing.

| Key Insights | Details |

|---|---|

|

PVC Processing Aids Market Size (2026E) |

US$ 1.1 Bn |

|

Market Value Forecast (2033F) |

US$ 1.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expansion of Infrastructure and Construction Activity

Strong infrastructure and construction activity fundamentally drive demand for PVC processing aids by increasing the volume and complexity of PVC products that must be manufactured efficiently and to exacting quality standards. Processing aids are specialty additives that enhance PVC’s flow characteristics during extrusion and molding, reducing melt viscosity and improving surface quality, which is essential in producing high-performance construction components such as pipes, fittings, profiles, and window frames.

As large-scale infrastructure and building projects proliferate, manufacturers face pressure to maintain high output rates, minimize defects, and ensure dimensional accuracy in products that must withstand mechanical stress, have long service lives, and be exposed to the environment. PVC processing aids play a pivotal role in ensuring these outcomes while optimizing production efficiency and lowering defect rates.

High construction activity also elevates the technical expectations placed on PVC products. Modern infrastructure requirements emphasize durability, cost-effectiveness, and compliance with performance standards for water distribution, drainage systems, and building envelopes. Without processing aids, the intrinsic high viscosity of PVC resin makes it difficult to achieve smooth extrusion, uniform wall thickness, and high throughput, all of which are critical in mass construction material manufacturing. Processing aids enable manufacturers to achieve these performance benchmarks, lower energy consumption in production, and reduce cycle times.

Regulatory Scrutiny on Polymer Additives

Strict and evolving regulatory requirements on chemical additives increase cost and complexity for manufacturers that use these components to modify polymer properties. Many additives, such as certain plasticizers and stabilizers, have been identified by authorities as potential health or environmental hazards, which require extensive testing, reporting and compliance documentation before they can be used in production.

For example, regulatory agencies in the European Union have scrutinized and restricted a subset of additives under comprehensive frameworks such as Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH), with several substances requiring special authorization or facing phase-outs due to toxicity concerns. This generates significant barriers to market entry for new formulations and can delay product launches while compliance data are developed and reviewed.

Manufacturers face extended lead times and increased technical burden due to regulatory uncertainty and frequent updates to restricted-substance lists. Compliance often requires redesigning existing formulations or qualifying alternative chemistries to meet the latest safety standards, thereby increasing research and development costs. Risk management obligations also impose ongoing monitoring and documentation, thereby diverting resources from the optimization of processing performance. Regulatory divergence between regions adds further complexity; companies targeting global supply chains must navigate overlapping and sometimes conflicting requirements, compelling tailored solutions for each jurisdiction.

Advent of Sustainability-Oriented Processing Solutions

Manufacturers are increasingly prioritizing eco-efficient production methods as regulatory frameworks tighten, and consumer expectations shift toward environmentally responsible products. Processing solutions designed to minimize energy consumption, reduce volatile organic compound (VOC) emissions, and enhance recyclability are gaining traction across the value chain. These solutions enable consistent product quality while lowering environmental footprint, allowing processors to align operational performance with global sustainability mandates.

Companies adopting such practices can achieve cost efficiencies through optimized material usage and waste reduction, creating competitive differentiation in a landscape where environmental compliance and resource efficiency are critical decision factors. The shift toward circular economy principles amplifies the relevance of sustainable processing. Innovations in biodegradable additives, bio-based stabilizers, and energy-efficient auxiliaries enhance product lifecycle management and end-of-life recyclability.

Integration of these solutions facilitates compliance with extended producer responsibility requirements and supports brand positioning aligned with eco-conscious standards. Collaboration with suppliers and downstream partners ensures that sustainability considerations permeate the supply chain, enhancing transparency and accountability. Organizations that leverage these solutions can anticipate long-term value creation by mitigating environmental risks, enhancing regulatory readiness, and meeting the growing demand for responsible industrial practices among end users and institutional clients.

Category-wise Analysis

Product Type Insights

Acrylic processing aids are anticipated to secure around 45% of the PVC processing aids market revenue share in 2026, reflecting strong acceptance across high-volume extrusion and molding operations. These aids provide balanced improvements in melt strength, fusion consistency, and surface quality, making them highly suitable for pipes, profiles, and sheets. Their predictable behavior under varying processing conditions allows manufacturers to maintain consistent product output while minimizing defects. Compatibility with automation systems enhances operational efficiency, enabling seamless integration into large-scale production lines. Long-standing supplier portfolios and widespread regulatory familiarity reduce adoption barriers, while ongoing innovations targeting improved dispersion, thermal stability, and processing efficiency continue to reinforce their leadership position in the market.

