- Processed Food

- Plant-based Butter Market

Plant-based Butter Market Size, Share, and Growth Forecast, 2025 - 2032

Plant-based Butter Market by Source (Almond, Oat, Soy, Coconut, Others), Nature (Organic, Conventional), Distribution Channel (B2B, B2C), and Regional Analysis for 2025 - 2032

Plant-based Butter Market Size and Trends Analysis

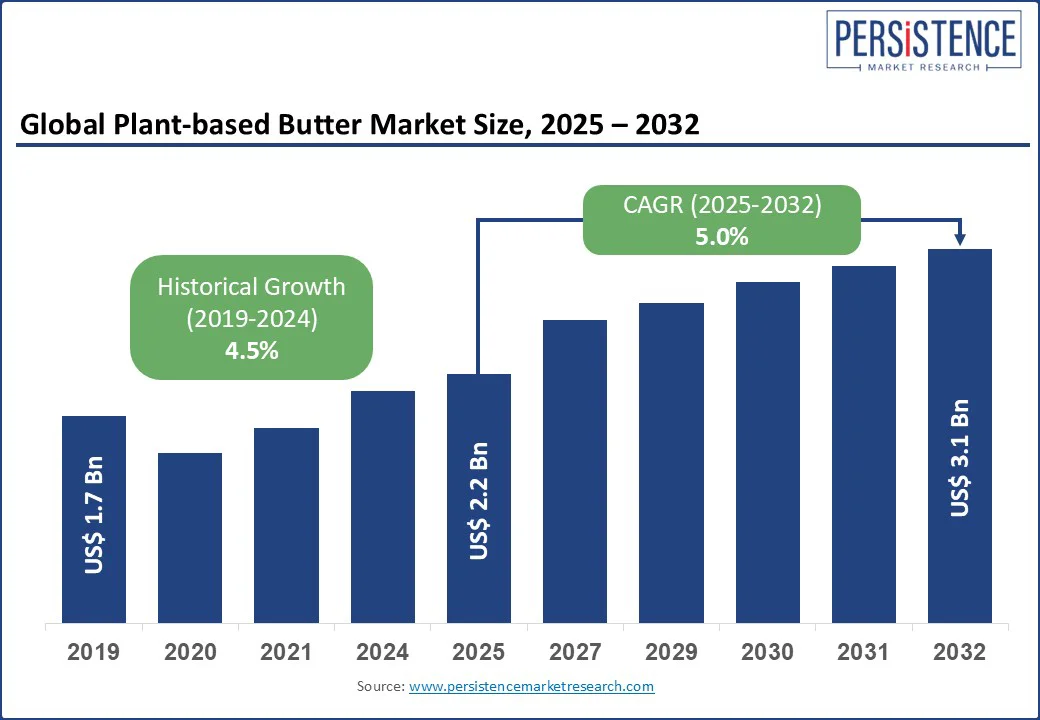

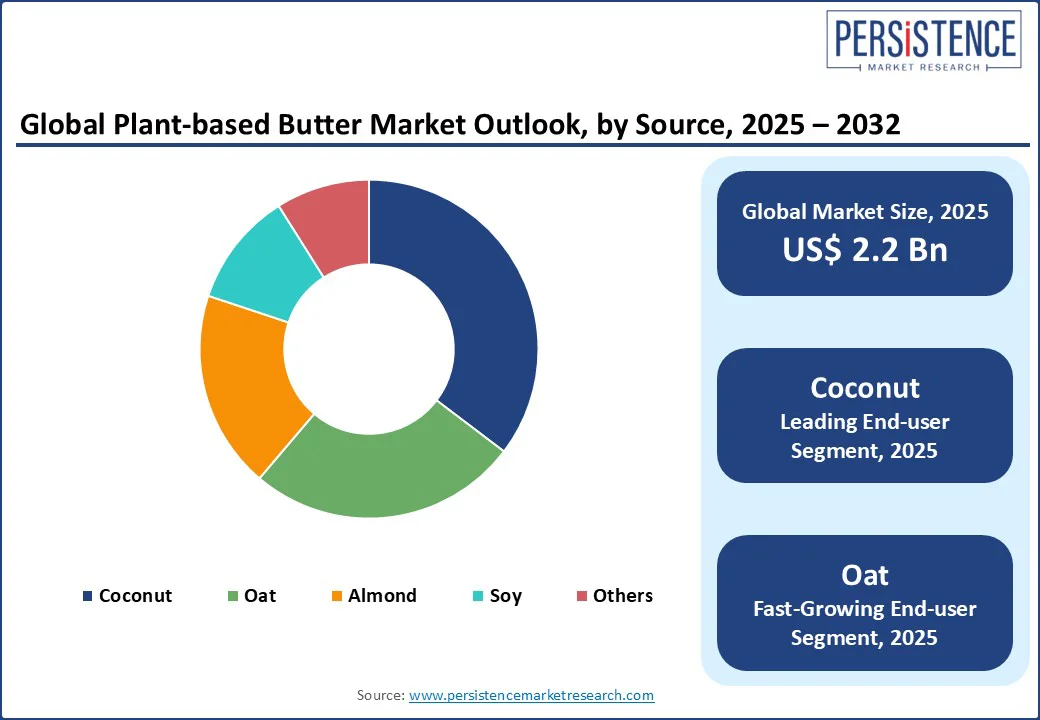

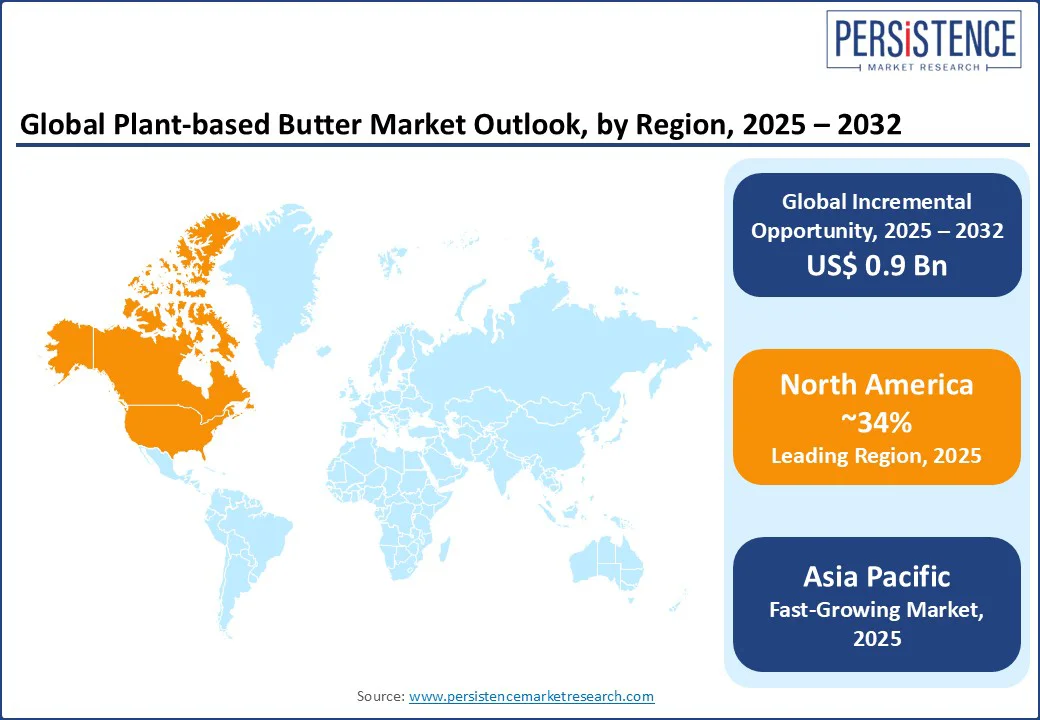

The global plant-based butter market size is likely to be valued at US$ 2.2 Bn in 2025 and reach US$ 3.1 Bn by 2032, registering a CAGR of 5.0% during the forecast period from 2025 to 2032.

