- Medical Devices

- Pediatric Hearing Aids Market

Pediatric Hearing Aids Market Size, Share, and Growth Forecast 2026 - 2033

Pediatric Hearing Aids Market by Product (Behind-the-Ear (BTE) Hearing Aids, Receiver-in-the-Ear (RIE) Hearing Aids, In-the-Ear (ITE) Hearing Aids, Canal Hearing Aids), Technology (Digital Hearing Aids, Analog Hearing Aids), End-user (Hospitals, Audiology Clinics, ENT Centers, Specialty Clinics), and Regional Analysis, 2026 - 2033

Pediatric Hearing Aids Market Share and Trends Analysis

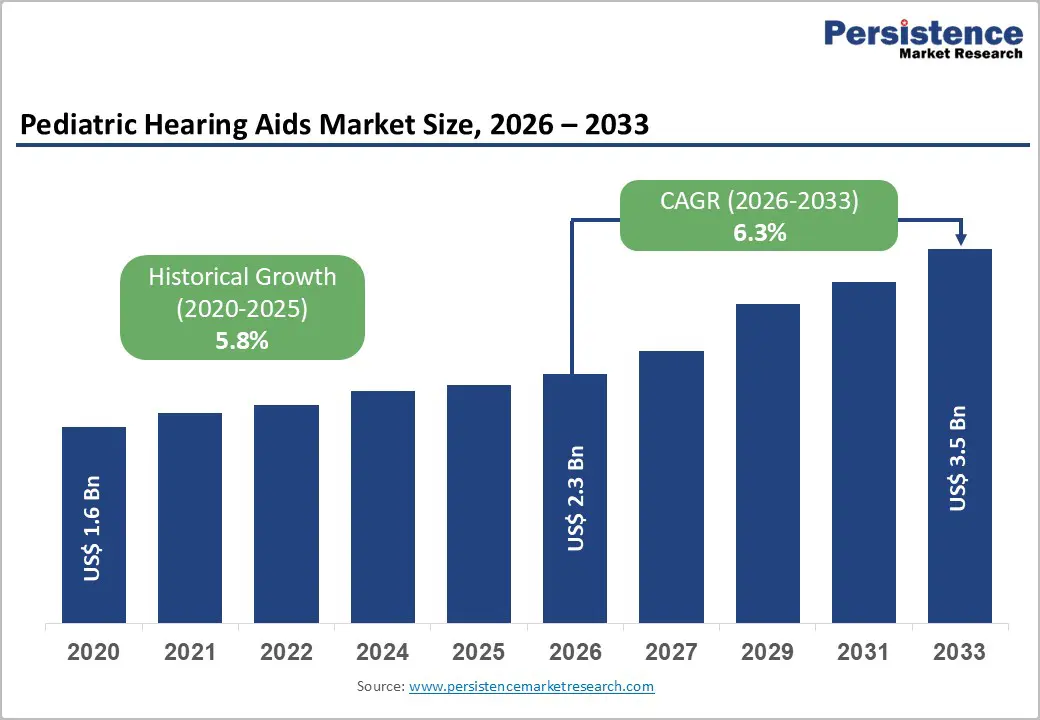

The global pediatric hearing aids market size is expected to reach US$ 2.3 billion in 2026 and US$ 3.5 billion, growing at a CAGR of 6.3% between 2026 and 2033. This consistent growth trajectory is driven by the globally recognized imperative of early hearing intervention in children, expanding universal newborn hearing screening (UNHS) programs, and rapid advances in pediatric hearing aid technology, including Bluetooth connectivity, AI-powered signal processing, and rechargeable miniaturized devices.

The World Health Organization (WHO) estimates that approximately 34 million children worldwide live with disabling hearing loss, with over 60% of childhood hearing loss attributable to preventable causes. Early-fit hearing aid intervention recommended within the first 6 months of life under the Joint Committee on Infant Hearing (JCIH) guidelines creates a large, clinically mandated addressable patient base that structurally sustains pediatric hearing aid demand across all regions through the 2033 forecast period.

