- Specialty & Fine Chemicals

- High Performance Polyethylene (HPPE) Market

High Performance Polyethylene (HPPE) Market Size, Share, and Growth Forecast, 2026 - 2033

High Performance Polyethylene (HPPE) Market By Product Type (High Density Polyethylene (HDPE), Others), Form (Films, Sheets, Others), Application (Automotive, Aerospace, Others), End-user Industry (Construction, Others), and Regional Analysis for 2026 – 2033

High Performance Polyethylene (HPPE) Market Size and Trends Analysis

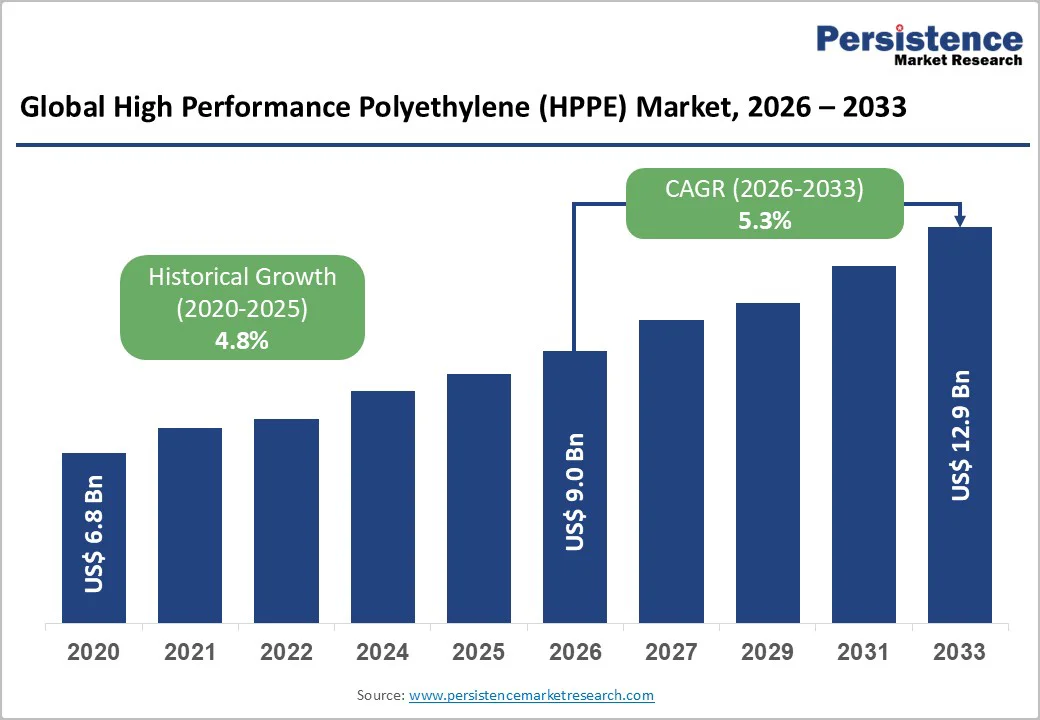

The global high performance polyethylene (HPPE) market size is likely to be valued at US$9.0 billion in 2026, and is expected to reach US$12.9 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033, driven by the increasing prevalence of lightweight material demands, rising need for durable polymers in automotive and healthcare, and advancements in high-strength fiber technologies. Rising demand for recyclable, chemical-resistant HPPE in construction and aerospace, coupled with UHMWPE and HDPE advances offering superior impact resistance, is driving market growth in high-performance polyethylene applications.

Key Industry Highlights:

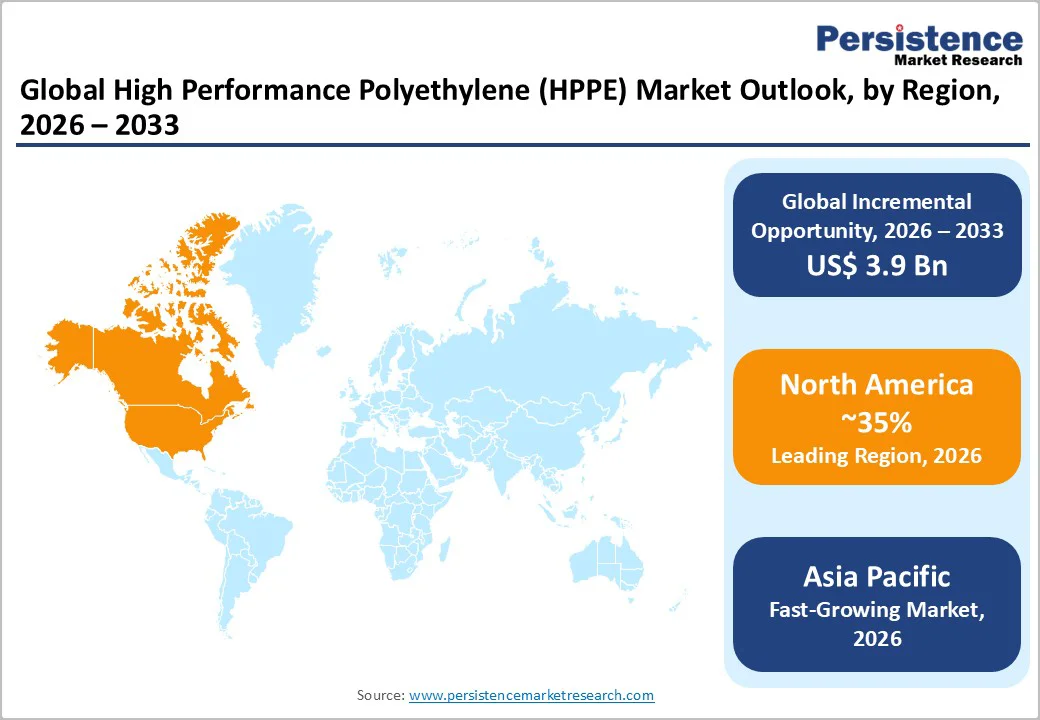

- Leading Region: North America is anticipated to account for a 35% market share in 2026, driven by advanced manufacturing hubs, high infrastructure spending, and robust polymer innovation in China and India.

- Fastest-growing Region: Asia Pacific, fueled by automotive expansions, rising awareness of lightweight composites, and growing investments in medical devices in Southeast Asia.

- Dominant Product Type: High Density Polyethylene (HDPE), to hold approximately 40% of the market share in 2026, as it delivers strong chemical resistance and longevity by mimicking robust structural bonds.

- Leading Form: Films, to contribute nearly 35% of the market revenue in 2026, due to their flexible barrier properties, ease of processing, and capacity for high-volume packaging solutions.

- Leading Application: Automotive, to account for over 30% of the market revenue, due to weight reduction needs, crash safety enhancements, and widespread integration into vehicle components.

- Leading End-user Industry: Construction, to dominate approximately 35% share, due to durable pipes and sheets requiring routine infrastructure upgrades, ensuring consistent demand.

| Key Insights | Details |

|---|---|

| High Performance Polyethylene Market (HPPE) Size (2026E) | US$9.0 Bn |

| Market Value Forecast (2033F) | US$12.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Lightweight Material Demands and Demand for Durable Polymers

The rising preference for lightweight material demands is quickly becoming a major opportunity for polymer developers, driven by the growing industry need for efficiency, sustainability, and reduced fuel consumption. Traditional heavy metals often create excess weight, especially in automotive and aerospace, leading to higher energy use and lower performance. High performance polyethylene (HPPE) technologies, including UHMWPE fibers, HDPE sheets, LLDPE films, MDPE rods, and reinforced pipes, address these concerns by offering a lightweight yet tough alternative. These formats simplify integration, reduce the need for secondary reinforcements, and are particularly effective during mass production or retrofits where rapid scaling is critical.

High performance polyethylene (HPPE) significantly lowers the risk of fatigue failure, corrosion, and environmental degradation, which remain major concerns in industrial settings. They also support improved recyclability and easier processing, especially for films and fibers, making them ideal for high-volume or remote applications. As global standards push for broader efficiency coverage and user-friendly materials, demand continues to expand across automotive, medical devices, and construction.