Methacrylate processing aids are expected to be the fastest-growing segment during the 2026–2033 forecast period, propelled by demand for enhanced clarity, gloss, and surface finish in premium PVC applications. Increasing adoption is driven by industries requiring aesthetic precision, such as electrical components, automotive parts, and decorative panels, where surface quality directly affects commercial value. Continuous technological refinements expand processing window flexibility, allowing processors to optimize operations across varying temperature and shear conditions. Equipment upgrades and the pursuit of high-value product differentiation accelerate adoption, while improved formulations addressing dispersion, thermal performance, and stability broaden application potential across complex extrusion and molding processes, supporting sustained growth in the segment.

Application Insights

Pipe & fitting extracts are poised to dominate, with a forecast market share of over 40% in 2026, driven by infrastructure investment and urban utility expansion. The segment’s growth is driven by rising demand for reliable water distribution, sanitation, and industrial fluid-handling systems. High-volume extrusion requires consistent melt strength and fusion stability, making processing aids critical to achieving defect-free, uniform products. PVC’s durability, chemical resistance, and cost-effectiveness reinforce its preference in public and private sector projects. Standardized formulations, mandated by regulatory and public procurement guidelines, further institutionalize the use of additives, ensuring quality compliance and operational efficiency across large-scale pipeline and fittings production.

Rigid sheets & panels are estimated to be the fastest-growing segment from 2026 to 2033, fueled by growth in construction interiors, signage, and industrial enclosures. The segment benefits from an increasing emphasis on aesthetic quality, dimensional precision, and surface finish, with processing aids enhancing performance during extrusion and calendering. Expansion of digital commerce channels enables wider distribution of sheets and panels, stimulating demand across residential, commercial, and industrial applications. Advancements in additive formulations enhance clarity, gloss, and thermal stability, enabling customization for decorative and functional applications.

End-User Insights

Building & construction is likely to be the leading segment, accounting for 50% of the PVC processing aids market share in 2026, driven by extensive PVC use in structural and utility applications. Widespread use in piping, window profiles, roofing, and interior paneling ensures steady material consumption. Contractors and developers prioritize consistent product quality, dimensional stability, and reduced installation defects, leading to increased reliance on processing aids.

Long-term public infrastructure funding and urban development projects provide visibility into demand patterns. Standardizing PVC formulations in construction projects, coupled with regulatory compliance requirements, reinforces additive use while enabling manufacturers to maintain operational efficiency and meet large-scale project timelines.

Electrical & electronics are anticipated to be the fastest-growing segment from 2026 to 2033, fueled by electrification initiatives and insulation performance requirements. Processing aids play a critical role in ensuring smooth extrusion, uniform wall thickness, and surface integrity for cables, wires, and conduit systems. Dimensional precision is essential for safety, regulatory compliance, and performance reliability, making additive selection a key operational consideration.

Advanced manufacturing technologies, including automated extrusion lines and precision cooling systems, enhance adoption rates. Increasing demand for energy-efficient buildings, smart grids, and industrial electrical solutions further drives growth, as manufacturers invest in high-performance formulations to meet evolving insulation and aesthetic requirements.

Regional Insights

North America PVC Processing Aids Market Trends

North America is anticipated to maintain a stable market position, with the United States contributing significantly through a well-entrenched innovation ecosystem. The regional market is driven by a strong industrial base and extensive construction and infrastructure activities. High adoption is driven by the need for consistent product quality, dimensional accuracy, and surface finish in large-scale production of piping, conduit, and panels. Strict building codes, fire safety standards, and environmental regulations necessitate the use of advanced additives that improve thermal stability, fusion consistency, and defect reduction.

Established chemical manufacturing capabilities, coupled with efficient supply and distribution networks, enable rapid deployment of specialized processing solutions. Demand from electrical, automotive, and high-value construction applications reinforces reliance on processing aids to maintain operational efficiency and product reliability, while long-standing technical expertise supports the adoption of innovative formulations. Growth is supported by increasing industrial automation, modernization of manufacturing facilities, and emphasis on sustainable production practices.

Additives that enhance melt strength, dispersion, and surface aesthetics facilitate the production of premium PVC products that meet performance and compliance standards. Rising demand for energy-efficient buildings, advanced electrical systems, and durable infrastructure components is accelerating the utilization of processing aids. Investment in research-driven formulations that prioritize eco-efficiency and recyclability enhances competitiveness and product differentiation. The integration of digital manufacturing practices and precision extrusion technologies further improves processing consistency and operational efficiency.

Europe PVC Processing Aids Market Trends

The European market is projected to experience steady expansion through 2033, supported by increasing focus on sustainable manufacturing and regulatory compliance. High-performance processing aids enhance dimensional stability, surface finish, and thermal resilience, enabling the production of PVC products that meet strict fire, chemical, and environmental standards. Demand from construction, automotive, and electrical applications ensures consistent consumption, while established chemical production and distribution networks allow efficient supply of tailored solutions.

