- HVAC

- Heterogeneous Mobile Processing and Computing Market

Heterogeneous Mobile Processing and Computing Market Size, Share, and Growth Forecast 2026 - 2033

Heterogeneous Mobile Processing and Computing Market by Processor Type (Graphics Processing Units (GPUs), Central Processing Units (CPUs), Neural Processing Units (NPUs), Digital Signal Processors (DSPs), FPGAs & TPUs), by Device Type (Smartphones, Tablets, Wearables, IoT Devices), by Application, by End-Use, by Regional Analysis, 2026 - 2033

Heterogeneous Mobile Processing and Computing Market Size and Trend Analysis

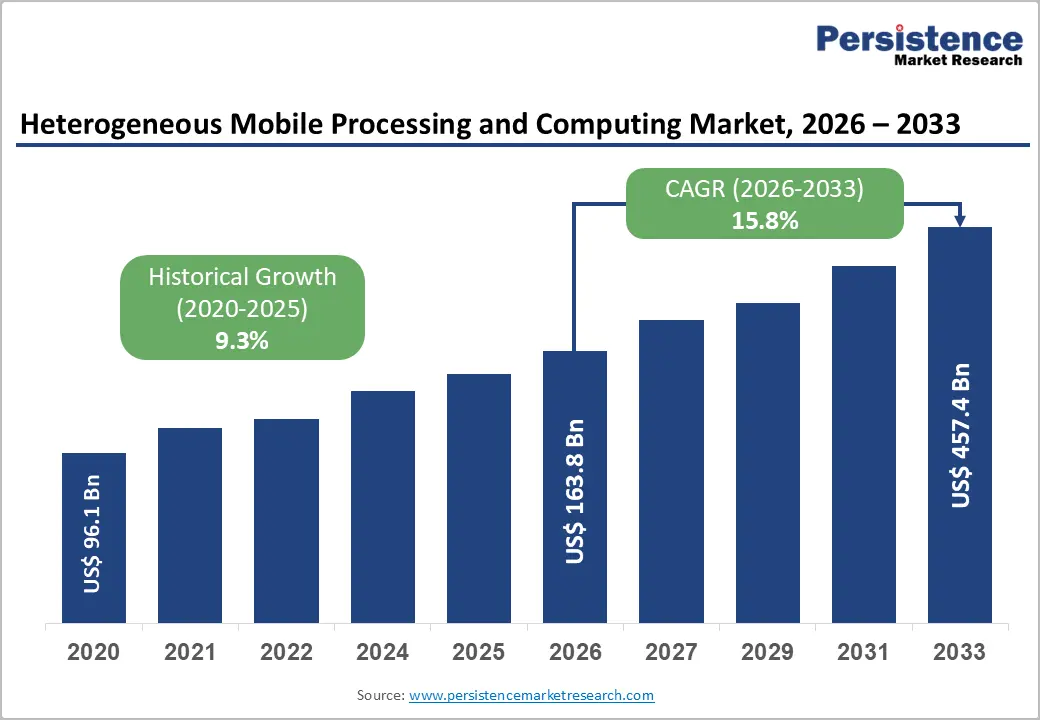

The global heterogeneous mobile processing and computing market size is expected to be valued at US$ 163.80 billion in 2026 and is projected to reach US$ 457.4 billion by 2033, growing at a CAGR of 15.8% between 2026 and 2033.

The convergence of AI on-device processing, 5G-enabled devices, and the proliferation of energy-efficient mobile System-on-Chip (SoC) architectures across consumer and enterprise segments contribute to its growth.

