- Inks, Coatings, Adhesives & Sealants (ICAS)

- Mining Dust Suppressants Market

Mining Dust Suppressants Market Size, Share, and Growth Forecast, 2026 - 2033

Mining Dust Suppressants Market by Product Type (Wet Dust Suppressants, Dry Dust Suppressants, Foam Suppressants), Application (Road Management, Longwall Mining, Stockpiles, Others), End-User (Coal Mining, Metal Mining, Mineral Mining), and Regional Analysis for 2026-2033

Mining Dust Suppressants Market Share and Trends Analysis

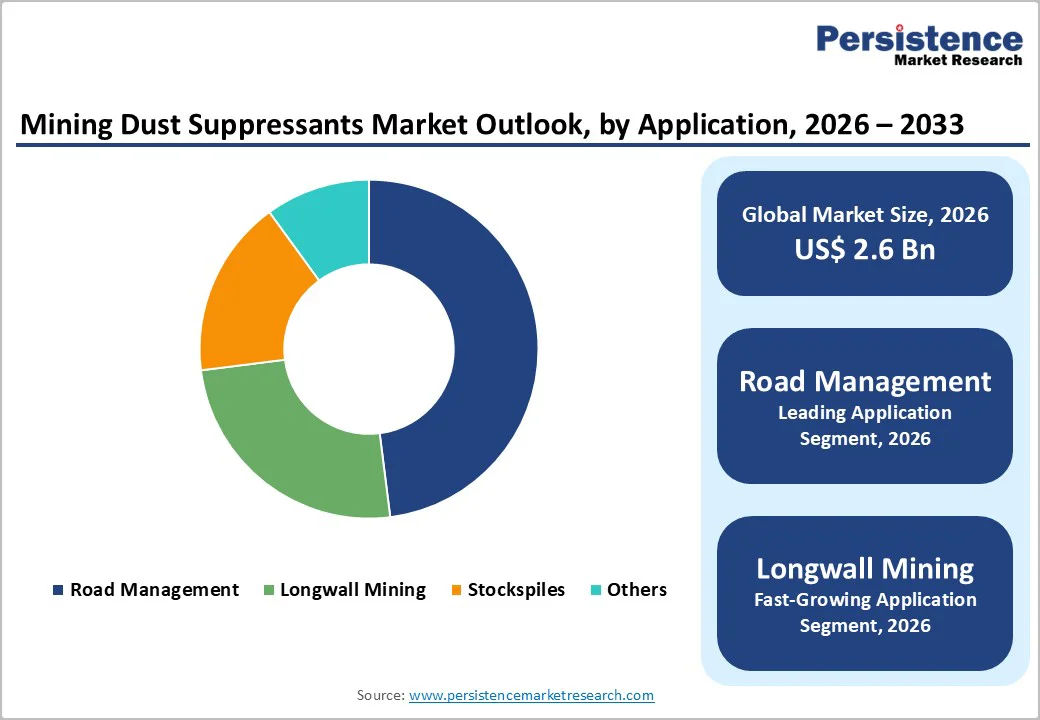

The global mining dust suppressants market size is likely to be valued at US$ 2.6 billion in 2026, and is projected to reach US$ 4.0 billion by 2033, growing at a CAGR of 6.1% during the forecast period 2026−2033.

The market is experiencing robust expansion driven by stringent environmental regulations, increasing occupational health awareness, and technological advancements in suppressant formulations. Mining operations globally face persistent challenges from fugitive dust emissions a critical concern affecting both worker safety and environmental compliance. As governments implement increasingly rigorous air quality standards and occupational exposure limits, mining companies are accelerating their adoption of effective dust control solutions.

Key Industry Highlights

- Product Type Dominance: Wet dust suppressants are poised to lead with about 62% revenue share in 2026, whereas dry dust suppressants are likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Application Leadership: Road management is slated to dominate with an estimated 48% revenue share in 2026, while longwall mining is expected to grow the fastest through 2033.

