- Metals & Minerals

- Iron Ore Pellets Market

Iron Ore Pellets Market Trends, Size, Share, Growth, Forecasts, 2025 - 2032

Iron Ore Pellet Market By Grade (BF Grade, DRI Grade) Trade (Captive, Seaborne) and Regional Analysis for 2025 - 2032

Iron Ore Pellets Market Share and Trends Analysis

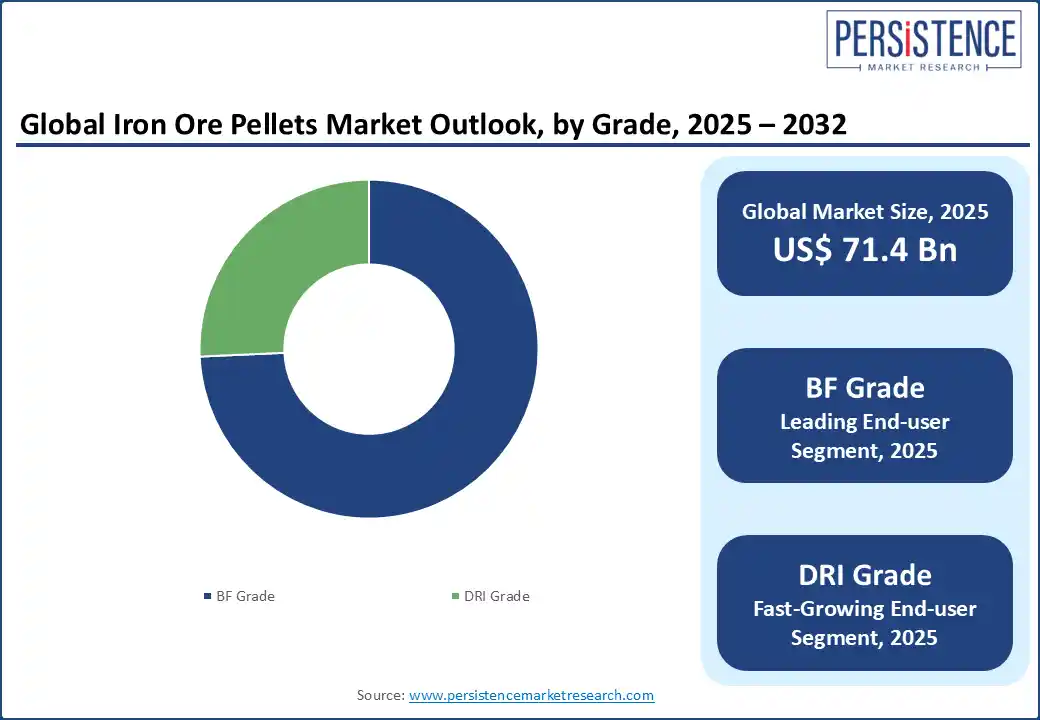

The global iron ore pellets market size is likely to be valued at US$ 71.4 Bn in 2025 and is expected to reach US$ 105.3 Bn growing at a CAGR of 5.7% during the forecast period from 2025 to 2032.

Pellet production plays a central role in the future of global DRI growth. DRI plants require DR-grade pellets with over 67% Fe and under 2% gangue, making these pellets essential for both gas-based and hydrogen-based DRI technologies Since 2016, DRI output has grown at nearly eight million tonnes per year, reaching 130–135 Mt in 2023, and could rise to 185–190 Mt by 2030. CDRI volumes tripled over the past two decades from 39 Mt to 102.1 Mt while HDRI jumped from 1.8 Mt to 13.9 Mt, driven by demand from EAF-based steelmakers. Every tonne depends on stable and high-quality pellet supply. Companies such as Vale are already setting up regional pellet hubs to address rising demand across multiple DRI sites.

Hydrogen-based projects such as H2 Green Steel and HYBRIT plan to produce over 5 Mt of green steel annually by 2030, using only DR-grade pellets as feedstock. These efforts underline the strategic need for reliable pellet supply chains. Any drop in pellet quality or availability could disrupt DRI timelines and efficiency. Sustained global steel production over 1,700 Mt across the top 15 nations directly reinforces the requirement for consistent pellet production, positioning it as the backbone of decarbonized steelmaking.