Key Industry Highlights

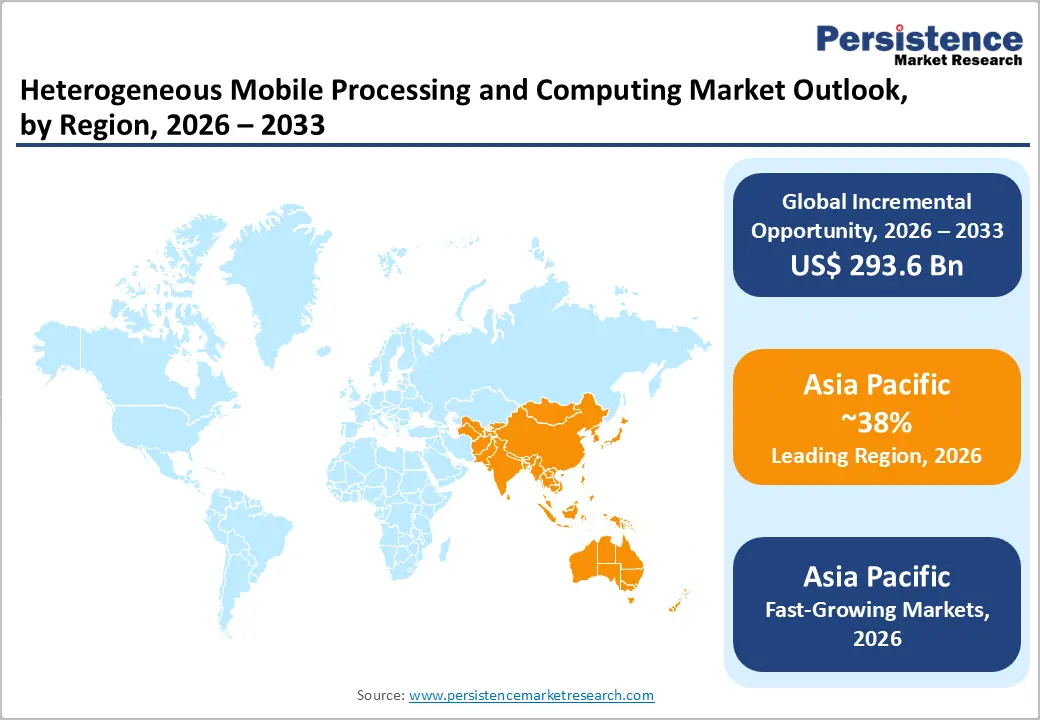

- Leading Region: Asia Pacific leads the Heterogeneous Mobile Processing and Computing Market market with a 38% regional share in 2026, anchored by the world's largest smartphone manufacturing ecosystem, the highest concentration of mobile SoC production capacity at leading fabs, and the most rapidly expanding 5G subscriber base globally, structural advantages that collectively make regional leadership self-reinforcing through 2033.

- Fast-Growing Region: Asia Pacific is also the fast-growing market expanding at a projected CAGR of 17.2% through 2033, catalysed by domestic semiconductor self-sufficiency programmes across China, India, and Japan, combined with the accelerating deployment of AI-capable 5G-enabled devices across the region's massive consumer base.

- Leading Segment: AI / ML Processing dominates the application segmentation with a 45.0% share equivalent to US$ 73.71 Billion in 2026, justified by the universal mandate across device categories for on-device AI inference capability, which has transformed NPU and GPU integration from a premium feature into a baseline SoC specification, a structural shift that sustains this segment's outsized share position for the full forecast horizon.

- Fast-Growing Processor Type: Neural Processing Units (NPUs) represent the fastest growing processor type segment in the heterogeneous mobile processing and computing market, driven by exploding demand for energy-efficient on-device generative AI inference that general-purpose CPUs and GPUs cannot serve at the power efficiency levels required by mobile and wearable form factors, a dynamic accelerating every major SoC vendor's NPU die-area investment.

- Key Opportunity: The expansion of heterogeneous mobile compute into the automotive end-use segment represents the market's most strategically time-sensitive opportunity, as automotive OEMs are actively sourcing mobile SoC derivatives for ADAS and in-vehicle AI applications across 7-10 year product lifecycles, creating design win opportunities with revenue durability that far exceeds consumer electronics replacement cycles and rewards early-moving heterogeneous computing specialists.