Key Industry Highlights:

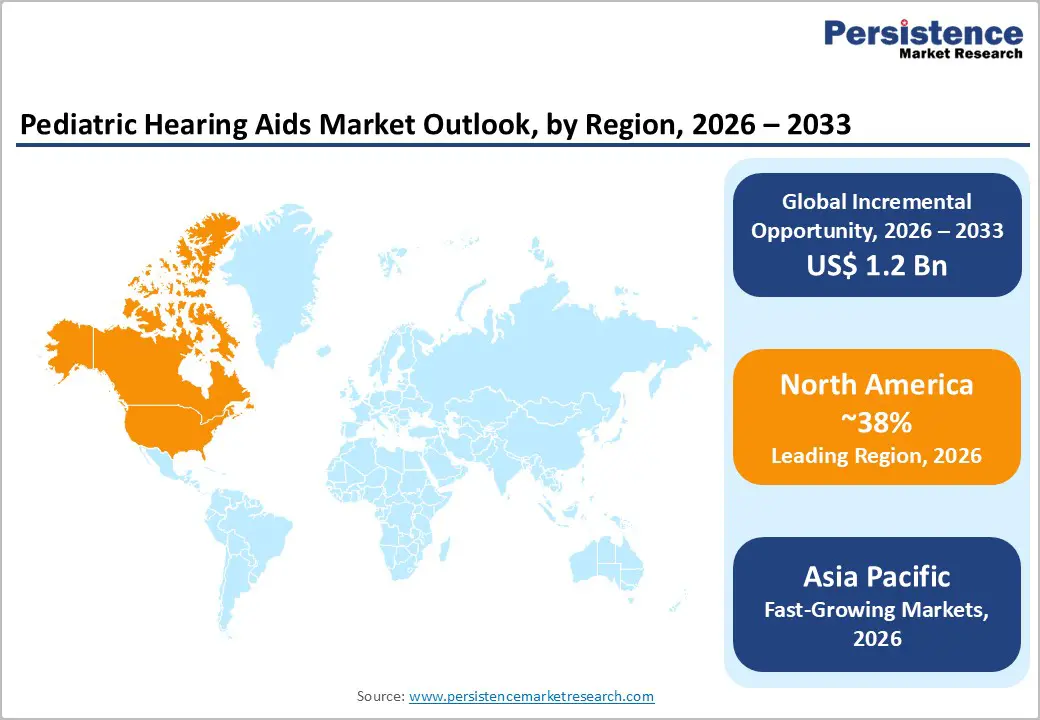

- Leading Region: North America dominates the Pediatric Hearing Aids market with approximately 38% revenue share in 2026, driven by near-universal CDC EHDI newborn hearing screening (>95% coverage), comprehensive Medicaid/CHIP reimbursement, and high advanced digital device adoption rates.

- Fast-Growing Market: Asia Pacific is the fast-growing market for pediatric hearing aids during 2026 - 2033, propelled by China's Healthy China 2030 UNHS mandates, India's RBSK screening program, and expanding audiology infrastructure across Japan, Australia, and Southeast Asian nations.

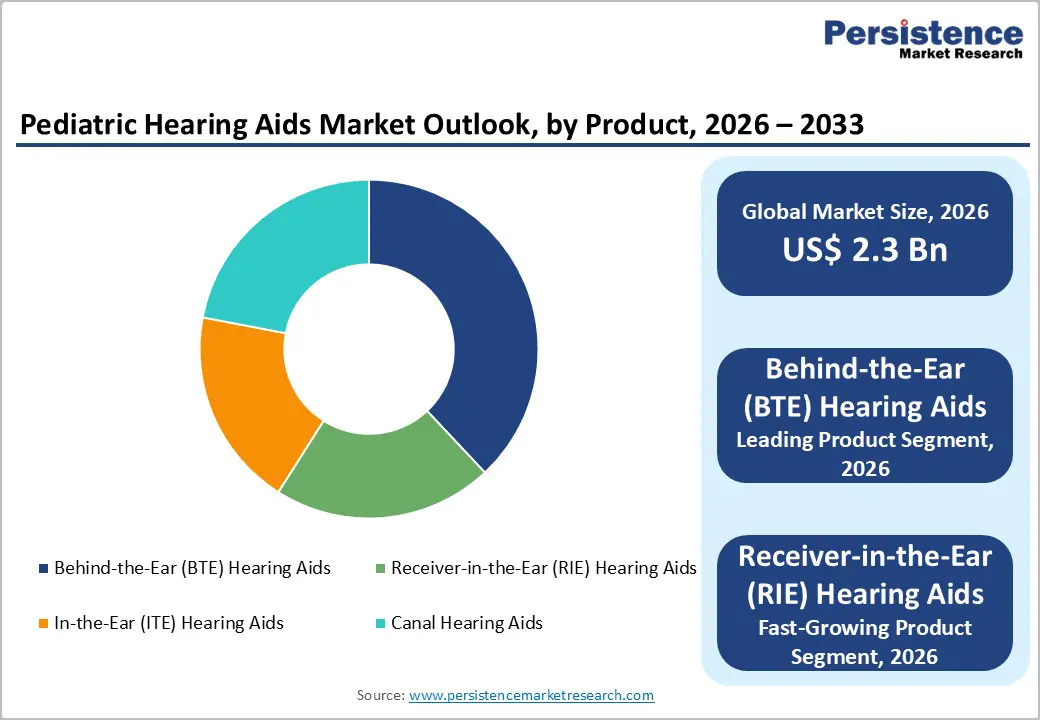

- Dominant Product Segment: Behind-the-Ear (BTE) Hearing Aids lead the product category with approximately 39% market share in 2025, preferred for their durability, adjustable ear molds accommodating growing pediatric ear canals, and clinical endorsement by AAA pediatric amplification guidelines.

