- Medical Devices

- Repositioning and Offloading Devices Market

Repositioning and Offloading Devices Market Size, Share, and Growth Forecast 2026 - 2033

Repositioning and Offloading Devices Market by Product (Repositioning devices, Offloading devices), by Device Category (Repositioning sheets & slings, Cushions & mattresses, Offloading boots & walkers, Heel & elbow protectors), by Application (Pressure ulcer prevention, Wound care, Post-surgical care, Rehabilitation), by Regional Analysis, 2026-2033.

Repositioning and Offloading Devices Market Size and Trends Analysis

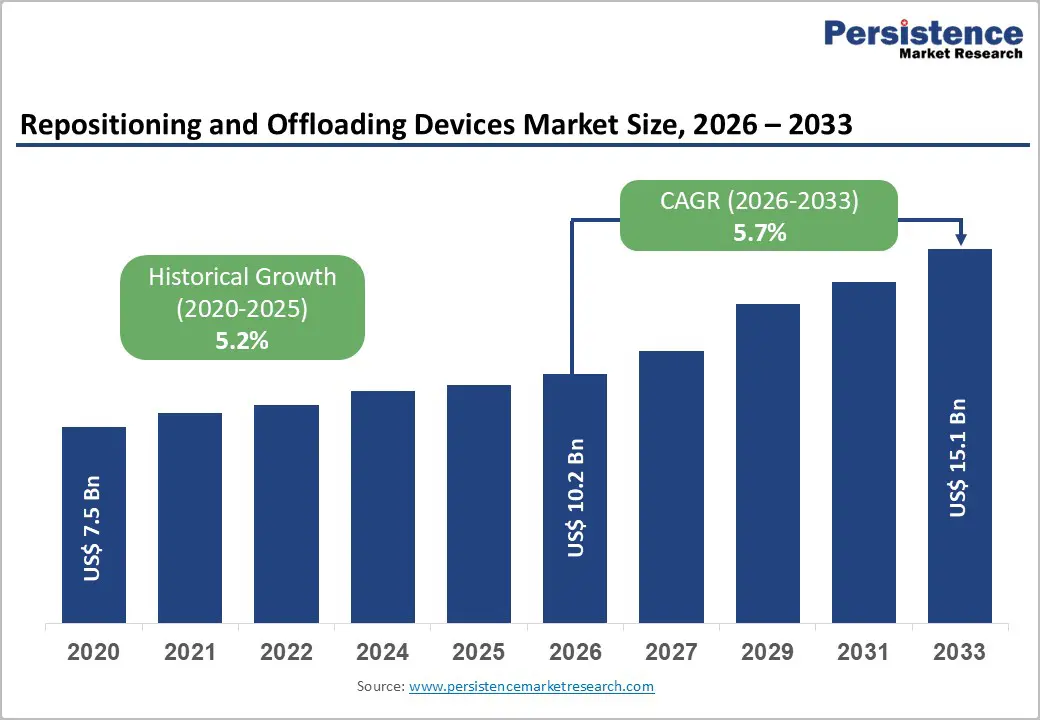

The global Repositioning and Offloading Devices market size is expected to be valued at US$ 10.2 billion in 2026 and projected to reach US$ 15.1 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

The market expansion is driven by the escalating prevalence of chronic diseases such as diabetes and obesity, an aging global population, and heightened awareness among healthcare professionals regarding pressure ulcer prevention and patient comfort. According to the United Nations, the global population aged 60 years and above is expected to more than double by 2050, significantly increasing the demand for repositioning and offloading devices in hospitals, long-term care facilities, and home care environments. Additionally, the Centers for Disease Control and Prevention (CDC) reports that more than 37 million Americans were living with diabetes in 2023, with approximately 1 in 5 unaware of their condition, creating substantial demand for offloading solutions in diabetic foot ulcer management and broader wound care applications. Technological advancements in device design, including pressure-relief systems and materials engineered for comfort, continue to enhance market penetration across acute care, rehabilitation, and homecare settings.