Advanced formulations improve dispersion, reduce defects, and extend product shelf life, thereby reinforcing operational efficiency and supporting long-term market stability. Growth during this period is driven by investment in energy-efficient infrastructure, industrial modernization, and electrical mobility initiatives. The adoption of additives that optimize melt strength, fusion consistency, and processing flexibility enables manufacturers to deliver high-quality panels, piping, and conduit systems that comply with strict performance criteria.

Digitalized manufacturing, automation, and precision extrusion technologies further enhance production efficiency and product quality. An emphasis on circular-economy practices and recyclability encourages the integration of eco-efficient additives, thereby providing competitive differentiation.

Asia Pacific PVC Processing Aids Market Trends

Asia-Pacific is expected to dominate the PVC processing aids market, with an estimated 50% share in 2026, driven by high-volume manufacturing in the construction, automotive, and electrical sectors that demand consistent product quality and operational efficiency. Dominance is anchored in extensive infrastructure programs, including urban transport systems, water distribution networks, and industrial facility expansions, creating predictable demand for processing solutions.

Integration of advanced manufacturing technologies and automation enhances melt strength, surface finish, and dimensional accuracy across large-scale extrusion and molding operations. Established chemical production hubs and supply chains enable cost-efficient distribution, while regulatory frameworks emphasizing safety, performance, and environmental compliance reinforce the adoption of advanced additives. Asia-Pacific is projected to be the fastest-growing market for PVC processing aids between 2026 and 2033, driven by industrial modernization, the rising adoption of performance-focused formulations, and the expansion of high-value PVC applications.

Growth is driven by demand for electrical insulation, automotive interiors, and decorative panels, where surface clarity, gloss, and dimensional precision are critical. Investment in research-driven additives improving thermal stability, dispersion, and fusion consistency supports entry into premium PVC segments. Urbanization, digitalized construction practices, and industrial automation accelerate adoption, while supportive trade and investment policies facilitate integration of global best practices, collectively sustaining rapid market expansion.

Competitive Landscape

The global PVC processing aids market structure reflects moderate fragmentation, with several multinational chemical companies collectively holding an estimated share exceeding one-third. Key players, including Arkema, Dow, ANEKA Belgium NV, Evonik Industries, BASF, and Mitsubishi Chemical Group Corporation, leverage extensive technical expertise and established research pipelines to maintain competitive positioning. Focus on formulation innovation allows these companies to develop additives that enhance melt strength, thermal stability, surface finish, and process efficiency across diverse PVC applications.

Regulatory compliance remains a critical differentiator, as adherence to environmental, safety, and performance standards enables seamless market entry and long-term customer trust. Competitive dynamics also center on the ability to provide tailored solutions for emerging high-value applications, such as electrical insulation, automotive interiors, and premium construction panels. Investment in research and development drives continuous improvement in additive performance, addressing challenges such as VOC reduction, recyclability, and energy-efficient processing.

Collaborations with equipment manufacturers and supply chain partners further enhance product compatibility and application versatility. The market’s moderate fragmentation presents opportunities for mid-sized firms to capture niche segments through technical specialization or regional focus, while leading multinationals consolidate advantages through scale, reputation, and innovation.

Key Industry Developments

- In January 2026, Palmer Holland entered into a North American distribution partnership with Kaneka to represent Kaneka’s Kane Ace Modifiers, Kane Ace MX, CPVC, and MS polymers, thereby expanding market access for engineered resin additives and processing aids.

- In January 2026, Wuxi Jubang Auxiliary exported 26 tons of high-performance PVC processing aids to Saudi Arabia, marking an expansion of its global supply efforts and support for the infrastructure and manufacturing sectors that require advanced additives to improve processing performance and product quality.

- In December 2025, Arkema divested its PVC impact modifiers and processing aids businesses to Indian specialty chemicals group Praana as part of a strategic portfolio refocus, transferring global operations for key copolymer additives used in PVC extrusion and molding while retaining certain U.S. assets and facilities.

Frequently Asked Questions

The global PVC processing aids market is projected to reach US$ 1.1 billion in 2026.

Rising demand for high-quality PVC products, industrial automation, and infrastructure expansion are driving the market.

The market is poised to witness a CAGR of 4.5% from 2026 to 2033.

Growing adoption of sustainability-oriented processing solutions and high-performance additives presents key market opportunities.

Some of the key market players include Arkema, Dow, ANEKA Belgium NV, Evonik Industries, BASF, and Mitsubishi Chemical Group Corporation.