Key Industry Highlights:

- DR-grade pellets with over 67% Fe and less than 2% gangue are essential to meet feedstock requirements of hydrogen-based and gas-based DRI plants.

- Blast furnace grade pellets dominated with a 74.3% value share in 2022 due to their cost efficiency, reliability, and widespread use in integrated steelmaking.

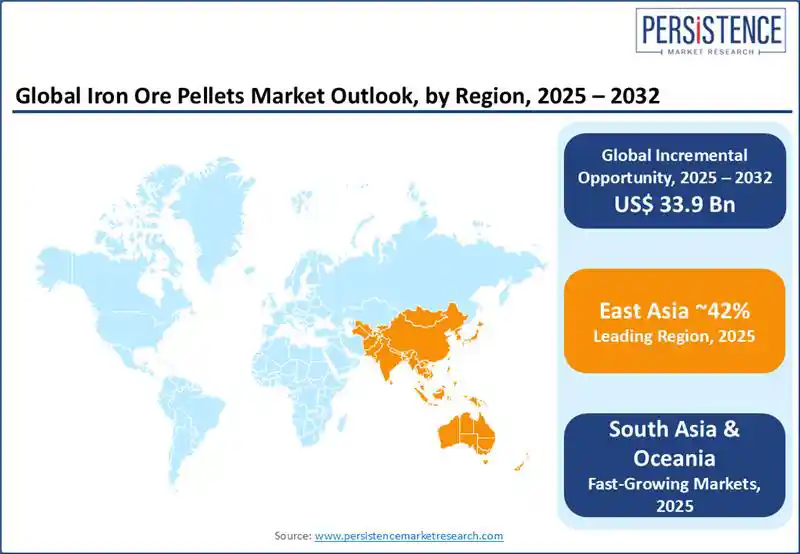

- East Asia holds the largest market share at 41.6%, supported by China’s expanding pellet capacity and installation of low-emission induration systems.

- India’s pellet output reached 105 million tonnes in FY2024–25, driven by growing domestic demand, raw material availability, and reduced dependence on exports.

- High-purity iron ore pellets are seeing strong demand from green steel producers like H2 Green Steel and OMK, with long-term supply deals reshaping the market.

- Briquettes developed through low-temperature processes offer 80% lower CO2 emissions than traditional pellets, raising competition for pellet manufacturers.

- Fossil-free pelletizing using biocarbon and bio-oil is gaining traction, with companies like Vale and LKAB achieving significant CO2 reductions in large-scale production.

- Green hydrogen steel projects such as HYBRIT and Stegra are boosting opportunities for DR-grade pellet suppliers by anchoring them in future-ready supply chains.

|

Global Market Attribute |

Details |

|

Market Size (2024A) |

US$ 67.7 Bn |

|

Estimated Market Size (2025E) |

US$ 71.4 Bn |

|

Projected Market Value (2032F) |

US$ 105.3 Bn |

|

Value CAGR (2025 to 2032) |

5.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.2% |

Market Dynamics:

Driver - Growing Demand for Low-Carbon Steelmaking Inputs

The demand for high-grade iron ore pellets is rising due to the global shift toward green steel production. Steelmakers are favouring feedstock with high iron content and low impurities to support direct reduction (DR) processes using hydrogen. DR-grade pellets with 68% Fe and ultra-low silica are proving essential in reducing CO2 emissions by up to 95% compared to blast furnace methods.

Major producers such as Vale and Metalloinvest are securing long-term supply deals and expanding capacity to meet this shift. As emission targets tighten globally, DR-compatible iron agglomerates are becoming a preferred input for sustainable steelmaking. Hydrogen-based steel plants in Sweden and Russia are actively integrating such pellets into their processes, indicating a long-term demand trajectory. For instance, H2 Green Steel’s tie-up with Vale and Metalloinvest’s 53-million-tonne supply agreement with OMK highlight industry-wide adoption. The transition to clean steel production is no longer experimental but entering large-scale implementation, making high-grade iron ore pellets a key enabler of decarbonization.

Restraint - Substitution Risk from Low-Emission Briquettes

Emerging technologies such as iron ore briquettes are posing challenges to traditional pellet demand. Companies are advancing low-temperature briquetting processes that reduce CO2 emissions by around 80% compared to pelletizing. With successful pilot tests and strong agglomerate strength, briquettes are becoming viable for DR steel production. Their lower carbon footprint and operational cost could divert investment away from pellet facilities.

