- Bulk Chemicals

- Mining Flotation Chemicals Market

Mining Flotation Chemicals Market Size, Share, and Growth Forecast 2026 - 2033

Mining Flotation Chemicals Market by Chemical Type (Collectors, Frothers, Flocculants, Depressants, Grinding Aids, and Others), Ore Type (Sulfide Ores and Non-Sulfide Ores), and Regional Analysis, 2026 - 2033

Mining Flotation Chemicals Market Size and Share Analysis

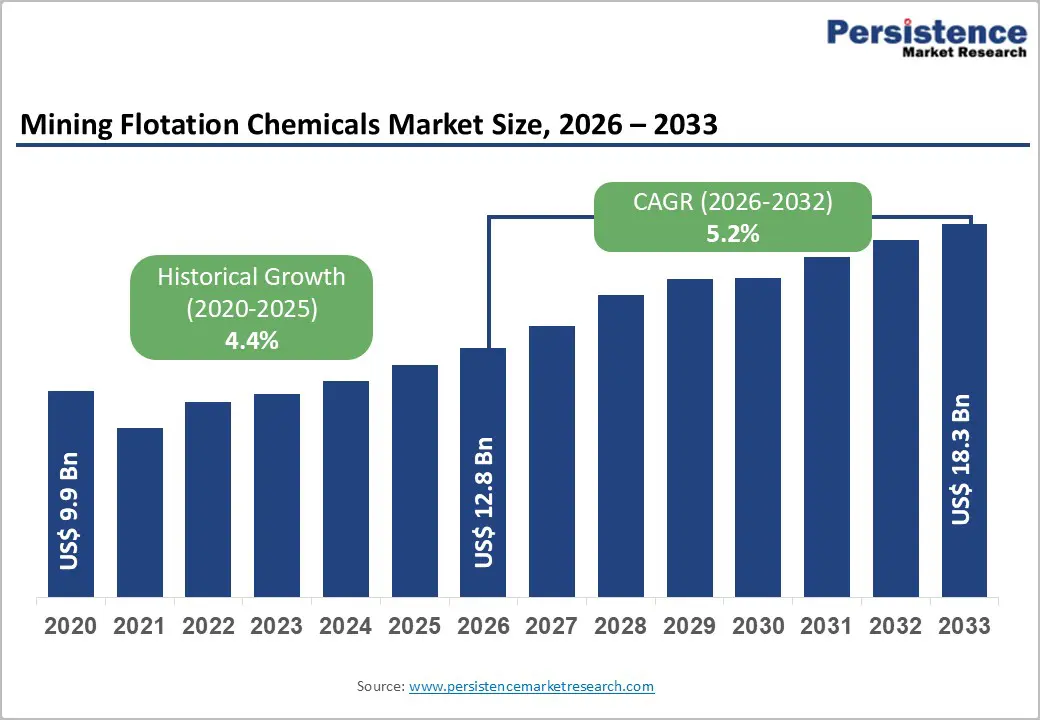

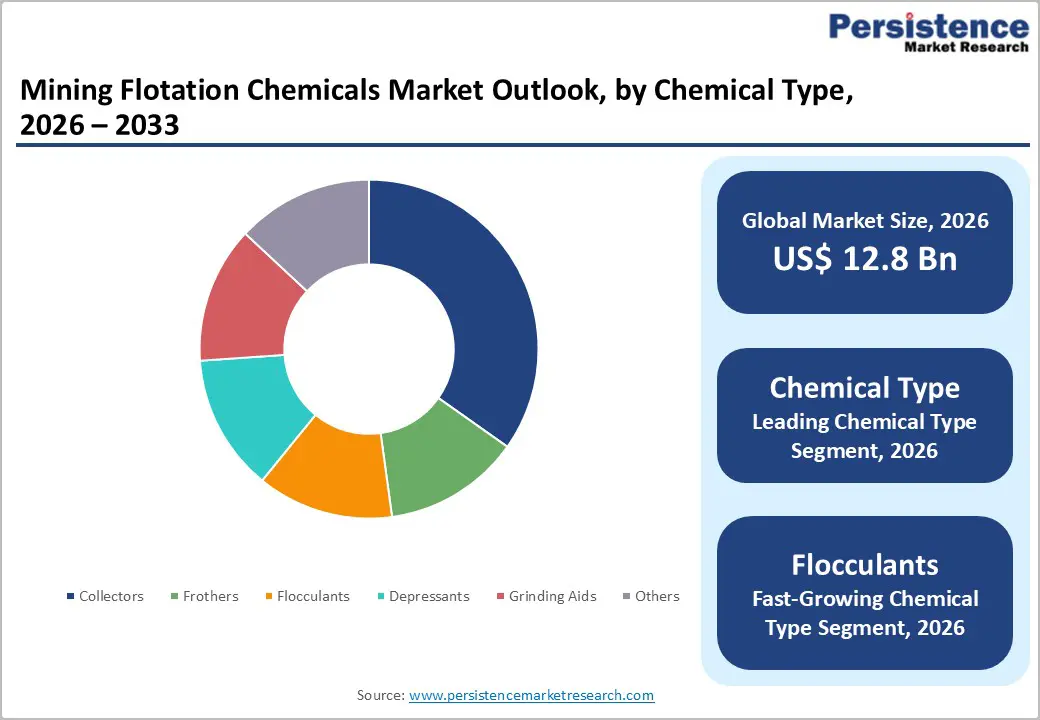

The global mining flotation chemicals market size is likely to be valued at US$ 12.8 billion in 2026 and is projected to reach US$ 18.3 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033.