- Fast-Growing Product Segment: Receiver-in-the-Ear (RIE) Hearing Aids are the fastest growing product category during 2026 - 2033, driven by superior acoustic performance, discreet form factor appealing to school-age children and adolescents, and new pediatric-focused RIE platforms from WS Audiology, GN ReSound, and Starkey.

Market Dynamics

Driver - Expansion of Universal Newborn Hearing Screening Programs and Early Intervention Mandates

Universal Newborn Hearing Screening (UNHS) programs are the single most important structural demand driver for the pediatric hearing aids market, systematically identifying infants with hearing loss at birth and triggering early hearing aid fitting. The Joint Committee on Infant Hearing (JCIH) 1-3-6 principle recommending screening by 1 month, diagnosis by 3 months, and intervention by 6 months, has been adopted across 48 U.S. states and is increasingly mandated in EU member states, Australia, Japan, and other high-income nations.

UNHS coverage now exceeds 95% of births in the U.S., according to the CDC's Early Hearing Detection and Intervention (EHDI) program, with annual identification of approximately 12,000 newborns with hearing loss in the U.S. alone. Each identified child creates a multi-year hearing aid fitting, follow-up, and upgrade cycle that sustains recurring device revenue.

Technological Innovation in Pediatric-Specific Digital Hearing Aid Platforms

Rapid advances in pediatric hearing aid technology are expanding clinical adoption and enabling premium product positioning that supports revenue growth. Modern pediatric digital hearing aids, exemplified by Sonova's Phonak Sky Marvel and Demant's Oticon Play PX, incorporate AI-powered speech enhancement, dedicated pediatric fitting software, real-ear measurement integration, and direct Bluetooth streaming from smartphones and educational audio systems such as Roger (Phonak).

The American Academy of Audiology (AAA) and American Speech-Language-Hearing Association (ASHA) clinical guidelines increasingly cite evidence supporting the use of advanced digital processing features in pediatric fittings to maximize speech intelligibility in noisy classroom environments. Connectivity features enabling real-time audiologist remote programming further extend product value and deepen brand loyalty among pediatric audiology practices and families, supporting premium pricing and repeat upgrade cycles.

Restraints - Shortage of Pediatric Audiologists and Specialized Fitting Expertise

Pediatric hearing aid fitting is a highly specialized clinical competency requiring expertise in ear canal acoustics, child development, and pediatric audiological assessment tools. The American Academy of Audiology (AAA) estimates a growing shortage of pediatric audiologists in the U.S., with rural and underserved communities facing wait times of 3-6 months for pediatric audiology appointments.

Globally, the WHO reports that over 80% of countries with high childhood hearing loss burden have fewer than one audiologist per million population, severely constraining timely device fitting and follow-up care that is essential for effective pediatric hearing aid outcomes.

Opportunities - Receiver-in-the-Ear (RIE) Hearing Aids as the Fastest Growing Product Segment

Receiver-in-the-Ear (RIE) hearing aids represent the fastest growing product segment in the pediatric hearing aids market, driven by their superior acoustic performance, discreet profile, and increasing suitability for older pediatric patients and adolescents seeking cosmetically acceptable solutions.

RIE devices provide higher gain bandwidth than traditional BTE models without sacrificing comfort or Bluetooth connectivity features validated in clinical studies published in the International Journal of Audiology. As children transition from infancy through school age and adolescence, the preference for less conspicuous hearing aids creates a sequential upgrade market opportunity from BTE in early childhood to RIE in later pediatric years. Companies, including WS Audiology's Signia, GN ReSound, and Starkey Laboratories, are launching pediatric-focused RIE platforms that target this transitional patient cohort with age-appropriate features and fitting software.

Asia Pacific Market Expansion Through Newborn Screening Scale-Up and Affordability Programs

Asia Pacific represents the fastest-growing regional market for pediatric hearing aids, with government-led newborn hearing screening expansion programs in China, India, Japan, and Australia creating a rapidly growing pipeline of newly diagnosed pediatric patients requiring hearing aid fitting. China's National Health Commission has mandated UNHS expansion as part of the Healthy China 2030 initiative, with screening coverage projected to reach 90%+ of newborns nationally.

