- Mining & Services

- Mining Drill Market

Mining Drill Market Size, Share, Trends, Growth, Regional Forecasts, 2026 to 2033

Mining Drill Market by Product Type (Rotary, Crawler, Top-Hammer, Diamond), End-User (Metal Mining, Mineral Mining, Coal Mining, Quarry Mining), Application (Surface, Underground, Exploration), and Regional Analysis for 2026-2033

Mining Drill Market Share and Trends Analysis

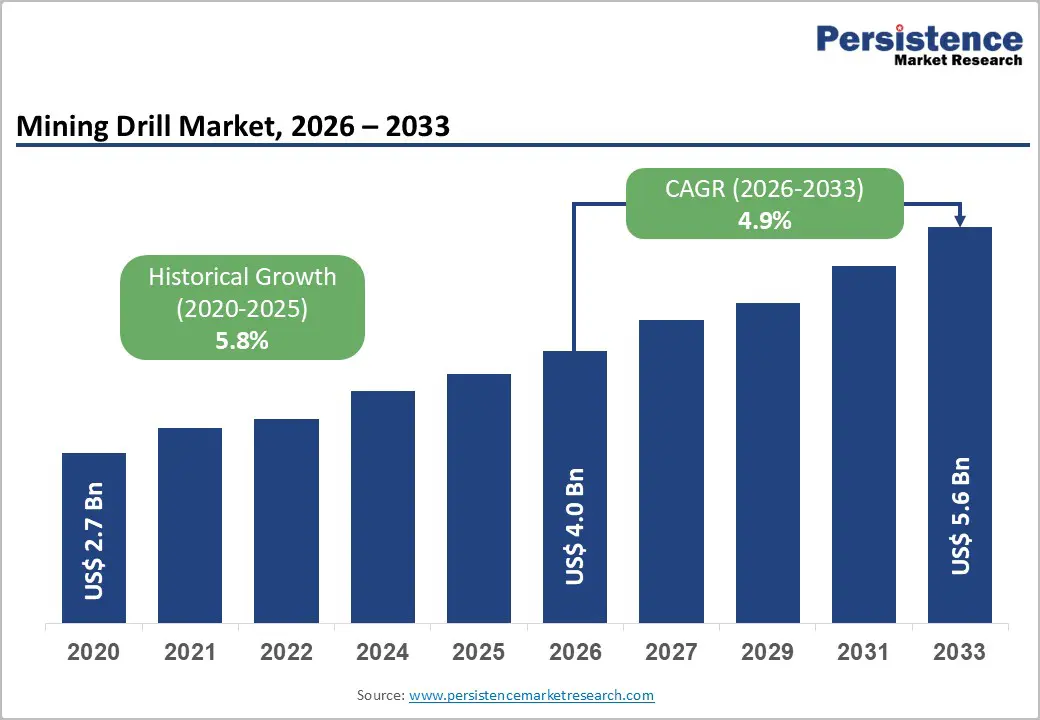

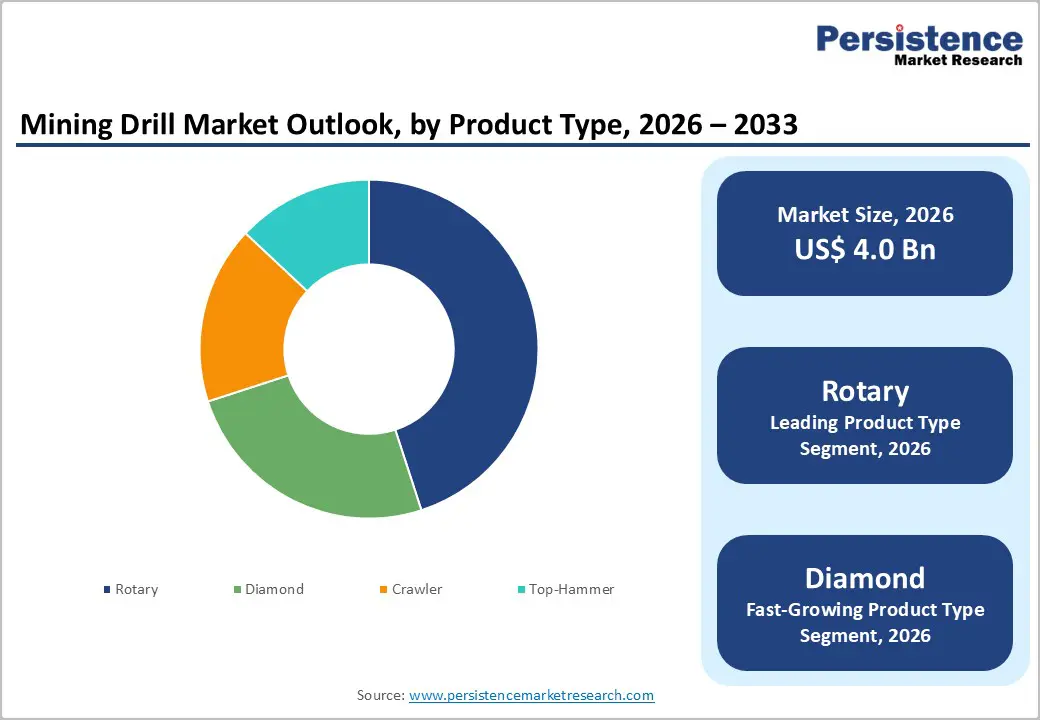

The global mining drill market size is likely to be valued at US$ 4.0 billion in 2026, and is projected to reach US$ 5.6 billion by 2033, growing at a CAGR of 4.9% during the forecast period 2026−2033. This sustained growth trajectory reflects the increasing global