Market Dynamics

Drivers - Surging Demand for AI On-Device Processing Across Mobile and Edge Platforms

The single most consequential demand driver reshaping the Heterogeneous Mobile Processing and Computing Market is the enterprise and consumer shift toward on-device AI inference, eliminating cloud round-trip latency for applications ranging from real-time language translation to biometric authentication. Mobile SoC vendors, including Qualcomm, Apple, and MediaTek, now dedicate discrete die area to Neural Processing Units (NPUs), with shipments of AI-capable mobile chips reaching hundreds of millions of units annually according to industry data.

The ARM architecture's dominance in mobile compute, combined with emerging RISC-V processor adoption in cost-optimised IoT devices, creates a heterogeneous processing environment where multiple compute engines, CPU, GPU, NPU, and DSP, operate in coordinated parallel. This architectural evolution is not reversible; software ecosystems, developer toolchains, and end-user experience expectations are all calibrated to heterogeneous multi-engine pipelines, locking in sustained silicon investment through 2033.

Proliferation of 5G-Enabled Devices and the Expansion of Edge Computing Infrastructure

What drives growth in the heterogeneous mobile processing and computing market with equal structural force is the global rollout of 5G networks, which fundamentally alters the compute-communication balance in mobile architectures. As 5G enables real-time data streams from millions of IoT devices and embedded systems, the need for high-performance computing (HPC) capabilities at the edge, rather than in centralised data centres, intensifies pressure on mobile SoC designers to pack greater heterogeneous compute density into power-constrained form factors.

Based on authenticated market intelligence, global 5G subscriptions surpassed 1.6 billion by 2024, with each new generation of connected device incorporating at a minimum a CPU, GPU, and dedicated signal processing engine. The resulting bill-of-materials complexity directly amplifies chipset average selling prices and design win cycles for every participant in the heterogeneous mobile processing and computing industry.

Restraints - High Complexity and Cost of Heterogeneous SoC Design and Verification

The primary restraint limiting faster adoption across the broader heterogeneous mobile processing and computing space is the exponentially increasing design and verification cost associated with integrating multiple processor types, GPUs, NPUs, DSPs, FPGAs, and CPUs on a single monolithic or chiplet-based die. Advanced process nodes at 3nm and below, where leading mobile SoCs now operate, carry non-recurring engineering (NRE) costs that routinely exceed US$ 500 million per design tape-out.

According to semiconductor industry data, it effectively confines full-capability heterogeneous SoC development to a handful of well-capitalised players. Smaller fabless design houses and regional OEMs consequently face structural barriers to entry, suppressing competitive diversity and slowing the pace of differentiation. This concentration risk also means that any design flaw or manufacturing yield issue at a single node carries disproportionate market disruption potential.

Thermal Management and Energy Efficiency Constraints in Mobile Form Factors

A second, technically grounded restraint is the thermodynamic ceiling imposed by mobile device form factors, which fundamentally limits the sustained throughput achievable from heterogeneous compute engines operating simultaneously. When a mobile SoC activates GPU acceleration, NPU inference, and DSP signal processing concurrently, as demanding AI workloads and real-time gaming increasingly require, thermal dissipation constraints force aggressive dynamic voltage and frequency scaling (DVFS), materially reducing peak performance headroom.

Battery energy density improvements have consistently trailed compute density scaling, with lithium-ion energy density improving at roughly 3.5% per year versus transistor density improvements of 40 to 50% per node generation based on publicly available semiconductor roadmaps. This mismatch creates a persistent ceiling on real-world heterogeneous performance that constrains user experience and, by extension, OEM willingness to pay a premium for top-tier heterogeneous silicon.

Opportunities - Integration of AI Accelerators in Automotive and Industrial Embedded Systems

The heterogeneous mobile processing and computing market presents strong opportunities between 2026 and 2033, particularly in automotive and industrial embedded systems, where the need for functional safety and real-time AI processing is rapidly increasing. Automotive OEMs and Tier 1 suppliers are actively adopting mobile-grade SoCs that can handle complex tasks such as sensor fusion, object detection, and path planning using NPUs and DSPs.

