- Beverages

- Almond Milk Market

Almond Milk Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Almond Milk Market by Formulation (Sweetened, Unsweetened), by Nature (Organic, Conventional), by Sales Channel (HoReCa, Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Online Retail, Others), by Regional Analysis, 2026-2033

Almond Milk Market Share and Trend Analysis

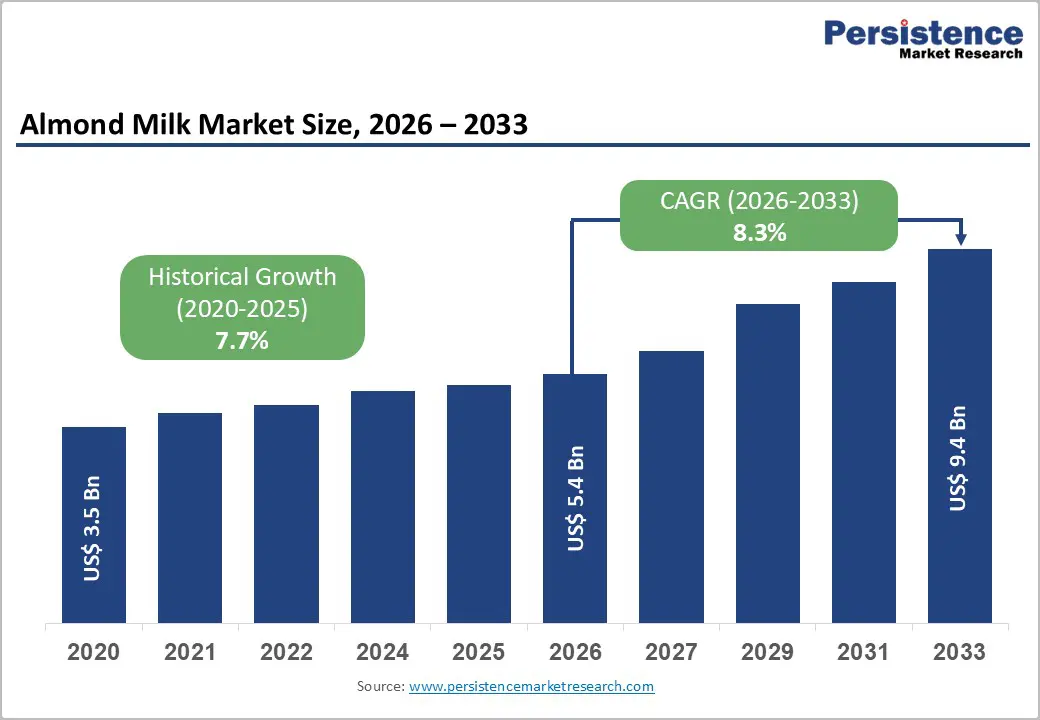

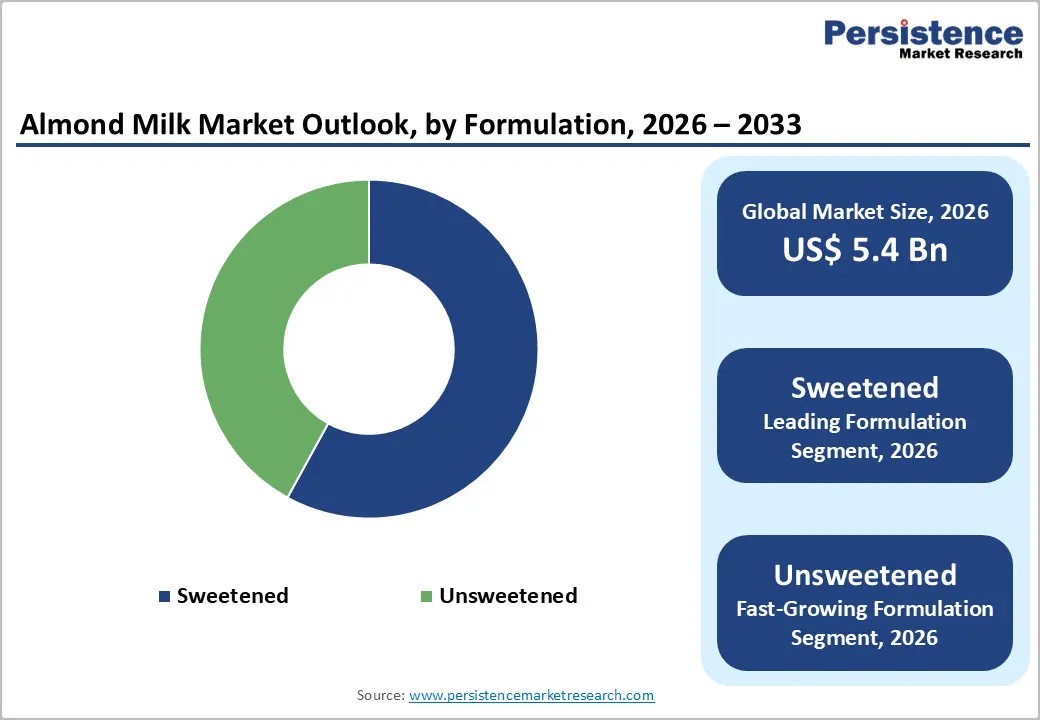

The global Almond Milk market size is expected to be valued at US$ 5.4 billion in 2026 and projected to reach US$ 9.4 billion by 2033, growing at a CAGR of 8.3% between 2026

The market's upward trajectory is primarily driven by the systemic shift in consumer dietary patterns toward plant-based nutrition and the surging prevalence of lactose intolerance. As a significant portion of the global population seeks dairy-free alternatives, Almond Milk has emerged as a preferred substitute due to its low-calorie profile and rich Vitamin E content. This transition is further supported by the expansion of retail networks and the entry of major food conglomerates into the dairy-alternative space.

