- Plastics, Polymers & Resins

- Polyethylene Film Market

Polyethylene Film Market Size, Share, and Growth Forecast 2026 - 2033

Polyethylene Film Market by Film Type (Low-Density Polyethylene (LDPE) Films, Linear Low-Density Polyethylene (LLDPE) Films, High-Density Polyethylene (HDPE) Films, Medium-Density Polyethylene (MDPE) Films, Cross-Linked Polyethylene (PEX) Films), Application (Packaging, Agriculture Films, Trash Bags & Liners, Others), Thickness, and Regional Analysis, 2026 - 2033

Polyethylene Film Market Size and Trend Analysis

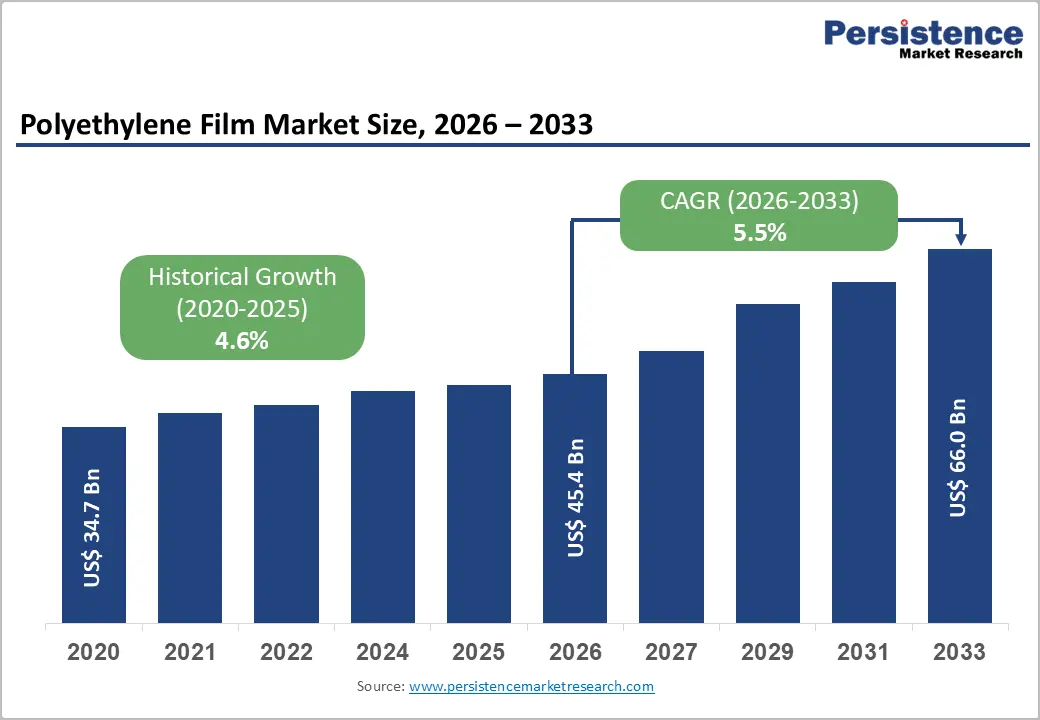

The global polyethylene film market size is expected to be valued at US$ 45.4 billion in 2026 and projected to reach US$ 66.0 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033. Soaring demand for flexible food packaging, agricultural mulch films, and e-commerce shipping liners is driving expansion.

According to PlasticsEurope, global polyethylene production exceeded 110 million tons in 2023, with film applications consuming the largest share. Continuous innovation in recyclable mono-material structures and bio-based polyethylene further reinforces market momentum across both developed and emerging economies.

