- Sensors & Controls

- Position Sensor Market

Position Sensor Market Size, Share, and Growth Forecast, 2026 – 2033

Position Sensor Market by Sensor Type (Linear Position Sensors, Rotary Position Sensors, Proximity / Discrete Position Sensors, Others), Technology (Resistive, Capacitive, Optical, Inductive, Ultrasonic, Magnetic, Others), Output, Industry, and Regional Analysis for 2026 – 2033

Position Sensor Market Size and Trends

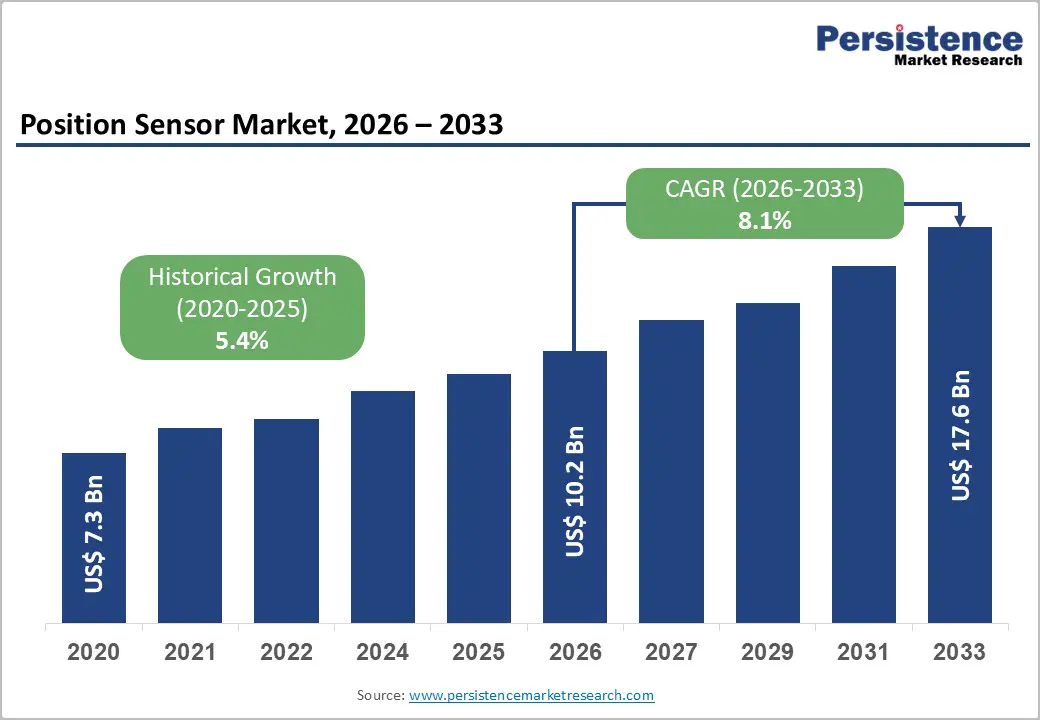

The global position sensor market size is projected to rise from US$10.2 Bn in 2026 to US$17.6 Bn by 2033. It is anticipated to witness a CAGR of 8.1% during the forecast period from 2026 to 2033, driven by the accelerating electrification of vehicles, which requires precise motor and battery position monitoring, combined with the widespread adoption of Industry 4.0 technologies that mandate real-time sensing and predictive maintenance capabilities. These dual trends have created structural demand for advanced position-sensing solutions across automotive, industrial manufacturing, aerospace, and healthcare sectors globally.

Key Industry Highlights:

- Leading Sensor Type: Proximity / Discrete Position Sensors dominate with over 30% market share in 2026, valued at more than US$ 3.1 Bn, driven by high-volume industrial automation needs for reliable object detection, safety interlocks, and process control. Linear position sensors are the fastest-growing segment due to increasing demand for precision control in robotics, CNC machines, industrial actuators, and electric vehicles.

- Leading Technology: Magnetic sensors lead the market with over 27% share in 2026, valued at more than US$ 2.8 Bn, due to their durability in harsh environments and reliable non-contact operation. Optical sensors are the fastest-growing technology, expanding at a CAGR of 11.8%, driven by superior accuracy, high resolution, and long-distance measurement capability for precision applications.

- Leading Output: Analog output holds over 42% market share in 2026, valued at more than US$ 4.3 Bn, due to its simple integration and cost-effectiveness in mass-produced industrial and automotive systems. Digital output is the fastest-growing segment, driven by increasing demand for real-time data integration, noise immunity, and direct connectivity with PLCs and IoT platforms.

