- Plastics, Polymers & Resins

- Recycled Polyethylene Market

Recycled Polyethylene Market Size, Share, and Growth Forecast, 2025 - 2032

Recycled Polyethylene Market Product Type (Polyethylene Terephthalate, High-density Polyethylene, Polypropylene, Low-density Polyethylene, Others), Source (Plastic Bottles, Plastic Films, Polymer Foam, and Others), Application (Non-Food Packaging, Food Packaging, Construction, Automotive, and Others), and Regional Analysis for 2025 - 2032

Recycled Polyethylene Market Size and Trends Analysis

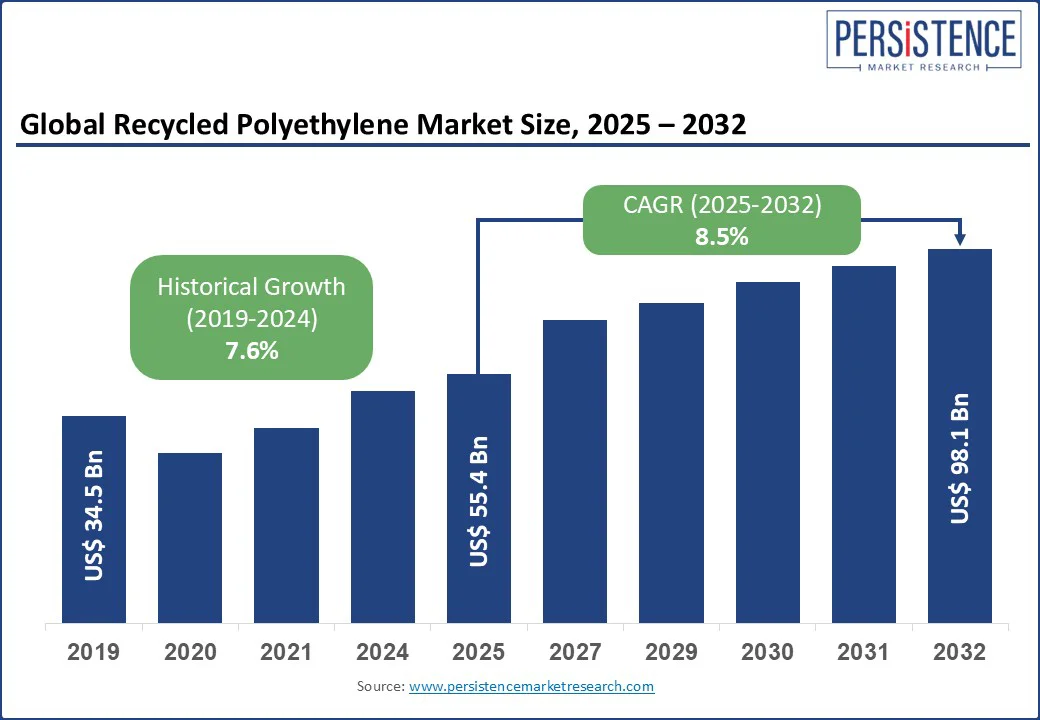

The global recycled polyethylene market size is likely to be valued at US$ 55.4 Bn in 2025 and is expected to reach US$ 98.1 Bn by 2032, registering a CAGR of 8.5% during the forecast period 2025-2032.

The sector's growth is driven by increasing environmental awareness, stringent government regulations promoting recycling, and the rising demand for sustainable packaging solutions across various industries. The versatility of recycled polyethylene, combined with its cost-effectiveness and eco-friendly attributes, positions it as a key material in addressing global sustainability challenges. The sector has seen steady growth, with a positive historical CAGR between 2019 and 2024, reflecting the increasing adoption of recycled materials in packaging, construction, and automotive sectors.

