- Medical Devices

- Neonatal Hearing Screening Devices Market

Neonatal Hearing Screening Devices Market Size, Share, and Growth Forecast 2026 - 2033

Neonatal Hearing Screening Devices Market by Product Type (Auditory Brainstem Response (ABR), Otoacoustic Emission (OAE), Combination), Modality (Table Top, Trolley Mounted, Portable and Hand-held), by End User (Hospitals, Specialty Clinics, Others), and Regional Analysis, 2026–2033

Neonatal Hearing Screening Devices Market Share and Trends Analysis

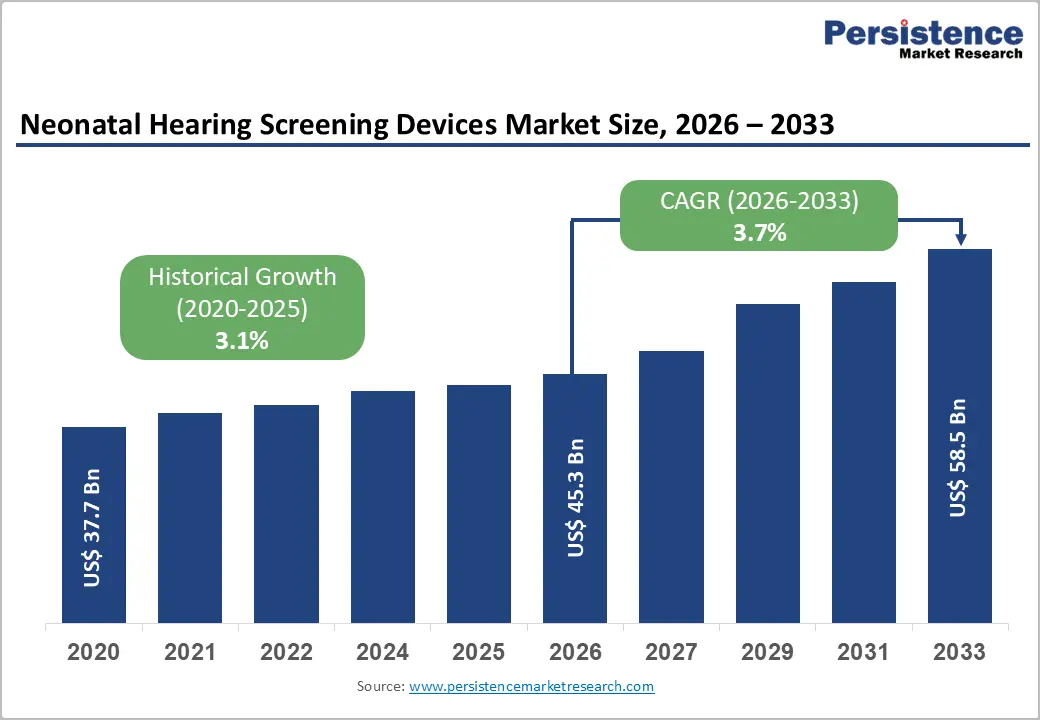

The global neonatal hearing screening devices market size is expected to be valued at US$ 45.3 billion in 2026 and projected to reach US$ 58.5 billion by 2033, growing at a CAGR of 3.7% between 2026 and 2033.

Steady market expansion is driven by the global adoption of universal newborn hearing screening (UNHS) programs and increasing government mandates for early hearing detection and intervention (EHDI). According to the World Health Organization (WHO), approximately 34 million children globally experience disabling hearing loss, with early screening recognized as the most effective pathway to timely intervention. The convergence of technological advances in portable and automated ABR and OAE devices with expanding neonatal care infrastructure across Asia-Pacific and Latin America is reinforcing consistent demand growth across all major geographies.