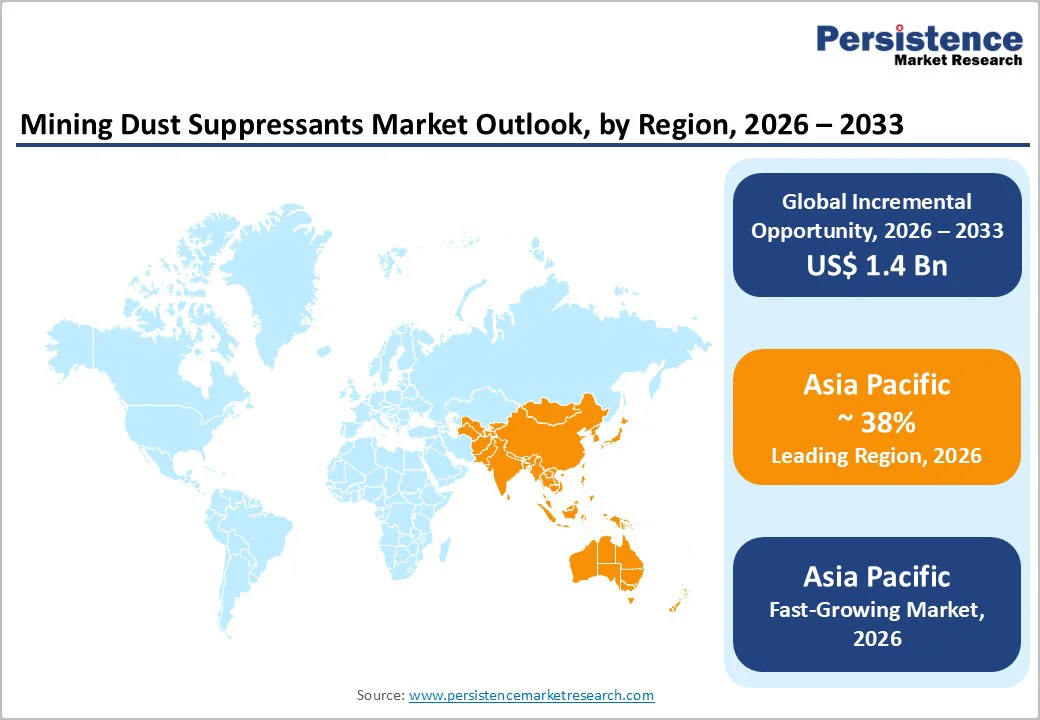

- Dominant Region: Asia Pacific is set to command about 38% market share in 2025, supported by extensive mining activity across China, India, Australia, and Indonesia.

- Fastest-growing Market: Asia Pacific is predicted to be the fastest-growing regional market through 2033 due to extensive mineral extraction operations in emerging economies.

- Market Drivers: Stringent environmental and worker-safety regulations, expanding global mining output, and increasing adoption of higher-performance, sustainable dust control solutions are the driving forces for the market.

- Market Opportunities: The digital transformation of the mining industry is creating significant opportunities for intelligent dust suppressant deployment systems.

| Key Insights | Details |

|---|---|

| Mining Dust Suppressants Market Size (2026E) | US$ 2.6 Bn |

| Market Value Forecast (2033F) | US$ 4.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Stringent Regulatory Frameworks for Dust Control

Mining operations across jurisdictions face intensifying regulatory pressure to control fugitive dust emissions and protect worker respiratory health. Authorities in key mining regions have introduced comprehensive respirable dust regulations, requiring companies to monitor exposure levels closely and implement effective dust management practices across both surface and underground operations. International organizations and labor bodies highlight the serious health risks of prolonged hazardous dust inhalation, emphasizing proactive prevention over reactive treatment of occupational diseases.