These capabilities are derived from smartphone-era architectures that have matured over the past decade. The automotive semiconductor market is expanding faster than the broader chip industry, driven by rising demand for ADAS and autonomous driving solutions. Companies that secure automotive-qualified SoC design wins during 2026-2027 can benefit from long product lifecycles of 7-10 years, unlike short consumer cycles. To capitalise on this opportunity, market participants should prioritise ISO 26262 certification and strengthen partnerships before competition intensifies.

Expansion of On-Device Generative AI Across the Global Smartphone Installed Base

The growing adoption of generative AI directly on smartphones represents a major opportunity for the heterogeneous mobile processing and computing market. Consumers increasingly demand private, low-latency AI features such as real-time image creation, personalized recommendations, and offline virtual assistants. This trend is pushing smartphone OEMs to prioritize NPU performance as a key hardware requirement from 2026 onwards.

AI-capable smartphones are expected to dominate the premium segment by 2027, with each new generation requiring higher processing power and efficiency. This creates a continuous upgrade cycle, benefiting both chipmakers and software providers. Companies that invest in software ecosystems, including model optimisation, compression techniques, and developer-friendly APIs, will gain a strong competitive advantage. Over time, these software capabilities will become as important as hardware performance, allowing companies to build long-term market leadership and drive sustained revenue growth in the evolving mobile AI landscape.