Key Industry Highlights:

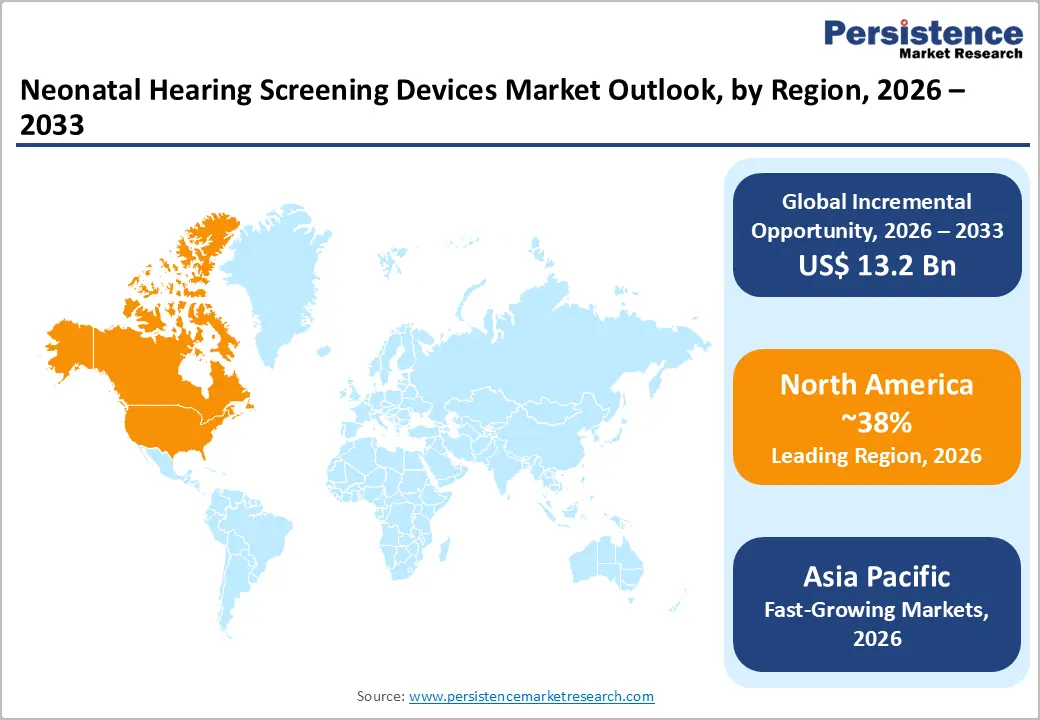

- Regional Leadership: North America dominates the global neonatal hearing screening devices market with approximately 38% share in 2025, supported by near-universal EHDI program coverage across the United States, strong reimbursement frameworks, and high adoption of advanced ABR and OAE screening technologies.

- Fast-growing Regional Market: Asia Pacific is the fast-growing region for neonatal hearing screening devices, driven by 40+ million annual births across China and India, China's National Neonatal Disease Screening Program, and India's RBSK mandate expanding institutional device procurement.