In response, countries with large, established mining industries have implemented mandatory dust monitoring programs and clearly defined exposure limits. For example, India's Ministry of Coal employs comprehensive air quality management strategies in mining areas, including surface miners, fog canons, mist sprayers, wheel washing systems, and mechanical road sweepers, to minimize fugitive dust generation. Continuous Ambient Air Quality Monitoring Systems (CAAQMS) connected to state pollution control board (SPCB) websites provide real-time monitoring, while First Mile Connectivity (FMC) projects aim to replace conventional road transport with mechanized loading and rail/conveyor systems. Regulators are increasingly enforcing these requirements through strict inspections and substantial penalties for non-compliance, prompting mining companies to treat dust control as a core element of their safety and sustainability strategies.

High Implementation and Maintenance Costs

Small and medium-scale mining enterprises confront substantial financial obstacles when implementing comprehensive dust suppressant programs. Advanced suppressant formulations featuring specialized polymers and chemical compounds demand higher pricing structures compared to basic water-based alternatives, with costs escalating further when precise application methodologies become necessary. Beyond product acquisition, organizations must absorb expenditures encompassing application equipment procurement, monitoring infrastructure installation, personnel training programs, and sustained maintenance activities throughout operational lifecycles. Underground mining operations introduce additional complexity, necessitating customized delivery systems that integrate seamlessly with existing ventilation networks and substantially increase both capital investment requirements and recurring operational expenses.

This financial environment shapes purchasing behavior across the dust suppressant market in consequential ways. Cost pressure consistently drives mining operators toward products requiring minimal upfront investment, even when such choices necessitate more frequent reapplication or deliver inferior dust containment performance. Suppliers positioned to offer financing solutions, flexible payment arrangements, or performance-based pricing models can differentiate themselves within this price-sensitive buyer segment. Mining companies that establish capital budgeting frameworks demonstrating return on investment (ROI) through reduced health and safety incidents, improved air quality compliance, enhanced employee productivity, and minimized regulatory penalties create compelling business cases for dust suppressant adoption.

Integration with Autonomous Mining Technologies

The digital transformation of the mining industry is creating significant opportunities for intelligent dust suppressant deployment systems. Autonomous haul trucks, drilling equipment, and material handling systems can be integrated with automated suppressant application technologies, allowing product usage to be optimized using real-time operational data. Sensor networks that monitor particulate matter levels, wind conditions, and traffic patterns enable precise, targeted application that reduces waste while enhancing overall dust control performance. For example, in December 2025, First Quantum Minerals successfully deployed automated drilling technology at its Sentinel mine in Kalumbila, Zambia, becoming the first mining operation in the country to use the system. The technology delivered a 33% increase in drill holes completed, 20+ hour continuous operation capability, and extremely high global positioning system (GPS) positioning accuracy.

This technological convergence is particularly attractive to mining operators seeking to improve operational efficiency and sustainability simultaneously. By linking dust control to broader digital and automation strategies, companies can better align environmental compliance with cost management and productivity objectives. Providers that develop IoT-enabled application systems and advanced data analytics platforms for dust management optimization are well positioned to serve premium customer segments focused on operational excellence and long-term performance.

Category-wise Analysis

Product Type Insights

Wet dust suppressants are likely to lead with an approximate 62% of the market revenue share in 2026. These water-based solutions, including plain water, surfactant-enhanced formulations, and chemical additives, remain the most widely deployed dust control method across mining operations due to their accessibility, ease of application, and lower upfront costs. Wet suppressants are particularly prevalent in surface mining operations, haul roads, and stockpile management applications where immediate dust knockdown is required. Their market leadership reflects the mining industry's established infrastructure for water distribution and the operational familiarity of maintenance personnel with application techniques.

Dry dust suppressants are slated to be the fastest-growing segment during the 2026-2033 forecast period. This accelerated growth stems from superior performance characteristics including extended control duration, reduced water dependency, and enhanced binding properties for fine particulate matter. Mining operations in water-scarce regions and underground applications are increasingly adopting dry suppressant technologies. Advanced polymer formulations create durable crusts on exposed surfaces that withstand vehicle traffic and environmental weathering, reducing reapplication frequency and total cost of ownership despite higher initial product costs. The segment's growth is further supported by innovations in environmentally benign formulations that address sustainability concerns.

