- Inks, Coatings, Adhesives & Sealants (ICAS)

- Europe Iron Oxide Pigments Market

Europe Iron Oxide Pigments Market Size, Share, and Growth Forecast 2026 - 2033

Europe Iron Oxide Pigments Market by Product Type (Natural, Synthetic), by Colour (Red, Yellow, Black), by End Use (Construction, Paints & Coatings, Plastics, Paper, Pharmaceuticals), and Regional Analysis for 2026 - 2033

Europe Iron Oxide Pigments Market Size and Trend Analysis

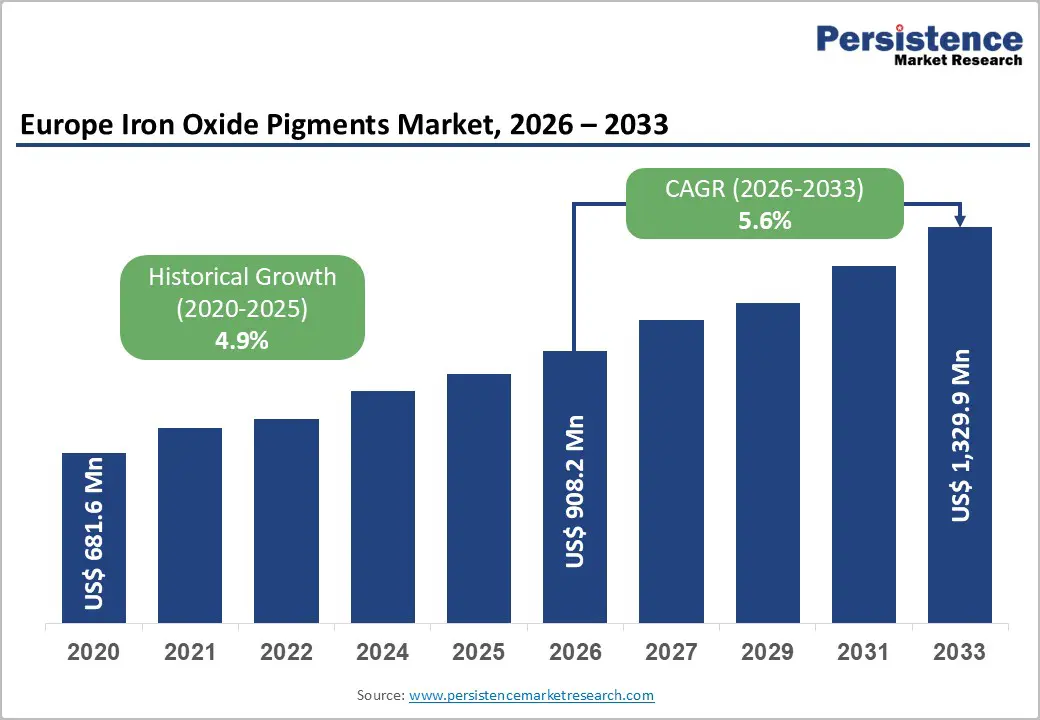

The Europe iron oxide pigments market size is supposed to be valued at US$ 908.2 Million in 2026 and is projected to reach US$ 1,329.9 Million by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

The Europe Iron Oxide Pigments market is sustained by a resilient and diversifying demand structure, fundamentally driven by the construction sector's dominant consumption of synthetic iron oxide pigments for concrete coloring, decorative paving, and architectural facade applications, reinforced by the European Commission's Renovation Wave Strategy targeting the energy-efficient renovation of 35 million buildings by 2030 and the EU's NextGenerationEU (NGEU) €648 billion recovery investment program funding public infrastructure construction across all 27 EU member states.

Key Industry Highlights:

- Leading Country: Germany leads the European Iron Oxide Pigments market, anchored by LANXESS AG's Bayferrox® world-leading synthetic iron oxide production at Krefeld-Uerdingen and Leverkusen, BASF SE's Ludwigshafen construction chemical pigment operations, VCI-documented €12 billion annual German chemical R&D investment, and the BMWSB's building renovation programs sustaining Germany's dual position as Europe's largest iron oxide pigment producer and consumer.