Category-wise Analysis

Processor Type Insights

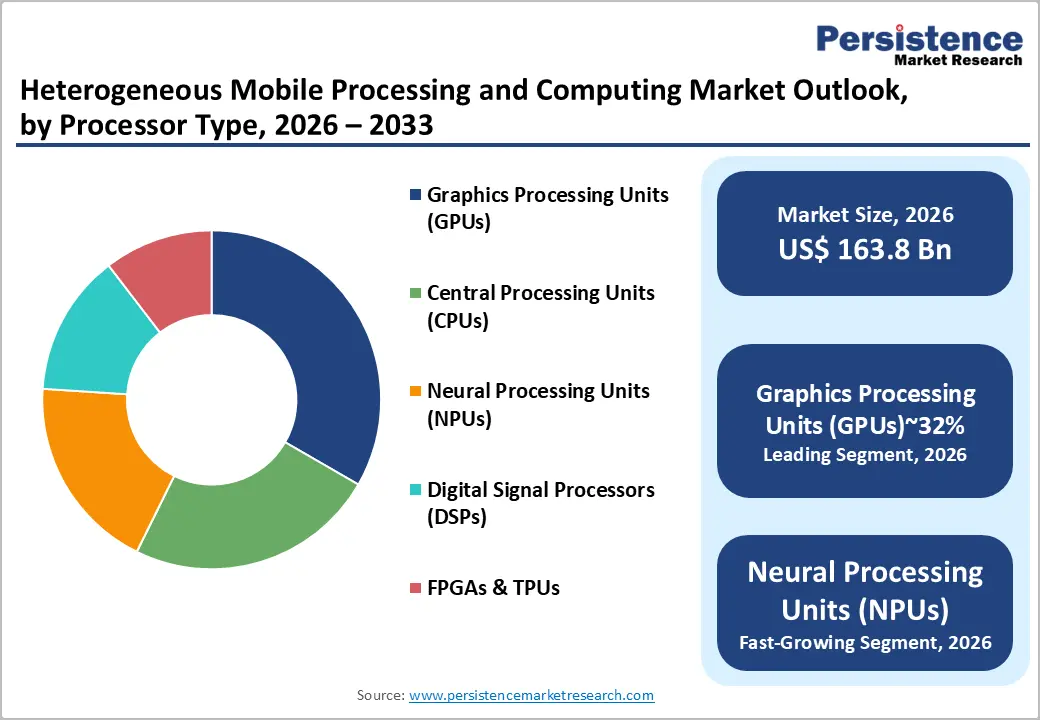

Graphics Processing Units (GPUs) account for 32.0% of the global heterogeneous mobile processing and computing market in 2026, reaching US$ 52.42 billion and maintaining their position as the leading processor type. GPUs dominate due to their parallel processing capabilities, which are essential for AI/ML workloads and real-time graphics rendering across devices. Every major mobile SoC now includes an integrated GPU, making it a core component of modern computing architectures. Additionally, GPU IP licensing continues to generate significant revenue for key providers.

Neural Processing Units (NPUs) are the fast-growing segment, driven by the increasing demand for on-device AI and generative applications that require efficient, low-power processing. While GPU dominance is expected to remain stable due to strong software support, NPU adoption is rising rapidly. Companies must balance GPU performance with NPU scaling to stay aligned with future technology trends and maintain competitiveness through 2033.

Device Type Insights

Smartphones hold 34.0% of the global heterogeneous mobile processing and computing market in 2026, valued at US$ 55.69 billion, making them the largest device category. Their leadership comes from high shipment volumes and rapid innovation cycles that continuously push advancements in GPU, NPU, and DSP integration within compact power limits. With global shipments exceeding 1.2 billion units in recent years, smartphones remain the primary driver of heterogeneous computing demand.

Wearables are emerging as a fast-growing market due to increasing adoption of health monitoring, real-time AI processing, and always-on connectivity features. These devices require highly efficient, low-power processing solutions tailored for small form factors. While smartphones will continue to dominate, the growth of wearables and IoT devices is gradually reshaping market dynamics. Companies should view wearables as a key entry point for developing next-generation energy-efficient computing technologies.

Application Insights

AI/ML processing accounts for 45.0% of the global heterogeneous mobile processing and computing market in 2026, reaching US$ 73.71 billion and emerging as the most dominant application segment. This leadership is driven by the growing importance of on-device AI across smartphones, wearables, and IoT systems, where it has become a standard feature rather than a premium offering. The complexity of AI models has increased significantly over the years, requiring higher computational power and more advanced hardware integration within SoCs.

As a result, both GPU and NPU capacities are expanding to support these workloads. Gaming is the fastest growing application segment, fuelled by advancements in cloud gaming, mobile ray tracing, and AI-driven game development. These trends are pushing the limits of mobile hardware performance. While AI/ML will continue to dominate, gaming is expected to gain a larger share, influencing future processor design and performance benchmarks.

End-user Insights

Consumer electronics account for 58.0% of the global heterogeneous mobile processing and computing market in 2026, valued at US$ 95 billion, making it the largest end-use segment. This dominance is driven by the high volume of devices such as smartphones, tablets, wearables, and smart home products, all of which rely heavily on advanced computing chips. The consumer electronics industry generates over US$ 1 trillion annually, with semiconductor content becoming increasingly important as AI features expand.

The automotive sector is the fast- growing end-use segment, supported by trends such as vehicle electrification, ADAS development, and advanced infotainment systems. These applications require powerful and reliable computing platforms capable of handling both safety-critical and non-critical functions. Although consumer electronics will remain dominant, the automotive segment offers higher long-term value due to greater chip content per vehicle and longer product lifecycles, making it a key growth opportunity for market players.

Regional Insights

North America Heterogeneous Mobile Processing and Computing Market Trends and Insights

North America holds 39.0% of the global heterogeneous mobile processing and computing market in 2026, valued at US$ 63.88 billion. Dominance stems from leading semiconductor firms, enterprise modernization, CHIPS Act investments, and 5G expansion. The region is expected to maintain over 35% share through 2033, driven by AI chip growth.