The mining flotation chemicals market is experiencing sustained expansion driven by escalating global demand for base and precious metals, including copper, gold, zinc, and lead, substantial investments in mining infrastructure, particularly across emerging markets in the Asia Pacific and Latin America, and technological advancement in flotation reagent formulations enabling efficient processing of increasingly complex lower-grade ore deposits.

Key Market Highlights

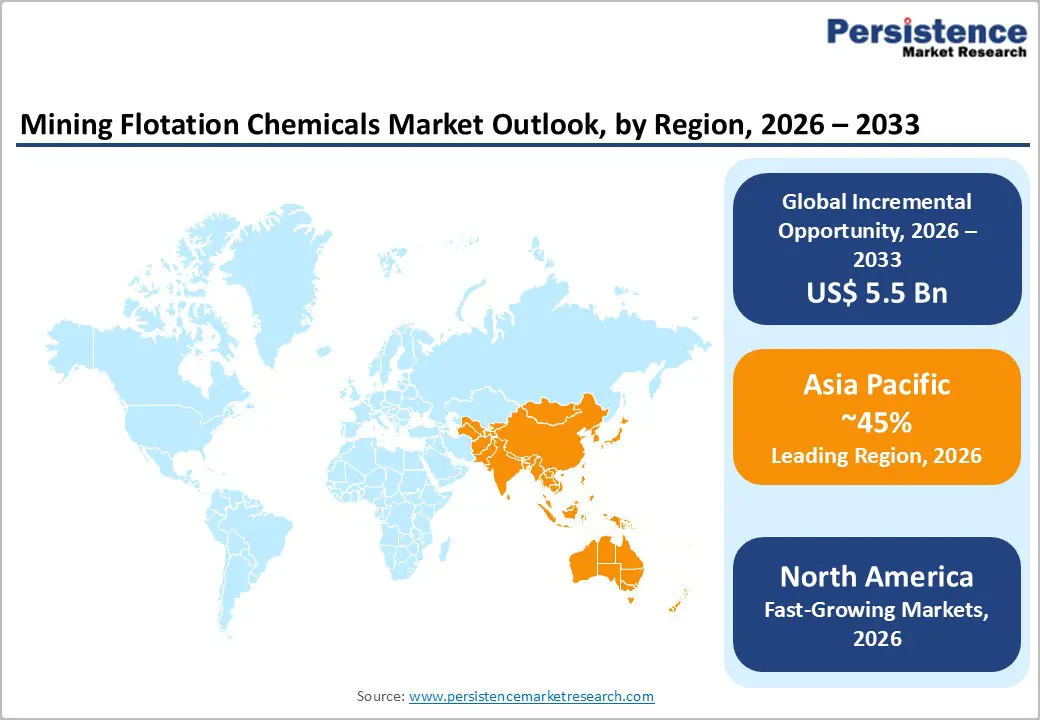

- Leading Region: Asia Pacific represents the dominant regional market, accounting for approximately 45% global flotation chemical demand, with China's mining sector dominance, India's rapid capacity expansion, and emerging mining activities across Indonesia and the Philippines supporting accelerated regional market growth.

