- Semiconductor Materials & Components

- DC-DC Converter Market

DC-DC Converter Market Size, Share, and Growth Forecast, 2025 - 2032

DC-DC Converter Market By Form Factor (Through-Hole/SMD, Brick Modules, Others), End-user (Electric Vehicles (EVs), Renewable Energy, Others), Material (Gallium Nitride (GaN), Silicon Carbide (SiC), Silicon, Others), and Regional Analysis for 2025 - 2032

DC-DC Converter Market Share and Trends Analysis

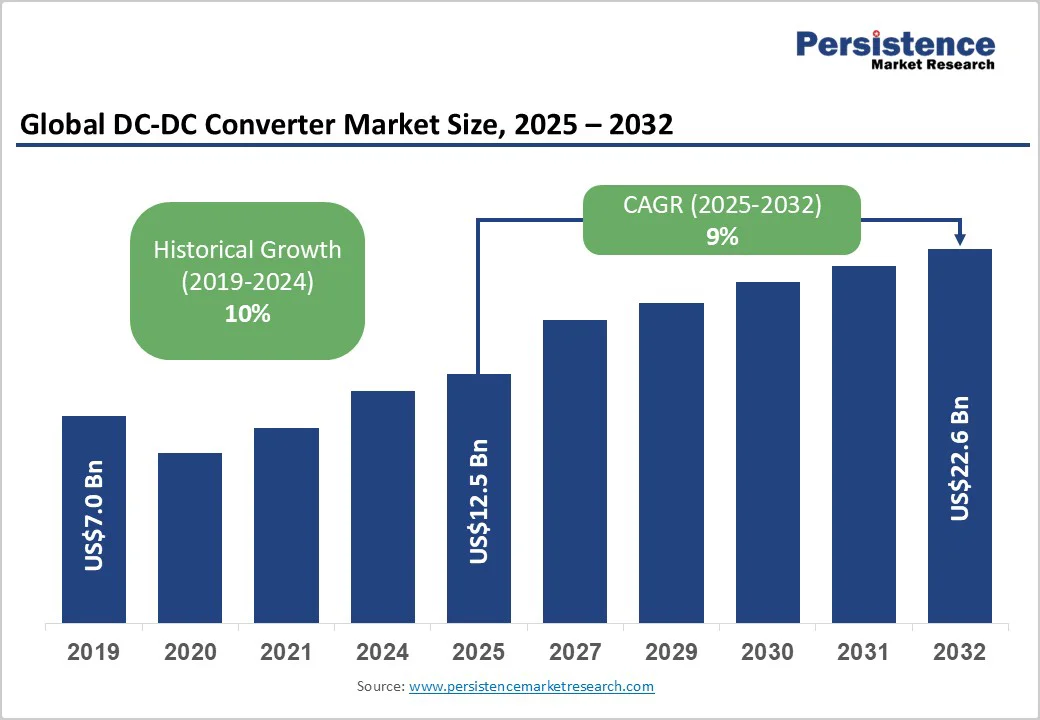

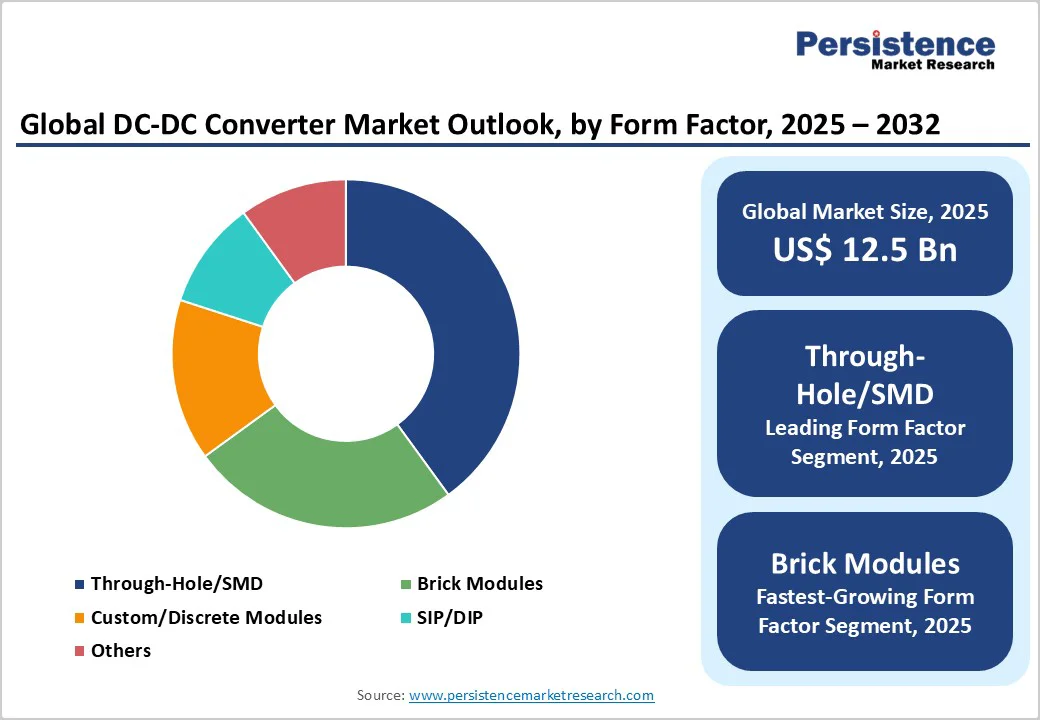

The global DC-DC converter market is expected to reach US$12.5 billion in 2025. It is estimated to reach US$22.6 billion by 2032, growing at a CAGR of 9% during the forecast period 2025−2032, driven by the escalating adoption of converters for powering electric vehicles (EVs), renewable energy systems, and data centers.