- United States Heterogeneous Mobile Processing and Computing Market Size

The United States accounts for 88% of North America’s market, reaching US$ 56.21 billion in 2026. Growth is driven by strong semiconductor IP presence, large 5G subscriber upgrades, and rising enterprise AI investments. Government-backed semiconductor initiatives will strengthen domestic fabrication and sustain technology leadership through 2030 and beyond.

Europe Heterogeneous Mobile Processing and Computing Market Trends and Insights

Europe holds 23.0% of the global market, valued at US$ 37.67 billion in 2026. Growth is driven by automotive silicon demand, industrial IoT adoption, and energy regulations. The European Chips Act and EU AI Act are accelerating domestic production and on-device AI adoption across automotive, industrial, and enterprise applications.

- Germany Heterogeneous Mobile Processing and Computing Market Size

Germany represents 24% of Europe’s market, valued at US$ 9.04 billion in 2026. Growth is driven by its automotive leadership and industrial systems demand. Companies like BMW and Volkswagen boost need for advanced compute platforms. Strong focus on safety certification and lifecycle support ensures high-value opportunities through 2033.

- United Kingdom Heterogeneous Mobile Processing and Computing Market Size

The UK contributes 18% of Europe’s market, totaling US$ 6.78 billion in 2026. Strength comes from semiconductor IP leadership, especially ARM, and a growing AI ecosystem. Consumer electronics demand and government AI programs support adoption, while the UK influences global standards despite having a relatively smaller manufacturing base.

- France Heterogeneous Mobile Processing and Computing Market Size

France holds 15% of Europe’s market, reaching US$ 5.65 billion in 2026. Growth is supported by consumer electronics demand, semiconductor activity, and defense investments. Government initiatives such as France 2030 promote domestic production, while aerospace and defense sectors increasingly adopt AI-enabled heterogeneous computing technologies.

Asia Pacific Heterogeneous Mobile Processing and Computing Market Trends and Insights

Asia Pacific accounts for 38.0% of the global market, valued at US$ 62.24 billion in 2026, and is the fastest-growing region. Growth is driven by strong device manufacturing, expanding 5G adoption, and government semiconductor initiatives. The region will dominate production and demand as fabrication capacity expands by 2030.

- China Heterogeneous Mobile Processing and Computing Market Size

China holds 45% of Asia Pacific’s market, valued at US$ 28.01 billion in 2026. Growth is driven by smartphone manufacturing, domestic semiconductor efforts, and companies like Huawei. Export restrictions have accelerated local innovation. Future growth depends on closing fabrication gaps while advancing AI and GPU technologies independently.

- India Heterogeneous Mobile Processing and Computing Market Size

India represents 12% of Asia Pacific’s market, reaching US$ 7.47 billion in 2026. Growth is driven by strong smartphone demand and expanding semiconductor talent. Government initiatives like PLI and semiconductor missions support local manufacturing and design. India’s market share is expected to rise significantly by 2033.

- Japan Heterogeneous Mobile Processing and Computing Market Size

Japan holds 16% of Asia Pacific’s market, valued at US$ 9.96 billion in 2026. Growth is driven by strengths in semiconductor materials, equipment, and automotive systems. Collaboration with TSMC supports advanced fabrication. Automotive players such as Toyota and Honda are likely to drive future demand for heterogeneous computing solutions.

Competitive Landscape

The heterogeneous mobile processing and computing market exhibits a moderately consolidated structure at the top tier, where a small number of vertically integrated or IP-dominant players, including Qualcomm, Apple, NVIDIA, MediaTek, and Samsung, capture the majority of silicon value and set the architectural direction for the entire ecosystem. Below that concentration point, the competitive landscape fragments rapidly across IP licensors, fabless specialists, and regional champions, creating a multi-layered competitive environment where differentiation occurs across design architecture, process node partnerships, software ecosystem depth, and energy-efficient computing benchmarks.