Key Industry Highlights:

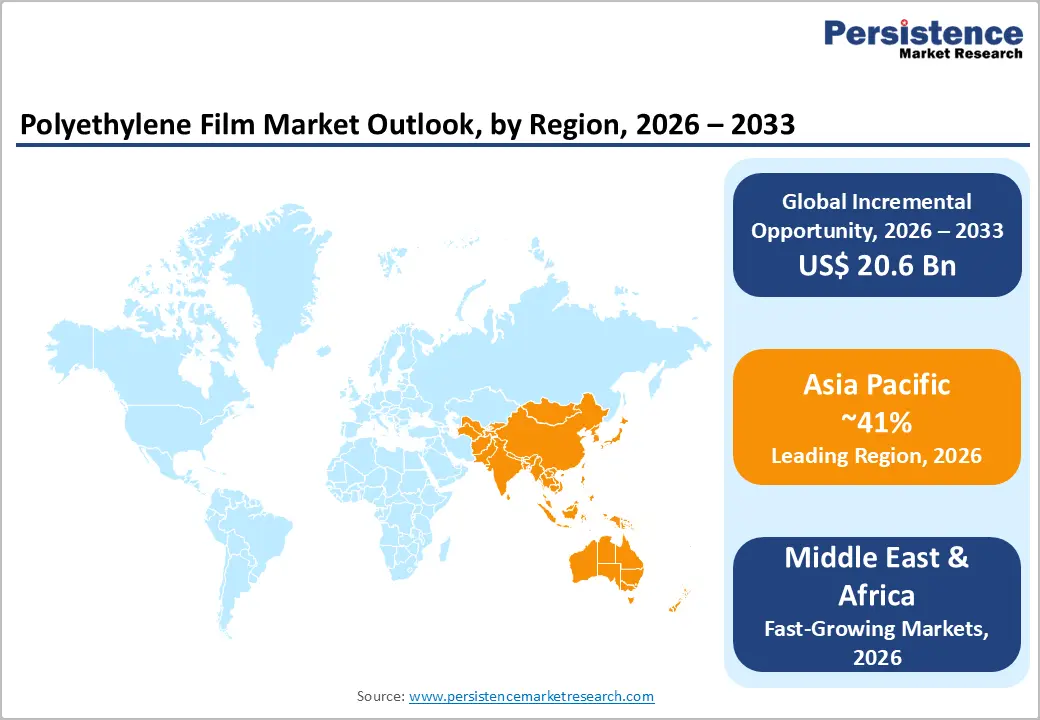

- Leading Region: Asia Pacific leads the global polyethylene film market with 41% share in 2026, propelled by China, India, and Southeast Asia's booming food packaging, e-commerce, and agricultural plasticulture sectors.

- Fastest Growing Region: Middle East & Africa is the fastest-growing region during 2026 - 2033, supported by rising food processing investments, expanding agricultural film usage, and growing e-commerce penetration across GCC and African economies.

