- Executive Summary

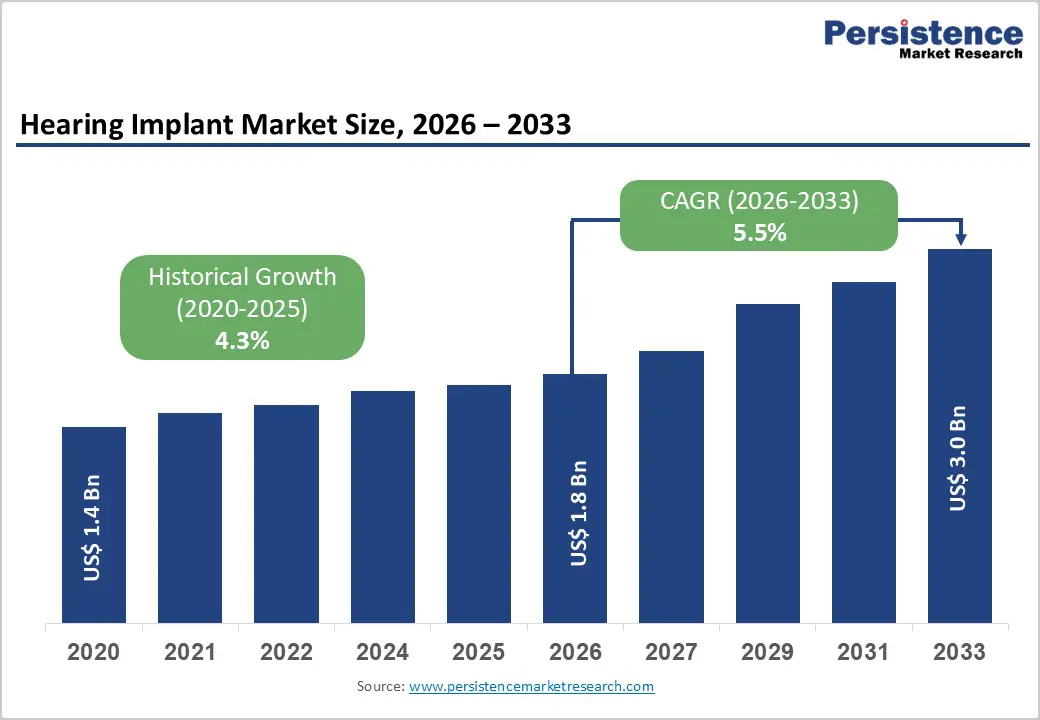

- Global Hearing Implant Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Product Adoption Analysis

- Recent Product Launches

- Regulatory Landscape

- Value Chain Analysis

- Key Deals and Mergers

- PESTLE Analysis

- Porter’s Five Force Analysis

- Price Trend Analysis, 2020 - 2033

- Key Highlights

- Key Factors Impacting Product Prices

- Pricing Analysis, By Product Type

- Regional Prices and Product Preferences

- Global Hearing Implant Market Outlook:

- Key Highlights

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, 2026-2033

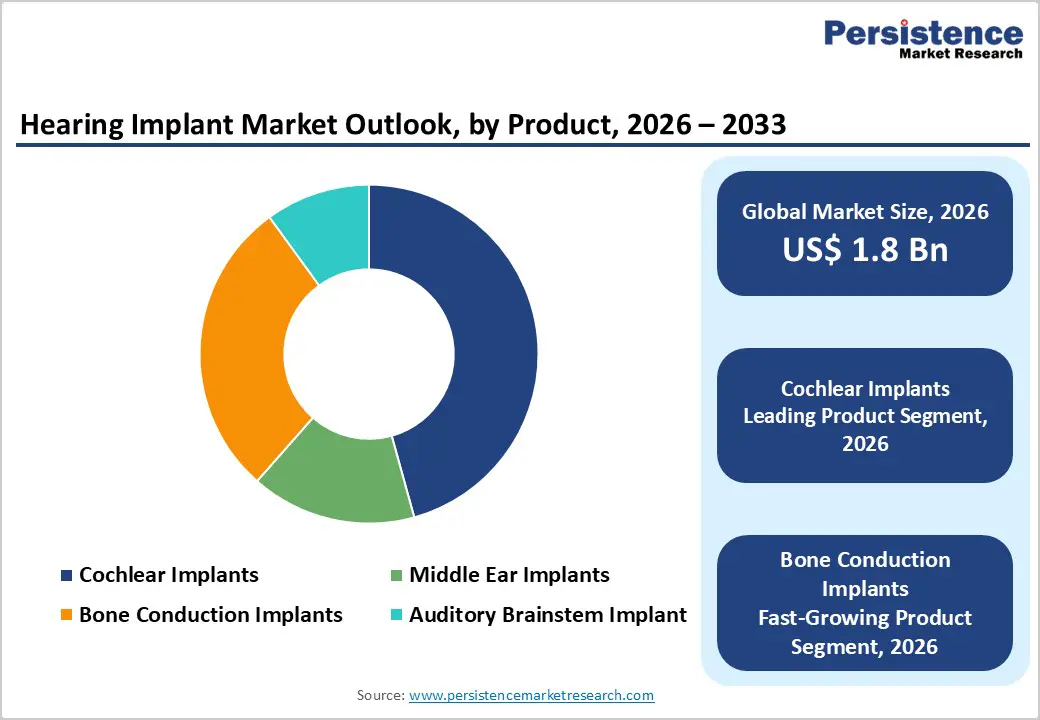

- Global Hearing Implant Market Outlook: Product

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis and Volume (Units) Analysis, By Product, 2020 - 2025