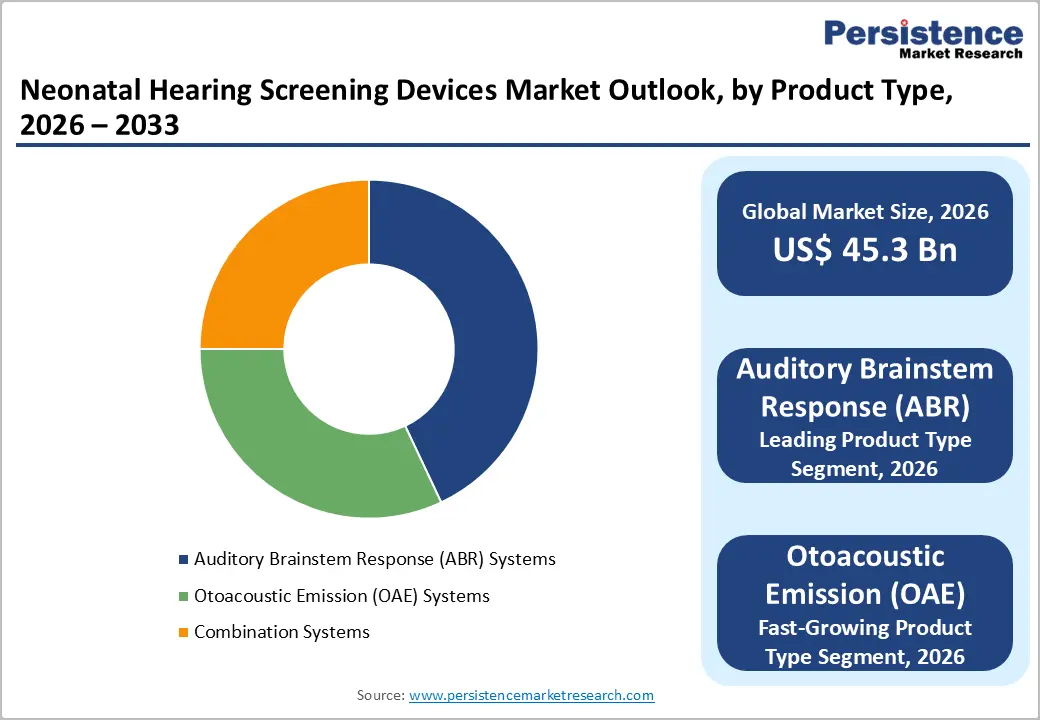

- Auditory Brainstem Response (ABR) devices lead the product type segment with approximately 43% market share in 2025, endorsed by the Joint Committee on Infant Hearing (JCIH) as the preferred NICU screening modality, driving consistent hospital procurement from manufacturers including Natus Medical and Grason-Stadler (GSI).

- Otoacoustic Emission (OAE) devices represent the fastest-growing product segment, propelled by their cost-effectiveness, speed, and suitability for well-baby nursery screening programs, with portable OAE devices gaining traction in community health deployments across Asia-Pacific and Latin American emerging markets.

- The key market opportunity lies in AI-integrated teleaudiology screening platforms and portable device expansion into LMICs, where the WHO estimates over 34 million children globally experience disabling hearing loss, with early detection rates critically low in underserved regions.

Market Dynamics

Drivers

Expansion of Universal Newborn Hearing Screening (UNHS) Mandates

Government-mandated universal newborn hearing screening programs constitute the most powerful structural demand driver for the neonatal hearing screening devices market. In the United States, the Early Hearing Detection and Intervention (EHDI) program administered by the Centers for Disease Control and Prevention (CDC) has driven neonatal hearing screening rates to over 98% of all U.S. newborns annually. In Europe, the European Consensus Statement on Neonatal Hearing Screening, endorsed by the European Federation of Audiology Societies (EFAS) has catalyzed national UNHS program implementations across member states.

As countries in Asia-Pacific and Latin America progressively legislate screening requirements, demand for both ABR and OAE devices is set to expand materially over the forecast period, creating durable volume growth across device categories and geographies.

Rising Global Birth Rates and Growing Neonatal Healthcare Infrastructure

Global birth volumes remain a foundational demand determinant for neonatal hearing screening devices. The United Nations Population Fund (UNFPA) estimates approximately 140 million births annually worldwide, each representing a potential screening event. Simultaneously, significant investments in neonatal intensive care unit (NICU) infrastructure, particularly across emerging economies in India, China, and Southeast Asia, are broadening the installed base for hearing screening equipment.

The World Bank reports consistent increases in health expenditure as a percentage of GDP across South and Southeast Asia, directly supporting procurement of diagnostic neonatal equipment. This intersection of high birth volumes and expanding healthcare infrastructure creates a structurally growing addressable market for neonatal hearing screening device manufacturers globally.