Key Industry Highlights

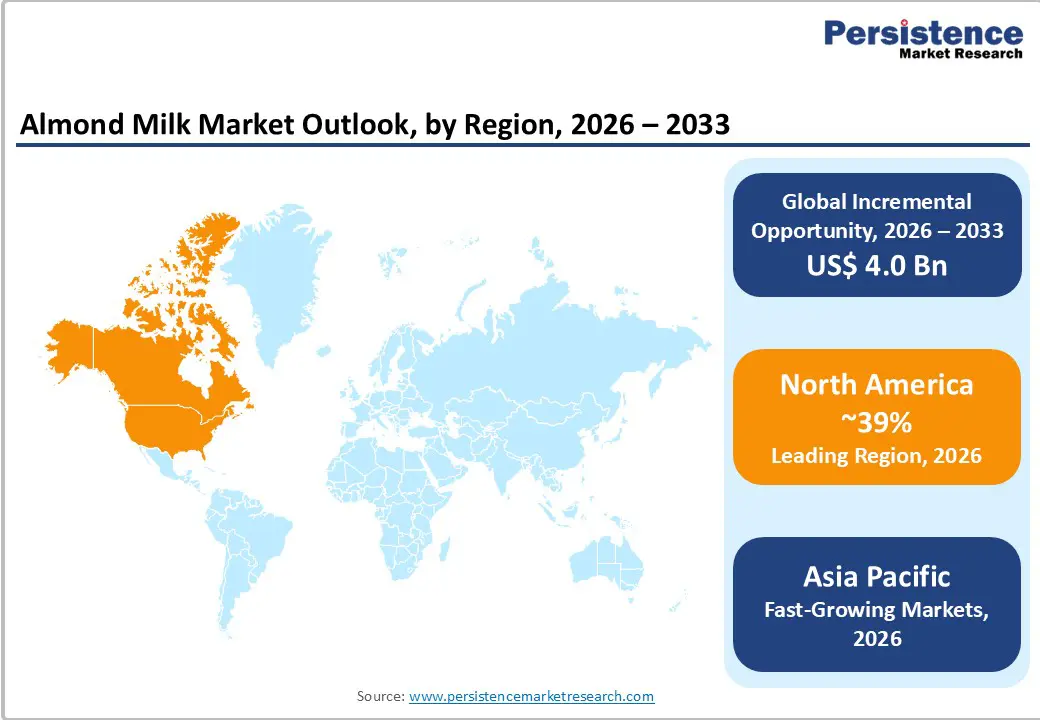

- Leading Region: North America dominates the global Almond Milk market with a 39% market share, driven by early adoption of plant-based diets, high lactose intolerance awareness, and a highly developed retail ecosystem.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market, fueled by exceptionally high lactose intolerance prevalence, rapid urbanization, and rising disposable incomes in China and India.

- Fastest-Growing Formulation Segment: Unsweetened Almond Milk is the fastest-growing formulation segment, supported by global sugar-reduction initiatives and rising health awareness.

- Dominant Nature Segment: Conventional Almond Milk holds the dominant share of the global market due to its lower price point, large-scale availability, and strong presence in mass retail channels.

- Market Drivers: The growing prevalence of lactose malabsorption and dairy protein allergies is a fundamental driver reshaping global beverage consumption.