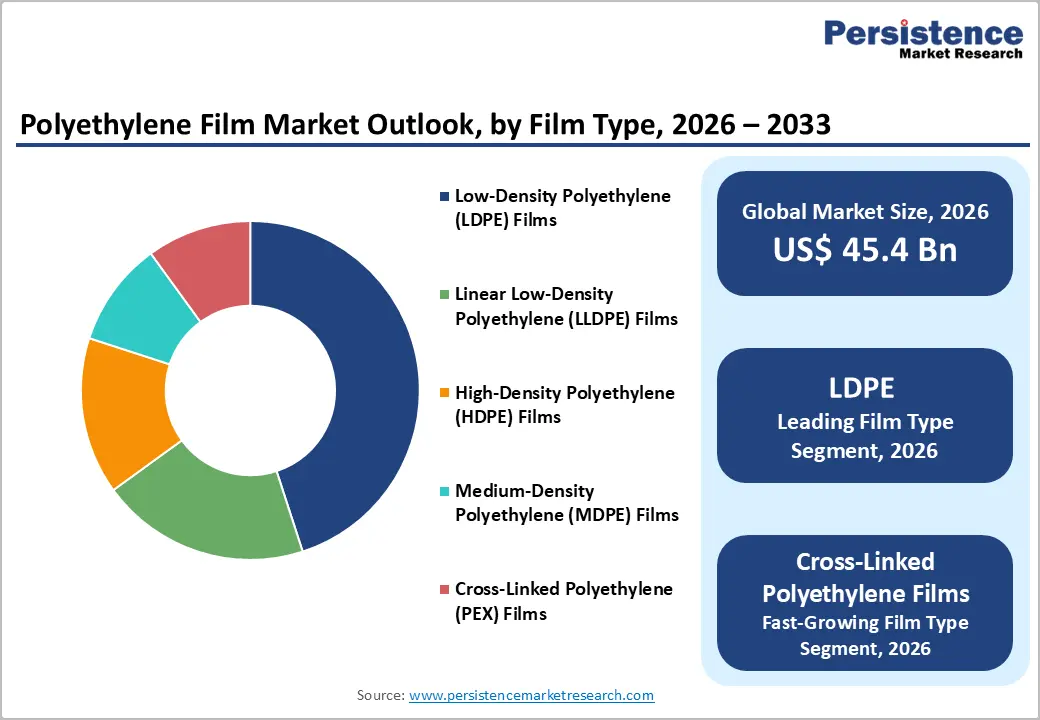

- Dominant Film Type: LDPE films dominate the product category with around 45% share in 2026, owing to flexibility, sealability, and broad suitability across food packaging, agriculture, and general-purpose film applications globally.

- Fastest Growing Film Type: Cross-Linked Polyethylene (PEX) films are the fast-growing segment at a leading CAGR, fueled by demand in EV battery thermal insulation, medical packaging, and high-performance industrial applications.

- Key Opportunity: A key opportunity lies in recyclable mono-material and bio-based PE films, supported by major brand owner sustainability commitments under the Ellen MacArthur Foundation New Plastics Economy initiative through 2030.

DRO Analysis

Drivers - Rising Demand from the Flexible Food and Beverage Packaging Industry

Flexible packaging dominates polyethylene film demand owing to its lightweight, hygienic, and protective qualities. According to the Flexible Packaging Association (FPA), flexible packaging accounted for nearly 20% of the US$ 200+ billion U.S. packaging industry in 2024, with food and beverage representing the largest end use. The U.S. Department of Agriculture (USDA) reports that processed food consumption continues rising at 3-4% annually, driving demand for stretch wraps, lidding films, and pouches.

Polyethylene films offer excellent moisture barriers, sealability, and printability, making them indispensable for fresh produce, frozen foods, dairy, and beverages. Additionally, rapid expansion of online grocery and meal-kit deliveries amplifies consumption of high-clarity, puncture-resistant polyethylene films globally.

Booming Agriculture and Greenhouse Film Adoption

Agricultural polyethylene films play a critical role in modern farming, supporting yield improvement and water conservation. According to the Food and Agriculture Organization (FAO), global plasticulture covers more than 6 million hectares of farmland, with mulch and greenhouse films forming the bulk. China alone uses over 2 million tons of mulch film annually, per the Chinese Academy of Agricultural Sciences.

These films extend growing seasons, reduce water use by up to 30%, and protect crops from pests and weather extremes. Government subsidies in India, China, and the EU under sustainable agriculture programs further accelerate uptake. UV-stabilized LDPE and LLDPE films are particularly preferred for greenhouse and silage applications, supporting steady volumetric growth.

Restraints - Mounting Environmental Concerns and Single-Use Plastic Bans

Polyethylene films face intensifying scrutiny due to plastic waste pollution. The United Nations Environment Programme (UNEP) estimates that 400 million tons of plastic waste are generated annually, with films and bags among the least recovered.

The European Union's Single-Use Plastics Directive (SUP) and bans across India, Kenya, and several U.S. states restrict carrier bag and certain film usage. Such regulations curtail demand in specific application segments and pressure manufacturers to invest heavily in recyclable or compostable alternatives, raising production costs and threatening growth in select end-use categories.