The primary basis of competition is shifting from raw performance metrics toward AI workload efficiency, specifically NPU inferences per watt, as OEM procurement decisions increasingly weight sustained real-world AI performance over peak synthetic benchmark scores. Emerging business model shifts include the monetisation of mobile AI software platforms and runtime optimisation tools as margin-accretive layers above commodity heterogeneous silicon, a trend that rewards participants who invest in developer ecosystems alongside hardware development.

Key Developments:

- January, 2025: Qualcomm Inc. announced the commercial availability of the Snapdragon 8 Elite platform, featuring a second-generation Hexagon NPU delivering a reported 45% improvement in AI inference throughput over its predecessor, directly targeting on-device generative AI workloads across premium Android smartphones and automotive ADAS systems.

- March, 2025: NVIDIA Corporation unveiled its Thor automotive SoC platform, a heterogeneous compute architecture integrating GPU acceleration, NPU inference, and safety-certified CPU cores onto a single die targeting autonomous vehicle compute requirements, with initial production vehicle integrations scheduled for 2026 model year platforms.

- October, 2024: MediaTek Inc. and TSMC jointly confirmed volume production of the Dimensity 9400 SoC on TSMC's 3nm process node, incorporating dedicated sixth-generation APU (AI Processing Unit) cores and claiming leadership in mobile AI efficiency benchmarks, reinforcing the competitive intensity characterising the fastest-growing segment in the heterogeneous mobile processing and computing market.

Heterogeneous Mobile Processing and Computing Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 96.07 Billion |

| Current Market Value (2026) | US$ 163.80 Billion |

| Projected Market Value (2033) | US$ 457.38 Billion |

| CAGR (2026 - 2033) | 15.8% |

| Leading Region | Asia Pacific (38%) |

| Dominant Processor Type | Graphics Processing Units (GPUs) (32.0%) |

| Top-Ranking Device Type | Smartphones (34.0%) |

| Top-Ranking Application | AI / ML Processing (45.0%) |

| Top-Ranking End-user | Consumer Electronics (58.0%) |

| Incremental Opportunity (2026 - 2033) | US$ 293.58 Billion |

Companies Covered in Heterogeneous Mobile Processing and Computing Market

- Qualcomm Inc.

- Apple Inc.

- ARM Holdings plc

- Samsung Electronics Co., Ltd.

- MediaTek Inc.

- NVIDIA Corporation

- Advanced Micro Devices, Inc. (AMD)

- Intel Corporation

- Texas Instruments Incorporated

- Imagination Technologies Group plc

- Broadcom Inc.

- Huawei Technologies Co., Ltd.

- Marvell Technology Group Ltd.

- Xilinx Inc. (an AMD company)

- Realtek Semiconductor Corporation

- STMicroelectronics N.V.

- NXP Semiconductors N.V.

- Renesas Electronics Corporation

- Rockchip Electronics Co., Ltd.

- Unisoc Technologies Co., Ltd.

Frequently Asked Questions

The heterogeneous mobile processing and computing market is valued at US$ 163.80 billion in 2026 and projected to reach US$ 457.4 billion by 2033, growing at a 15.8% CAGR, driven by rising on-device AI adoption.

Growth is driven by rapid on-device AI adoption and global 5G expansion, increasing demand for advanced SoCs integrating GPUs, NPUs, and DSPs to support high-performance edge computing workloads.

AI/ML Processing leads with 45% share in 2026, as on-device AI becomes essential across devices, driving strong demand for NPUs and GPUs, outpacing growth of other application segments.

Asia Pacific leads with 38% share in 2026, supported by strong semiconductor manufacturing ecosystems, major foundries like TSMC and Samsung, and high mobile device production and consumption demand.

Major opportunities include automotive AI SoCs, industrial embedded systems, and on-device generative AI in smartphones, driven by rising demand for real-time processing, privacy, and long lifecycle semiconductor deployments.

Leading companies include Qualcomm, Apple, NVIDIA, ARM, MediaTek, Samsung, and Intel; the market is highly competitive, driven by innovation in AI accelerators, ecosystem strength, and continuous performance advancements.