The plant-based butter market has experienced steady growth in recent years, driven by increasing consumer demand for dairy-free alternatives, rising health consciousness, and the growing popularity of vegan and flexitarian diets.

The market growth is propelled by the need for sustainable, low-saturated-fat butter alternatives that cater to diverse dietary preferences and environmental concerns. Plant-based butter, derived from sources such as almond, oat, soy, and coconut, offers a healthier and eco-friendly substitute to traditional dairy butter, with applications in cooking, baking, and spreading across households, foodservice, and processed food industries.

Key Industry Highlights:

- Leading Region: North America, holding a 34% market share in 2025, driven by high health consciousness, a strong vegan consumer base, and advanced retail infrastructure.

- Fastest-growing Region: Asia Pacific, fueled by rising health awareness, increasing disposable incomes, and growing adoption of plant-based diets in countries such as China and India. Europe, advancing through sustainability-focused regulations and consumer demand for clean-label, plant-based products.

- Dominant Source: Coconut, commanding nearly 35.5% market share, reflecting its creamy texture and versatility in culinary applications.

- Leading Distribution Channel: B2C distribution channel holds the largest market share, accounting for 68% of sales in 2025, driven widespread availability of plant-based butter in retail outlets such as supermarkets, hypermarkets, and online platforms.

|

Global Market Attribute |

Key Insights |

|

Plant-based Butter Market Size (2025E) |

US$ 2.2 Bn |

|

Market Value Forecast (2032F) |

US$ 3.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.0% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.2% |

Market Dynamics

Driver: Rising Demand for Vegan and Health-Conscious Diets

The rising demand for vegan and health-conscious diets is a key driver for the plant-based butter market. Growing awareness of the environmental impact of animal agriculture, combined with health concerns over saturated fats and cholesterol found in dairy butter, is prompting consumers to seek plant-based alternatives.

Vegan diets, once niche, have entered the mainstream, fueled by social media influence, celebrity endorsements, and increased availability of plant-based options in retail and foodservice.

Plant-based butter, made from ingredients such as almond, soy, coconut, or oat, appeals not only to vegans but also to flexitarians and lactose-intolerant consumers seeking healthier spreads. These products often contain healthier fats, added nutrients, and fewer allergens, aligning with the clean-label movement.

For instance, brands like Miyoko’s Creamery and Kite Hill are introducing innovative, nutrient-rich plant-based butters to meet this growing demand. This shift in consumer preferences is creating sustained growth opportunities for manufacturers in the global market.

Restraint: High Production Costs and Limited Accessibility

High production costs and limited accessibility remain significant restraints for the plant-based butter market. Manufacturing plant-based butter often requires sourcing specialty ingredients such as almonds, coconuts, or oats, which are more expensive than traditional dairy inputs. Additionally, the processing techniques such as emulsification, flavor enhancement, and texture optimization are technologically intensive and increase production costs.

These higher costs are often passed on to consumers, making plant-based butter pricier than conventional dairy butter, which can limit mass-market adoption, particularly in price-sensitive regions. Limited accessibility also constrains growth, as plant-based butter is not yet widely available in all supermarkets, convenience stores, or emerging markets.

Distribution challenges, smaller production scales, and shelf-life considerations further restrict its presence in mainstream retail. For instance, premium products from brands like Miyoko’s Creamery or Kite Hill are typically found only in specialty stores or online platforms, limiting reach to broader consumer segments. These factors collectively slow widespread adoption despite growing demand.

Opportunity: Expansion of Plant-based Butter in Foodservice and Processed Foods

The expansion of plant-based butter in foodservice and processed foods presents a significant opportunity for market growth. As restaurants, bakeries, and cafes increasingly cater to vegan, lactose-intolerant, and health-conscious consumers, the demand for plant-based butter as a functional and sustainable ingredient is rising. It offers the same spreadability, flavor, and performance as traditional butter, making it suitable for baking, cooking, and finishing applications.