- Fastest Growing Country: Eastern Europe and Mediterranean markets represent the fastest-growing European regions, driven by NextGenerationEU NGEU €648 billion infrastructure investment flowing through national RRP programs, accelerating construction sector iron oxide pigment consumption in Poland, Italy, Spain, and Czech Republic, supported by EU Cohesion Fund co-financing of public infrastructure projects requiring colored concrete and architectural construction materials.

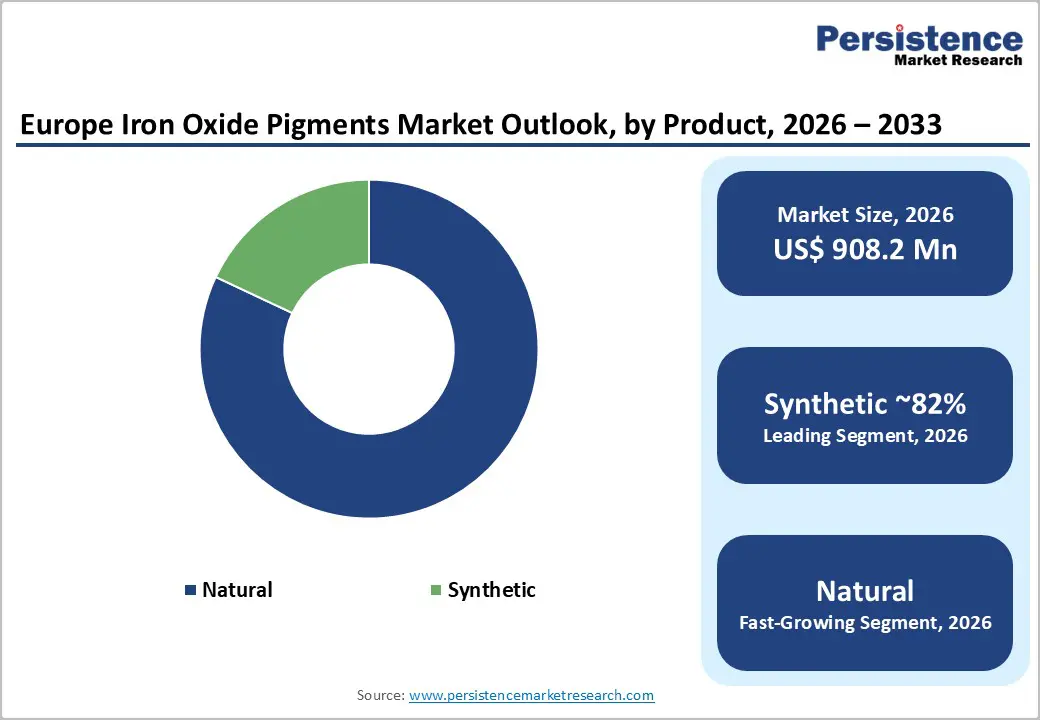

- Dominant Product Type: Synthetic iron oxide dominates the Product Type segment with approximately 82% revenue share, anchored by LANXESS AG's Bayferrox® certified batch consistency to DIN ISO 10601 standards, technically superior performance in alkaline concrete environments, and universal specification by European construction chemicals companies including Sika AG, MAPEI, and Heidelberg Materials for colored concrete and render applications.

- Fastest Growing End Use: Pharmaceuticals is the fastest-growing End Use segment, propelled by Clariant AG's September 2024 pharmaceutical-grade E172 iron oxide launch, EFPIA's €42 billion European pharma R&D investment documented for 2022, the EU Critical Medicines Alliance expanding European API and dosage form manufacturing capacity, and pharmaceutical-grade iron oxide's premium pricing versus construction grades generating above-average revenue growth per tons.