demand for mineral extraction driven by renewable energy transition, critical mineral requirements for battery technology, and accelerated infrastructure development in emerging economies.

The surge in lithium, cobalt, and rare earth element mining to support electrification initiatives, substantial capital investment in deepwater and underground mining operations, and technological advancement in automated and electric drilling equipment.

Key Industry Highlights

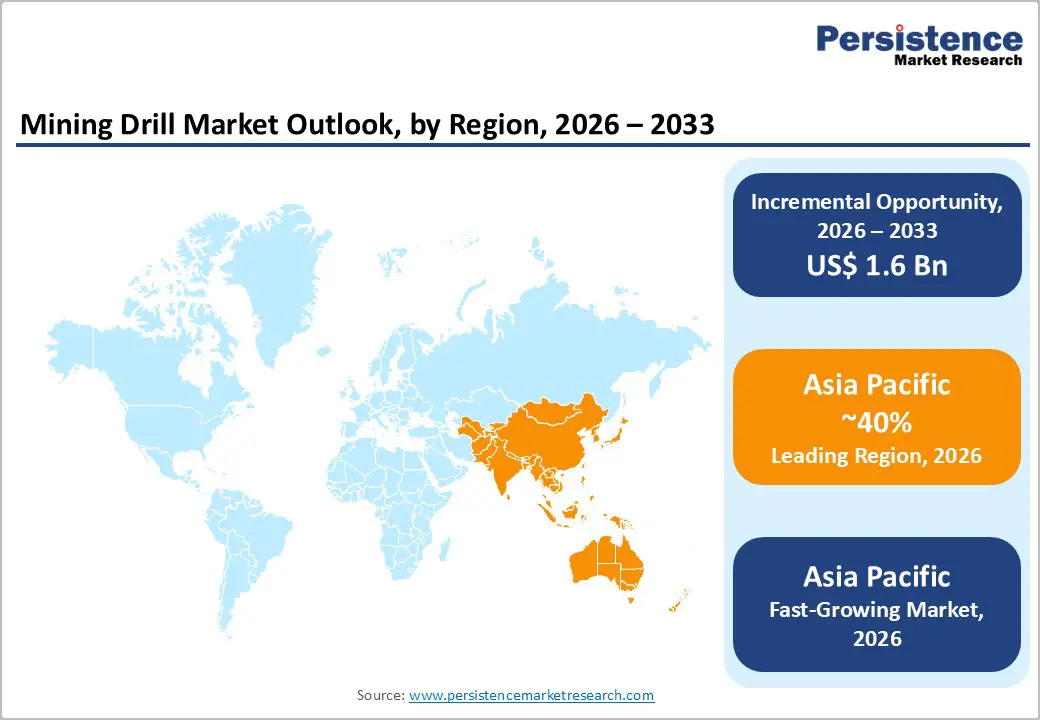

- Dominant Region & Fastest-growing Market: Asia Pacific is likely to be both the dominant and fastest-growing regional market through 2033, accounting for approximately 40% share, supported by its vast operations and processing hubs.