Volatility in Petrochemical Feedstock Prices

Polyethylene film production is highly dependent on ethylene derived from naphtha and natural gas. According to the U.S. Energy Information Administration (EIA), natural gas prices fluctuated between US$ 2 and US$ 6 per MMBtu through 2023-2024, while crude oil prices swung between US$ 70 and US$ 95 per barrel.

This volatility creates pricing uncertainty across the polyethylene value chain, squeezing converter margins and complicating long-term supply contracts. Geopolitical disruptions, such as Red Sea shipping issues and Middle East tensions, further amplify feedstock cost risk, hindering planning and capital expansion decisions for film producers.

Opportunities - Growth in Recyclable Mono-Material and Bio-Based Polyethylene Films

Sustainability is reshaping the polyethylene film opportunity landscape. Brand owners including Nestlé, Unilever, and PepsiCo have committed to 100% recyclable, reusable, or compostable packaging by 2025-2030 under the Ellen MacArthur Foundation's New Plastics Economy initiative. This is fueling demand for mono-material PE structures replacing multi-layer laminates, enabling mechanical recycling at scale.

Bio-based polyethylene from sugarcane ethanol, pioneered by Braskem's I'm green™ range, is gaining traction across European and North American FMCG markets. The broader flexible packaging market transition toward circular economy models opens substantial growth runways for innovators offering recyclable PE films, particularly in food, personal care, and pharmaceutical segments by 2033.

Rising Adoption of Cross-Linked Polyethylene (PEX) Films in Specialty Applications

Cross-linked polyethylene (PEX) films, projected to grow at a 6% CAGR during 2026 - 2033, represent the fastest-growing film type. Their superior thermal resistance, mechanical strength, and chemical inertness make them ideal for medical packaging, heat-shrink applications, automotive battery insulation, and high-performance building films.

The U.S. FDA approves PEX for various medical and food-contact uses, while electric vehicle battery makers increasingly specify PEX films for thermal management. According to the International Energy Agency (IEA), global EV sales surpassed 17 million units in 2024, accelerating demand for advanced thermal-resistant films. Manufacturers such as Mondi plc and Sealed Air Corporation are actively investing in PEX-related innovations to capture this premium niche.

Category-wise Analysis

Film Type Insights

Low-Density Polyethylene (LDPE) films lead the global market with approximately 45% share in 2026. LDPE's flexibility, transparency, sealability, and cost-effectiveness make it the universal choice for shrink wraps, bread bags, frozen food films, and general-purpose packaging. According to PlasticsEurope, LDPE remains one of the highest-volume polyethylene grades produced worldwide. Its compatibility with high-speed converting equipment and excellent machinability across blown and cast extrusion lines reinforces its dominance.

LDPE films perform well in greenhouse and mulch agricultural applications due to UV transparency and tear resistance. Continuous reformulation toward recyclable mono-material structures and incorporation of bio-based LDPE, such as Braskem's I'm green™, further sustains the segment's leadership through the forecast period.

Application Insights

Packaging is the dominant application, holding nearly 65% of the global polyethylene film market share in 2026. Within packaging, food and beverage represents the single largest sub-segment due to widespread use of stretch films, lidding films, pouches, and bags. According to the Flexible Packaging Association (FPA), food and beverage account for approximately 60% of total flexible packaging consumption.

Pharmaceutical and personal care applications are also rising rapidly, supported by stringent U.S. FDA and European Medicines Agency (EMA) packaging requirements. The boom in e-commerce, with global online retail sales surpassing US$ 6 trillion in 2024 per UNCTAD, drives heavy use of polyethylene mailers, bubble wraps, and protective films, reinforcing packaging's leadership.

Thickness Insights

The 30-60 Microns thickness segment leads the polyethylene film market with around 38% share in 2026. This thickness range strikes an optimal balance between mechanical strength, material economy, and machinability across diverse high-volume applications such as grocery bags, food wraps, lamination films, and lightweight industrial liners. Converters favor this gauge for blown and cast extrusion as it ensures consistent processing and downgauging potential to reduce material consumption.