India's Rashtriya Bal Swasthya Karyakram (RBSK) program conducts free hearing screening across 0-18-year age groups in government health facilities, identifying large volumes of hearing-impaired children. Manufacturers that develop cost-optimized, locally manufactured, or government-subsidized pediatric hearing aid platforms for these markets, including Cochlear Limited and WS Audiology, are positioned to capture a disproportionate share of the Asia Pacific's high-growth trajectory.

Category-wise Analysis

Product Insights

The Behind-the-Ear (BTE) Hearing Aids segment dominates the Pediatric Hearing Aids market, accounting for approximately 39% of total product revenue in 2026. BTE devices are the clinical gold standard for pediatric fittings due to their robust durability, ease of handling by caregivers, compatibility with external receivers and ear molds that can be replaced as a child's ear canal grows, and ability to accommodate a wide range of hearing loss severities from mild to profound.

The American Academy of Audiology (AAA) pediatric amplification guidelines specifically recommend BTE configurations for young children. Leading BTE pediatric platforms, including Phonak Sky (Sonova), Oticon Play (Demant), and Signia Fun (WS Audiology) are clinically validated and widely specified by pediatric audiology practices globally, reinforcing BTE's durable market leadership.

Technology Insights

The digital hearing aids segment leads the technology category, accounting for approximately 91% of technology-based market revenue in 2026. Digital signal processing (DSP) technology has become the universal standard in pediatric audiology practice, enabling real-time automatic environment classification, directional microphone processing, noise reduction, and tinnitus management features that are clinically essential for speech and language development outcomes in hearing-impaired children.

The transition from analog to digital was accelerated by FDA and CE-mark regulatory requirements, and the ASHA and AAA no longer recommend analog devices for pediatric fittings. The residual analog segment serves only specific low-resource settings where digital devices are cost-prohibitive, with its share projected to decline further as digital manufacturing costs continue to fall through the forecast period.

End-user Insights

The Audiology clinics segment leads the pediatric hearing aids market, representing approximately 43% of end-user revenue in 2026. Specialized pediatric audiology clinics are the primary point of hearing aid fitting, programming, and follow-up care for children with hearing loss, as they employ pediatric audiologists with the expertise and equipment, including real-ear measurement systems, pediatric sound booths, and age-appropriate behavioral audiometry protocols required for high-quality pediatric fittings.

Referral pathways from hospital-based UNHS programs and ENT physicians consistently direct pediatric hearing aid cases to audiology clinic settings. The American Academy of Audiology and its international counterparts actively promote clinic-based fitting as best practice, sustaining the audiology clinic channel's dominant position throughout the forecast horizon.

Regional Insights

North America Pediatric Hearing Aids Market Trends and Insights

North America leads the global Pediatric Hearing Aids market with approximately 38% of total revenue in 2025. The region benefits from near-universal newborn hearing screening coverage (>95% in the U.S., CDC EHDI), strong insurance reimbursement pathways including Medicaid and CHIP coverage for pediatric hearing aids in all states, and a dense network of pediatric audiology clinics. Advanced digital and AI-powered pediatric hearing aid adoption rates are the highest globally in this region.

U.S. Pediatric Hearing Aids Market Size

The U.S. accounts for approximately 87% of North America's pediatric hearing aids revenue, driven by the CDC EHDI program identifying approximately 12,000 newborns with hearing loss annually. Comprehensive Medicaid Early and Periodic Screening, Diagnostic, and Treatment (EPSDT) benefit mandates pediatric hearing aid coverage for low-income children, while the Individuals with Disabilities Education Act (IDEA) supports school-age hearing device funding.

Europe Pediatric Hearing Aids Market Trends and Insights

Europe is the second-largest regional market, characterized by strong national health service reimbursement frameworks and established pediatric audiology infrastructure. NHS provision in the U.K., statutory coverage in Germany under GKV, and subsidized programs in France and Scandinavia ensure high device uptake among diagnosed children. EU harmonization of newborn hearing screening is progressing through EuroHear network initiatives, driving consistent regional demand growth.

Germany Pediatric Hearing Aids Market Size

Germany accounts for approximately 22% of European pediatric hearing aids revenue. The GKV (statutory health insurance) framework mandates coverage of medically indicated pediatric hearing aids, and Germany's newborn hearing screening law (2009) ensures near-universal birth screening. Sonova, Demant, and WS Audiology maintain strong commercial presence, supported by Germany's world-class pediatric audiology training institutions.