Vale and Midrex are already preparing to scale up briquette technology globally, signalling a shift in market dynamics. If widely adopted, these briquettes could replace pellets in applications where environmental performance and cost savings are prioritized. The increasing focus on alternative feedstock is putting pressure on conventional pellet producers to innovate or risk losing market share.

Opportunity - Accelerated Shift to Fossil-Free Pelletizing

A clear industry trend is the adoption of renewable fuels in pellet production to curb emissions. Pelletizing, which contributes significantly to Scope-1 emission is decarbonized using bio-oil and biocarbon alternatives. LKAB and Vale have demonstrated the viability of such replacements by producing commercial-grade pellets with up to 350,000 tonnes of CO2 savings annually per plant. This move supports broader goals such as 33% reduction in operational emissions by 2030, and aligns with national strategies for carbon neutrality. As steelmakers commit to low-emission value chains, fossil-free agglomerate production is becoming a norm. Iron ore pellets made via renewable fuels are expected to set new benchmarks in sustainable raw material supply.

Key Trends

Integration with Green Hydrogen Projects

- The rise of hydrogen-based DRI plants is creating new demand centers for iron ore pellets. Facilities such as Stegra’s in Sweden are preparing for large-scale operations that rely on a consistent, fossil-free pellet supply. Rail-based logistics and long-term procurement plans are developed to support these industrial-scale green steel projects.

- Projects such as HYBRIT have already completed pilot phases and are entering commercial rollout, requiring a stable feedstock of DR-grade pellets. With producers like LKAB and Metalloinvest investing in premium-grade concentrate with up to 68% Fe, there is a strong opportunity for pellet suppliers to embed themselves in next-generation green steel value chains.

Category-wise Analysis

Grade Insights

BF grade iron ore pellets hold the largest market share at 74.3% by value in 2022. Steel producers continue to rely on blast furnace technology due to its established infrastructure and cost efficiency. BF pellets offer consistent quality and support large-scale output, making them the preferred choice for integrated steel plants worldwide. Low production cost and wide availability further strengthen their dominance across mature steel markets.

On November 13, 2024, Vale secured a multi-year agreement with ROGESA to supply BF-grade pellets from 2025 to 2027. This deal supports ongoing blast furnace operations while preparing for a shift toward cleaner production. From 2028, ROGESA plans to adopt DR-grade pellets with the commissioning of its DRI plant in Dillingen. The transition reflects growing momentum in green steel while BF pellets continue to anchor global supply chains.

Trade Insights

Captive trade type holds 72.4% market share, led by integrated steel producers sourcing pellets for in-house consumption. Companies such as Tata Steel and JSW Steel continue expanding pellet capacity to secure raw material supply, reduce costs, and ensure quality consistency. Strong backward integration and rising steel demand further boost captive pellet consumption.

Regional Insights

North America Market Trends

North America contributes 10.2% to the global iron ore pellet market, driven by strong investments in high-grade pellet production and sustainable technologies. In the U.S., the expansion of direct reduction-grade pellet capacity is aligned with the country’s metallics strategy and the rapid rise of electric arc furnace (EAF) steelmaking. U.S. Steel’s Keetac facility, now producing 4 million tons of DR-grade pellets annually, plays a key role in supplying 104 operating minimills with low-cost, high-purity input.

In Canada, the Iron Ore Company of Canada (IOC) is reinforcing the region’s position in both sustainable pellet production and international supply. Recent efforts to cut emissions through electric boiler and burner upgrades highlight Canada’s shift toward low-carbon pelletizing.

At the same time, growing exports of DR-grade pellets to hydrogen-based HBI plants in France and Sweden reflect the region’s strategic role in global green steel supply chains. This dual focus on decarbonization and advanced feedstock supply is strengthening North America’s influence in the transition to fossil-free steelmaking.

East Asia IronOre Pellets Market Trend

East Asia dominates the iron ore pellet market with a 41.6% value share, led by China’s aggressive capacity expansion and decarbonization push. On September 25, 2024, Metso partnered with BSIET to deliver a 1.7 MTPA traveling grate induration system for Ruifeng Iron and Steel in Tangshan. The facility will replace outdated shaft furnaces and marks the 12th pellet project by Metso and BSIET in China. Their compact, low-emission technology supports China’s ongoing green steel transition and solidifies East Asia’s leadership.