According to PlasticsEurope, downgauging trends across the broader flexible packaging industry continue to drive a shift toward 30–60-micron formats. Brand owners aiming to meet sustainability commitments, such as the Ellen MacArthur Foundation's circular economy targets, are increasingly specifying thinner gauges, reinforcing this segment's dominance through the forecast period.

Regional Analysis

North America Polyethylene Film Market Trends and Insights

North America commands a substantial share, supported by mature flexible packaging, agricultural plasticulture, and e-commerce ecosystems. Key trends include rapid adoption of recyclable mono-material PE structures, growing demand for stretch and shrink films in logistics, and rising bio-based polyethylene uptake. According to the American Chemistry Council (ACC), U.S. polyethylene resin output remains the world's second largest, fueling robust regional film production capacity.

U.S. Polyethylene Film Market Size

The United States accounts for nearly 85% of the North American polyethylene film market. The Flexible Packaging Association (FPA) values the U.S. flexible packaging sector at over US$ 40 billion, with PE films forming the largest component. E-commerce growth, US$ 1.1 trillion in U.S. retail sales reported by the U.S. Census Bureau in 2024, drives demand for protective mailers, while sustainability mandates accelerate recyclable mono-PE adoption.

Europe Polyethylene Film Market Trends and Insights

Europe is shaped by stringent EU SUP Directive, REACH, and Packaging and Packaging Waste Regulation (PPWR) mandates pushing recyclable and reusable PE films. The region leads in mono-material innovations and bio-based polyethylene adoption. Demand from food packaging, agriculture, and pharmaceutical sectors remains strong, with brand owner commitments under Ellen MacArthur Foundation initiatives reshaping product portfolios across Germany, France, Italy, and U.K.

Germany Polyethylene Film Market Trends

Germany commands approximately 22% of the European polyethylene film market. The German Federal Statistical Office (Destatis) reports the chemical industry generated revenues exceeding EUR 230 billion in 2024, anchoring polymer film output. Strong demand from automotive, food packaging, and pharmaceutical sectors, combined with stringent recyclability standards, drives advanced PE film innovation and consumption.

U.K. Polyethylene Film Market Insights

The United Kingdom holds nearly 14% of European polyethylene film demand. According to the Office for National Statistics (ONS), retail sales reached GBP 517 billion in 2024, supporting strong flexible packaging consumption. Government plastic packaging tax of GBP 217.85 per tonne on films with under 30% recycled content is steering producers toward recyclable PE alternatives.

France Polyethylene Film Market Insights

France accounts for around 12% of the European market. INSEE data shows the French food and beverage sector generates over EUR 200 billion in annual revenues, sustaining heavy PE film demand. National anti-waste laws (AGEC Law) and strong agricultural plasticulture, France being one of Europe's largest farming economies, drive film consumption across packaging and agriculture segments.

Asia Pacific Polyethylene Film Market Trends and Insights

Asia Pacific leads globally with 41% market share in 2026, propelled by China, India, and Southeast Asia. China alone consumes over 2 million tons of agricultural mulch film annually per the Chinese Academy of Agricultural Sciences. Booming e-commerce, food processing, and construction sectors fuel demand. Trends include rapid greenhouse film expansion, shift toward thinner gauges, and rising bio-based PE adoption among multinational brand owners operating regionally.

India Polyethylene Film Market Size and Share

India captures approximately 15% of Asia Pacific polyethylene film demand. MoSPI reports India's GDP grew by 8.2% in fiscal 2024, with strong food processing and e-commerce expansion. Government initiatives like PMKSY food processing scheme and PM Kisan support agricultural film usage, while rising packaged-food consumption fuels flexible PE film demand.

Japan Polyethylene Film Market Size

Japan accounts for around 17% of Asia Pacific demand. According to the Japan Petrochemical Industry Association (JPIA), polyethylene production remains a key chemical export. Demand stems from highly developed food, electronics, and medical packaging sectors, with strict JIS quality standards driving premium PE film adoption, including high-performance lamination and barrier structures.