Application Insights

Road management is slated to dominate with roughly 48% of the mining dust suppressants market revenue share in 2026. This segment encompasses haul roads, access roads, mine site perimeters, and transportation corridors within mining complexes. Haul roads represent the single largest dust generation source in surface mining operations, with heavy-duty trucks continuously traveling unpaved routes that extend for dozens of kilometers within large-scale mining sites. The segment's market leadership stems from multiple factors: the sheer scale of road networks in mining operations, continuous vehicle traffic generating persistent dust clouds, visibility and safety concerns requiring immediate dust control, and community relations pressures as road dust frequently migrates beyond mine boundaries.

Longwall mining is expected to be the fastest-growing from 2026 to 2033. This underground coal mining method involves mechanized shearing of coal faces in large rectangular blocks, generating enormous quantities of respirable dust in confined spaces with limited ventilation. The segment's accelerated growth is driven by the global expansion of longwall mining operations, particularly in China, India, Australia, and the United States, where this method offers superior productivity and resource recovery compared to conventional room-and-pillar mining.

End-User Insights

Coal mining is anticipated to command approximately 45% of the market revenue share in 2026, reflecting coal's continued significance in global energy production and the particularly hazardous nature of coal dust. Coal mining generates substantial respirable crystalline silica and combustible dust, creating both health and safety imperatives for rigorous dust control. Major coal-producing nations, including China, India, the United States, Australia, and Indonesia, maintain extensive coal mining operations that require ongoing dust management across exploration, extraction, processing, and transportation phases. The coal mining sector faces intense regulatory oversight regarding dust exposure limits, driving consistent demand for effective suppressant solutions despite broader energy transition trends affecting coal consumption.

Metal mining is forecasted to be the fastest-growing segment throughout the 2026-2033 period, propelled by the consistently high global demand for copper, lithium, nickel, cobalt, and rare earth elements essential for renewable energy technologies, electric vehicles, and advanced manufacturing. The expansion of metal mining operations which creates substantial market opportunities for dust suppressant providers. Metal ore mining often involves hard rock formations that generate particularly hazardous crystalline silica dust during drilling, blasting, and crushing operations. Large-scale copper and gold mining projects, frequently located in remote regions with stringent environmental permitting requirements, implement comprehensive dust management programs as conditions of operational approval.

Regional Insights

Asia Pacific Mining Dust Suppressants Market Trends

Asia Pacific is anticipated to lead with an estimated 38% of the mining dust suppressants market share in 2026, as well as post the highest 2026-2033 CAGR, driven by extensive mining activity across China, India, Australia, and Indonesia, along with growing mineral extraction in other emerging economies. The dominance reflects the sheer scale of its coal, iron ore, base metal, and industrial mineral operations, as well as an ongoing transition from smaller, fragmented sites to larger, highly mechanized mines. China’s role as a leading producer of coal and a wide range of industrial minerals generates substantial demand for dust control solutions, while initiatives to improve environmental protection and mine safety are accelerating the adoption of advanced suppressant technologies and integrated dust management systems.

India represents a high-growth opportunity, supported by rising coal production for power generation and increasing extraction of iron ore, bauxite, and other minerals, underpinned by systematic dust control programs. Across Southeast Asia, countries such as Indonesia, Vietnam, and the Philippines are expanding mining to support industrialization and infrastructure development, driving demand for tailored suppressant solutions suited to diverse climatic conditions. At the same time, regional manufacturing strengths in China and India are enabling local production and competitive pricing, although inconsistent regulatory enforcement, strong price sensitivity among smaller operators, and limited technical support in remote areas remain key challenges.

Europe Mining Dust Suppressants Market Trends

The Europe mining dust suppressants market is characterized by moderate, regulation-driven growth and a strong emphasis on environmental and occupational health standards. The region’s market dynamics are shaped by the European Union (EU) stringent regulatory frameworks, which set detailed requirements for worker protection and for minimizing environmental impact. Germany, the United Kingdom, France, and Spain represent core markets, supported by coal mining, aggregate extraction, and industrial mineral operations. Germany's lignite mining activities and the U.K.'s remaining deep coal operations continue to sustain demand for dust suppressants, even as Europe gradually transitions away from coal-fired power generation.