Iron-rich agglomerates remain central to steelmaking across key provinces such as Hunan, where iron ore output jumped to 104,600 Ton in March 2025 from 71,500 Ton in February. Updates from the National Bureau of Statistics confirm active and expanding operations with the region nearing past highs such as 12,277,000 Tonnes recorded in December 2014. High product uniformity, reliable supply chains, and adoption of energy-efficient pelletizing systems drive demand and reinforce East Asia’s strong position in the global market.

South Asia & Oceania Iron Ore Pellets Market Trends

South Asia & Oceania accounts for 17.2% of the global market share, driven by India’s consistent growth in iron ore pellet output. India raised its pellet production from 59.6 million tonnes in 2018–19 to 94 million tonnes in 2023–24. In FY2024–25, the country reached 105 million tonnes, marking a 5% year-on-year rise. Increased steel demand, wider adoption of blast furnace feedstock crossing 50%, and capacity expansions such as Bengal Energy’s 1.2 MTPA plant in West Bengal pushed this growth.

India’s raw material availability remained strong, with iron ore production at 251.13 million tonnes in 2021–22, supporting pelletizing units. Design capacity hit 164 million tonnes by 2025, up from 148 million the year before. Lower dependence on imports and shrinking exports, which dropped to 6.32 million tonnes in 2022–23 from 13.75 million in 2020–21, signal a market turning inward to meet domestic steelmaking needs. This regional momentum reinforces South Asia’s role as a growing hub for agglomerated iron feedstock.

Competitive Landscape

The global iron ore pellets market is fairly consolidated, with major players such as LKAB, Rio Tinto (IOC), Vale S.A., Metalloinvest, and Samarco controlling 33% to 38% of the overall market. These companies focus on advancing low-carbon pellet technologies, transitioning to direct reduction (DR)-grade products, and aligning with hydrogen-based steelmaking needs. Their strategies increasingly center around fossil-free fuels, alternative agglomerates, and integration with clean steel ecosystems to maintain technical and environmental leadership.

Top manufacturers are scaling up their production capacity and entering logistics partnerships to strengthen global pellet delivery. Meanwhile, small and mid-sized players often depend on long-term contracts to secure demand under fixed pricing structures. Across the board, producers are prioritizing high-Fe, low-impurity pellet output to cater to the EAF and HBI markets, reflecting a shift from traditional blast furnace-grade materials toward premium and green-compliant feedstock.

Key Developments:

- On November 13, 2024, Vale entered a multi-year agreement with ROGESA (a JV of Dillinger and Saarstahl AG) to supply blast furnace-grade pellets from 2025 to 2027, followed by a transition to direct reduction (DR) pellets starting in 2028. This supports ROGESA’s upcoming hydrogen-based DRI plant in Dillingen, aligning with Europe's shift to green steel. The deal reinforces Vale's role as a key DR pellet supplier and supports its goal to reduce Scope 3 emissions by 15% by 2035.

- On May 01, 2025, Ferrexpo, a major Ukraine-based producer, announced its readiness to supply high-quality DR-grade pellets to European green steelmakers. After producing 489,720 tonnes of DR pellets in 2024 (up from zero in 2023), the company positioned itself as a critical player supporting the EU’s green steel ambitions from 2027 onwards. This shift reflects the company’s focus on aligning pellet specifications with strict European sustainability standards.

Companies Covered in Iron Ore Pellets Market

- Vale SA

- LKAB

- Metalloinvest MC LLC

- Iron Ore Company of Canada

- ArcelorMittal

- Cleveland-Cliffs Inc.

- FERREXPO

- METALLOINVEST MC LLC

- Rio Tinto

- Samarco

- Tata Steel

Frequently Asked Questions

The global iron ore pellets market is projected to be valued at US$ 71.4 Bn in 2025.

BF-grade iron ore pellets are expected to hold around 65–68% share of the global market by value in 2025, driven by continued reliance on blast furnace operations in traditional steelmaking regions despite growing DR-grade adoption.

The iron ore pellets market is poised to witness a CAGR 5.7% from 2025 to 2032.

Rising demand for DR-grade pellets to enable hydrogen-based low-carbon steelmaking is driving iron ore pellets market growth.

Scaling fossil-free pellet production using renewable fuels presents a major opportunity to meet sustainability targets.