Key Industry Highlights:

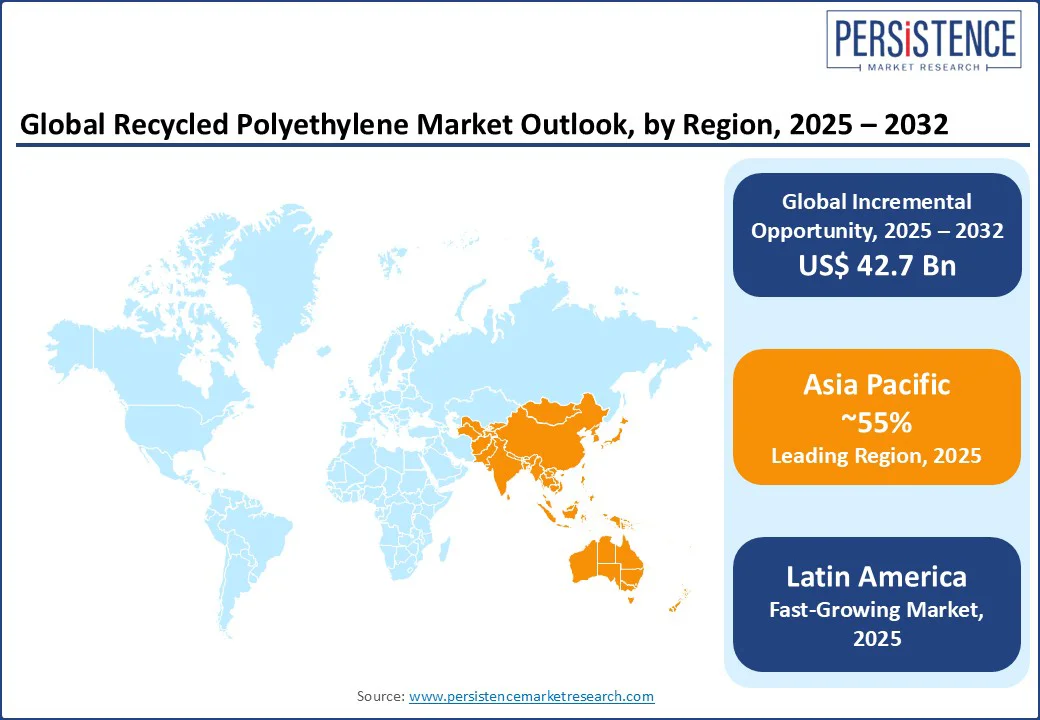

- Leading Region: Asia Pacific, commanding a 60% market share in 2025, driven by high industrial activity, rapid urbanization, and supportive government policies promoting recycling in countries such as China and India.

- Fastest-growing Region: Latin America emerges as the fastest-growing regional market for recycled PE, advanced recycling infrastructure, growing consumer demand for sustainable products, and regulatory incentives for circular economy practices.

- Dominant Product Type: High-density Polyethylene (HDPE), holding approximately 40% of the share, due to its widespread use in packaging and construction applications.

- Leading Application: Non-Food Packaging, accounting for over 45% of market revenue, driven by its extensive use in e-commerce, retail, and industrial packaging.

- Historical Growth: The domain registered a CAGR of 7.6% from 2019 to 2024, fueled by growing demand for eco-friendly materials and advancements in recycling technologies.

|

Global Market Attribute |

Key Insights |

|

Recycled Polyethylene Market Size (2025E) |

US$ 55.4 Bn |

|

Market Value Forecast (2032F) |

US$ 98.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.6% |

Market Dynamics

Driver- Rising Demand for Sustainable Packaging Solutions

The rising demand for sustainable packaging solutions is a key driver in the recycled polyethylene market, fueled by increasing environmental awareness and stricter regulatory frameworks worldwide. Governments, particularly in the European Union, North America, and parts of Asia Pacific, are implementing policies and bans on single-use plastics, prompting manufacturers to adopt eco-friendly alternatives. For instance, the European Union’s Single-Use Plastics Directive and India’s nationwide ban on select single-use plastic items have accelerated the shift toward recyclable materials.

Consumers are also becoming more conscious of their environmental footprint, favoring products with recyclable or biodegradable packaging. This shift is especially pronounced in industries such as food & beverage, personal care, e-commerce, and retail, where packaging plays a major role in brand perception.