Key Market Highlights

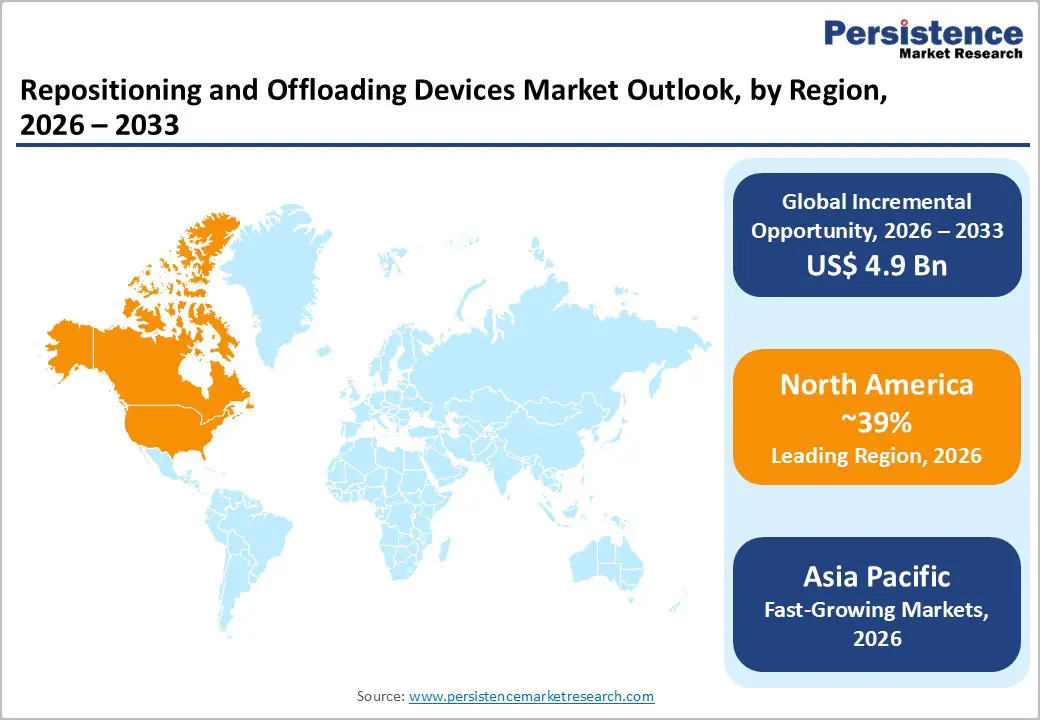

- North America leads the Repositioning and Offloading Devices market with about 39% share in 2025, supported by advanced hospital infrastructure, strong reimbursement frameworks, and stringent quality metrics that prioritize pressure injury prevention across care settings in the U.S. and Canada.

- Asia Pacific is the fastest-growing region, driven by surging diabetes incidence exceeding 215 million adults in China and India, rapid hospital and long-term care expansion, and cost-competitive manufacturing capabilities that support broader device access across emerging healthcare systems.

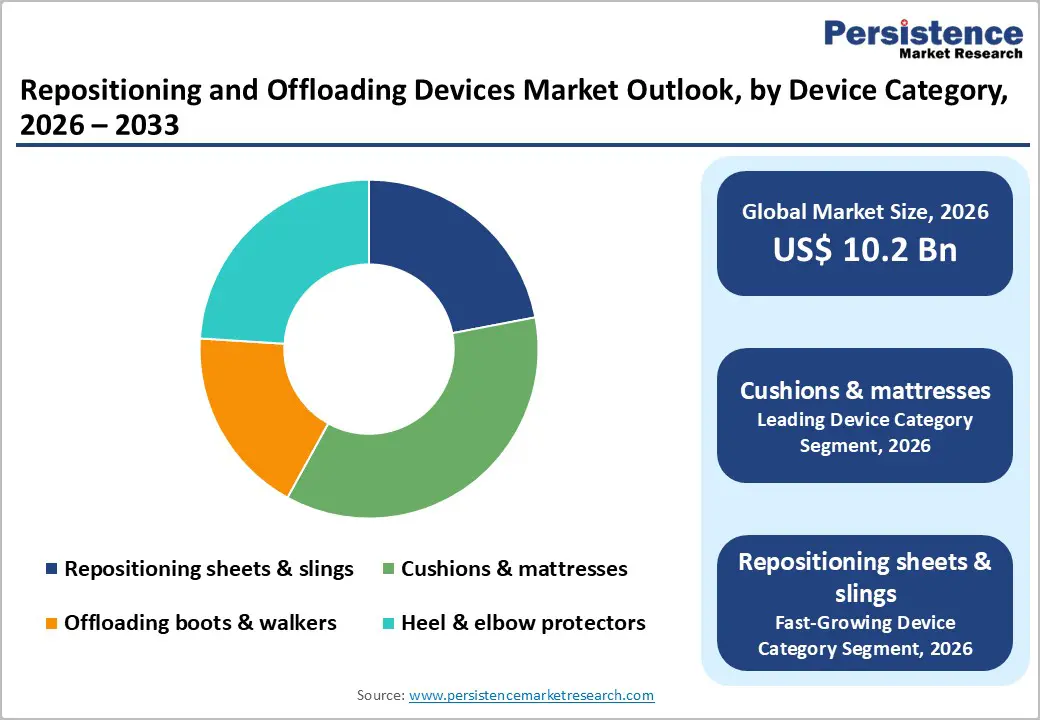

- Cushions and mattresses form the dominant device category with around 36% share in 2025, owing to their universal use as baseline prevention tools in hospitals, nursing homes, and homecare, reinforced by guideline recommendations and reimbursement recognition as medically necessary support surfaces.