- Leading & Fastest-growing Product Type: Rotary currently dominates the product type segment, commanding approximately 45% of total market revenue, whereas diamond drill is likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Leading & Fastest-growing End-User: Metal mining represents the top end-user segment, capturing approximately 68% of market revenue share in 2026, while mineral mining is expected to be the fastest-growing segment over the 2026-2033 forecast period.

- Major Driver: The global shift toward renewable energy and electric vehicle (EV) adoption is creating unprecedented demand for minerals that support clean energy infrastructure.

- Opportunity Outlook: Manufacturers develop autonomous drilling systems that use sensors, Global Positioning System (GPS) technology, and machine learning (ML) algorithms.

| Key Insights | Details |

|---|---|

| Mining Drill Market Size (2026E) | US$ 4.0 Bn |

| Market Value Forecast (2033F) | US$ 5.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

DRO Analysis

Energy Transition and Critical Mineral Demand

The global shift toward renewable energy and EV adoption creates unprecedented demand for minerals that support clean energy infrastructure. Mining companies now ramp up exploration efforts to meet this need. Operators secure supply chains by developing new deposits, which boosts the market for mining drill equipment. The pressure to obtain mining permits intensifies competition among firms. As a result, companies procure advanced drilling systems, such as electric and autonomous rigs. These technologies gain premium value because they enhance efficiency in challenging environments. Industry leaders invest heavily in such equipment to stay ahead.

Firms will prioritize sustainable practices to align with environmental regulations. Autonomous drills will reduce human exposure to hazards, while electric systems will lower emissions at sites. Manufacturers respond by innovating designs that integrate seamlessly with digital monitoring tools. Operators gain actionable insights from real-time data, which optimizes resource extraction. Supply chain resilience strengthens as companies diversify sourcing from stable regions. Ultimately, this evolution will drive equipment upgrades across operations, ensuring long-term viability in a resource-constrained world.

Infrastructure Investment and Deep Mining Requirements

Depletion of high-grade surface ore deposits forces mining firms to shift toward deeper underground operations. Companies now require specialized drilling equipment that operates reliably in extreme conditions, such as high pressure, intense heat, and unstable rock formations. This transition demands tools with enhanced durability, precision, and energy efficiency. Operators upgrade their fleets to handle narrow veins and complex geology effectively. Suppliers gain a competitive advantage by offering systems that boost extraction rates while minimizing downtime and operational risks. The focus on underground methods accelerates innovation in compact, high-torque drills designed for confined spaces. Major infrastructure programs in Asia Pacific, particularly in China and India, sustain this mining expansion and create steady demand for raw materials.

Governments fund large-scale projects for roads, ports, power grids, and urban development, which spurs the need for commodities such as steel, cement, and aggregates. Firms respond by scaling up production at deeper sites to supply these essential materials reliably. Equipment providers position themselves strategically to deliver rugged drills suited for continuous, high-volume operations. Manufacturers integrate advanced features such as remote diagnostics and modular components for easier maintenance. This trend will transform global supply chains completely. Operators will achieve superior safety records and operational efficiency through smart sensors that enable real-time monitoring and predictive adjustments. Deeper mining practices will enhance resource recovery rates from challenging deposits. Ultimately, this evolution solidifies the critical role of cutting-edge drilling technology in securing long-term resource supplies for worldwide development needs.

Eco-Compliance and Sustainability Pressures

Stringent environmental regulations and rising sustainability concerns act as major restraints on the growth of the mining drill market. Governments worldwide enforce strict rules on operations. These rules aim to curb negative effects such as habitat loss, water contamination, and soil erosion. Mining firms now face mandates that demand cleaner processes and reduced ecological harm. Companies invest in solutions such as water recycling units (WRUs), dust control systems, and land restoration programs to meet these standards. Equipment suppliers adapt by designing drills with lower emissions and quieter operations. These requirements raise upfront costs and slow project approvals. As a result, they limit market expansion for traditional rigs. Operators balance compliance with profitability. They often delay equipment purchases as a result.