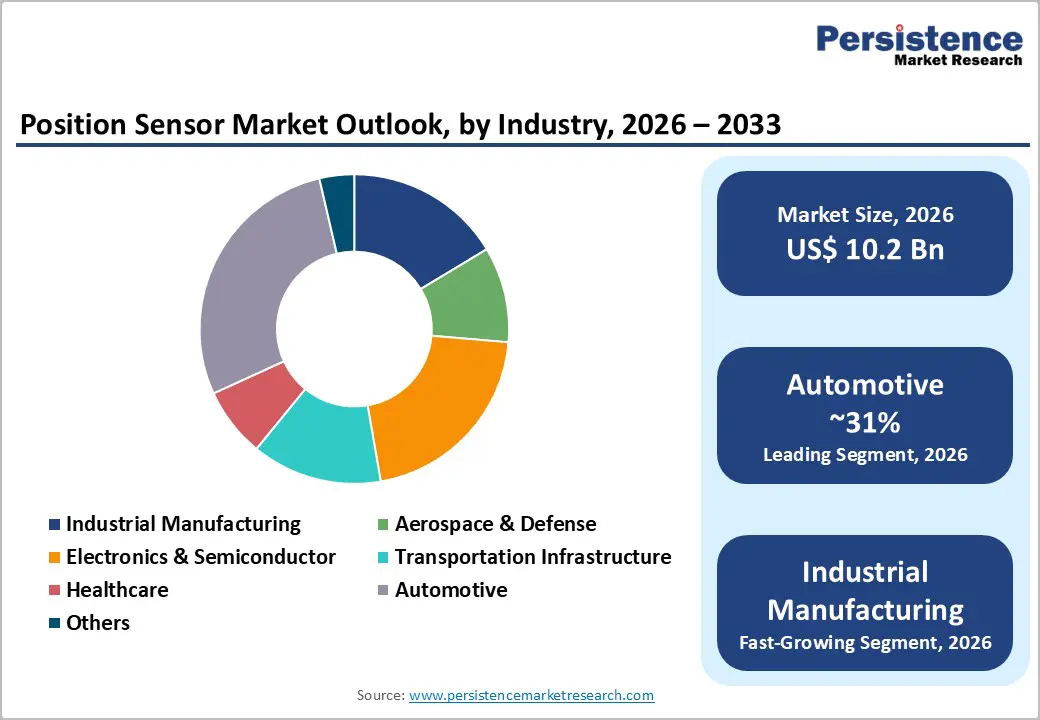

- Leading Industry: Automotive commands the largest share at over 31% in 2026, valued at more than US$ 3.2 Bn, driven by electrification, ADAS, and stringent safety requirements. Industrial manufacturing is the fastest-growing industry due to Industry 4.0 adoption, robotics integration, and rising demand for predictive maintenance and automation.

