- Plastics, Polymers & Resins

- Polyethylene Wax Market

Polyethylene Wax Market Size Share, and Growth Forecast, 2025 - 2032

Polyethylene Wax Market By Product Type (Low Density Polyethylene, Others), Processing Method (Polymerization, Others), Application (Coating, Others), and Regional Analysis for 2025 - 2032

Polyethylene Wax Market Size and Trends Analysis

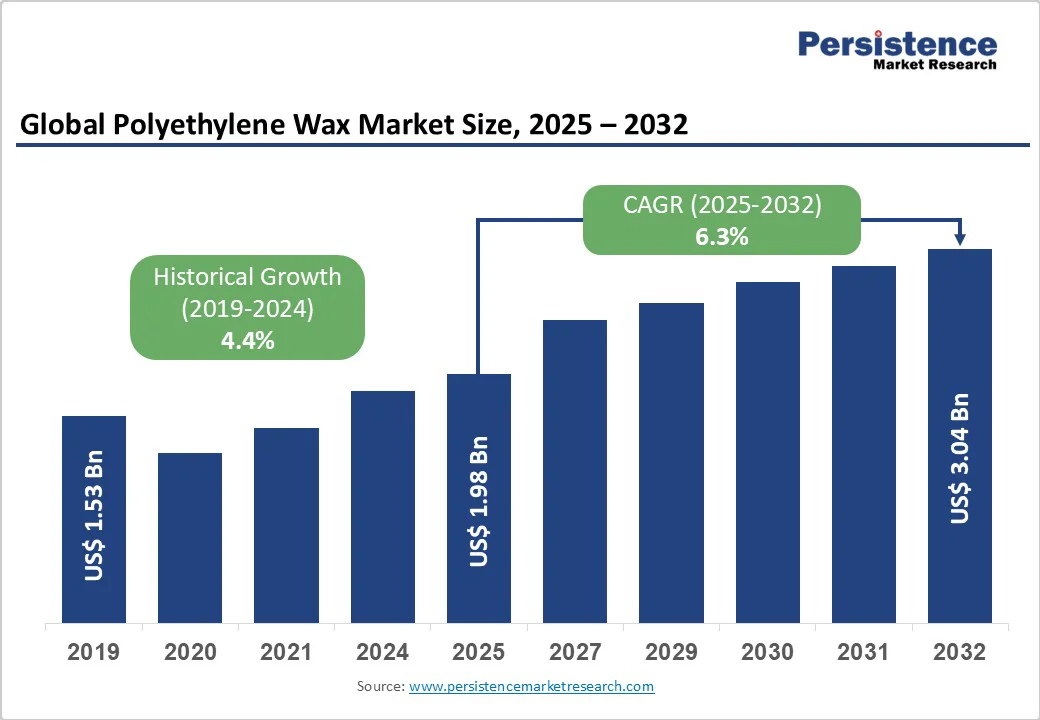

The global polyethylene wax market size was valued at US$1.98 Billion in 2025 and is projected to reach US$3.04 Billion by 2032, growing at a CAGR of 6.3% between 2025 and 2032, driven by rising demand from coatings and printing ink industries.

Technological advancements in processing methods and the increasing adoption across diverse end-use applications support robust growth momentum through enhanced product performance and manufacturing efficiency.