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Product, 2026 - 2033

- Cochlear Implants

- Middle Ear Implants

- Bone Conduction Implants

- Auditory Brainstem Implant

- Market Attractiveness Analysis: By Product

- Global Hearing Implant Market Outlook: End User

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By End User, 2020 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Hospitals

- ENT clinics

- Ambulatory Surgery Centers

- Market Attractiveness Analysis: End User

- Key Highlights

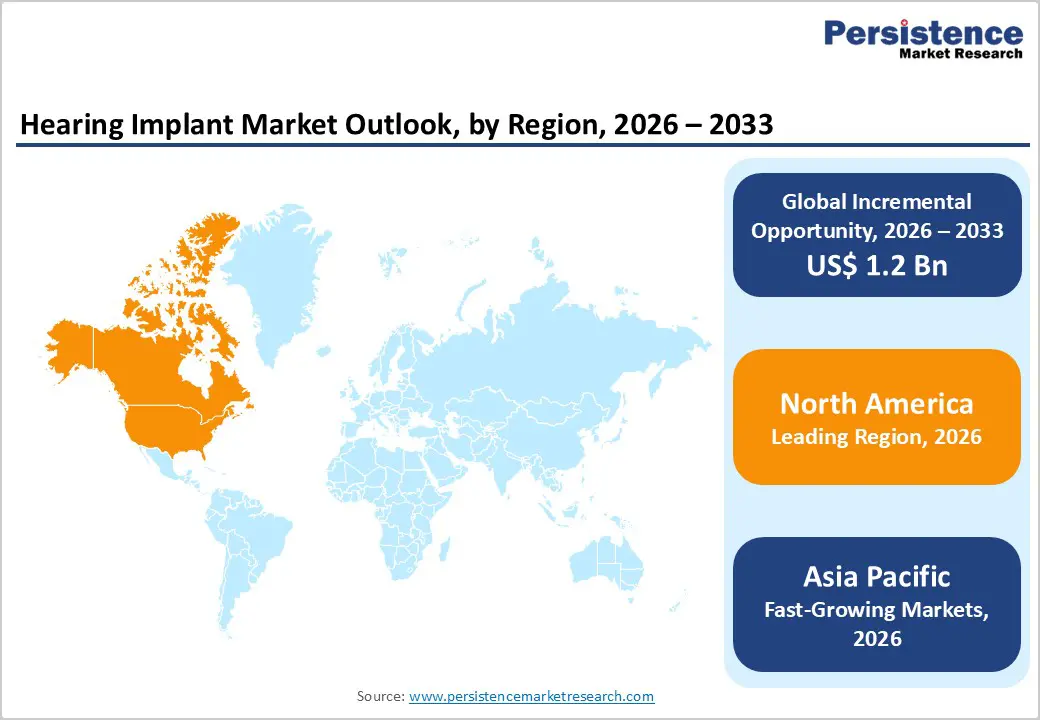

- Global Hearing Implant Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Region, 2020 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By Region, 2026 - 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Hearing Implant Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- U.S.

- Canada

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Product, 2026 - 2033

- Cochlear Implants

- Middle Ear Implants

- Bone Conduction Implants

- Auditory Brainstem Implant

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Hospitals

- ENT clinics

- Ambulatory Surgery Centers

- Market Attractiveness Analysis

- Europe Hearing Implant Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Product, 2026 - 2033

- Cochlear Implants

- Middle Ear Implants

- Bone Conduction Implants

- Auditory Brainstem Implant

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Hospitals

- ENT clinics

- Ambulatory Surgery Centers

- Market Attractiveness Analysis

- East Asia Hearing Implant Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product

- End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- China

- Japan

- South Korea

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Product, 2026 - 2033

- Cochlear Implants

- Middle Ear Implants

- Bone Conduction Implants

- Auditory Brainstem Implant

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Hospitals

- ENT clinics

- Ambulatory Surgery Centers

- Market Attractiveness Analysis

- South Asia & Oceania Hearing Implant Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Product, 2026 - 2033

- Cochlear Implants

- Middle Ear Implants

- Bone Conduction Implants

- Auditory Brainstem Implant

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Hospitals

- ENT clinics

- Ambulatory Surgery Centers

- Market Attractiveness Analysis

- Latin America Hearing Implant Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Product, 2026 - 2033

- Cochlear Implants

- Middle Ear Implants

- Bone Conduction Implants

- Auditory Brainstem Implant

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Hospitals

- ENT clinics

- Ambulatory Surgery Centers

- Market Attractiveness Analysis

- Middle East & Africa Hearing Implant Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Product, 2026 - 2033

- Cochlear Implants

- Middle Ear Implants

- Bone Conduction Implants

- Auditory Brainstem Implant

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Hospitals

- ENT clinics

- Ambulatory Surgery Centers

- Market Attractiveness Analysis

- Competition Landscape

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Recent Developments)

- Cochlear Limited

- Overview

- Segments and Product & End User

- Key Financials

- Market Developments

- Market Strategy

- MED-EL Medical Electronics.

- Advanced Bionics AG

- Oticon Medical

- Medtronic

- Demant A/S

- WS Audiology A/S

- ZHEJIANG NUROTRON BIOTECHNOLOGY CO., LTD.

- Starkey Laboratories, Inc

- Unitron

- TODOC Co., Ltd.

- Neubio AG.

- Envoy Medical Corporation

- Others

- Cochlear Limited

- Market Structure

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

Loading page data

Please wait a moment