- Repositioning sheets and slings are among the fastest-growing categories as safe patient-handling policies strengthen, with hospitals investing in ergonomic solutions that reduce caregiver injuries, improve repositioning compliance, and support integrated pressure ulcer prevention strategies.

| Global Market Attributes | Key Insights |

|---|---|

| Repositioning and Offloading Devices Size (2026E) | US$ 10.2 billion |

| Market Value Forecast (2033F) | US$ 15.1 billion |

| Projected Growth CAGR(2026-2033) | 5.7% |

| Historical Market Growth (2020-2025) | 5.2% |

Market Growth Drivers

Rising geriatric population and chronic disease prevalence

The rapid expansion of the global geriatric population is a fundamental driver for repositioning and offloading devices, as older adults face disproportionately high risk of pressure injuries due to reduced mobility, frailty, and multiple comorbidities. The United Nations estimates that people aged 65 years and above will account for nearly 1 in 6 individuals globally by 2050, sharply increasing the pool of patients requiring long-term care and continuous pressure management. In parallel, chronic conditions such as diabetes, cardiovascular diseases, and neurological disorders are rising, with the International Diabetes Federation (IDF) indicating that 537 million adults worldwide were living with diabetes in 2021, a figure projected to reach 643 million by 2030. These patients have elevated risk of pressure ulcers and diabetic foot ulcers, necessitating consistent use of offloading boots, special mattresses, and repositioning supports. Hospitals and long-term care facilities increasingly adopt structured pressure ulcer prevention bundles, placing repositioning and offloading devices at the core of evidence-based protocols, thereby sustaining steady demand growth.

Technological advancements and innovation in device design

Technological innovation is significantly enhancing the clinical performance and adoption of repositioning and offloading devices, boosting both patient outcomes and caregiver efficiency. Modern systems incorporate multi-layer foam, dynamic air-cell mattresses, gel cushions, and specialized ergonomic designs that more effectively redistribute pressure and minimize shear and friction forces implicated in pressure ulcer development. Clinical guidelines from bodies such as the European Pressure Ulcer Advisory Panel (EPUAP) and National Pressure Injury Advisory Panel (NPIAP) emphasize the clinical benefits of advanced support surfaces and offloading technologies in both prevention and treatment pathways. In diabetic foot care, offloading technologies such as total contact casting (TCC) and removable walkers have demonstrated significantly higher healing rates for neuropathic ulcers compared with standard footwear in randomized controlled trials, strengthening clinician confidence in device-based interventions. Emerging devices also integrate sensors, AI-enabled monitoring, and connectivity for real-time pressure mapping and compliance tracking, aligning with broader digital health and remote care trends and improving adoption in technologically advanced health systems.

Market Restraints

High cost of advanced devices and reimbursement challenges

Despite strong clinical need, the high acquisition and maintenance costs of advanced repositioning and offloading devices act as a key barrier, particularly in resource-constrained settings. Dynamic air mattresses, smart sensor-based systems, and sophisticated offloading walkers are significantly more expensive than conventional foam mattresses or simple supports, straining budgets of public hospitals and long-term care facilities in low- and middle-income countries. In many markets, reimbursement frameworks provide partial or restricted coverage for these devices, often prioritizing treatment of established ulcers over preventive technologies, which delays adoption in earlier stages of patient risk. Where reimbursement exists, documentation requirements and administrative burden can also discourage routine prescribing in outpatient and homecare contexts. Consequently, providers may default to basic repositioning practices and low-cost surfaces despite evidence that advanced systems can reduce ulcer incidence and overall care costs, limiting full market potential.

Limited awareness and inconsistent implementation of prevention protocols

Another important restraint is the variability in awareness and implementation of standardized pressure ulcer prevention protocols among healthcare professionals and institutions. Studies from acute care and intensive care units show that medical device-related pressure ulcers (MDRPUs) can represent over 30% of all pressure injuries, yet many staff members lack specific training on appropriate offloading and repositioning practices for device-prone areas such as heels, occiput, and ears. Research from European and Middle Eastern hospitals indicates gaps in nurses’ knowledge regarding MDRPU risk factors, documentation, and evidence-based prevention strategies, resulting in suboptimal use of specialized supports and cushions. Furthermore, adherence to repositioning schedules (for example, turning patients every 2 hours) is often inconsistent due to workload and staffing constraints, undermining the effectiveness of available technologies. These gaps reduce the realized clinical benefits of devices and slow institutional investment, especially where procurement budgets are tightly scrutinized.