- Key Market Opportunity: Low-carbon EPD-certified iron oxide pigment and pharmaceutical-grade E172 segment expansion represent the dual key market opportunities, with LANXESS Bayferrox's EN 15804 EPD documentation enabling EU Taxonomy-compliant green construction procurement, EFPIA-documented pharmaceutical manufacturing investment growth, Clariant's Healthcare Pigments portfolio, and EU Renovation Wave targeting 35 million building renovations by 2030, sustaining structurally growing premium iron oxide pigment demand through 2033.

| Key Insights | Details |

|---|---|

|

Iron Oxide Pigments Market Size (2026E) |

US$ 908.2 Million |

|

Market Value Forecast (2033F) |

US$ 1,329.9 Million |

|

Projected Growth CAGR (2026–2033) |

5.6% |

|

Historical Market Growth (2020–2025) |

4.9% |

Market Dynamics

Drivers - EU Renovation Wave Strategy and NextGenerationEU Infrastructure Investment Driving Construction Sector Iron Oxide Pigment Demand

The European Commission's Renovation Wave Strategy, launched in October 2020 as a flagship pillar of the European Green Deal, targeting the energy-efficient renovation of at least 35 million buildings by 2030 and doubling the annual building renovation rate across the EU from its current 1% to approximately 2% per year, is the most structurally significant demand driver for the European Iron Oxide Pigments market, as construction renovation and new build programs are the dominant consumption channels for synthetic iron oxide red, yellow, and black pigments in colored concrete, decorative pavement, architectural terracotta render, and cement-based flooring applications. The EU's NextGenerationEU (NGEU) recovery fund, allocating €648 billion across EU member states through 2026 for infrastructure investment under national Recovery and Resilience Plans (RRPs), is directly funding public infrastructure construction programs in roads, bridges, public buildings, and housing that generate substantial colored concrete and decorative construction material procurement demand.

LANXESS AG (headquartered in Cologne, Germany), the world's largest producer of synthetic iron oxide pigments, supplies its Bayferrox® brand iron oxide pigments to the European construction chemicals, ready-mix concrete, and precast concrete product manufacturing industries as the technically and commercially dominant iron oxide pigment family in European construction applications. BASF SE contributes complementary construction pigment dispersions through its Pigment Dispersions and Construction Chemicals business units, serving European concrete manufacturers.

Paints and Coatings Industry Sustained Iron Oxide Pigment Procurement Under CEPE-Documented European Production Scale

The European paints and coatings industry, with the European Council of the Paint, Printing Ink and Artists' Colours Industry (CEPE) documenting approximately 3.5 million tons of European paint and coatings production annually, is the second-largest sustained demand channel for European iron oxide pigments, consuming red, yellow, and black iron oxide grades as cost-effective, chemically stable, UV-resistant, non-toxic, and REACH-compliant inorganic coloring agents in architectural decorative coatings, industrial protective coatings, wood coatings, and vehicle refinishing applications.

Iron oxide pigments' superior lightfastness (ISO 105-B02 rating: 7–8 on a 1–8 scale), excellent weather resistance, and chemical stability in alkaline coating environments, combined with their REACH Regulation compliance and EU GHS/CLP safety classification as non-carcinogenic and non-toxic, make them the preferred inorganic pigment family for European paint formulators seeking durable, regulatory-compliant, and cost-competitive coloring agents for both interior and exterior coating applications. Huntsman International LLC's Tioxide® product division and Venator Materials PLC (headquartered in Wynyard, UK) serve the European paints and coatings iron oxide pigment market with certified-performance iron oxide grades meeting EN ISO color consistency standards required by European architectural coating manufacturers.

Restraints - REACH Regulation Compliance Costs and Evolving EU Chemical Substance Restriction Proposals Creating Formulation Investment Burden

The European Chemicals Agency (ECHA)'s REACH Regulation (EC) No 1907/2006 compliance requirements, including Substance of Very High Concern (SVHC) candidate list evaluations, extended safety data sheet documentation obligations, and progressive restrictions under the EU Chemical Strategy for Sustainability, impose ongoing regulatory compliance investment costs on iron oxide pigment manufacturers and their European downstream customers in the paints, plastics, and construction sectors.

The European Chemical Industry Council (Cefic) has documented that REACH compliance administration costs represent a structurally significant overhead for specialty chemical and pigment manufacturers, with smaller European pigment processors and formulators facing disproportionate per-unit compliance costs that create competitive pressure from non-EU pigment suppliers operating under less stringent chemical registration frameworks.