The processed food industry is also adopting plant-based butter to develop vegan snacks, spreads, confectionery, and ready-to-eat meals, responding to consumer demand for healthier and environmentally friendly alternatives. For instance, companies like Upfield and Conagra are partnering with foodservice chains to supply plant-based butter for bakery and culinary applications, enhancing menu inclusivity.

Additionally, the integration of plant-based butter into mass-produced baked goods allows manufacturers to label products as vegan or dairy-free, attracting a broader consumer base. This dual adoption in foodservice and processed foods is poised to drive significant market expansion globally.

Category-wise Analysis

Source Insights

Coconut-based butter holds the largest market share, expected to account for approximately 35.5% of the industry share in 2025. Its dominance stems from the creamy texture and mild flavor of coconut oil, which closely mimics traditional dairy butter, making it a popular choice for cooking, baking, and spreading.

Coconut oil’s natural solidity at room temperature and its high content of medium-chain triglycerides (MCTs) appeal to health-conscious consumers seeking heart-healthy fats. The widespread availability of coconut as a raw material and its versatility across various culinary applications solidify its market leadership.

The oat-based butter segment is the fastest-growing from 2025 to 2032. Oat butter’s creamy texture and neutral taste make it highly versatile for culinary applications, while its association with health benefits, such as high fiber and beta-glucan content, attracts consumers focused on cholesterol management. Additionally, oats are a sustainable crop with a lower environmental impact compared to other sources, aligning with the growing demand for eco-friendly products.

Nature Insights

Conventional plant-based butter dominates the sector, expected to account for 85% of the share in 2025. Its leadership is driven by its affordability and widespread availability in supermarkets, grocery stores, and convenience stores. Conventional products benefit from established supply chains and lower production costs compared to organic alternatives, making them accessible to a broader consumer base. The ease of access and competitive pricing ensure their continued dominance.

The organic plant-based butter segment is the fastest-growing from 2025 to 2032. Growing consumer preference for organic products, driven by concerns about synthetic pesticides, fertilizers, and GMOs, fuels this segment’s growth. Health-conscious consumers, particularly in developed regions, are willing to pay a premium for organic plant-based butter, which is perceived as safer and more sustainable. The increasing availability of organic products through online retail and specialty stores further accelerates adoption.

Distribution Channel Insights

The B2C distribution channel holds the largest market share, accounting for 68% of sales in 2025. This dominance is driven by the widespread availability of plant-based butter in retail outlets such as supermarkets, hypermarkets, and online platforms.

The growing health consciousness and rise of veganism have increased consumer demand for plant-based butter for household use, particularly for cooking and baking. The convenience and variety offered through B2C channels make them the preferred choice for individual consumers.

The B2B distribution channel is expected to grow from 2025 to 2032. This growth is driven by the increasing adoption of plant-based butter by foodservice providers, restaurants, bakeries, and institutional buyers. These entities are incorporating plant-based butter into their menus and products to cater to the growing demand for vegan and health-conscious options.

Regional Insights

North America Plant-based Butter Market Trends

North America, projected to hold a 34% market share in 2025, is a leading region in the plant-based butter market, driven by high health consciousness, a robust vegan consumer base, and advanced retail infrastructure. Consumers in the U.S. and Canada are increasingly shifting toward plant-based diets, motivated by concerns over cholesterol, saturated fats, and the environmental impact of dairy production.

This trend has fueled demand for plant-based butter alternatives made from almonds, soy, coconut, and oats, which provide healthier fat profiles and align with clean-label preferences. The region’s well-established retail networks, including supermarkets, specialty stores, and online platforms, make plant-based products widely accessible to consumers.

For instance, Upfield and Miyoko’s Creamery have expanded distribution across North American grocery chains, offering a variety of vegan butter products for both home and professional use. Additionally, strong foodservice adoption and marketing initiatives promoting health and sustainability are further driving market growth in the region.