Southeast Asia Polyethylene Film Market Size

Southeast Asia represents nearly 14% of regional demand, with Thailand, Indonesia, Vietnam, and Malaysia leading. The ASEAN Secretariat reports manufacturing FDI inflows above US$ 100 billion in 2024. Rising packaged food consumption, expanding aquaculture, and rapid e-commerce growth fuel polyethylene film uptake across diverse packaging and agricultural applications.

Competitive Landscape

The global polyethylene film market is fragmented, with the top ten players holding a moderate share while numerous regional converters operate locally. Leaders such as Mondi plc, Amcor plc, Sealed Air Corporation, Berry Global, and ProAmpac LLC focus on recyclable mono-material innovations, mergers, and capacity expansion. Key differentiators include sustainable PE structures, high-barrier multi-layer technologies, and digital printing capabilities.

Strategic partnerships with brand owners under sustainability commitments are common, while bio-based polyethylene partnerships, such as those with Braskem, gain traction. Emerging trends include thin-gauge downgauging, recycled content integration, and circular economy-aligned product portfolios across packaging, agriculture, and industrial film segments globally.

Key Developments

- In February 2025: Amcor plc announced the merger with Berry Global, creating one of the world's largest packaging companies with significant polyethylene film production capacity across multiple continents.

- In September 2024: Mondi plc launched its FunctionalBarrier Paper Recyclable platform alongside expanded recyclable PE film offerings, supporting brand owners' transition toward mono-material flexible packaging structures.

- In May 2024: Sealed Air Corporation introduced new recyclable polyethylene-based shrink films under its CRYOVAC® brand, targeting fresh meat and protein packaging customers worldwide.

Polyethylene Film Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 34.7 billion |

| Current Market Value (2026) | US$ 45.4 billion |

| Projected Market Value (2033) | US$ 66.0 billion |

| CAGR (2026 - 2033) | 5.5% |

| Leading Region | Asia Pacific, 41% |

| Dominant Category-1 | LDPE Films, 45% share |

| Top-ranking Category-2 | Packaging, 65% share |

| Incremental Opportunity | US$ 20.6 billion |

Companies Covered in Polyethylene Film Market

- Mondi plc

- Amcor plc.

- Sealed Air Corporation

- Huthamaki Oyj

- Winpak Ltd.

- ProAmpac LLC

- PolymerShapes LLC

- Nitto Denko Corporation

- Sphere Group

- Glenroy, Inc.

- Plastissimo Film Co., Ltd.

- Schur Flexibles Holding GesmbH

- Armando Alvarez Group

- Trioplast Industries

- Superfilm Packaging Industies

- Eiffel S.P.A.

Frequently Asked Questions

The global polyethylene film market is expected to be valued at US$ 45.4 billion in 2026 and is forecast to reach US$ 66.0 billion by 2033, advancing at a healthy 5.5% CAGR through the forecast period.

Surging demand for flexible food and beverage packaging, supported by 20% flexible packaging share within the U.S. packaging industry per FPA, alongside booming agricultural plasticulture across China and India, drives robust market growth.

Asia Pacific leads with around 41% market share in 2026, anchored by China's massive mulch film consumption exceeding 2 million tons annually, India's expanding food processing, and Southeast Asia's e-commerce growth.

The transition toward recyclable mono-material and bio-based polyethylene films, driven by brand owner commitments under the Ellen MacArthur Foundation New Plastics Economy initiative, offers substantial growth potential across food, personal care, and pharmaceutical end-uses.

Major players include Mondi plc, Amcor plc, Sealed Air Corporation, Huhtamaki Oyj, Berry Global, ProAmpac LLC, Winpak Ltd., Nitto Denko Corporation, Trioplast Industries, and Constantia Flexibles, alongside numerous regional converters.