Pressure from advocacy groups and local communities pushes firms toward greener methods even further. Stakeholders demand transparency in impact assessments and long-term site rehabilitation plans. Manufacturers respond by embedding eco-friendly features such as electric powertrains and biodegradable lubricants into new drill models. This shift favors innovative suppliers who prioritize sustainability certifications. This integration transforms regulatory hurdles into competitive edges. Companies that lead in low-impact drilling will secure contracts in sensitive areas. Operators gain community support and faster permitting through proven environmental stewardship. Ultimately, this evolution ensures the mining drill sector aligns with global conservation goals while sustaining operations.

Commodity Price Swings and Market Instability

Fluctuating commodity prices and market volatility serve as key restraints on the mining drill market's expansion. The mining sector remains highly cyclical. Global economic shifts, supply-demand imbalances, and geopolitical tensions influence it heavily. Price swings in materials such as coal, iron ore, copper, and gold affect company profits directly. Firms cut exploration efforts during downturns. They postpone production ramps and capital spending as well. Operators defer purchases of drilling rigs in response. This caution stems from uncertain returns on investment. Suppliers face order delays and reduced backlogs as a result. Companies prioritize cash preservation over fleet upgrades in tough times.

Uncertainty also discourages funding from investors and banks for new projects. Financial institutions demand clearer outlooks before approving loans. Exploration budgets shrink under such pressure. Manufacturers respond by diversifying into service contracts and modular upgrades. They target resilient segments such as maintenance tools. Companies will build more flexible supply chains to weather cycles better. Leaders hedge risks through long-term offtake agreements with buyers. Operators gain stability by focusing on high-margin deposits. This approach sustains demand for versatile drills. Ultimately, volatility pushes the industry toward agile strategies. Equipment providers thrive by offering adaptable, cost-effective solutions that align with fluctuating conditions.

Advances in Drill Technology and Automation

Manufacturers develop autonomous drilling systems that use sensors, GPS technology, and machine learning algorithms. These systems deliver precise control over operations. They achieve faster penetration into rock formations and lower fuel use. Components experience less wear, which extends equipment life. Companies gain reliability in harsh environments through such innovations. Suppliers position themselves as partners in productivity gains. Operators upgrade fleets to match these capabilities, driving steady demand. Remote operation features let teams oversee rigs from central hubs. Personnel avoid direct exposure to hazards such as dust and collapses.

Real-time data analytics reveal performance trends, ground conditions, and machine status. Teams make swift adjustments based on these inputs. Predictive maintenance prevents breakdowns before they occur. Mining firms prioritize these tools to cut costs and boost output. Integration will transform site management completely. Leaders will deploy hybrid fleets that blend autonomy with human oversight. This setup enhances accuracy in complex deposits. Manufacturers thrive by bundling software with hardware offerings. They secure recurring revenue from updates and support. Ultimately, these advances align equipment with broader goals of efficiency and worker protection, fueling market growth.

Prospecting and Revealing New Mineral Reserves

Despite advances in geological surveying methods, companies leave vast mineral resources unexplored across the globe. Population expansion, urban development, and industrial growth fuel steady demand for metals and materials. The organization now intensifies efforts to locate fresh deposits that sustain long-term supply. Exploration teams launch extensive drilling campaigns to map resources and confirm reserves accurately. This push opens doors for equipment makers who supply robust tools for initial site assessments. Operators rely on these systems to evaluate potential in uncharted territories effectively. Advanced drilling rigs penetrate tough rock layers and deliver precise data on ore quality. Innovations allow access to remote sites with complex terrain, such as rugged mountains or dense forests.

Manufacturers equip machines with down-hole sensors and high-resolution logging tools. These features cut sampling times and improve success rates in discovery phases. Companies gain confidence to advance projects from exploration to full production. They will depend on next-generation drills to unlock deeper or harder-to-reach zones. Suppliers lead by offering portable, modular units that teams deploy quickly. This agility supports joint ventures in frontier regions. Operators secure early-mover advantages through superior resource intelligence. Ultimately, heightened exploration activity cements advanced drilling as a cornerstone of future mineral supply chains, spurring sustained market demand.