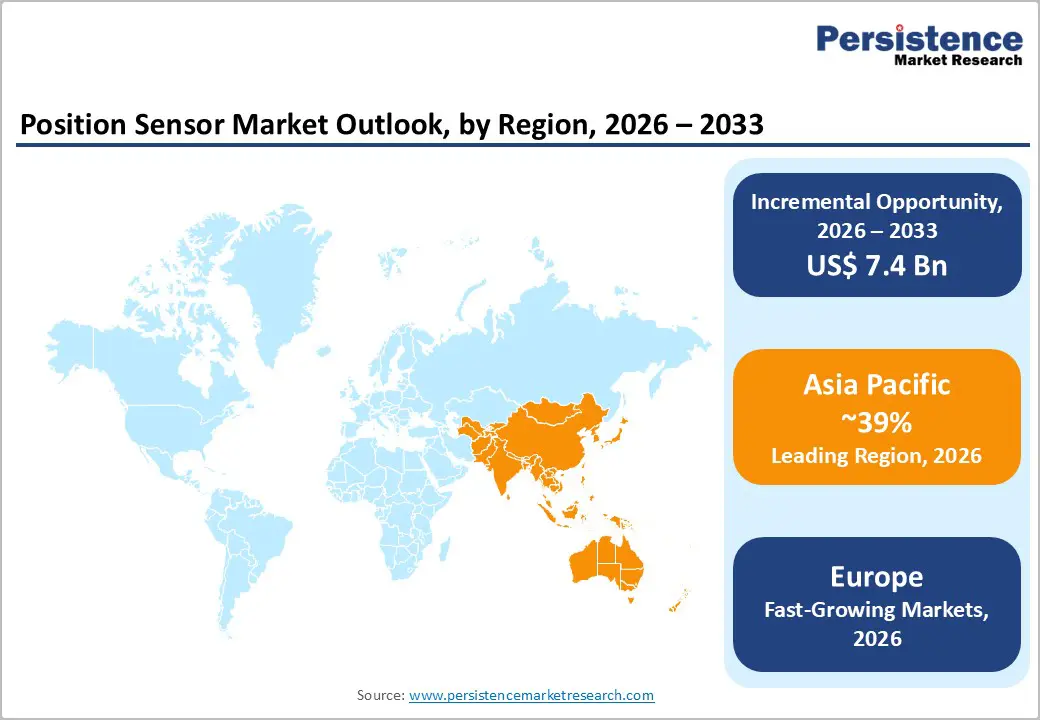

- Leading Region: Asia Pacific leads the market with over 39% share by 2026, supported by massive automotive production, industrialization, and consumer electronics manufacturing. North America holds over 25% share, driven by strong OEM presence, strict safety standards, and advanced manufacturing ecosystems. Europe captures over 21% share, supported by strong industrial automation adoption and EV development.

| Report Attribute | Details |

|---|---|

|

Position Sensor Market Size (2026E) |

US$10.2 Bn |

|

Market Value Forecast (2033F) |

US$17.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.4% |

Market Dynamics

Driver

Automotive Electrification Driving Position Sensor Demand

The global shift toward electric vehicles (EVs) is a major growth driver, as electrified propulsion systems rely heavily on accurate position feedback for safe and efficient operation. EVs require multiple position sensing applications, including rotor position detection in electric motors, throttle and pedal position monitoring, steering angle measurement, and battery management system feedback. As vehicle architectures evolve, magnetic and inductive position sensors have become indispensable for critical systems such as steer-by-wire and active suspension, where precise control is essential for stability, comfort, and energy efficiency. The high accuracy requirement, e.g., ±0.3° over the full 360° ranges supports improved motor control and optimized power usage in battery-powered vehicles.

Industry 4.0 Digital Transformation and Predictive Maintenance Integration

Smart manufacturing environments require IO-Link-enabled position sensors that support bidirectional communication, allowing real-time transmission of operational parameters and diagnostic data for predictive maintenance. By combining position sensing with edge computing, manufacturers detect anomalies early and reduce downtime by up to 20-30% through proactive fault prediction and maintenance scheduling. The integration of sensor networks across motion control, vibration monitoring, and asset tracking is becoming essential for modern production lines. Advanced manufacturers in Europe, North America, and East Asia are leading this trend, while global investments in industrial automation continue to expand sensor deployment across conveyor systems, robotics, and various production equipment.

Restraint

High Integration Complexity and Electromagnetic Interference Sensitivity

Position sensors, especially inductive and magnetic types, face significant integration complexity in industrial and automotive settings due to dense electromagnetic environments. These sensors are highly sensitive to temperature variations and electromagnetic interference from nearby high-power components, which cause signal distortion, drift, and reduced accuracy. To maintain reliable performance, additional shielding, filtering, and frequent calibration are often required, increasing overall system costs. Designers also struggle with hysteresis effects and sensor drift across wide thermal cycles –40°C to 125°C, necessitating advanced compensation techniques. These factors complicate miniaturization and require sophisticated signal processing circuitry, further adding to design complexity and expense.

Competition from Alternative Sensing Technologies and Cost Pressures

Position sensing technologies are facing growing substitution pressure from alternative solutions such as optical encoders, laser displacement sensors, and 3D time-of-flight systems, which often provide higher resolution and lower maintenance in specific applications. The widespread availability of low-cost magnetic and Hall effect sensors has intensified price competition, compressing profit margins for traditional position sensor manufacturers, especially in cost-sensitive segments like consumer electronics and tier-2 automotive suppliers. Semiconductor firms are increasingly focusing R&D and production on high-volume MEMS sensors for smartphones and wearables, leading to supply constraints for niche automotive and industrial position sensing needs. This shift also limits innovation in specialized position sensor designs, slowing the development of advanced solutions.

Opportunity

Aerospace and Defense Sector Expansion Through Next-Generation Aircraft Programs

The aerospace and defense sector offers strong growth potential for the position sensor market as next-generation aircraft programs and fleet modernization initiatives demand highly reliable sensing solutions. Position sensors are critical for flight safety and performance, providing precise feedback for control surfaces, landing gear status, and thrust vector control. Programs such as COMAC C919, Airbus A350, and a wide range of UAVs are driving demand for miniaturized sensors that withstand extreme temperatures, high vibration, and high-altitude conditions. Defense modernization budgets in the United States, Europe, and Indo-Pacific nations are accelerating upgrades of military aviation platforms with advanced avionics and autonomous flight capabilities.