Companies are responding by integrating recycled polyethylene into packaging to meet sustainability goals, reduce greenhouse gas emissions, and comply with circular economy principles. Technological advancements in recycling processes are also enhancing material quality, making recycled PE a viable substitute for virgin plastics without compromising performance. This convergence of consumer demand, corporate responsibility, and regulatory pressure is significantly accelerating market growth for sustainable packaging solutions.

Restraint - Challenges in Recycling Infrastructure and Quality Control

Challenges in recycling infrastructure and quality control remain significant restraints in the recycled polyethylene market. In many regions, particularly in developing economies, recycling facilities are limited, outdated, or unevenly distributed, leading to inefficiencies in waste collection and processing. For instance, in several Southeast Asian countries, less than 30% of plastic waste is formally collected for recycling, with much ending up in landfills or waterways. Even in developed markets, the lack of standardized collection systems and segregation practices often results in contaminated feedstock, which reduces the yield and quality of recycled polyethylene.

Quality control is another major concern, as recycled PE can exhibit variability in color, strength, and purity compared to virgin materials, limiting its application in high-performance or food-grade packaging. Additionally, the presence of mixed plastics and additives complicates the recycling process, increasing costs and reducing material consistency. Overcoming these issues requires significant investment in advanced sorting technologies, standardized recycling protocols, and improved supply chain coordination to ensure a steady flow of high-quality recycled polyethylene.

Opportunity- Advancements in Recycling Technologies

Advancements in recycling technologies present a significant opportunity for the recycled polyethylene market, enabling higher efficiency, improved material quality, and expanded end-use applications. Innovations such as chemical recycling and advanced mechanical recycling methods are helping overcome limitations associated with contamination, mixed plastics, and degraded polymer properties.

For example, depolymerization processes can break down polyethylene into its original monomers, producing material with quality comparable to virgin plastic. Similarly, AI-powered sorting systems and near-infrared (NIR) spectroscopy are enhancing the precision of material separation, reducing impurities, and increasing yield. For instance, in 2023, Coca-Cola and Indorama Ventures implemented enhanced PET and PE recycling technologies in their joint recycling plants, achieving food-grade quality output from post-consumer waste.

These advancements not only improve the economic viability of recycling but also open doors for recycled PE to enter demanding sectors such as food-grade packaging and medical applications. Moreover, technology integration supports a circular economy by enabling repeated recycling without significant loss of performance. As governments and corporations push for higher recycled content targets, these innovations are set to drive market growth and attract substantial investment.

Category-wise Analysis

Product Type Insights

HDPE dominates the recycled polyethylene market, expected to account for approximately 35% of the share in 2025. Its dominance is attributed to its strength, versatility, and widespread use in applications such as packaging, construction, and automotive components. HDPE’s high recyclability and compatibility with various processing techniques make it a preferred choice for manufacturers seeking sustainable materials. Its ability to be molded into bottles, containers, and pipes further enhances its demand in both industrial and consumer markets.

The fastest-growing segment is Polyethylene Terephthalate (PET), driven by increasing demand for recycled PET in food and beverage packaging. PET’s clarity, lightweight nature, and suitability for food-grade applications make it ideal for bottles and containers. The rise in consumer demand for sustainable packaging, coupled with advancements in PET recycling technologies, is accelerating its adoption, particularly in the Asia Pacific and North America.