- Fastest Growing Region: North America maintains a strong regional presence with approximately 24.4% global market share, driven by established mining infrastructure, advanced technological capabilities, and stringent environmental regulations.

- Leading Chemical Type: Collectors dominate the chemical type segment, with approximately 38% market share, driven by essential functionality for mineral separation, advanced selectivity, and ongoing innovation in biodegradable collector formulations.

- Growing Ore Type: Sulfide ore applications account for approximately 61% of the market, reflecting extensive extraction of copper, lead, zinc, and nickel globally, whereas non-sulfide ores are the fastest-growing segment, with a 5.5% CAGR, driven by expanding demand for precious metals and rare earths.

- Key Market Opportunity: Critical minerals mining expansion and wastewater treatment applications represent significant long-term market opportunities, with the energy transition driving copper demand and circular-economy principles.

| Key Insights | Details |

|---|---|

| Mining Flotation Chemicals Market Size (2026E) | US$ 12.8 Bn |

| Market Value Forecast (2033F) | US$ 18.3 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.2% |

| Historical Market Growth (2020 - 2025) | 4.4% |

Market Dynamics

Drivers - Expanding Mining Production and Rising Demand for Base Metals

The expansion of global mining production, coupled with rising demand for base and precious metals, is a fundamental driver of the global mining flotation chemicals market. Rapid urbanization, industrialization, and infrastructure development, particularly in emerging economies, are significantly increasing the consumption of metals such as copper, zinc, lead, nickel, iron ore, gold, and silver. Copper demand is accelerating due to its critical role in renewable energy systems, electric vehicles, power transmission, and electronics, while precious metals continue to see strong demand from jewelry, investment, and high-technology applications.

To meet this growing demand, mining companies are expanding production capacity, reopening dormant mines, and developing new deposits, many of which are characterized by lower ore grades and more complex mineralogy. Flotation reagents are essential for addressing these challenges, as they enable the selective separation of target minerals from gangue, thereby making mining operations economically viable. Collectors enhance the hydrophobicity of desired mineral particles, allowing them to attach to air bubbles and rise to the surface, while frothers stabilize these bubbles to form an effective mineral-rich froth.

Declining ore quality requires higher reagent dosages and more specialized chemical formulations to maintain recovery rates and concentrate purity. Growth in large-scale mining projects across Latin America, Africa, and the Asia-Pacific further supports demand for flotation chemicals, as these regions hold substantial reserves of base and precious metals. Flotation remains the most cost-effective and scalable beneficiation technique for sulfide and increasingly complex oxide ores, reinforcing its central role in modern mining operations.

Technological Innovation and Sustainable Reagent Development

Technological innovation and the development of sustainable flotation reagents are increasingly driving growth and transformation within the global mining flotation chemicals market. Mining companies face mounting pressure to improve operational efficiency while reducing environmental impact, water consumption, and chemical toxicity. In response, chemical manufacturers are investing heavily in research and development to create advanced reagent formulations that offer higher selectivity, improved recovery rates, and reduced dosage requirements. Innovations such as tailored collectors for complex and polymetallic ores, high-performance frothers with enhanced bubble stability, and multifunctional modifiers are enabling mines to process lower-grade ores more efficiently.

Sustainability considerations are reshaping reagent portfolios, with growing adoption of biodegradable, low-toxicity, and plant-based flotation chemicals that comply with increasingly stringent environmental regulations. These eco-friendly alternatives help mining operators reduce tailings toxicity, improve water recyclability, and lower long-term remediation costs without compromising metallurgical performance.

Digitalization and process-optimization technologies, including real-time monitoring and reagent-optimization software, further enhance the effectiveness of advanced flotation chemicals by enabling precise dosing and adaptive control. This integration of chemistry with process automation enhances plant productivity and reduces reagent waste. As environmental, social, and governance (ESG) standards become central to mining investment decisions, demand for innovative and sustainable flotation reagents is expected to rise steadily.