Key Industry Highlights

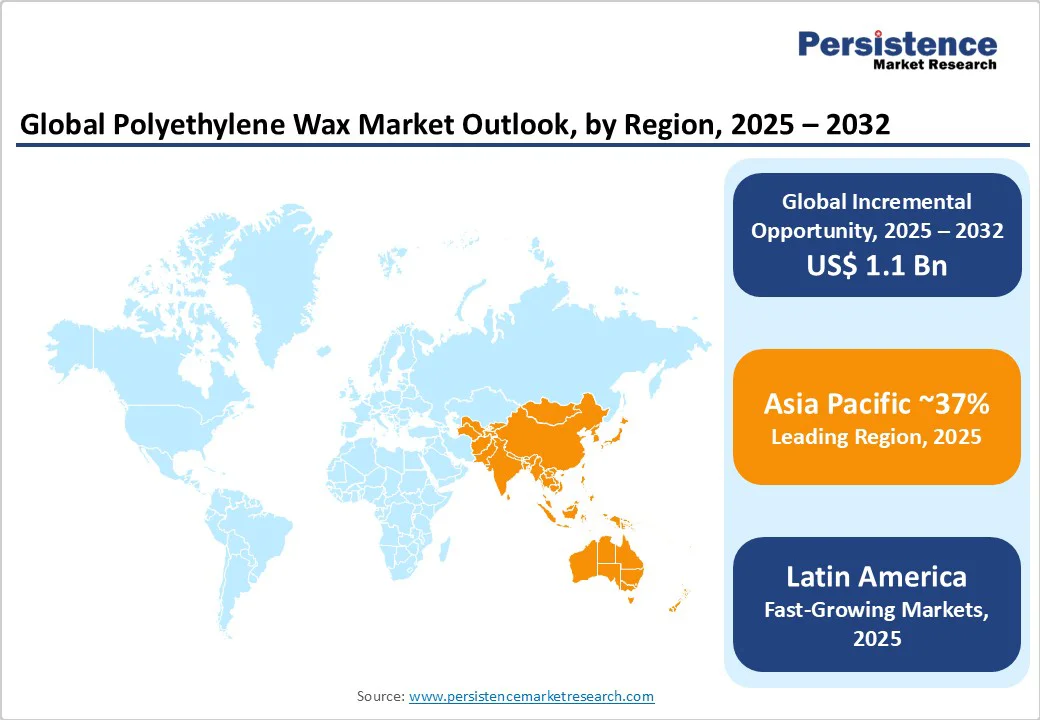

- Regional Leadership: Asia Pacific leads with a 37% market share, North America grows at 6.9% CAGR, and Europe holds 27% amid steady demand and industrial development.

- Product Segments: HDPE wax dominates with 45% share, while oxidized polyethylene grows fastest at 7.3% CAGR, driven by emerging applications.

- Processing Innovation: Chemical modification captures 50% market share, with physical blending accelerating at 7.2% CAGR to meet evolving industry requirements.

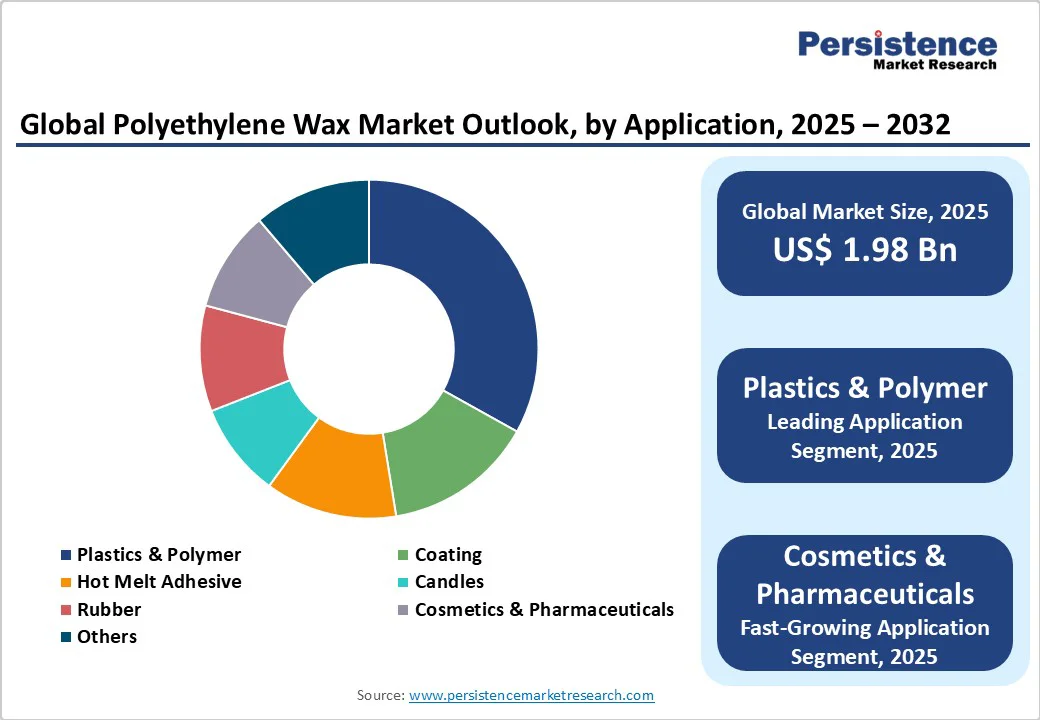

- Application Expansion: Plastics & polymer applications lead with 33% share, while cosmetics and pharmaceuticals grow fastest at 8.4% CAGR amid rising demand for specialty formulations.

- Sustainability Focus: Bio-based alternatives and strict environmental compliance are propelling growth in the premium segment.