- Key Developments: In July 2025, Premier Protein® launched an Almondmilk Protein Shake line to address protein-content limitations in dairy-free beverages; In January 2025, Califia Farms introduced a 3-ingredient Almond Milk in the UK, reinforcing clean-label positioning and minimal processing trends.

| Key Insights | Details |

|---|---|

| Global Almond Milk Market Size (2026E) | US$ 5.4 Bn |

| Market Value Forecast (2033F) | US$ 9.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.7% |

Market Dynamics

Driver – Growing Prevalence of Lactose Intolerance and Dairy Allergies

The primary driver for the Almond Milk market is the increasing medical necessity for dairy alternatives among the global population. According to the National Institutes of Health (NIH), approximately 68% of the world’s population has some degree of lactose malabsorption, with rates being significantly higher in Asia and Africa. In North America, nearly 36% of people face challenges digesting dairy products. This physiological reality forces a massive consumer base to seek substitutes that offer similar functional properties to cow’s milk without the digestive distress. Almond Milk, being naturally lactose-free and cholesterol-free, fills this gap perfectly. Furthermore, the rising awareness of milk protein allergies in infants and adults has propelled the demand for plant-based beverages. Major brands like Danone S.A. and Blue Diamond Growers have capitalized on this by fortifying their products with Calcium and Vitamin D, ensuring that health-conscious consumers do not compromise on essential nutrients while switching from traditional dairy.

Restraints – Nutritional Gaps and Competition from Emerging Plant-Based Alternatives

Despite its popularity, Almond Milk faces criticism regarding its low protein content compared to dairy and soy milk. A standard cup of Almond Milk contains only about 1 gram of protein, whereas cow’s milk provides around 8 grams. This nutritional disparity can be a restraint for consumers seeking complete meal replacements. Additionally, the market is facing intense competition from newer plant-based alternatives like Oat Milk, which is often perceived as creamier and more environmentally friendly due to lower water consumption during cultivation. Data suggests that as consumers become more educated about the "water footprint" of different crops, some are pivoting away from almonds toward grains and seeds. This competitive pressure requires Almond Milk manufacturers to invest heavily in fortification and marketing to maintain their market share against rapidly growing substitutes like those produced by Oatly Group AB.

Opportunity – Growth Potential in the Global HoReCa Sector and Coffee Culture The HoReCa

The HoReCa (Hotels, Restaurants, and Cafes) sector represents a massive untapped opportunity for Almond Milk expansion, particularly through "Barista Edition" products. As the specialty coffee culture spreads across Asia Pacific and Europe, there is a surging demand for plant-based milks that foam and steam like dairy. Developing specialized formulations that do not "curdle" in acidic coffee environments is a key technological frontier. Partnerships between almond producers and global coffee chains, such as Starbucks or Costa Coffee, have already shown that offering dairy-free options can increase foot traffic. Furthermore, the rising number of health-focused cafes in urban centers like Shanghai, Mumbai, and Dubai provides a fertile ground for Almond Milk integration into smoothies, bowls, and baked goods. Statistics indicate that the food service segment is one of the fastest-growing channels, offering manufacturers a way to achieve high-volume sales through bulk distribution agreements.

Category-wise Analysis

By Nature, conventional almond milk dominates the global market

In terms of nature, the Conventional segment currently commands the largest share of the market, estimated at approximately 72% in 2025. The primary reason for this leadership is the significantly lower price point and wider availability of conventional products in mainstream retail outlets like Walmart and Tesco. Conventional Almond Milk benefits from established large-scale agricultural practices that allow for competitive pricing, making it accessible to a broader demographic. Nevertheless, the Organic segment is witnessing a rapid surge in demand. Savvy consumers are increasingly wary of pesticide residues and are willing to pay a premium for USDA Organic or EU Organic certified products. The growth of the Organic segment is particularly strong in Europe and North America, where transparency in the supply chain and "farm-to-table" ethics are major purchasing influencers.

By formulation, unsweetened almond milk is expected to show promising growth in the global market

The Sweetened segment held the leading position in the Almond Milk market, accounting for a dominant 59% market share in 2025. This dominance is largely attributed to the taste preferences of mainstream consumers who are transitioning from traditional dairy to plant-based options. Many consumers find the natural nutty flavor of almonds to be slightly bitter or thin, making sweetened versions often flavored with Vanilla or Chocolate more palatable for direct consumption and cereal use. However, the Unsweetened segment is projected to be the fastest-growing category between 2026 and 2033 at a CAGR of 9.2% . This shift is driven by the global "War on Sugar" and rising health consciousness. As medical organizations like the American Heart Association (AHA) emphasize the reduction of added sugars to combat obesity and type 2 diabetes, more consumers are opting for original, unsweetened variants for their smoothies and cooking needs.