High Development and Processing Costs

High development and processing costs present a significant barrier for companies advancing next-generation high performance polyethylene (HPPE) and novel polymer systems. Developing innovative grades such as UHMWPE composites, HDPE blends, or LLDPE films requires extensive research, specialized catalysts, and advanced extrusion technologies that are far more expensive than commodity plastics. Performance is an even greater challenge: many enhanced HPPE, molecularly tuned variants, and additive-stabilized forms are sensitive to temperature, shear, and contamination, requiring rigorous optimization to ensure they maintain integrity throughout production and end-user. Achieving long-term durability often involves costly fatigue trials, sophisticated rheological testing, and the use of high-grade stabilizers, which significantly increase R&D expenditures.

Meeting stringent regulatory expectations for mechanical data, recyclability, and batch consistency requires multiple validation studies under various conditions and across several production batches. This adds both time and financial burden to development timelines. Scaling up manufacturing requires controlled environments, specialized extruders, and quality-assurance systems, further driving up overall costs. For smaller processors, these challenges can limit grade diversification or delay commercialization.

Advancements in Recyclable and High-Strength Delivery Platforms

Advancements in recyclable and high-strength high performance polyethylene (HPPE) delivery platforms are transforming the global materials landscape by addressing two major challenges, waste dependence and load-bearing limitations. Recyclable HPPE is engineered to achieve 95% post-consumer content, reducing reliance on virgin feedstocks and enabling circular supply chains in construction and packaging. Innovations, such as bio-derived catalysts, closed-loop extrusion, molecular engineering, and fiber reinforcement, significantly improve reprocess ability and reduce emissions, lowering logistical costs for industries and sustainability initiatives.

Progress in high-strength platforms, including UHMWPE ropes, HDPE pipes, LLDPE geomembranes, and MDPE rods, supports more robust performance by enhancing tensile strength, the material’s first line of defense against abrasion and impact. These formats minimize downtime, boost compliance, and allow modular assembly without heavy equipment, making them highly suitable for mass deployment programs. New technologies such as nano-additives, self-healing polymers, and VLP-based composites further enhance load response and environmental resilience.

Category-wise Analysis

Product Type Insights

High density polyethylene (HDPE) is anticipated to dominate the market, accounting for approximately 40% of the market share in 2026. Its dominance is driven by robust density, cost-effectiveness, and versatility, making it preferred for piping and films. High Density Polyethylene (HDPE) provides barrier protection, ensures durability, and contributes to efficiency, making it suitable for large-scale construction campaigns. For example, High-Density Polyethylene (HDPE) pipes have surged in popularity across diverse applications, owing to their exceptional properties and remarkable versatility. Recognized for their numerous advantages over traditional piping materials, HDPE pipes have become the preferred choice in crucial sectors such as water supply, gas distribution, agriculture, and sewage systems.

Ultra high molecular weight polyethylene (UHMWPE) represents the fastest-growing segment, due to its extreme toughness and expanding use in medical devices. Its strong impact profile makes it ideal for targeted wear resistance, reducing failures. Continuous innovations in molecular adjuvants are further strengthening their performance, driving rapid adoption across North America and Europe, where demand for next-generation, high-specification polymers is accelerating. For example, Ultra-high molecular weight polyethylene (UHMWPE) is the most common bearing material in total joint arthroplasty due to its unique combination of superior mechanical properties and wear resistance over other polymers. A great deal of research in recent decades has focused on further improving its performance in order to provide durable implants in young and active patients.

Form Insights

Films are expected to dominate the market, contributing nearly 35% of revenue in 2026, due to remaining the primary choice for packaging, flexible barriers, and agricultural mulching requiring thin, resilient layers. Their strong flexibility, trained processing, and ability to handle high-volume runs drive higher adoption. Films are leading LLDPE packaging rollouts as well as incorporating emerging MDPE trials. For example, Iris offers “Yellow Mulch Film” and “Red Mulch Film,” described to help in weed suppression, moisture conservation, and soil?temperature regulation, exactly the kinds of “flexible barrier/mulch films” that dominate in agriculture.