Competition from Asian Low-Cost Synthetic Iron Oxide Pigment Producers Compressing European Market Pricing

The European Iron Oxide Pigments market faces persistent pricing pressure from Chinese synthetic iron oxide pigment manufacturers, particularly Hunan Sanhuan Pigment Co., Ltd. and other Chinese producers concentrated in Hunan and Zhejiang provinces, who benefit from lower production cost structures, favorable domestic energy prices, and Chinese government industrial policy support that enables export pricing at levels below European manufacturing cost equivalents.

The European Commission's trade defense instruments, including EU Anti-Dumping Regulation (EU) 2016/1036, provide some measure of competitive protection for European iron oxide pigment manufacturers, but the structural cost differential between European and Chinese production continues to challenge European producers' pricing power in commodity-grade synthetic iron oxide pigment market segments.

Opportunities - Pharmaceutical-Grade Iron Oxide Pigment Demand Growth Driven by EU Pharmaceutical Sector and Colorant Regulation Compliance

The European pharmaceutical industry's growing consumption of ultra-high-purity pharmaceutical-grade iron oxide pigments, governed by European Pharmacopoeia (Ph. Eur.) monograph standards E172 and the European Food Safety Authority (EFSA)'s colorant approval framework, is creating a premium-priced, high-growth specialty segment within the European Iron Oxide Pigments market that offers substantially higher average selling prices and margin profiles compared to standard construction or paints-grade iron oxide commodity products. Iron oxide red (E172 Red), yellow (E172 Yellow), and black (E172 Black) pigments are approved EU food and pharmaceutical colorants used extensively in pharmaceutical tablet coating, capsule shell coloring, and medical device color-coding applications, with the European Federation of Pharmaceutical Industries and Associations (EFPIA) documenting European pharmaceutical sector R&D investment exceeding €42 billion in 2022 and sustaining a large and structurally growing pharmaceutical-grade iron oxide colorant procurement base.

Clariant AG (headquartered in Muttenz, Switzerland), a leading global specialty chemicals company, offers Ph. Eur. and USP-compliant pharmaceutical-grade iron oxide pigment products through its Pigments & Dyes and Healthcare business segments, serving European pharmaceutical tablet manufacturing customers. The EFPIA's documented expansion of European pharmaceutical manufacturing capacity under the European Health Union and Critical Medicines Alliance frameworks is expected to drive above-average growth in pharmaceutical-grade iron oxide pigment procurement through the 2026–2033 forecast period.

Green Construction and Sustainable Concrete Coloring Innovation Creating Demand for Low-Carbon Iron Oxide Pigment Formulations

The European construction sector's accelerating transition toward low-carbon and sustainable building materials, mandated by the EU's Energy Performance of Buildings Directive (EPBD), the Level(s) EU Sustainable Buildings Framework, and EN 15804 environmental product declaration standards for construction products, is creating a commercially significant opportunity for iron oxide pigment manufacturers able to develop and certify low-carbon footprint pigment grades that support European concrete and construction material producers' lifecycle carbon reduction commitments. Supplementary Cementitious Materials (SCM) and geopolymer concrete systems, which are increasingly adopted by European precast concrete manufacturers as lower-carbon alternatives to conventional Portland cement formulations under EN 206 concrete standard frameworks, require specialized iron oxide pigment grades compatible with the alkaline chemistry and reduced water-cement ratio formulation parameters of these innovative, sustainable concrete systems.

LANXESS AG's Bayferrox® synthetic iron oxide product line already incorporates environmental product declarations (EPDs) aligned with EN 15804, positioning LANXESS as an early-mover in providing documented low-carbon iron oxide pigment solutions to European green building material manufacturers seeking EU Taxonomy Regulation-compliant construction product portfolios. The European Concrete Platform's sustainable concrete roadmap and NRMCA Europe's low-carbon concrete initiatives sustain structural demand for certified sustainable iron oxide pigment procurement from European ready-mix and precast concrete producers through the forecast period.