Europe Plant-based Butter Market Trends

Europe's plant-based butter market is experiencing significant growth, driven by increasing health consciousness, environmental concerns, and a rising vegan population. Key trends shaping the domain include a shift toward cleaner labels, with consumers favoring products free from artificial additives and preservatives. Innovations in flavor and texture are enhancing the appeal of plant-based butter, making it more comparable to traditional dairy butter.

Almond-based butter remains the dominant segment, offering a familiar taste and texture, while other variants like coconut and oat-based butters are gaining popularity due to their unique flavors and health benefits. Distribution channels are diversifying, with increased availability in supermarkets, specialty stores, and online platforms, making plant-based butter more accessible to a broader consumer base. This expansion is further supported by strategic partnerships and investments from leading brands aiming to capitalize on the growing demand for plant-based alternatives.

Overall, Europe's plant-based butter market is poised for continued growth, driven by evolving consumer preferences and a supportive retail environment.

Asia Pacific Plant-based Butter Market Trends

The Asia Pacific plant-based butter market is experiencing robust growth, driven by rising health awareness, increasing disposable incomes, and the growing adoption of plant-based diets in countries such as China and India.

Consumers are increasingly seeking alternatives to traditional dairy butter due to concerns over cholesterol, saturated fats, and lactose intolerance. Urban populations, particularly millennials and health-conscious individuals, are leading the shift toward vegan and plant-based lifestyles.

Rising disposable incomes enable consumers to afford premium plant-based products, further boosting demand. Additionally, expanding retail and foodservice channels in the region are improving accessibility, making plant-based butter more widely available.

For instance, brands like Upfield and Califia Farms are entering Asian markets, offering almond-, coconut-, and oat-based butter variants tailored to local tastes. Almond-based butter remains particularly popular due to its familiar texture and flavor. Overall, health trends, economic growth, and dietary shifts position the Asia Pacific as a high-potential market for the expansion of plant-based butter.

Competitive Landscape

The Global Plant-based Butter Market is characterized by intense competition, driven by innovation in product formulations, sustainability initiatives, and regional expansion strategies. Key players compete on the basis of taste, texture, nutritional profile, and eco-friendly packaging.

Upfield leads with its widespread distribution and diverse product portfolio, while Miyoko’s Creamery focuses on artisanal, organic offerings. Emerging players like Fora Foods are disrupting the industry with innovative flavors and sustainable sourcing. Leading companies are investing in R&D to improve the taste, texture, and nutritional profile of plant-based butter.

Upfield and Conagra are focusing on expanding their distribution networks through partnerships with supermarkets and foodservice providers. Miyoko’s Creamery emphasizes sustainable sourcing and eco-friendly packaging to appeal to environmentally conscious consumers. Smaller players such as Fora Foods are leveraging online retail and social media marketing to reach niche consumer segments, particularly younger, health-conscious demographics.

Key Developments:

- In November 2023, Ripple Foods raised $49 million in its latest funding round, enhancing its position in the fast-growing dairy-alternative category. The company is known for its pea-based milk and is expanding its product offerings to include plant-based butter.

- In September 2024, Upfield introduced the world's first plastic-free, recyclable tub for its plant-based butters and spreads. This innovation, developed in collaboration with Footprint, MCC, and Pagès Group, aims to reduce plastic content by 80% across its portfolio by 2030.

Companies Covered in Plant-based Butter Market

- Upfield

- Miyoko’s Creamery

- Conagra, Inc.

- Califia Farms

- LLC

- Kite Hill

- Ripple Foods

- PBC

- Elmhurst Buttered Direct

- Milkadamia

- Fora Foods

- Naturli’ Foods A/S

Frequently Asked Questions

The Global Plant-based Butter Market is projected to reach US$ 2.2 Bn in 2025.

Rising demand for vegan and health-conscious diets and supportive government initiatives for sustainable food systems are key drivers.

The Plant-based Butter Market is poised to witness a CAGR of 5.0% from 2025 to 2032.

Expansion of plant-based butter in foodservice and processed food applications is a key opportunity.

Upfield, Miyoko’s Creamery, Conagra, Inc., and Naturli’ Foods A/S are among the key players.