Restraints

High Device Costs and Budget Constraints in Low-Income Markets

Advanced neonatal hearing screening devices, particularly automated ABR systems, carry significant acquisition costs ranging from US$ 5,000 to US$ 30,000 per unit, creating substantial adoption barriers in low- and middle-income country (LMIC) healthcare systems. The WHO Global Hearing Report 2021 highlights that the majority of the world's unscreened neonatal population resides in LMICs where per-capita healthcare budgets are severely constrained, limiting public procurement capability and sustaining significant screening coverage gaps despite the clinical necessity of early hearing diagnosis.

Shortage of Trained Audiologists and Skilled Healthcare Personnel

Effective deployment of neonatal hearing screening programs requires not only device procurement but also adequate numbers of trained audiological professionals for device operation, result interpretation, and follow-up diagnostic referrals. The WHO estimates a global shortage of approximately 250,000 audiologists, with the deficit most acute in Sub-Saharan Africa and South Asia.

This workforce constraint limits the scalability of institutional screening programs, creates operational bottlenecks even where devices are available, and slows the conversion of rising newborn volumes into active screening encounters, moderating overall market growth potential in underserved regions.

Opportunities

Growth of Portable and Automated Screening Devices for Community-Level Deployment

The development and commercialization of portable, battery-operated, and automated neonatal hearing screening devices represents a transformational opportunity for market participants targeting underserved geographies. Traditional tabletop ABR and OAE systems require fixed clinical infrastructure, whereas next-generation handheld and portable devices such as those developed by Interacoustics A/S and Vivosonic Inc. enable community health workers and primary care personnel to conduct screenings in rural clinics, birthing centers, and home settings.

India's Rashtriya Bal Swasthya Karyakram (RBSK) program, which mandates health screening for all children under 18 including newborn hearing assessment, demonstrates the policy-driven demand potential for portable screening solutions across LMIC markets. The combination of miniaturization, automation, and connectivity in emerging device models substantially expands the deployable installed base.

Integration of Teleaudiology and AI-Powered Screening Analytics

The convergence of telehealth infrastructure and artificial intelligence with neonatal hearing screening creates a compelling emerging market opportunity. AI-driven automated interpretation of ABR waveforms and OAE signal patterns is progressively reducing reliance on specialist audiologist review, enabling high-throughput screening in resource-constrained environments. Companies, including Natus Medical Incorporated and Intelligent Hearing Systems (IHS) are investing in cloud-connected screening platforms that enable remote result review and follow-up referral management.

The American Academy of Audiology (AAA) has endorsed teleaudiology frameworks as viable models for expanding diagnostic reach. With global telehealth adoption accelerating post-pandemic, hearing screening device manufacturers that integrate teleaudiology capabilities into their platforms are positioned to unlock significant incremental demand in both established and emerging markets.

Category-wise Analysis

Product Type Insights

The Auditory Brainstem Response (ABR) segment leads the neonatal hearing screening devices market by product type, commanding approximately 43% of total market share in 2025. ABR testing's clinical superiority in detecting auditory neuropathy spectrum disorder (ANSD) and sensorineural hearing loss, particularly in high-risk neonates in NICUs, underpins its dominant market position.

The Joint Committee on Infant Hearing (JCIH) in its 2019 Position Statement explicitly recommends ABR as the preferred screening modality for NICU infants, given its ability to assess the entire auditory pathway from the cochlea to the brainstem. Key suppliers, including Natus Medical Incorporated, MAICO Diagnostics GmbH, and Grason-Stadler (GSI) have established strong ABR device portfolios, further consolidating the segment's leading position.

Modality Insights

The tabletop modality segment leads the neonatal hearing screening devices market, accounting for approximately 40% of the modality-based market share in 2025. Tabletop devices remain the workhorse of hospital-based newborn hearing screening programs, offering the highest measurement accuracy, comprehensive diagnostic capability, and robust connectivity to electronic health record (EHR) systems for automated data documentation. Major birthing hospitals with high annual delivery volumes typically exceeding 1,000 births per year standardize on tabletop ABR and OAE systems for their structured screening workflows.