Category-wise Analysis

By Product Type Insights

Synthetic iron oxide pigments lead the Europe Iron Oxide Pigments market by product type, commanding approximately 82% of total product type segment revenue in 2026, a structurally dominant position reflecting synthetic iron oxide's technically superior and commercially consistent performance characteristics versus natural iron oxide (ochres, siennas, umbers) in European industrial-scale construction, paints, and plastics applications requiring precise color consistency, controlled tinting strength, and certified chemical purity specifications that naturally mined ochre pigments with inherent compositional variability cannot reliably deliver.

Synthetic iron oxide pigments, produced through either the Penniman-Zoph precipitation process, the Laux aniline reduction process, or the calcination process, are manufactured to exacting DIN ISO 10601 and EN ISO color space specifications that ensure batch-to-batch consistency required by European construction chemical and architectural coating manufacturers. LANXESS AG's Bayferrox® synthetic iron oxide line, produced at its Krefeld-Uerdingen and Leverkusen facilities in Germany, represents the most commercially dominant synthetic iron oxide product family in the European market by volume and revenue. Natural iron oxide pigments hold approximately 18% of product type revenue, serving niche artisanal, heritage restoration, and natural building material applications where authentic earthy tonality from natural mineral composition is a valued product characteristic.

By Colour Insights

Red iron oxide pigments lead the Europe Iron Oxide Pigments market by colour, accounting for approximately 42% of total colour segment revenue in 2026, a dominant position anchored in red iron oxide's (α-Fe2O3 hematite phase) exceptional UV stability, high tinting strength, chemical inertness in alkaline concrete environments, and broad applicability across the three largest iron oxide consumption sectors: colored concrete in construction, architectural and industrial protective coatings in the paints and coatings sector, and colorant applications in the plastics and rubber industries. Red iron oxide's deep reddish-brown to bright vermilion color range, achievable through particle size control during synthesis in the 20–300 nm range, provides the most versatile and commercially demanded color palette within the iron oxide pigment family for European architectural and construction coloring applications.

LANXESS AG's Bayferrox® Red grades and Huntsman International LLC's Tioxide® iron oxide red portfolio are the most widely specified red iron oxide products in European procurement programs for concrete and paint manufacturing. Yellow iron oxide (goethite, α-FeOOH) holds the second-largest colour share at approximately 33%, valued for its bright lemon-to-ochre yellow color range in decorative concrete, yellow road marking paint, and primer coating applications.

By End-user Insights

Construction leads the Europe Iron Oxide Pigments market by end use, commanding approximately 45% of total end-use segment revenue in 2026, a structurally dominant position reflecting the construction sector's historical and continued role as the single largest iron oxide pigment consumption channel in Europe, where synthetic iron oxide red, yellow, black, and blended pigments are consumed in mass-volume applications including colored ready-mix concrete for residential and commercial flooring and facades, precast concrete paving stones, roof tiles, concrete blocks, and cement-based render systems that collectively represent the largest aggregate pigment consumption across all European end-use categories.

The European Construction Industry Federation (FIEC)'s documented €1.8 trillion European construction output in 2023 and the EU's Renovation Wave Strategy targeting 35 million building renovations by 2030 provide both current-scale and forward-growth mandates sustaining construction iron oxide pigment procurement. LANXESS AG's direct supply relationships with major European chemical construction companies including Sika AG, MAPEI, and Heidelberg Materials (formerly HeidelbergCement) confirm its dominant commercial position in European construction iron oxide pigment procurement. Paints & Coatings holds the second-largest end-use share at approximately 27% of revenue, sustained by CEPE's documented 3.5 million tons of European paint production base.

Competitive Landscape

Europe iron oxide pigments market is moderately consolidated at the premium synthetic pigment tier, with LANXESS AG commanding a globally dominant position through its Bayferrox® brand, followed by BASF SE, Huntsman International LLC, and Clariant AG as commercially significant European-headquartered participants. Venator Materials PLC and Applied Minerals, Inc. serve specialty niche segments. Hunan Sanhuan Pigment and Titan Kogyo compete in cost-driven commodity segments.