Market Opportunities

Expansion in post-surgical care and rehabilitation settings

Rising surgical volumes across orthopedics, cardiovascular procedures, oncology, and trauma care create substantial opportunity for repositioning and offloading devices in post-surgical and rehabilitation pathways. Patients undergoing joint replacements, spinal surgeries, and complex abdominal procedures often experience limited mobility and elevated pain levels, increasing their vulnerability to pressure injuries and positioning-related complications during recovery. Advanced support surfaces, heel protectors, and positioning wedges help maintain proper alignment, reduce localized pressure, and support early mobilization in both inpatient and rehabilitation center environments. Additionally, the global shift toward shorter hospital stays and expansion of outpatient surgery centers demands portable, user-friendly offloading solutions that patients can use at home after discharge. Devices tailored for home rehabilitation, such as lightweight offloading walkers and modular cushions, offer manufacturers opportunities to expand beyond institutional channels and tap into the growing homecare and tele-rehabilitation ecosystem.

Smart devices, connectivity, and remote monitoring

Integration of repositioning and offloading devices with digital health, IoT, and AI-based analytics offers a compelling opportunity for differentiation and long-term growth. Sensor-embedded mattresses, cushions, and wearables can continuously monitor pressure distribution, patient position, micro-movements, and moisture levels, transmitting data to centralized dashboards for real-time clinical oversight. Emerging platforms using thermal imaging and AI algorithms to detect early tissue changes are being explored in diabetic foot ulcer care, enabling early intervention before overt skin breakdown occurs. Industry analyses indicate that adoption of connected wound care and pressure management solutions is projected to grow at a double-digit CAGR, with smart systems expected to expand their share of capital purchases in advanced health systems over the coming decade. Remote monitoring is particularly attractive for homecare and long-term care facilities, where clinicians and payers seek to reduce readmissions and emergency visits by identifying risk escalation early. Manufacturers that combine physical devices with software platforms, analytics, and service contracts can build recurring revenue models and strengthen customer retention.

Category-wise Insights

Product Analysis

Within the product spectrum, both repositioning devices and offloading devices play critical and often complementary roles in comprehensive pressure injury prevention strategies. Repositioning devices typically include repositioning sheets, slings, transfer aids, and powered or non-powered surfaces that facilitate safe and frequent patient turning, decreasing sustained pressure and shear forces on bony prominences. Offloading devices focus on selectively unloading high-risk areas such as heels, sacrum, or forefoot—through boots, walkers, offloading shoes, and specialty supports, particularly for diabetic foot ulcers and other localized wounds. Repositioning devices are more ubiquitous across intensive care units, general wards, and long-term care, driven by institutional protocols that structure turning schedules and safe patient-handling practices. Offloading devices, meanwhile, see strong adoption in wound care clinics, diabetic foot centers, and outpatient settings where limb preservation and ulcer healing are primary objectives. Together, these product categories align with guideline-based care bundles and are expected to sustain balanced demand as health systems move toward prevention-focused, multidisciplinary wound care models.

Device Category Analysis

Within device categories, cushions and mattresses constitute the leading segment with about 36% market share in 2025, reflecting their foundational role across nearly all care settings. Support surfaces ranging from high-specification foam mattresses to low-air-loss and alternating pressure systems are often the first-line intervention for patients at risk of pressure injury, supported by strong evidence and clinical guideline recommendations. These devices are employed in hospitals, nursing homes, and homecare, making them one of the most widely adopted categories in the ecosystem. Policy and reimbursement frameworks in regions such as North America and Europe frequently recognize advanced support surfaces as medically necessary equipment for high-risk patients, further reinforcing usage. In addition, continuous innovation in materials (for example, viscoelastic foam, gel, hybrid foam–air designs) and features such as microclimate management, shear reduction, and patient movement assistance enhances comfort and clinical outcomes. The everyday necessity of mattresses and cushions across beds, wheelchairs, and recliners ensures stable baseline demand, while premium feature upgrades generate additional value for manufacturers.