Pipes represent the fastest-growing segment, driven by their strong infrastructure presence and expanding role in water and gas conveyance. They offer convenient, quick, and accessible durability, attracting projects that prefer robust, low-leakage settings. Increased outreach programs, preventive design focus, and wider availability of routine and industrial pipes further accelerate deployment, boosting rapid adoption across both urban and rural areas. For example, Rajkee Pipes, one of the large HDPE pipe manufacturers in India, provides HDPE piping systems for a wide range of infrastructure applications: municipal water supply, underground drainage/sewerage, industrial effluent, chemical waste transport, marine pipelines, etc.

Application Insights

Automotive is expected to lead the market, holding approximately 30% of the share in 2026, driven by persistent lightweighting needs, large vehicle programs, and strong global demand for fuel-efficient components. Their dominance continues as manufacturers expand use for bumpers, tanks, and interiors. Rising adoption of LLDPE films and expanded aerospace campaigns highlight the growing focus on performance enhancement. For example, Plastic Omnium, a global automotive components supplier, is a leading producer of plastic fuel tanks and other lightweight automotive plastic parts for many car and commercial?vehicle manufacturers worldwide.

Medical devices are the fastest-growing segment, due to strong momentum in implants and expanding inclusion of biocompatible HPPE in surgical tools. The growing shift toward lightweight, sterilizable platforms, along with better tissue compatibility, accelerates the adoption. Advancements in UHMWPE prosthetics and the continued progress of fiber-reinforced devices entering clinical trials drive market growth. For example, Orthoplastics manufactures medical-grade UHMWPE (GUR resin), which is widely used in orthopedic implants, particularly for joint replacements (hip, knee, shoulder, etc.).

End-user Industry Insights

The construction segment is likely to dominate the market, with approximately 35% share in 2026, due to the high volume of infrastructure projects and strong global emphasis on resilient materials. Regular piping schedules, code requirements, and widespread access to modular systems drive consistent demand. Rising focus on geomembranes, fibers, and rods in agriculture further strengthens construction market leadership. For example, Sudarshan Pipes manufactures HDPE pipes (PE-80/PE-100) for a wide variety of applications: potable water supply, municipal water distribution, drainage/sewerage, irrigation, underground drainage, and industrial water/slurry transport.

Healthcare is the fastest-growing field, driven by the rising need for biocompatible implants, vulnerability to wear, and expanding adoption of sterile devices. Improved safety profiles, tailored molecular weights, and stronger biocompatibility for medical use support rapid uptake. The growing use of UHMWPE joints, LLDPE packaging, and MDPE sheets among aging populations further accelerates market growth. For example, Orthoplastics produces cross-linked UHMWPE (and even Vitamin E-stabilized grades) that provide high abrasion/wear resistance, low friction, high impact strength, and excellent biocompatibility, ideal for long-lasting, load-bearing prosthetic joints or implant components.

Regional Insights

North America High Performance Polyethylene (HPPE) Market Trends

North America is projected to account for nearly 35% of the global high performance polyethylene (HPPE) market in 2026, driven by the region’s advanced manufacturing infrastructure, strong research and development capabilities, and high public awareness of material benefits. Industry systems in the U.S. and Canada provide extensive support for polymer programs, ensuring wide accessibility of high performance polyethylene (HPPE) across automotive, medical, and construction populations. Increasing demand for UHMWPE fibers, convenient, and easy-to-process grades is further accelerating adoption, as these formats improve performance and reduce barriers associated with traditional metals.

Innovation in high performance polyethylene (HPPE) technology, including stable molecular structures, improved extrusion delivery, and targeted reinforcement, is attracting significant investment from both public and private sectors. Government initiatives and sustainability campaigns continue to promote the use of industrial wear, seismic events, and emerging efficiency threats, creating sustained market demand. The growing focus on LLDPE films and MDPE rods, particularly for packaging and agriculture, is expanding the target applications for high performance polyethylene (HPPE). For example, U.S. law enforcement agencies and the Department of Defense deploy ballistic vests and helmets made with Dyneema®, due to its ultra-high strength, which improves protection while reducing equipment weight by up to 40%. This makes Dyneema® a preferred material for lightweight body-armor plates, tactical protective vests, and next-generation ballistic helmets, reinforcing HPPE’s rising demand in the region.