- Strategic Consolidation: Industry leaders pursue innovation partnerships and sustainable technology initiatives to strengthen positions and enhance operational efficiency.

| Key Insights | Details |

|---|---|

| Polyethylene Wax Market Size (2025E) | US$1.98 Bn |

| Market Value Forecast (2032F) | US$3.04 Bn |

| Projected Growth CAGR (2025-2032) | 6.3% |

| Historical Market Growth (2019-2024) | 4.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rapid Industrial Expansion and Infrastructure Development

Rapid industrial growth in emerging economies is fueling demand for polyethylene wax in manufacturing, coatings, and construction materials. China’s industrial output and India’s expanding manufacturing sector contribute to over US$127 Billion in annual chemical processing investments, with polyethylene wax accounting for 3-5% of additive use.

Global infrastructure spending surpassed US$10 Trillion in 2024, driving the need for oxidized polyethylene wax in protective coatings to enhance durability and corrosion resistance. Expanding automotive and packaging industries across Asia Pacific further boost demand for processing aids and surface modifiers, making polyethylene wax vital for improving production efficiency and maintaining high-quality performance standards.

Increasing Adoption of Hot Melt Adhesives and Advanced Coatings

The global shift toward efficient bonding and high-performance surface treatments is driving polyethylene wax demand in hot melt adhesives and advanced coatings. Growing at a 7.4% CAGR, the hot melt adhesive market uses polyethylene wax for 15-25% of formulation weight in packaging, woodworking, and automotive applications.

Demand for micronized and oxidized grades is rising with the need for scratch resistance, gloss, and anti-blocking. With over US$50 Billion invested annually, the European coatings industry emphasizes low-VOC, eco-friendly formulations. Expanding e-commerce packaging and stricter emission regulations further boost polyethylene wax adoption in sustainable, high-performance adhesive and coating systems offering durability and rapid setting properties.

Barrier Analysis - Volatile Raw Material Costs and Supply Chain Dependencies

Volatile ethylene prices and petroleum-based feedstock fluctuations impose major cost pressures on polyethylene wax manufacturers, with raw materials accounting for 60-70% of production expenses. Global energy market instability can trigger 15-25% price swings in finished wax products quarterly.

Supply chain disruptions and regional production concentration heighten geopolitical and transportation risks, forcing reliance on costly alternative suppliers. Small-to-medium producers remain particularly vulnerable to feedstock volatility, limiting competitiveness and threatening pricing stability and product availability across global markets.

Environmental Regulatory Compliance and Sustainability Pressures

Stringent environmental regulations on plastic production and disposal pose compliance challenges for polyethylene wax manufacturers, driving investments in emission control and waste management. Frameworks such as the EU REACH increase costs and delay new product launches.

Rising sustainability expectations push companies toward bio-based alternatives, demanding high R&D spending with uncertain returns. Policies promoting circular economy goals and plastic reduction restrict growth in single-use applications, while limited recycling infrastructure for wax-containing products complicates end-of-life management and regulatory approvals for new formulations.

Opportunity Analysis - Bio-Based and Sustainable Polyethylene Wax Development

The global shift toward sustainable materials is driving demand for bio-based polyethylene wax derived from renewable sources such as sugarcane and plant oils. Braskem’s I’m Green™ portfolio showcases 80-100% renewable content, offering drop-in replacements for conventional waxes without equipment changes.

Research efforts focus on biodegradable formulations with lactic acid linkages for complete decomposition in packaging uses. Growing consumer preference for sustainable ingredients, especially in cosmetics and personal care, enhances market appeal, while bio-refinery investments and feedstock processing create integrated opportunities supporting sustainability and regulatory compliance advantages for manufacturers.

Emerging Applications in Cosmetics and Pharmaceuticals

The growing cosmetics and pharmaceutical sectors offer lucrative opportunities for specialized polyethylene wax formulations that ensure superior performance and regulatory compliance. Premium cosmetic products, such as lipsticks, skin and hair care items, use polyethylene wax to enhance texture, gloss, and stability, achieving 25-40% higher prices than industrial grades.

In pharmaceuticals, FDA-compliant waxes support tablet coatings, capsules, and controlled-release systems. Rising demand for sustainable, high-performance ingredients positions bio-based polyethylene wax as a premium alternative. Rapid personal care growth in Asia Pacific and Latin America, alongside regulatory harmonization, enables global market expansion and cost-efficient product standardization.

Category-wise Analysis

Product Insights

High-Density Polyethylene (HDPE) wax is anticipated to dominate the market with a 45% share in 2025, maintaining leadership through its superior hardness, thermal stability, and versatility across diverse industrial applications. Renowned for its excellent lubrication properties and compatibility with multiple polymer systems, HDPE wax is indispensable in PVC processing, masterbatch production, and coating formulations.