Application Analysis

Pressure ulcer prevention is the dominant application segment for repositioning and offloading devices, reflecting the high clinical and economic burden of pressure injuries across acute and long-term care. Prevalence studies report hospital-acquired pressure injury rates ranging from 5% to over 10% in high-risk units, with associated treatment costs running into tens of thousands of dollars per severe case, driving payers and providers to prioritize prevention strategies. Devices such as high-specification mattresses, heel protectors, and repositioning systems are embedded in prevention bundles alongside risk assessment tools and skin care protocols, making them integral to quality and safety initiatives. Wound care, including diabetic foot ulcers, venous leg ulcers, and complex surgical wounds, represents another critical application, where targeted offloading and precise body positioning materially influence healing trajectories and limb salvage rates. Post-surgical care and rehabilitation also contribute significantly to demand, as immobile post-operative patients and those undergoing intensive rehabilitation require controlled positioning and pressure distribution to avoid complications and facilitate functional recovery. These overlapping applications ensure that devices see usage across the full continuum of care, from intensive care units to outpatient physiotherapy.

Regional Insights

North America Repositioning and Offloading Devices Market Trends

North America is the leading regional market, accounting for about 39% market share in 2025, underpinned by advanced healthcare infrastructure, high per capita healthcare spending, and strong emphasis on quality metrics and patient safety. The United States drives the bulk of regional demand, with the CDC estimating that more than 2.5 million patients develop pressure ulcers annually, contributing to increased length of stay, infection risk, and healthcare costs. Federal agencies and payers have linked reimbursement penalties and quality ratings to hospital-acquired pressure injury incidence, prompting health systems to invest heavily in preventive technologies, including advanced mattresses, repositioning systems, and offloading devices. Robust adoption of electronic health records and clinical decision support tools also facilitates integration of risk-based protocols that trigger device use for patients classified as high risk.

Asia Pacific Repositioning and Offloading Devices Market Trends

Asia Pacific is the fastest-growing region in the Repositioning and Offloading Devices market, with forecast CAGR outpacing global averages between 2026 and 2033, driven by demographic shifts, rapid hospital infrastructure expansion, and rising chronic disease prevalence. China, India, Japan, and ASEAN countries are central to regional demand dynamics, each at different stages of healthcare system maturity but all facing increasing burdens of diabetes and age-related morbidity. The International Diabetes Federation reports that China and India together account for over 215 million adults with diabetes, making diabetic foot disease and pressure ulcer prevention key clinical priorities. As tertiary hospitals and specialist wound care centers proliferate, demand for offloading walkers, heel protectors, and high-grade mattresses is accelerating from a relatively low baseline, generating substantial growth potential.

Competitive Landscape

Market Structure Analysis

The repositioning and offloading devices market is moderately consolidated, with competition centered on product innovation, clinical effectiveness, and ease of use. Manufacturers focus on developing ergonomically designed, pressure-redistribution solutions that reduce caregiver burden and improve patient comfort. Technological advancements such as lightweight materials, modular designs, and smart pressure-monitoring features are strengthening competitive positioning. Pricing, durability, and compliance with hospital safety standards play a key role in purchasing decisions, especially in acute and long-term care settings. Companies are also expanding distribution networks and targeting home-care applications to capture growing demand driven by aging populations and rising awareness of pressure injury prevention.

Key Market Developments

- In May 2025, Frontier Medical Group was honoured with the King’s Award for Enterprise in International Trade, recognizing its significant international growth and global impact through clinically driven pressure area care innovations that were distributed in over 34 countries.

Companies Covered in Repositioning and Offloading Devices Market

- Stryker

- Medline Industries, LP

- Hill-Rom Services, Inc.

- Frontier Medical Group

- Walgreen Health Solutions LLC

- Arjo Group

- Next Health LLC

- Sage Products LLC

- Seneca Devices Inc.

- Guldmann A/S

- Mölnlycke Health Care AB

- Permobil AB

Frequently Asked Questions

The global Repositioning and Offloading Devices market is expected to reach US$ 10.2 billion in 2026.

Key demand drivers include the rapid expansion of the global elderly population, projected to more than double by 2050, and the mounting burden of chronic diseases such as diabetes, which already affects 537 million adults worldwide.

North America is the leading region, with around 39% share in 2025, underpinned by advanced healthcare infrastructure, strong reimbursement for high-specification support surfaces, and stringent quality and reporting frameworks targeting reductions in hospital-acquired pressure injuries.

The most significant opportunity lies in the development of smart, connected repositioning and offloading devices that integrate sensors, IoT connectivity, and AI analytics to enable real-time pressure mapping, early risk detection, and remote monitoring.

Major players include Stryker, Hill-Rom Services, Inc., Medline Industries, LP, Arjo Group, Mölnlycke Health Care AB, Guldmann A/S, and Permobil AB, alongside specialized companies such as Frontier Medical Group, Seneca Devices Inc., and Sage Products LLC.