Key differentiators include EN ISO color consistency certification, Ph. Eur. pharmaceutical-grade compliance, EN 15804 environmental product declaration availability, and direct construction OEM supply relationships. Emerging trends include low-carbon footprint EPD-certified pigment grades, bio-based carrier dispersions for water-borne coating applications, and circular economy pigment recovery programs aligned with EU Chemical Strategy for Sustainability requirements.

Key Developments:

- In January 2025, LANXESS AG announced the expansion of its Bayferrox® synthetic iron oxide pigment production capacity at its Krefeld-Uerdingen, Germany facility, targeting growing European construction sector demand for colored concrete applications under the EU's Renovation Wave and NextGenerationEU infrastructure investment programs driving above-average iron oxide pigment procurement from German and European precast concrete manufacturers.

- In September 2024, Clariant AG launched a new range of Ph. Eur.-compliant pharmaceutical-grade iron oxide pigments under its Healthcare Pigments portfolio, specifically developed for tablet coating and capsule shell coloring applications, meeting the most stringent European Pharmacopoeia E172 purity and color consistency specifications, targeting the growing European pharmaceutical manufacturing capacity investment under the EU Critical Medicines Alliance framework.

- In April 2024, Venator Materials PLC announced a strategic portfolio optimization focusing on high-value specialty iron oxide pigment grades for paints, coatings, and plastics, repositioning away from commodity construction-grade iron oxide toward premium-margin specialty pigment segments where its REACH-certified product quality and European manufacturing credentials provide sustainable competitive differentiation versus lower-cost Asian commodity imports.

Companies Covered in Europe Iron Oxide Pigments Market

- Huntsman International LLC

- Venator Materials PLC

- Applied Minerals, Inc.

- Cathay Industries

- Lanxess

- BASF SE

- KRONOS Worldwide, Inc.

- Hunan Sanhuan Pigment Co., Ltd.

- Titan Kogyo, Ltd.

- Clariant AG

Frequently Asked Questions

The Europe Iron Oxide Pigments market is estimated to be valued at US$ 908.2 Million in 2026 and is projected to reach US$ 1,329.9 Million by 2033, registering a forecast CAGR of 5.6% from 2026 to 2033. The market recorded a historical CAGR of 4.9% between 2020 and 2025.

The primary drivers are the European Commission's Renovation Wave Strategy mandating 35 million building renovations by 2030 and NGEU's €648 billion infrastructure investment generating colored concrete and architectural render iron oxide procurement, and the CEPE's documented 3.5 million tons European annual paint production base consuming LANXESS AG's Bayferrox® and Huntsman's REACH-certified iron oxide red, yellow, and black pigment grades as the standard inorganic colorant specification across European architectural and industrial protective coating formulations.

Synthetic iron oxide pigments lead the Product Type segment with approximately 82% revenue share in 2026, anchored by LANXESS AG's Bayferrox® certified batch consistency to DIN ISO 10601 standards manufactured at Krefeld-Uerdingen and Leverkusen, technically superior performance in alkaline concrete environments versus natural ochre alternatives, and universal specification by European construction chemicals companies including Sika AG, MAPEI, and Heidelberg Materials for industrial-scale colored concrete, precast paving, and architectural render applications.

Germany leads the European Iron Oxide Pigments market, anchored by LANXESS AG's world-leading Bayferrox® synthetic iron oxide production, BASF SE's construction pigment dispersions, VCI-documented €12 billion annual chemical R&D investment, the BMWSB's building renovation programs, and KfW Bundesbank's energy efficiency financing sustaining Germany's unique dual position as both Europe's highest-volume iron oxide pigment production geography and its largest single-country construction sector consumption geography.

The most significant opportunities are pharmaceutical-grade E172 iron oxide segment expansion and low-carbon EPD-certified construction pigment development, with Clariant AG's September 2024 pharmaceutical pigment launch, EFPIA's €42 billion European pharma R&D investment driving capsule and tablet colorant demand, LANXESS Bayferrox's EN 15804 EPD documentation enabling EU Taxonomy-compliant green construction procurement, and the Renovation Wave Strategy's targeted 35 million building renovations by 2030 creating structurally growing sustainable construction iron oxide procurement streams.