?Healthcare and Medical Device Integration Through Remote Patient Monitoring

Healthcare is emerging as a major growth area, as these sensors enable advanced functionalities in critical medical devices such as infusion pumps, ventilators, adjustable beds, anesthesia machines, and surgical robots. Integration with wearables and IoT health platforms allows continuous remote patient monitoring, real-time data capture, and predictive diagnostics. Medical device manufacturers are increasingly adopting AMR (anisotropic magnetoresistive) sensors due to their higher sensitivity compared to reed switches, allowing smaller magnets and lower power consumption essential for portable, battery-powered equipment. The shift toward connected medical systems and smart diagnostics, supported by growing investments in healthcare infrastructure, is accelerating demand for reliable, miniaturized position sensors.

Category-wise Analysis

Sensor Type Analysis,

Proximity / discrete position sensors dominate the global market, capturing more than 30% market share in 2026 with a value exceeding US$ 3.1 Bn, as they directly meet widespread industrial needs for simple, reliable detection of object presence and position. They are essential for automation, safety interlocks, and process control in manufacturing lines where binary (on/off) feedback is critical. Their robustness, cost-effectiveness, and ease of integration across diverse machinery make them the preferred choice for high-volume applications. The growing demand for smart factories and robotics implementations further boosts their adoption.

Linear position sensors demonstrate significant growth as many industries are increasingly moving toward automation and precision control, where accurate linear measurement is essential. They are widely needed in robotics, CNC machines, industrial actuators, and electric vehicles for reliable feedback on motion and positioning. The rise in smart manufacturing and Industry 4.0 drives demand for sensors that deliver real-time, high-accuracy data for process optimization. Their strong compatibility with digital control systems and the ability to support predictive maintenance further boosts adoption across sectors.

Technology Analysis,

Magnetic dominates the market, capturing over 27% market share in 2026 with a value exceeding US$ 2.8 Bn, due to the reliable detection of position and movement without mechanical contact, which reduces wear and maintenance. They perform well in harsh environments with dust, moisture, and vibration, meeting industrial and automotive durability needs. Their ability to offer precise, real-time feedback supports safety and control systems. Magnetic technologies are cost-effective to integrate at scale, aligning with broad adoption requirements across sectors.

Optical demonstrates the highest growth with a CAGR of 11.8% due to delivering exceptional accuracy and repeatability, which is critical for precision applications. Their non-contact operation reduces wear and maintenance needs, making them ideal for high-speed and high-duty-cycle environments. Optical sensors support high-resolution measurement over long distances, enabling advanced motion control and safety systems.

Output Analysis,

Analog holds over 42% of the market share in 2026, with a value exceeding US$ 4.3 Bn, as they offer simple, reliable, and cost-effective measurements, which are essential for mass-produced industrial and automotive applications. They provide continuous real-time output without complex digital processing, meeting the need for quick and accurate feedback in motion control systems. Analog sensors deliver continuous voltage or current outputs proportional to position displacement, enabling simple integration with existing analog control electronics and reducing system complexity in non-networked applications.

Digital is expected to grow at the highest rate as industries increasingly demand real-time, precise, and easily integrated positional data for automation and safety-critical applications. Digital sensors offer better noise immunity and higher accuracy, which is essential for robotics, industrial automation, and electric vehicles. Their ability to directly communicate with PLCs, microcontrollers, and IoT platforms reduces the need for additional signal conditioning and improves system reliability.

Industry Analysis,

Automotive commands the largest market share at over 31% in 2026, with a value exceeding US$ 3.2 Bn, due to modern vehicles increasingly relying on accurate position sensing for safety, efficiency, and automation. Position sensors are essential for advanced driver-assistance systems (ADAS), electric power steering, transmission control, and throttle control, where precise motion and position data are critical. The growth of EVs also drives demand for sensors in battery management, motor control, and regenerative braking systems. Stringent safety and emission regulations push automakers to adopt more sensors to enhance performance, reliability, and fuel efficiency.

Industrial manufacturing is expected to grow at a significant rate due to modern factories increasingly shifting toward automation and smart manufacturing, where accurate position feedback is essential for robotics, CNC machines, and automated guided vehicles (AGVs). Position sensors enable precise motion control, reducing errors and improving product quality, especially in high-speed production lines. As manufacturers adopt Industry 4.0 and IIoT, real-time monitoring of machine position becomes critical for predictive maintenance and minimizing downtime. Rising demand for customized and flexible production requires adaptable positioning systems, driving more sensor integration across manufacturing equipment.