Source Insights

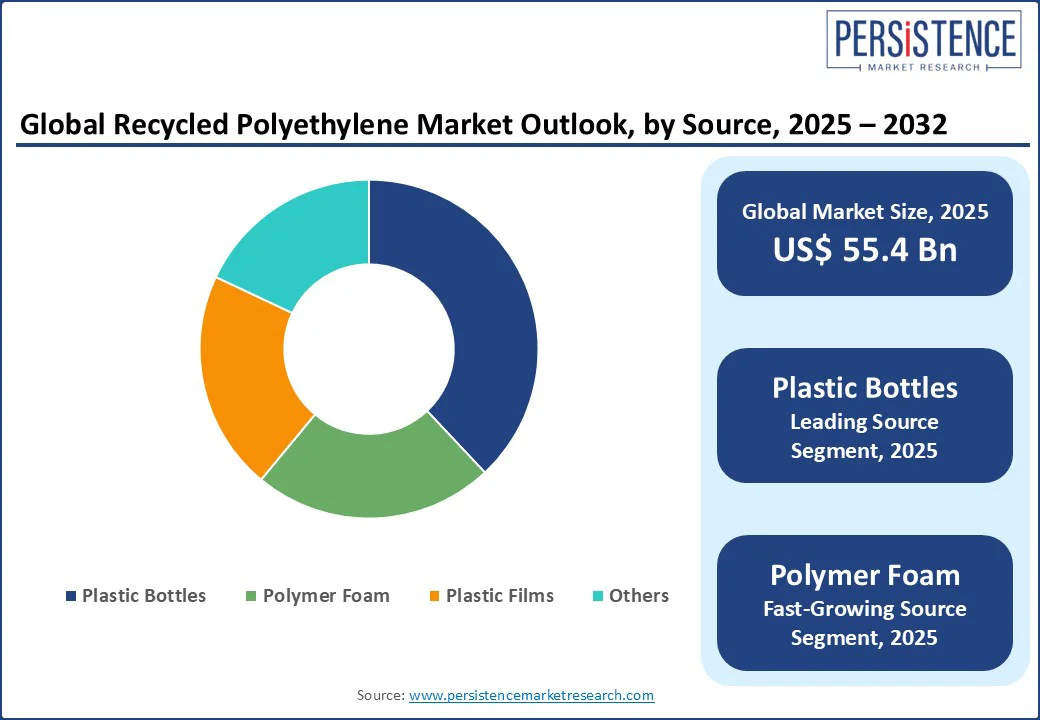

Plastic bottles hold the largest market share, accounting for approximately 38% of revenue in 2025. Their dominance is driven by the high volume of plastic bottle waste generated globally, particularly from the beverage industry, and the established infrastructure for collecting and recycling PET and HDPE bottles.

The fastest-growing source segment is polymer foam, fueled by increasing applications in the construction and automotive industries. Recycled polymer foam is gaining traction due to its lightweight and insulating properties, making it suitable for sustainable building materials and automotive components. Advancements in foam recycling technologies are further driving the adoption of this segment in emerging markets.

Application Insights

Non-food packaging leads the recycled polyethylene market, holding a 32% share in 2025. This segment’s dominance is driven by its extensive use in e-commerce, retail, and industrial packaging, where durability and cost-effectiveness are critical. Recycled polyethylene’s ability to be customized for various packaging formats, such as bags, films, and containers, supports its widespread adoption. Major e-commerce platforms, such as Amazon and Alibaba, rely heavily on recycled polyethylene for sustainable packaging solutions.

The fastest-growing application is food packaging, propelled by advancements in recycling technologies that enable the production of food-grade recycled polyethylene. Regulatory approvals for recycled PET and HDPE in food contact applications, combined with consumer demand for sustainable packaging, are driving rapid growth in this segment, particularly in Europe and North America.

Regional Insights

North America Recycled Polyethylene Market Trends

The North America recycled polyethylene market is witnessing steady growth, driven by increasing regulatory support, corporate sustainability commitments, and rising consumer demand for eco-friendly products. The United States and Canada are at the forefront, with well-established recycling infrastructure and initiatives aimed at reducing plastic waste. Government policies, such as state-level bans on single-use plastics and extended producer responsibility (EPR) programs, are encouraging manufacturers to incorporate higher recycled content in packaging.

Industries such as food & beverage, personal care, and e-commerce are adopting recycled polyethylene for non-food and food-grade packaging, supported by advancements in purification technologies. For instance, chemical recycling methods are enabling the production of recycled PE with properties comparable to virgin materials, expanding its use in premium applications. Additionally, major companies, including Procter & Gamble and Dow, are investing in closed-loop systems and large-scale recycling facilities. This combination of regulatory pressure, corporate action, and technological progress is accelerating market expansion across North America.

Latin America Recycled Polyethylene Market Trends

Latin America is emerging as the fastest-growing regional market for recycled polyethylene, fueled by a combination of improving recycling infrastructure, increasing consumer preference for sustainable products, and supportive government policies promoting circular economy practices. Countries such as Brazil, Mexico, and Chile are making significant investments in modern recycling facilities, enabling higher collection rates and better-quality output.