Advancements in semiconductor technology, stringent energy efficiency regulations, and rising infrastructure investments will also drive market growth. Growing demand for reliable, high-efficiency, and cost-effective power conversion systems further supports expansion. Innovations in wide-bandgap semiconductors and sustainability-focused regulations are shaping next-generation product development and deployment.

Key Industry Highlights

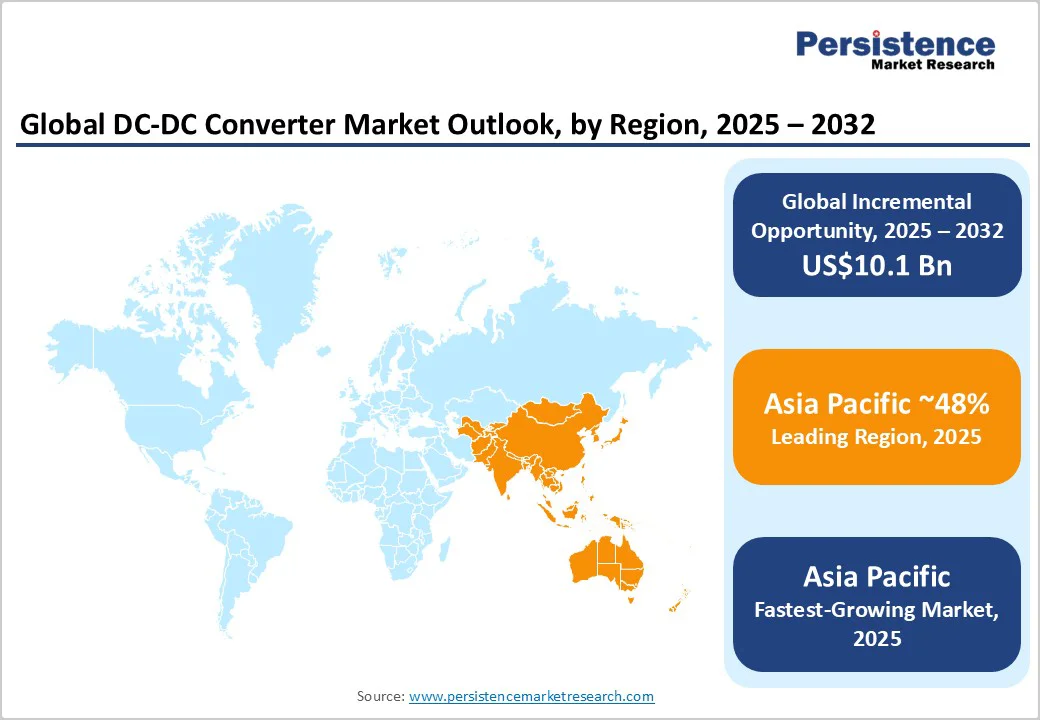

- Dominant Region: Asia Pacific is expected to dominate the market with about 48% share in 2025, driven by manufacturing and infrastructure development across China, India, and the ASEAN bloc.