Restraints- Stringent Environmental Regulations and Environmental Impact Concerns

Stringent environmental regulations and growing concerns about the ecological impacts of mining activities constitute a major restraint on the global mining flotation chemicals market. Many conventional flotation reagents, particularly certain collectors and frothers, are associated with toxicity, poor biodegradability, and long-term persistence in tailings and process water. Governments and regulatory authorities across North America, Europe, and parts of the Asia Pacific are enforcing stricter discharge limits, chemical usage controls, and mine-closure compliance requirements to mitigate soil and water contamination. These regulations increase the cost and complexity of reagent selection, storage, handling, and disposal for mining operators.

In some regions, restrictions or outright bans on specific chemical formulations force mines to reformulate processes or switch to alternative reagents, which may be less effective or more expensive. Compliance also requires additional investments in water treatment, tailings management, and environmental monitoring systems, thereby indirectly reducing growth in reagent consumption. Heightened scrutiny from local communities and environmental groups further intensifies pressure on mining companies to limit chemical usage.

Volatility in Metal Prices and High Operating Costs in Mining

Volatility in global metal prices and persistently high operating costs pose another significant restraint on the mining flotation chemicals market. Prices of base and precious metals are influenced by global economic cycles, geopolitical tensions, trade policies, and supply-demand imbalances, leading to periods of sharp price fluctuations. During downturns, mining companies often curtail production, delay expansion projects, or place high-cost operations on care and maintenance, directly reducing demand for flotation reagents. At the same time, rising costs for energy, labor, equipment maintenance, water management, and environmental compliance are exerting pressure on mining margins.

Flotation chemicals represent a recurring operational expense, and in cost-sensitive environments, mining operators may seek to reduce reagent consumption, negotiate lower prices, or switch to cheaper alternatives. Budget constraints can also limit the adoption of advanced or specialty flotation reagents, despite their performance benefits. This cautious spending behavior, particularly during prolonged periods of low metal prices, can suppress market growth and create demand uncertainty for flotation chemical suppliers.

Opportunities - Critical Minerals Mining Expansion for Energy Transition and Electric Vehicle Production

The accelerating shift toward renewable energy, battery storage systems, and electrified transportation is significantly increasing demand for minerals such as lithium, nickel, cobalt, copper, graphite, and rare earth elements. Many of these critical minerals are found in complex and low-grade ore bodies, requiring advanced flotation processes to achieve economically viable recovery levels. Flotation chemicals play a crucial role in selectively separating valuable mineral phases, improving concentrating purity, and maximizing metal recovery from challenging deposits. Specialized collectors and modifiers are increasingly required to process polymetallic ores and fine particles common in battery and EV-related minerals.

Governments worldwide are promoting domestic sourcing of critical minerals through policy incentives and strategic investments, thereby driving new mine development and beneficiation facilities. This trend directly drives demand for high-performance and customized flotation reagents. As the energy transition accelerates and EV adoption expands globally, sustained investment in critical minerals mining is expected, positioning flotation chemicals as an essential enabler of supply chain resilience and long-term market growth.

Wastewater Treatment and Circular Economy Applications Development

The growing focus on wastewater treatment and circular economic practices within the mining industry presents a significant opportunity for the mining flotation chemicals market. Mining operations are under increasing pressure to reduce freshwater consumption, minimize waste generation, and improve environmental performance. Flotation chemicals are being adapted and applied beyond traditional ore beneficiation to support wastewater treatment, tailings management, and resource recovery from waste streams. In mining wastewater treatment, flotation-based processes using specialized reagents help remove suspended solids, oils, and dissolved metals, enabling water reuse within processing plants. This reduces reliance on freshwater sources and lowers operational costs.

Flotation chemicals are increasingly used in the reprocessing of tailings and mine waste to recover residual valuable metals, supporting circular economy objectives. These applications extend mine life, improve overall resource efficiency, and reduce the environmental footprint of mining operations. As regulatory requirements tighten and sustainability targets become more stringent, demand for flotation chemicals designed for wastewater treatment and circular recovery applications is expected to grow, creating new revenue streams and long-term opportunities for chemical suppliers.