U.K. Pediatric Hearing Aids Market Size

The U.K. represents approximately 19% of the European market revenue. The NHS Newborn Hearing Screening Programme (NHSP) achieves screening coverage exceeding 99% of births, feeding a well-developed NHS audiology service that provides digital BTE hearing aids free at point of care. NHS digital hearing aid upgrades and teleaudiology follow-up services are creating demand for connected device platforms from leading manufacturers.

France Pediatric Hearing Aids Market Size

France contributes approximately 15% of the European pediatric hearing aids market. The 100% Santé reform (2021) and Assurance Maladie reimbursement frameworks provide full coverage for pediatric hearing aids up to defined price caps, significantly expanding access. France's CAMSP (early childhood medico-social centers) provide integrated audiology, speech therapy, and hearing aid fitting services for children under 6, creating a structured early-intervention funnel.

Asia Pacific Pediatric Hearing Aids Market Trends and Insights

Asia Pacific is the fast-growing regional market, expected to register a positive CAGR in the forecast period. China is a wide market driven by the Healthy China mission 2030, UNHS mandates, and expanding public hospital audiology capacity across tier-2 and tier-3 cities. Japan, Australia, South Korea, and India are also scaling pediatric hearing screening and device access programs. Regional growth is further supported by rising middle-class healthcare expenditure and increasing awareness of early hearing intervention benefits.

India Pediatric Hearing Aids Market Size

India accounts for approximately 14% of the Asia Pacific's pediatric hearing aids revenue. The Rashtriya Bal Swasthya Karyakram (RBSK) program screens 0-18-year-olds across government facilities, while the ADIP (Assistance to Disabled Persons) scheme subsidizes hearing aids for below-poverty-line children. Domestic manufacturers and international brands, including Sivantos (WS Audiology) are localizing affordable BTE models for India's price-sensitive market.

Competitive Landscape

The pediatric hearing aids market is highly competitive, driven by rising awareness of early hearing loss diagnosis and the growing importance of timely intervention in children. Companies compete through advanced digital technologies, wireless connectivity, noise reduction features, and child-friendly designs that improve comfort and usability. Strong focus is placed on durability, customization, and compatibility with educational and assistive listening devices. Regulatory approvals and partnerships with hospitals, audiology centers, and hearing clinics play a major role in market expansion. Increasing investments in research, product innovation, and affordable solutions continue to strengthen competition across developed and emerging healthcare markets.

Key Developments

- In April 2026, Oticon introduced its Play SI pediatric hearing aid family, designed specifically for children and teenagers with hearing loss. The new range featured second-generation AI-powered sound processing trained on millions of sound scenes, 4D user-intent sensors for real-time listening adaptation, and Bluetooth LE Audio connectivity for hands-free calls and Auracast access.

- In April 2026, Western University launched the ALLEars project, a large-scale collaboration with Boys Town National Research Hospital, to develop AI-powered custom earmolds for children using hearing aids.

Companies Covered in Pediatric Hearing Aids Market

- Sonova Holding AG

- Demant A/S

- WS Audiology

- GN Store Nord A/S

- Starkey Laboratories, Inc.

- Cochlear Limited

- MED-EL

- Sivantos Pte. Ltd.

- RION Co., Ltd.

- Horentek Hearing Diagnostics

- Audina Hearing Instruments

- Sebotek Hearing Systems

- Eargo, Inc.

Frequently Asked Questions

The global Pediatric Hearing Aids market is estimated to be valued at US$ 2.3 billion in 2026.

The primary demand drivers include expanding universal newborn hearing screening programs with CDC EHDI achieving >95% U.S. birth coverage and identifying approximately 12,000 newborns with hearing loss annually, combined with the WHO estimate of 34 million children globally living with disabling hearing loss, JCIH early intervention mandates, and rapid advances in AI-powered digital pediatric hearing aid platforms.

North America leads with approximately 38% of global pediatric hearing aids revenue in 2025.

Two key opportunities include the Receiver-in-the-Ear (RIE) segment the fastest growing product category driven by adolescent preference for discreet devices and new pediatric RIE platforms from WS Audiology, Starkey, and GN ReSound; and Asia Pacific market expansion through government-mandated UNHS programs in China (Healthy China 2030) and India (RBSK), which are systematically generating large volumes of newly diagnosed pediatric patients requiring device fitting.

The market is dominated by five global hearing health companies: Sonova Holding AG (Phonak Sky), Demant A/S (Oticon Play), WS Audiology (Signia Fun, Widex), GN Store Nord A/S (ReSound), and Starkey Laboratories.