Region-wise Insights

North America Almond Milk Market Trends and Insights

North America is the leading region in the global Almond Milk market, commanding a substantial 39% market share in 2025. This leadership is rooted in the region's early adoption of plant-based diets and the presence of a highly sophisticated retail infrastructure. The United States is the primary hub for both production and consumption, with California serving as the heart of the global almond supply chain. Innovative marketing strategies by industry giants like Blue Diamond Growers (through their Almond Breeze brand) and Danone S.A. (through Silk) have successfully moved Almond Milk into the "mainstream" refrigerator.

Furthermore, the regulatory framework in the U.S. and Canada is conducive to market growth, with clear labeling standards and active fortification programs. Consumers in this region are increasingly looking for "clean-label" products that are free from carrageenan and artificial gums. The "barista" trend is also highly prevalent here, with Almond Milk being a staple in nearly every coffee shop across the continent. Recent developments show an increase in private-label brands by major grocers, which has lowered the entry price for many families, further solidifying the region's dominant position.

Asia Pacific Almond Milk Market Trends and Insights

Asia Pacific is the fastest-growing region in the Almond Milk market for the 2025-2032 forecast period. This explosive growth is driven by the massive population base in China and India, where lactose intolerance is exceptionally common. As disposable incomes rise and urbanization accelerates, consumers in these nations are shifting from traditional unpackaged dairy to branded, healthy alternatives. The "manufacturing advantage" of the region also plays a role, as local players are increasingly setting up processing units to reduce the cost of imported goods.

In Japan and South Korea, Almond Milk is gaining popularity as a beauty and skin-health beverage due to its high Vitamin E and antioxidant content. The market is also benefiting from favorable government initiatives in countries like China, which encourage the consumption of plant proteins to reduce the environmental burden of dairy farming. The expansion of e-commerce platforms like Alibaba and JD.com has made premium international and local almond brands accessible to consumers even in Tier-2 and Tier-3 cities, driving the rapid adoption of plant-based nutrition across the region.

Market Competitive Landscape

The global Almond Milk market is moderately consolidated, with a few major players holding significant market shares, while a growing number of regional and niche brands create a fragmented tail. Key market leaders like Danone S.A., Blue Diamond Growers, and Nestlé S.A. leverage their massive distribution networks and marketing budgets to maintain dominance. Their strategies often involve aggressive product diversification—such as launching "Barista Blends," protein-fortified variants, and sugar-free options—to cater to evolving consumer tastes.

Emerging business models focus on sustainability and D2C (Direct-to-Consumer) sales to build brand loyalty. Smaller players and startups are differentiating themselves through "cleaner" ingredient lists, often avoiding stabilizers like guar gum or xanthan gum to appeal to the ultra-health-conscious segment. Research and development trends are currently focused on improving the "mouthfeel" and creaminess of Almond Milk to better mimic dairy, as well as developing shelf-stable packaging that reduces the need for refrigeration during transport.

Key Developments:

- In July 2025, Premier Protein® expanded its portfolio with the launch of a new Almondmilk Protein Shake line, targeting consumers seeking dairy-free, high-protein beverages with clean taste and plant-based positioning.

- In January 2025, Califia Farms introduced a 3-ingredient plant-based milk in the UK, emphasizing minimal processing and ingredient transparency.

Companies Covered in Almond Milk Market

- Danone S.A.

- Blue Diamond Growers

- Oatly Group AB

- Campbell Soup Company

- Nestlé S.A.

- SunOpta Inc.

- Lactalis Group

- Pacific Foods

- Orgain, Inc.

- Hiland Dairy

- Others

Frequently Asked Questions

The global Almond Milk market is projected to be valued at US$ 5.4 Bn in 2026.

The primary drivers include the high prevalence of lactose intolerance, the rise of veganism, and increasing consumer awareness regarding the health benefits of low-calorie, nutrient-fortified plant-based diet.

The Global Almond Milk market is poised to witness a CAGR of 8.3% between 2025 and 2032

A major opportunity lies in the Horia sector and the development of Barista-grade blends. As coffee culture expands globally, providing almond-based alternatives that perform well in hot beverages is a key growth avenue.

Key market participants include Danone S.A., Blue Diamond Growers, Nestlé S.A., SunOpta Inc., and Califia Farms, all of whom are investing heavily in innovation and regional expansion