- Dominant Form Factor: Surface-mount device (SMD) modules are set to hold approximately 40% of the market revenue share, on account of their compatibility with automated assembly processes and their versatility across multiple sectors.

- Fastest-growing Form Factor: The brick modules segment is projected to grow at the fastest CAGR of about 11.2% during 2025-2032, driven by the rising demand for advanced converters in high-power industrial systems and data centers.

- Leading End-user: EVs and renewable energy segments are the primary growth drivers, with combined CAGR exceeding 10% through 2032.

- Competitive Dynamics: Strategic mergers and acquisitions are rapidly consolidating the industry, especially among semiconductor innovators and system integrators.

- Key Trend: The increasing adoption of smart, connected power modules in industrial IoT and data centers will elevate efficiency standards and create new verticals.

- Demand Driver: Regulatory frameworks, such as the European Union (EU)’s Green Deal and EV incentives extended in the U.S., are catalyzing the demand for sustainable and scalable power solutions.

- October 2025: Wärtsilä announced that it is set to deliver Australia’s largest DC-coupled hybrid battery energy storage system, capable of powering up to 120,000 homes and businesses, integrating solar generation with battery storage via a DC/DC converter to reduce energy losses and optimize solar power utilization.

|

Key Insights |

Details |

|

DC-DC Converter Market Size (2025E) |

US$12.5 Bn |

|

Market Value Forecast (2032F) |

US$22.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

10% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Incorporation of DC-DC Power Modules into EVs

A critical market driver is the growing integration of high-density DC-DC power modules in EVs, accelerating the transition toward sustainable transportation. This space is characterized by the increasing penetration of electric powertrains, which demand compact, high-efficiency converters capable of handling voltages up to 1,000V. Governments worldwide are supporting this shift through incentives and regulatory mandates; for example, the European Union (EU)’s EV acceleration plans are set to increase the share of EVs in new car sales to 2030, significantly boosting demand for high-voltage power modules. Market participants are capitalizing on this opportunity by developing specialized power modules that meet stringent safety and reliability standards, especially in battery management and fast-charging systems.

Complexities in the Deployment of Advanced WBG Semiconductors

One of the most significant structural challenges hindering the DC-DC converter market growth is the variety of difficulties associated with the development and deployment of advanced wide-bandgap (WBG) semiconductor components, notably silicon carbide (SiC) and gallium nitride (GaN) devices. For instance, these components, although offering superior efficiency and thermal management, are produced with complex and costly manufacturing processes, resulting in a price premium that exceeds traditional silicon-based solutions by approximately 30-50%. This cost disparity limits growth in price-sensitive markets such as consumer electronics and small-scale industrial applications, constraining overall market penetration.

Worsening this are supply chain disruptions, exacerbated by geopolitical tensions and materials scarcity, which are affecting the availability of critical raw materials such as silicon carbide wafers. The manufacturing ecosystem for WBG power modules remains underdeveloped, with only a handful of players controlling the market, resulting in supply bottlenecks and longer lead times.

Energy Transition Ambitions of Developing Economies

Emerging economies, particularly Southeast Asia, offer a lucrative niche for market expansion, driven by rapid industrialization and government-led initiatives to promote energy efficiency and renewable energy integration. Countries such as Indonesia and Vietnam are channeling a large share of their resources annually into energy infrastructure, focusing increasingly on grid modernization and renewable power projects that require scalable, high-capacity DC-DC converters. The region’s burgeoning manufacturing sector, especially for electric vehicles and consumer electronics, underscores a considerable unmet need for customized power modules that balance cost, performance, and regulatory compliance.

Technological convergence between digital communication and power electronics, such as integrating IoT sensors into power modules, has also created a distinctive market opportunity for engineering smart, adaptive converters that optimize energy use in real time. These solutions will primarily target data centers and smart grid applications, leveraging policy shifts that promote grid resilience and renewable energy integration, such as the European Union’s Fit for 55 initiative.