Europe High Performance Polyethylene (HPPE) Market Trends

Europe is driven by increasing awareness of performance benefits, strong industry systems, and government-led innovation programs. Countries such as Germany, France, and the U.K. have well-established manufacturing frameworks that support routine integrations and encourage adoption of advanced polymer delivery methods, including high performance polyethylene (HPPE). These robust formulations are particularly appealing for automotive populations, cost-conscious developers, and healthcare users, improving efficiency and coverage rates.

Technological advancements in high performance polyethylene (HPPE) development, such as enhanced recyclability, strength-targeted delivery, and improved bio-based formulations, are further boosting market potential. European authorities are increasingly supporting research and trials for polymers against both routine and extreme conditions, strengthening market confidence. The growing emphasis on convenient, prefabricated options is aligned with the region’s focus on preventive manufacturing and reducing waste. Public awareness campaigns and development drives are expanding reach in both urban and rural areas, while chemical companies are investing in catalysts and novel grades to increase efficacy.

Asia Pacific High Performance Polyethylene (HPPE) Market Trends

Asia Pacific is likely to be the fastest-growing market for high performance polyethylene (HPPE) in 2026, driven by rising industrial awareness, increasing government initiatives, and expanding application programs across the region. Countries such as India, China, Japan, and Southeast Asian nations are actively promoting polymer campaigns to address automotive demands and emerging healthcare needs. High performance polyethylene (HPPE) is particularly attractive in these regions due to its lightweight integration, ease of scaling, and suitability for large-scale manufacturing drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-process high performance polyethylene (HPPE), which can withstand challenging operational conditions and minimize downtime dependence. These innovations are critical for reaching remote facilities and improving overall efficiency coverage. Growing demand for construction, electronics, and agriculture applications is contributing to market expansion. Public-private partnerships, increased polymer expenditure, and rising investment in material research and production capacity are further accelerating growth. The convenience of HPPE delivery, combined with improved durability and reduced risk of failures, positions high performance polyethylene (HPPE) as a preferred choice.

Competitive Landscape

The global high performance polyethylene (HPPE) market features competition between established chemical leaders and emerging processors. In North America and Europe, DuPont and DSM lead through strong R&D, distribution networks, and industry ties, bolstered by innovative grades and application programs. In Asia Pacific, LyondellBasell advances with localized solutions, enhancing accessibility. Strength-enhanced delivery boosts performance, cuts failure risks, and enables mass integrations across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Recyclable formulations solve sustainability issues, aiding penetration in eco-focused areas.

Key Industry Developments

- In September 2025, Borealis launched its Borstar® Nextension Polyethylene (PE) technology, advancing polyolefin innovation with superior toughness, sealing performance, and processability. This initiative supports packaging downgauging, enhances cost efficiency, and promotes design-for-recycling, addressing key industry sustainability and performance needs.

- In July 2024, ExxonMobil introduced its Enable 1617 performance polyethylene (PE) resin, optimized for thin-gauge hand wrap applications. The grade delivers high tenacity, consistent extrusion, and supports high incorporation of post-consumer recycled (PCR) content, aligning with sustainability and performance objectives.

Companies Covered in High Performance Polyethylene (HPPE) Market

- DuPont

- Teijin

- DSM

- Dow

- Celanese

- LyondellBasell

- Braskem

- Asahi Kasei

- Sabic

- Mitsui Chemicals

- Mitsuboshi

- Artek

- US Plastic Corp.

- Plastics International.

- Roll-a-Pipe Pty Ltd

- Luoyang Guorun Pipes

- Shandong Buoy & Pipe Industry Co., Ltd.

Frequently Asked Questions

The global high performance polyethylene (HPPE) market is projected to reach US$9.0 billion in 2026.

The rising prevalence of lightweight material demands and the demand for durable polymers are the key drivers.

The high performance polyethylene (HPPE) market is poised to witness a CAGR of 5.3% from 2026 to 2033.

Advancements in recyclable and high-strength delivery platforms are key opportunities.

DuPont, DSM, Dow, LyondellBasell, and Teijin are the key players.