Regulatory measures, including bans on certain single-use plastics and incentives for using recycled content in packaging, are encouraging both domestic manufacturers and multinational companies to adopt recycled PE in their production processes. Consumer awareness of environmental issues is also on the rise, particularly in urban areas, driving demand for eco-friendly packaging in retail, food & beverage, and e-commerce sectors. Moreover, partnerships between governments, private companies, and NGOs are helping improve waste management systems and promote community-level recycling programs. This combination of policy support, infrastructure upgrades, and shifting market preferences is propelling the region’s rapid growth in the recycled PE sector.

Asia Pacific Recycled Polyethylene Market Trends

Asia Pacific is projected to command a 60% market share in the global recycled polyethylene market by 2025, making it the dominant regional player. This growth is driven by high industrial activity, rapid urbanization, and strong government initiatives aimed at reducing plastic waste. Countries such as China and India are at the forefront, implementing strict regulations on single-use plastics and offering incentives for the use of recycled materials in packaging, construction, and consumer goods.

China’s National Sword policy and India’s Extended Producer Responsibility (EPR) framework have encouraged investment in advanced recycling facilities and improved waste segregation systems. The region’s booming e-commerce, retail, and food & beverage sectors are also fueling demand for sustainable packaging solutions. Additionally, increasing public awareness of environmental issues and corporate sustainability commitments from major brands are accelerating adoption. Combined with technological advancements in recycling processes, these factors are solidifying Asia Pacific’s leadership in the global recycled polyethylene market.

Competitive Landscape

The global recycled polyethylene market is highly competitive, with a mix of global and regional players. Key companies include KW Plastics, Veolia, Custom Polymers, Plastipak Holdings, The Coca-Cola Company Incorporated, Suez, B. Schoenberg & Co., Fresh Pak Corporation, B&B Plastics, Green Line Polymers, Ultra Poly Corporation, Clear Path Recycling, and Jayplas. These companies leverage advanced recycling technologies, strategic partnerships, and sustainability-focused innovations to maintain their market positions.

Leading players are focusing on sustainability, technological innovation, and strategic acquisitions to gain a competitive edge. Companies such as The Coca-Cola Company and Veolia are investing in advanced recycling technologies, such as chemical and enzymatic recycling, to improve the quality of recycled polyethylene. Strategic partnerships with e-commerce and retail giants are also common, enabling customized packaging solutions. Additionally, firms are expanding their regional presence through acquisitions and investments in recycling infrastructure to meet growing demand and comply with regulatory requirements.

Key Developments

- In Mar 2025, Coca-Cola added “Recycle Me Again” to its 20-oz bottles (Coca-Cola, Diet Coke, Coke Zero) as part of its World Without Waste initiative aimed at eliminating 80 million pounds of new plastic.

- In March 2024, Suez’s Circular Polymer Plant in Bang Phli, Thailand, became the first to earn accreditation from Plastic Credit Exchange (PCX). It converts 30,000 tonnes/year of LDPE and LLDPE into quality PCR, boasts 94% water reuse, and avoids 35,000 tonnes of GHG emissions annually.

Companies Covered in Recycled Polyethylene Market

- KW Plastics

- Veolia

- Custom Polymers

- Plastipak Holdings

- The Coca-Cola Company

- Suez

- B. Schoenberg & Co.

- Fresh Pak Corporation

- B&B Plastics

- Green Line Polymers

- Ultra Poly Corporation

- Clear Path Recycling

- Jayplas

Frequently Asked Questions

The global recycled polyethylene market is projected to reach US$ 55.4 Bn in 2025.

The surge in demand for sustainable packaging and government-backed recycling initiatives is a key driver.

The Recycled Polyethylene market is poised to witness a CAGR of 8.5% from 2025 to 2032.

Advancements in recycling technologies, particularly chemical and enzymatic recycling, are a key opportunity.

KW Plastics, Veolia, Custom Polymers, Plastipak Holdings, and The Coca-Cola Company are key players.