Category-wise Analysis

Chemical Type Insights

Collectors, representing the dominant flotation chemical type, account for approximately 38% of the market, making them the leading revenue generator across flotation applications. Collectors alter mineral surface properties, thereby selectively enhancing flotation yield and enabling preferential attachment of valuable minerals to air bubbles during flotation. Xanthate-based collectors, including sodium isopropyl xanthate (SIPX) and sodium isobutyl xanthate (SIBX) dominate sulfide ore flotation, with potassium ethyl xanthate widely deployed in copper-gold sulfide ore processing, achieving recovery efficiencies exceeding 85% for copper and 60% for gold.

The segment's dominance reflects essential functionality in mineral separation, widespread deployment across diverse ore types, and continuous innovation in collector chemistry, enabling improved selectivity and environmental sustainability. Advanced collector formulations incorporating biodegradable alternatives and enhanced selective properties are expanding market opportunities while supporting regulatory compliance objectives. The segment is projected to expand at approximately 5.9% CAGR through 2032, representing the fastest-growing chemical type segment driven by ongoing innovation and increasing demand for performance-optimized flotation solutions.

Ore Type Insights

Sulfide ore flotation represents the dominant application segment, accounting for approximately 61% of mining flotation chemical demand, driven by extensive global extraction of base metals, including copper, lead, zinc, and nickel from sulfide ore bodies. Sulfide ores require specialized flotation chemistry to achieve economic recovery from increasingly complex ore compositions and lower-grade deposits. Copper sulfide ores constitute the largest sulfide application, with flotation chemistry enabling selective recovery of copper minerals while depressing iron sulfides and gangue.

Lead-zinc flotation applications require sophisticated multi-stage flotation circuits utilizing specialized collectors, frothers, and depressants to achieve selective mineral separation.

Nickel sulfide ore processing, particularly relevant to battery metal demand, increasingly employs advanced flotation chemistry to support energy transition objectives. The segment's dominance reflects established processing methodologies, extensive deployment of infrastructure, and continuous technological advancement that support efficient sulfide ore beneficiation. Non-sulfide ores, accounting for approximately 39% of demand, are experiencing accelerated growth at a 5.5% CAGR, driven by expanding precious metals and rare earth mining, and are the fastest-growing ore type segment through 2033.

Regional Insights

North America Mining Flotation Chemicals Trends

North America maintains a significant presence, driven by established mining infrastructure, advanced technological capabilities, and substantial copper, gold, and coal production in the United States and Canada. Environmental regulations, including EPA requirements and sustainability initiatives by major mining corporations, are shaping market dynamics, leading to the adoption of eco-friendly and biodegradable flotation reagents. North America accounts for approximately 24.4% global flotation reagents market share in 2026, reflecting the region's developed mining sector and technological sophistication.

Advanced mineral-extraction technologies and a commitment to sustainable mining practices continue to support demand for specialized flotation chemical formulations. Strategic investments by leading companies in biodegradable reagent development and digital monitoring systems are enhancing market competitiveness while supporting environmental compliance objectives across North American mining operations.

Europe Mining Flotation Chemicals Trends

Europe represents a mature flotation chemicals market characterized by stringent environmental regulations, an emphasis on sustainability, and technical innovation in reagent formulations. The UK government's Net Zero 2050 initiative encourages the adoption of environmentally friendly mining chemicals, creating regulatory drivers for biodegradable frothers, depressants, and dispersants. Germany, France, and Spain maintain advanced chemical manufacturing and research capabilities that support continuous innovation in flotation reagents.

The region's regulatory harmonization through European Commission directives promotes the adoption of sustainable and environmentally compliant reagent systems. Urban mining initiatives, particularly metal recycling from electronic waste, are expanding the use of flotation chemicals in non-traditional sectors. European emphasis on circular economy principles and resource efficiency supports the development of versatile flotation chemistry solutions applicable across diverse end-use industries.