EU-wide regulatory harmonization has standardized dust control requirements, creating opportunities for suppliers that can manage complex compliance obligations and deliver reliable performance across multiple countries. Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) driven chemical regulations strongly influence product development, favoring established companies with robust technical, regulatory, and safety capabilities, and raising entry barriers for new participants. Buyers in Europe show a clear preference for environmentally sustainable formulations, including bio-based products, recyclable materials, and low-toxicity chemistries, which aligns with the region’s leadership in green chemistry and circular economy initiatives.

North America Mining Dust Suppressants Market Trends

North America represents a mature, technologically advanced market for mining dust suppressants, with the United States driving most of the regional demand through extensive coal mining in Appalachia and the Western states, as well as substantial metal mining in Nevada, Arizona, and Alaska. The region is defined by stringent regulatory frameworks, with respirable dust regulations setting some of the world’s most rigorous exposure limits and compliance monitoring requirements. This regulatory environment compels mining operators to adopt premium suppressant technologies and comprehensive dust management systems, reinforcing a focus on high-performance solutions and sophisticated implementation.

The market is further distinguished by a strong innovation ecosystem, where leading chemical manufacturers, mining technology firms, and research institutions collaborate on next-generation suppressant solutions, including bio-based formulations, smart application systems, and products designed for extreme climates such as Arctic and desert conditions. Canada adds meaningful demand through its diverse mining portfolio in coal, potash, oil sands, and precious metals, with many operations in remote areas that require durable, long-duration dust control solutions.

Competitive Landscape

The global mining dust suppressants market structure exhibits moderate fragmentation, dominated by leading players such as Solenis LLC, Quaker Houghton, Midwest Industrial Supply, and Zydex Industries. These companies collectively capture 45-50% of market share. Competitive positioning centers on technical performance validation, application expertise, service network coverage, and total cost of ownership value propositions.

Leading suppliers differentiate through comprehensive technical support including on-site assessments, pilot testing programs, customized formulation development, and performance monitoring services that extend beyond product sales. Companies with global operational footprints and established relationships with major mining corporations hold competitive advantages in securing large-scale supply agreements and participating in new mine development projects from the design phase.

Key Industry Developments

- In October 2025, Codelco and ennomotive launched two complementary global innovation challenges inviting worldwide startups, research centers, and technology companies to develop solutions for mineral dust agglomeration during transport and advanced dust measurement and mitigation technologies for Chuquicamata mine's interaction between underground block-caving and open-pit operations.

- In August 2025, Conuma Resources Limited's Brule Mine in British Columbia received a CA$ 13,000 penalty for 32 fugitive dust emissions violations over 18 months. Total particulate matter (PM) discharges ranged from 5% to 375% above authorized provincial limits, posing health risks including fine particulate matter (PM2.5) aggravation of asthma, chronic bronchitis, and increased heart attack risk according to U.S. Environmental Protection Agency (EPA) findings.

- In March 2025, Caterpillar introduced the Cat 789D autonomous water truck, a fully integrated solution that automates both the truck and water delivery process to optimize haul road watering and improve dust suppression on mine sites.

Frequently Asked Questions

The global mining dust suppressants market is projected to reach US$ 2.6 billion in 2026.

Tightening environmental and worker-safety regulations, expanding global mining activity, and the shift toward higher-performance, sustainable dust control solutions are driving the market.

The market is poised to witness a CAGR of 6.1% from 2026 to 2033.

Key market opportunities include the growing adoption of eco-friendly and bio-based suppressants and the expanding deployment of digitally enabled, IoT-based integrated dust management systems.

Solenis LLC, Quaker Houghton, Midwest Industrial Supply, and Zydex Industries are some of the key players in the market.