Category-wise Analysis

Form Factor Insights

In 2025, the predominant form factor is likely to be surface-mount device (SMD) modules, capturing approximately 40% of the DC-DC converter market revenue share. This is primarily owing to their compatibility with automated assembly processes and their versatility across multiple sectors, including consumer electronics, industrial, and automotive applications. The high-volume manufacturing and standardization of SMT components facilitate cost efficiencies and rapid deployment.

At the same time, the brick modules segment is projected to grow at the fastest CAGR of about 11.2% between 2025 and 2032, driven by rising demand for advanced converters in high-power industrial systems and data centers that require scalable, modular solutions capable of handling high wattage and enhanced thermal dissipation. The properties of brick modules permit easier system upgrades and maintenance, making them attractive for evolving applications such as renewable energy and electric vehicle fast-charging infrastructure, where power density and reliability are critical.

End-user Insights

Automotive electrification is slated to dominate the market in 2025, with an estimated 45% share, driven by rapid EV adoption, regulatory mandates to reduce emissions, and ongoing advancements in battery management systems. The vertical is experiencing a high CAGR over 2025-2032 due to innovation in high-voltage power modules, increased average battery voltages, and the proliferation of fast-charging networks.

In contrast, renewable energy systems, including solar, wind, and hybrid grids, are emerging as the fastest-growing vertical, with a forecast CAGR of approximately 12.3% between 2025 and 2032. This growth is driven by the global push for decarbonization, policy incentives, and investments exceeding US$300 billion annually in clean energy projects. These applications require converters capable of handling wide input/output voltage ranges and fluctuating power levels, which encourage the adoption of high-capacity, high-efficiency modules with robust thermal management.

Material Insights

Silicon remains the primary semiconductor material in 2025, with an estimated 60% market share, largely due to mature manufacturing processes and lower costs. However, wide-bandgap materials, notably GaN and SiC, are rapidly gaining traction, driven by their superior efficiency, thermal management, and ability to operate at higher voltages and frequencies. SiC, in particular, is developing its niche in high-voltage industrial, aerospace, and renewable energy applications, where operational efficiency is paramount and cost can be justified by performance gains. GaN, meanwhile, is experiencing strong growth in consumer electronics, telecom, and data centers, where its high switching speeds enable ultra-compact, high-performance power modules. Market consolidation around these advanced materials indicates a significant shift in technological paradigms, fostering innovation that supports the development of smaller, more efficient, and environmentally friendly power systems.

Regional Insights

Asia Pacific DC-DC Converter Market Trends

Asia Pacific is poised to command an estimated 48% share of the global market in 2025, driven by manufacturing advantages in China, Japan, and South Korea, as well as rapid infrastructure development and renewable energy deployments. China remains the dominant force, investing over US$300 billion annually in EV infrastructure, smart grids, and industrial automation, massively fueling the demand for scalable, high-performance power modules. Japan’s focus on semiconductor innovation and eco-friendly manufacturing bolsters its leadership position, especially in GaN and SiC-based modules.

India’s burgeoning automotive sector and policy push for renewable energy are set to open extensive opportunities for vendors to supply cost-effective, high-efficiency converters that align with domestic standards. Manufacturing strengths, government incentives, and rapid urbanization contribute to this regional market’s sustained growth, making it a strategic focal point for global suppliers seeking high-volume, high-margin opportunities.

North America DC-DC Converter Market Trends

North America, expected to account for an estimated 28% of the DC-DC converter market share in 2025, is advancing rapidly through its robust energy and automotive sectors, driven by strong regulatory support for clean energy and EV adoption. The United States headlines regional growth, with investments exceeding US$250 Billion in infrastructure modernization, grid resilience, and EV charging stations. Regulatory frameworks such as the U.S. Department of Energy (DOE)’s initiatives for energy efficiency standards and California’s stringent emissions targets are compelling original equipment manufacturers (OEMs) to develop high-efficiency, compact power modules.

Innovation ecosystems concentrated in Silicon Valley and semiconductor hubs in Texas have fostered the rapid development of WBG semiconductor-based converters. The regional market is consolidating around key players leveraging advanced manufacturing capabilities and strategic partnerships with automakers and energy utilities, making it a hub for high-value, technology-rich power solutions. Future growth will likely center on integrated power modules for autonomous vehicles and grid stabilization projects, supported by federal subsidies and research grants.