Regional Insights

North America Position Sensor Market Trends

North America accounts for over 25% of the market share in 2026, reaching approximately US$ 2.6 Bn, driven by its role as a global technology hub and the presence of major automotive OEMs across the U.S. and Canada. Strict functional safety frameworks, including ISO 26262 for automotive and IEC 61508 for industrial systems, sustain demand for certified, high-reliability position sensors. Advanced manufacturing ecosystems, large-scale investments in autonomous and electric vehicles, and strong aerospace and defense activity in states such as California, Michigan, Washington, and Arizona further support market growth. U.S. OEMs are increasingly deploying position sensors in EV battery management and powertrain systems, while AI and edge computing adoption is accelerating demand for smart sensors with embedded diagnostics.

Asia Pacific Position Sensor Market Trends

Asia Pacific dominates the global market, accounting for a share of over 39% by 2026, and is expected to grow at the highest rate with a CAGR of 13.1%, due to massive automotive production capacity, rapid industrialization, and dense consumer electronics manufacturing across China, Japan, South Korea, India, and Southeast Asia. China alone dominates the region, supported by its leadership in electric vehicle manufacturing and emerging autonomous vehicle platforms. The region benefits from vertically integrated automotive supply chains, economies of scale in sensor manufacturing, and government-led Industry 4.0 and smart factory initiatives. Japan contributes premium high-precision positioning solutions through established sensor technology firms, while India is the fastest-growing market with rising manufacturing investments and expanding automotive and electronics assembly.

Europe Position Sensor Market Trends

Europe is expected to hold more than 21% share by 2026, driven by stringent environmental regulations, Industry 4.0 adoption, and leadership in autonomous and electric vehicle development. Germany anchors regional demand, supported by automotive and industrial giants driving usage across EV powertrains, ADAS, and precision machinery. The UK, France, Spain, and Benelux contribute through aerospace, medical devices, and industrial automation applications. European OEMs emphasize high reliability and durability, favoring premium suppliers like TE Connectivity and Infineon Technologies. Capacitive position sensors are growing, driven by automotive safety mandates, electrification, and advanced motor and battery management systems.

Competitive Landscape

The position sensor market is moderately fragmented, with a mix of global automation leaders and specialized sensor manufacturers competing across industries. Manufacturers focus on product differentiation through higher accuracy, miniaturization, and multi-axis sensing to address robotics, automotive, and industrial automation needs. Strategic partnerships with OEMs and system integrators help embed sensors early in equipment design, strengthening long-term demand. Companies also pursue cost-competitive manufacturing and regional expansion, particularly in the Asia-Pacific, while investing in smart and IoT-enabled sensors to maintain technological leadership.

Key Industry Developments

- In September 2025, TDK Corporation launched a joint research project with ASICS to analyze and visualize athletes’ movements using high-precision motion and position sensing technology. By combining TDK’s sensor expertise with ASICS’s sports engineering capabilities, the collaboration aims to enhance athlete performance and support the development of advanced sports shoes and training tools.

- In July 2025, STMicroelectronics agreed to acquire NXP Semiconductors’ MEMS sensors business for up to US$950 million in cash, strengthening its position in automotive and industrial sensors. The deal, expected to close in H1 2026, will expand ST’s MEMS technology portfolio and is projected to be earnings-per-share accretive, supported by NXP’s ~US$300 million MEMS revenue base in 2024.

Companies Covered in Position Sensor Market

- TE Connectivity

- Honeywell International Inc.

- Sensata Technologies, Inc.

- STMicroelectronics N.V.

- TDK Corporation

- Keyence Corporation

- Texas Instruments Inc.

- Infineon Technologies AG

- Bourns, Inc.

- Althen Sensors

- Gill Sensors & Controls Limited

- Positek Limited

- Others

Frequently Asked Questions

The global market is projected to be valued at US$10.2 Bn in 2026.

The growing need for precise motion and position feedback to enable automation, safety, and efficiency is a key driver of the market.

The market is expected to witness a CAGR of 8.1% from 2026 to 2033.

The expanding adoption of robotics, along with the rising demand for high-accuracy, contactless position sensing creating strong market expansion potential.

TE Connectivity, Honeywell International Inc., Sensata Technologies, Inc., STMicroelectronics N.V., TDK Corporation, Keyence Corporation are among the leading key players.