Asia Pacific Mining Flotation Chemicals Trends

Asia Pacific represents the dominant regional market, accounting for approximately 45-50% global mining flotation chemical demand, driven by China's mining dominance, producing 51.8% of global coal and substantial precious and base metal mining across the region. China's mining sector has contributed significantly to the Asia-Pacific's flotation chemical demand, driven by ongoing expansions in copper, lithium, and other critical mineral mining.

India's Ministry of Coal is targeting Atma-Nirbhar (self-reliance) through rapid capacity expansion, planning to open 100 new mines by FY2029-30, adding 500 million tonnes per annum capacity, with 13 mines operationalized in FY2024-25 (83 million tonnes capacity) and over 20 additional mines planned for FY2025-26. Indonesia and the Philippines are emerging as significant players with rich copper and gold deposits attracting substantial mining investments. The region's rapid industrialization, expanding mining infrastructure, and focus on improving mineral-processing efficiency create sustained demand drivers for flotation chemical formulations, supporting economic growth across the Asia-Pacific through 2033.

Competitive Landscape

The mining flotation chemicals market exhibits moderate consolidation, with leading global manufacturers including Solvay S.A., BASF SE, AkzoNobel N.V., and Clariant AG capturing significant market share through vertically integrated production, extensive research and development capabilities, and global distribution networks. Solvay S.A. launched biodegradable reagents designed for copper ore flotation, advancing sustainable product portfolios. Companies compete on product efficacy, selectivity for specific ore types, environmental sustainability credentials, and development of customized formulations.

Strategic partnerships between chemical suppliers and major mining corporations facilitate co-development of proprietary flotation solutions tailored to unique ore bodies and processing challenges. Emerging players focus on specialized applications and regional market penetration, with smaller firms capitalizing on niche opportunities in specific mineral processing applications. Investment in digital technologies, automation, and data analytics optimization represents competitive differentiation strategy supporting operational efficiency and cost reduction across flotation processes.

Key Market Developments

- In December 2024, Solvay SA announced development of new biodegradable reagent specifically designed for copper ore flotation applications, reducing environmental impact while enhancing separation selectivity and operational efficiency in large-scale mining operations.

- In September 2024, BASF SE launched an advanced flotation reagent formulation for industrial mineral processing, incorporating enhanced collector selectivity, thereby improving recovery rates and reducing energy consumption relative to conventional alternatives.

- In June 2024, AG introduced specialized froth flotation reagents for precious metal extraction, thereby improving resource efficiency in gold and silver mining operations while meeting environmental compliance requirements.

Companies Covered in Mining Flotation Chemicals Market

- Solvay S.A.

- BASF SE

- Senmin International (Pty) Ltd

- SNF S.A.S.

- DowDuPont Inc.

- AkzoNobel N.V.

- Clariant AG

- Chevron Phillips Chemical Company LLC

- QiXia TongDa Flotation Reagent Co. Ltd.

- CTC Mining

- Yantai Humon Chemical Auxiliary Co. Ltd.

- ArrMaz

- Tieling Flotation Reagents Co., Ltd

- Coogee Chemicals Pty Ltd.

- Axis House (Pty) Ltd.

Frequently Asked Questions

The global mining flotation chemicals market is projected to reach US$ 18.3 billion by 2033 from US$ 12.8 billion in 2026, representing a compound annual growth rate (CAGR) of 5.2% during the forecast period.

Primary demand drivers include expanding global mining production and rising demand for base and precious metals including copper, gold, zinc, and lead across construction, automotive, electronics, and renewable energy sectors.

Collectors are the dominant type of flotation chemicals, accounting for approximately 38% of the total market share and emerging as the primary contributor to revenue generation across a wide range of flotation applications.

Asia Pacific represents the dominant regional market, accounting for approximately 45% global flotation chemical demand, driven by China's mining sector dominance producing 51.8% of global coal and substantial precious and base metal mining.

Primary opportunities include critical minerals mining expansion for energy transition and electric vehicle production driving demand for specialized flotation chemistry in lithium, cobalt, nickel, and rare earth mineral extraction, wastewater treatment and circular economy applications.

Key market players include BASF SE, Solvay S.A., Clariant AG, AkzoNobel N.V., Chevron Phillips Chemical, SNF S.A.S., DowDuPont Inc., Huntsman Corporation, Kemira OYJ, Evonik Industries, and Orica Limited.