Category-wise Analysis

Product Type Insights

Rotary is poised to dominate by commanding approximately 45% of the mining drill market revenue share in 2026, driven by its versatility and efficiency across surface and underground mining operations. They use a rotating drill bit to crush and cut through diverse rock formations effectively. This design suits them for creating large-diameter holes in open pits and tunnels alike. Operators favor rotary drills for their adaptability to varied tasks, such as blast hole creation and grade control. The machines handle soft overburden or hard ore with consistent performance. Minimal downtime and straightforward maintenance enhance their appeal in demanding environments. Demand for rotary drilling equipment grows steadily as mining firms expand production. Companies prioritize rigs that integrate with automated systems for optimal output. Their broad applicability ensures a strong position in the evolving mining drill market.

Diamond drill is likely to be the fastest-growing segment during the 2026-2033 forecast period, fueled by precision needs in exploration and hard-rock extraction. These tools feature embedded diamond bits that slice through tough formations effectively. At the same time, they extract intact core samples for precise resource evaluation. Miners increasingly focus on deep, intricate deposits as shallow, accessible ores dwindle. Recent advances strengthen bit longevity under extreme wear. Automation integration allows seamless operation in isolated, high-stakes sites. Operators achieve superior data quality, which informs investment decisions confidently. This momentum positions diamond drills for accelerated adoption across global operations. Companies gain efficiency in delineating reserves for battery metals and rare earths. Suppliers respond with modular designs that cut deployment times.

End-User Insights

Metal mining is anticipated to hold an estimated 68% of the market revenue share in 2026. This segment focuses on extracting key metals such as iron, copper, gold, and aluminum. Industries such as construction, automotive production, and electronics rely heavily on these materials. Companies now seek efficient, advanced rigs to meet rising needs. High-performance machines thrive in tough conditions, such as deep shafts and variable rock. Operators depend on robust drills for both new deposit exploration and project expansions, since these tools ensure precise blasting patterns and ore recovery.

Mineral mining is expected to be the fastest-growing segment over the 2026-2033 forecast period. Mineral mining centers on extracting non-metallic resources such as limestone, gypsum, and phosphate. These materials serve key roles in construction, agriculture, and chemical production. Industries expand rapidly, which heightens the need for reliable supplies. Firms now deploy specialized drilling rigs tailored to these softer formations. Operators achieve clean cuts and uniform fragmentation to optimize processing downstream. Advanced technologies enhance precision and speed in these operations. Machines integrate sensors for real-time adjustments, reducing overbreak and waste. Demand rises as projects scale to feed infrastructure booms and fertilizer needs.

Regional Insights

Asia Pacific Mining Drill Market Trends

Asia Pacific is likely to be both the leading and fastest-growing regional market for mining drills between 2026 and 2033, accounting for approximately 40% of the market share in 2026. China anchors demand with vast operations and processing hubs, even as provincial rules temper certain activities. India unlocks potential through road networks, power plants, and fresh surveys for untapped ores. Japan leads in crafting high-tech rigs that serve local and international clients. ASEAN countries such as Indonesia, Vietnam, and the Philippines host active sites and draw global capital for prospecting. Lower production costs give manufacturers an edge, while brisk urbanization fuels steady equipment needs.

Infrastructure projects for highways, cities, and solar farms consume huge volumes of aggregates and metals. Operators ramp up drilling to supply these builds reliably. Economic expansion and raw material hunger sustain procurement cycles. Firms pour funds into smart rigs and eco-friendly upgrades to boost output. Suppliers set up local plants and repair depots, which cuts lead times and builds loyalty. Automation will redefine site efficiency across the region. Leaders secure contracts by blending affordability with reliability. This environment rewards agile players who tailor solutions to local rocks and climates.

Europe Mining Drill Market Trends

Europe secures a strong position in the global market for mining drills through advanced manufacturing and resource strategies. Germany, the United Kingdom, and France lead as innovation centers. They produce cutting-edge rigs for domestic and export markets. The European Union (EU) Critical Raw Materials Act spurs exploration for lithium, cobalt, and rare earth elements. Governments push firms to source materials locally, which boosts drilling activity. Operators upgrade fleets to meet strict environmental rules under directives such as Directive 2006/21/EC. These standards require emission controls and waste handling systems. Companies favor low-emission drills that align with green policies.