Europe DC-DC Converter Market Trends

Europe is anticipated to capture a market share of approximately 23% in 2025, with Germany, the U.K., and France leading innovation and deployment activities, notably driven by stringent regulatory standards such as the EU’s Fit for 55 and Clean Energy Package, which emphasize decarbonization. These policies incentivize the adoption of high-efficiency power modules, especially in the automotive and renewable sectors. Germany’s dual focus on automotive electrification and renewable energy integration positions it as a key hub for high-performance power electronics.

Europe’s harmonized standards across member states are reducing barriers to cross-border investments, encouraging technological convergence in power modules that can operate reliably in diverse climatic and regulatory environments. The region is witnessing increased investments in R&D, niche startups focused on ultra-compact converters, and strategic alliances between automotive OEMs and semiconductor firms. The shift toward high-voltage, high-density modules in grid management and EV fast chargers underscores Europe’s strategic push toward energy independence and climate neutrality by 2040.

Competitive Landscape

The global DC-DC converter market structure remains relatively fragmented, with a few players at the top having a dominating presence. Major companies, such as Vicor Corporation, Infineon Technologies, Texas Instruments, and Mean Well, are establishing competitive advantages through a combination of proprietary technology, extensive distribution networks, and strategic collaborations. The market exhibits a mix of large, diversified industrial manufacturers and smaller, specialized firms that focus on niche segments such as aerospace-grade or automotive-specific power modules.

Vertical integration and regional manufacturing hubs contribute to increased competitive dynamics, where innovation speed and supply chain resilience define market success. The rise of WBG semiconductor manufacturers is gradually reshaping the industry structure, creating a new layer of competition focused on advanced materials and miniaturized, high-efficiency solutions.

Key Industry Developments

- In October 2025, XP Power launched a digital version of its HRF15 series 15-W DC/DC converters that feature output voltage and current programming via PMBus, enhancing automation and remote control for high-precision equipment. Compared to the analog version, the digital interface simplifies integration, reduces setup time, and improves reliability with advanced monitoring, data logging, and real-time diagnostics. The converters offer extremely low ripple and high stability, with adjustable output rails supporting constant current and voltage from 0 to 100%.

- In September 2025, VPT, Inc. introduced the VXR125-27000S, the first 270 V input DC-DC converter offering 125 W output power and operating over a 160 V to 400 V range. This model features VPT’s patented epoxy-encapsulated V-SHIELD® packaging, which ensures high chemical and environmental resistance, along with dual-sided conduction cooling for efficient thermal management. Delivering up to 89% efficiency and enhanced transient response, the converter is designed to operate at +105 °C without derating. It also meets rigorous military and aerospace standards, making it suitable for mission-critical applications.

- In September 2025, Sterling Gtake E-Mobility Ltd (SGEM) partnered with China’s Landworld Technology to locally manufacture on-board chargers and DC/DC converters at its Faridabad EV campus under a technology license and supply agreement. This collaboration is expected to generate around INR 450 crore (US$54.2 Million) in business by FY30, aligning with SGEM’s strategy to expand domestic EV component manufacturing and reduce import dependence.

Companies Covered in DC-DC Converter Market

- Vicor Corporation

- Infineon Technologies

- Texas Instruments

- ON Semiconductor

- Power Integrations

- Analog Devices

- STMicroelectronics

- Littelfuse

- Murata Manufacturing

- TDK Corporation

- ROHM Semiconductor

- Maxim Integrated

- Nexperia

- Alpha and Omega Semiconductor

Frequently Asked Questions

The DC-DC converter market is projected to reach US$12.5 Billion in 2025.

The escalating adoption of converters for powering electric vehicles (EVs), renewable energy systems, and data centers, and advancing semiconductor technologies are driving the market.

The DC-DC converter market is poised to witness a CAGR of 9% from 2025 to 2032.

Key market opportunities stem from rising demand for compact, efficient power conversion systems, innovations in wide-bandgap semiconductors, and regulations promoting sustainable energy.

The key players in the market include Vicor Corporation, Infineon Technologies, and Texas Instruments.