Its highly crystalline structure ensures higher melting points, improved chemical resistance, and enhanced mechanical strength compared to lower-density alternatives. The material’s extensive uses in plastics processing, as both an internal and external lubricant, support consistent demand across automotive, packaging, and construction sectors that rely on durable performance under rigorous processing conditions.

Oxidized Polyethylene (OPE) wax represents the fastest-growing segment, projected to expand at a 7.3% CAGR, fueled by demand for advanced formulations offering improved compatibility and functional performance. Containing polar functional groups such as carbonyl and hydroxyl moieties, OPE wax enhances adhesion to water-based systems and polar substrates.

Its growing use in printing inks for superior rub resistance and pigment dispersion underscores this trend. The coatings industry increasingly utilizes oxidized polyethylene for enhanced scratch resistance and surface durability in automotive and industrial finishes. High-value applications in textiles, leather processing, and performance adhesives create premium pricing opportunities and justify continued investment in OPE wax innovation.

Processing Method Insights

Chemical modification is anticipated to hold a dominant 50% of the market share in 2025, reflecting the industry's preference for tailored performance achieved through controlled chemical reactions.

Techniques such as oxidation, grafting, and functionalization enable manufacturers to develop specialized wax grades with enhanced compatibility, optimized molecular weight distribution, and improved thermal and mechanical properties for targeted end-user applications. Advanced chemical modification equipment and process control systems support the production of high-value specialty grades commanding premium prices in cosmetics, pharmaceuticals, and advanced coatings.

Physical blending represents the fastest-growing segment, projected to expand at a 7.2% CAGR, driven by cost-effective processing and rising demand for customized formulations. This method combines different polyethylene wax grades or integrates additives without chemical reactions, offering flexibility for diverse application needs.

Automated blending systems and advanced mixing technologies ensure consistent quality and performance, making physical blending ideal for price-sensitive industries. Its adaptability to rapid formulation changes and its compliance with varying performance and regulatory standards strengthen its role in meeting evolving market requirements.

Application Insights

Plastics & polymer applications are anticipated to lead with 33% market share in 2025, establishing polyethylene wax as essential for modern polymer processing and manufacturing efficiency. Polyethylene wax serves critical functions as a processing aid, lubricant, and flow modifier in plastic processing operations, including extrusion, injection molding, and blow molding.

The expanding global plastics industry, valued at US$580 Billion annually, drives sustained demand for polyethylene wax additives, improving manufacturing efficiency and product quality. Applications in PVC processing, where polyethylene wax reduces processing temperatures and improves surface finish, represent significant volume consumption supporting market leadership. The growth of lightweight automotive components and advanced packaging materials creates expanding opportunities for specialized polyethylene wax grades offering enhanced performance characteristics.

Cosmetics & pharmaceuticals emerges as the fastest growing application segment with 8.4% CAGR, reflecting increasing demand for high-performance ingredients in personal care and healthcare products. Premium cosmetic applications, including lipsticks, foundations, and skincare products, utilize polyethylene wax for texture enhancement, stability improvement, and sensory optimization.

The expanding global cosmetics market, particularly in emerging economies, drives demand for specialized wax grades meeting stringent regulatory requirements and performance standards. Pharmaceutical applications, including tablet coatings, controlled-release formulations, and capsule manufacturing, require high-purity polyethylene wax grades complying with FDA and international regulatory standards.

Growing consumer preference for premium personal care products and increasing healthcare spending support sustained growth in cosmetics and pharmaceutical applications, justifying premium pricing for specialized formulations.

Regional Insights

North America Polyethylene Wax Market Trends

North America demonstrates prominent growth with a 6.9% CAGR, establishing the region as a dynamic market driven by advanced manufacturing capabilities and strong regulatory frameworks supporting innovation. The U.S. leads regional expansion with a market value of ~US$350 Million in 2024, reflecting robust industrial demand and technological advancement.

The region's mature petrochemical infrastructure provides a reliable feedstock supply and cost-competitive production capabilities, supporting major manufacturers including Honeywell International, Baker Hughes, and Westlake Corporation.

Government initiatives promoting advanced manufacturing and Industry 4.0 adoption create favorable conditions for polyethylene wax applications in automotive, aerospace, and electronics industries, requiring precise performance characteristics.

The regulatory landscape in North America, governed by strict EPA and FDA standards, boosts demand for high-quality polyethylene wax formulations. A focus on sustainable practices and circular economy principles promotes opportunities for bio-based alternatives and recycling initiatives.

Investments in R&D, supported by universities and government funding, position manufacturers to lead in next-generation polyethylene wax technologies, including nanotechnology and smart materials. An emphasis on reshoring and supply chain resilience enhances domestic production for strategic industries.