Eastern European nations open doors for expansion via road projects and new mines. Regulatory alignment across the EU simplifies compliance for suppliers. Mature rivals compete on technology and service quality. Partnerships between makers and operators target automation and sustainability features. Firms invest in digital tools for predictive upkeep and real-time monitoring. Manufacturers will embed these capabilities standardly, turning rules into market strengths. Leaders gain edges through certified eco-rigs that speed approvals. Operators cut downtime and risks with smart systems. This focus creates a premium segment for innovative drills. Suppliers thrive by localizing support networks.

North America Mining Drill Market Trends

North America is the second largest regional market for mining drill through established operations and an innovation focus. The United States leads regional demand with active exploration for copper, gold, and rare earth elements. Large operators pursue critical minerals to support supply chains. Commodity cycles challenge growth, but technology upgrades counter slowdowns effectively. Firms invest in automation to lift productivity amid economic shifts. Regulatory bodies enforce environmental, social, and governance (ESG) standards strictly. These rules push the adoption of clean rigs and safety features. Companies prioritize drills that pass compliance checks swiftly.

Renewable energy projects for solar farms, wind turbines, and battery plants drive steady mineral needs. Operators ramp up surveys to feed these initiatives reliably. Consolidation among major players concentrates buying power, which squeezes suppliers on pricing and service. Manufacturers respond with tailored digital platforms and Internet of Things (IoT) integrations. Predictive tools cut unplanned stops and optimize fleets. Companies will standardize these systems across sites, blending human oversight with machine precision. Leaders secure loyalty through end-to-end support packages. This mature market rewards providers who align tech with sustainability mandates. Suppliers gain ground by localizing production and training programs.

Competitive Landscape

The global mining drill market structure is moderately consolidated, dominated by leading players such as Atlas Copco, Epiroc, Sandvik, Caterpillar Inc., and Komatsu Ltd. These players collectively capture 55-60% of the market share. Market concentration rises moderately after recent consolidation among top players. Specialized technology providers and regional manufacturers still find ample opportunities to compete effectively. Firms differentiate through cutting-edge innovations such as autonomous controls and data analytics.

Strong aftermarket services build customer loyalty and extend equipment life. Geographic reach secures contracts in diverse markets, from Asia-Pacific hubs to North American sites. Operators favor suppliers with proven uptime records and rapid support networks. Leaders balance scale with agility to capture niche segments. This landscape rewards adaptability amid evolving demands for sustainable, high-performance rigs.

Key Industry Developments

- In February 2026, Cambria Gold Mines launched a 27,000-meter infill diamond drilling program at its Premier Gold Project in British Columbia to upgrade resource confidence and support restart plans. Operations began at the Premier-Northern Lights deposit near the 2,500 tpd mill, starting from surface and shifting to underground drilling in the Prew Zone at 12.5-meter spacing to target high-grade ore shoots.

- In February 2026, Banyan Gold Corp. launched a fully funded 40,000-meter diamond drilling program at its AurMac Project in Yukon's Tombstone Gold Belt, deploying four rigs to advance Airstrip and Powerline deposits while exploring regional targets. The effort targets expanding high-grade gold and silver zones, converting inferred resources to indicated, and testing geophysical anomalies via AI analysis.

- In November 2025, Almonty Industries initiated a major 14,000-meter diamond drilling program at its Panasqueira tungsten mine in Portugal, using three rigs over 12 months at a cost of € 2.5 million. The campaign targets Level 4 expansion to boost annual output, extend mine life, and refine the resource model based on prior vein discoveries.

Companies Covered in Mining Drill Market

- Epiroc AB

- Sandvik AB

- Caterpillar Inc.

- Atlas Copco AB

- Boart Longyear

- Komatsu Ltd.

- Revathi Equipment

- Furukawa Co. Ltd.

- Schramm Inc.

- Tesmec S.p.A.

- Liebherr Group

- Metso Outotec

- Robbins Company

- Herrenknecht AG

Frequently Asked Questions

The global mining drill market is projected to reach US$ 4.0 billion in 2026.

The market is driven by rising demand for critical minerals in renewables and electric vehicles, which is spurring exploration drilling.

The market is poised to witness a CAGR of 5.3% from 2026 to 2033.

Major opportunities lie in building autonomous rigs and real-time analytics, which can boost safety and output.

Atlas Copco, Epiroc, Sandvik, Caterpillar Inc., and Komatsu Ltd. are some of the key players in the market.