Europe Polyethylene Wax Market Trends

Europe maintains a significant 27% market share while demonstrating steady growth supported by stringent regulatory frameworks and advanced manufacturing technologies across key member states. Germany, the U.K., France, and Spain lead regional demand through substantial automotive, chemical processing, and packaging industries requiring high-performance polyethylene wax solutions.

The European Union's comprehensive REACH regulations establish rigorous safety and environmental standards, creating barriers to entry while supporting premium pricing for compliant formulations. The region's commitment to sustainability and circular economy principles drives investment in bio-based polyethylene wax alternatives and recycling technologies, positioning European manufacturers as leaders in sustainable chemical production.

Europe’s advanced automotive sector, with its focus on lightweight materials and electric vehicle technologies, is driving demand for specialized polyethylene wax formulations designed to enhance advanced composite materials and battery applications.

Investments in green chemistry research and sustainable manufacturing processes position Europe at the forefront of next-generation polyethylene wax technologies. The harmonized regulatory environment across the EU member states enables manufacturers to develop standardized formulations serving multiple markets, reducing compliance costs while maximizing market reach.

Asia Pacific Polyethylene Wax Market Trends

Asia Pacific dominates global market share with 37% of the total revenue, establishing the region as the primary growth engine driven by massive manufacturing capacity and expanding industrial applications. China leads regional expansion with the largest polyethylene wax market, supported by extensive plastic processing infrastructure and growing demand across automotive, packaging, and construction sectors.

India demonstrates the prominent growth potential, reflecting rapid industrialization and expanding consumer markets. The region's cost advantages in raw materials and manufacturing enable competitive pricing while supporting global export opportunities.

Manufacturing advantages such as established petrochemical infrastructure, a skilled workforce, and government support favor polyethylene wax production. The growing packaging industry, driven by e-commerce and shifting consumer preferences, boosts demand for polyethylene wax-modified adhesives and coatings.

Investments in advanced manufacturing technologies improve efficiency and product quality, enabling expansion into high-value applications. Government initiatives promoting sustainability create opportunities for bio-based polyethylene wax alternatives while supporting economic development.

Competitive Landscape

The global polyethylene wax market is moderately consolidated, with major players controlling 55-60% of market share through strong distribution networks, broad product portfolios, and advanced technological capabilities. Key leaders such as BASF SE, Clariant AG, Honeywell International Inc., The Lubrizol Corporation, and Mitsui Chemicals Inc. leverage extensive R&D and global production to serve varied industries.

The remaining 40-45% is held by regional and niche manufacturers targeting specialized applications. Market concentration differs by segment, with premium sectors dominated by experts and commodity areas characterized by fragmented, price-driven competition.

Key Industry Developments

- In May 2024, Clariant introduced AddWorks PPA, a PFAS-free polymer processing aid, and AddWorks PKG 158, an efficient antioxidant solution for color protection. These products are designed for recycled polyolefins and are expected to be launched in Spring 2024, aiming to minimize plastic's environmental impact.

- In April 2024, ExxonMobil introduced a new wax product brand, Prowaxx, allowing differentiation between waxes and demonstrating strategic intent to invest in the future of wax. Prowaxx serves as an anchor for the product portfolio and customer decision-making.

- In March 2023, Micro Powders unveiled new natural and PTFE additives at ECS 2023, including NatureTex, NatureMatte C44, MP-28AL, and PolyTuf 1229, offering haptic effects, gloss reduction, and burnish resistance.

Companies Covered in Polyethylene Wax Market

- BASF SE

- Clariant International

- Honeywell International Inc.

- Innospec Inc.

- Mitsui Chemicals America, Inc.

- Westlake Chemical Corporation

- Trecora Resources

- The Lubrizol Corporation

- EUROCERAS

- Qingdao Haihao Chemical Co., Ltd.

- Prizm Marketing Inc.

- Indian Petrochemical Corporation Ltd.

- National Organic Chemicals Ltd.

- Hengshui Yimei New Material Technology Co., Ltd.

- DEUREX AG

Frequently Asked Questions

The polyethylene wax market is projected to be valued at US$1.98 Billion in 2025.

Rapid industrial expansion in emerging economies, increasing adoption of hot melt adhesives and advanced coatings, and technological advancement in polymer processing drive market growth.

The polyethylene wax market demonstrates robust growth at a 6.31% CAGR from 2025 to 2032.

Bio-based and sustainable wax development, emerging applications in cosmetics and pharmaceuticals, and advanced manufacturing integration with smart materials present significant growth opportunities.

Market leaders include BASF SE, Clariant AG, Honeywell International Inc., The Lubrizol Corporation, and Mitsui Chemicals Inc.