Manufacturers such as GN Otometrics and Interacoustics A/S hold strong positions in the tabletop segment. However, the portable and handheld modality segment is growing rapidly, driven by community-level screening program expansion across the Asia Pacific and Africa.

End-user Insights

Hospitals represent the dominant end-user segment in the neonatal hearing screening devices market, capturing approximately 65% of the total end-user segment share in 2025. Hospitals' leadership position is anchored by their role as the primary site for newborn delivery and initial health assessment across virtually all global healthcare systems. Birthing hospitals are the mandated first point of universal hearing screening under EHDI and equivalent national programs, creating obligatory device procurement requirements regardless of budget cycles.

According to the CDC EHDI Data Summary, over 3.7 million newborns were screened for hearing loss in U.S. hospitals in 2021 alone. The concentration of NICU infrastructure where ABR screening is clinically mandated for high-risk infants further reinforces hospitals as the primary institutional buyer of neonatal hearing screening devices globally.

Regional Insights

North America Neonatal Hearing Screening Devices Market Trends and Insights

North America leads the global neonatal hearing screening devices market with approximately 38% of total market share in 2025, driven by near-universal EHDI program implementation, strong reimbursement frameworks, and a mature installed base of screening devices across hospital birthing centers. Rising investment in connected screening platforms and AI-assisted interpretation tools is defining the region's next competitive horizon.

U.S. Neonatal Hearing Screening Devices Market Size

The United States accounts for approximately 85% of the North American market share in 2025, underpinned by the federally coordinated EHDI program achieving over 98% newborn screening coverage. Demand is sustained by device refresh cycles, technology upgrades toward automated and cloud-connected platforms, and NICU expansion projects at leading academic medical centers.

Europe Neonatal Hearing Screening Devices Market Trends and Insights

Europe holds a significant market position in neonatal hearing screening devices, with a heterogeneous landscape of national UNHS programs at varying levels of maturity across member states. Western European markets exhibit high device penetration and demand for technology refresh, while Eastern European markets offer growth potential as national screening mandates are progressively implemented under EU public health frameworks.

Germany Neonatal Hearing Screening Devices Market Size

Germany represents the largest European national market, accounting for approximately 20% of the European regional share in 2025. Germany's mandatory universal newborn hearing screening program operational since 2009 under directives of the Gemeinsamer Bundesausschuss (G-BA) generates consistent annual device procurement volume, supported by leading local manufacturers and strong clinical research ecosystems in audiology.

U.K. Neonatal Hearing Screening Devices Market Size

The United Kingdom holds approximately 16% of the European market share in 2025. The NHS Newborn Hearing Screening Programme (NHSP), operational since 2006, delivers structured OAE-based screening to over 700,000 newborns annually. Ongoing NHS digitalization investments and device fleet renewals sustain consistent demand for AABR and OAE screening equipment from established manufacturers.

Asia Pacific Neonatal Hearing Screening Devices Market Trends and Insights

Asia-Pacific is the fastest-growing regional market for neonatal hearing screening devices, fueled by high birth volumes, with China and India together accounting for over 40 million births annually, and the progressive expansion of national newborn screening programs. China's National Program for Neonatal Disease Screening has significantly boosted device demand, with urban hospital coverage rates exceeding 90% in major cities according to government health commission data.

India Neonatal Hearing Screening Devices Market Size

India represents the highest-growth national opportunity in Asia-Pacific, holding approximately 16% of regional market share in 2025. India's RBSK program mandating childhood health screening and the government's Ayushman Bharat health infrastructure expansion are creating new institutional procurement channels. However, significant rural-urban screening coverage disparities present both a challenge and a growth opportunity for portable device manufacturers.

Competitive Landscape

The neonatal hearing screening devices market is moderately consolidated, with competition driven by technological innovation, product accuracy, portability, and integration with hospital workflows. Companies focus on developing advanced OAE and ABR systems that offer faster screening, improved sensitivity, and user-friendly interfaces for neonatal and NICU settings. Strategic collaborations with hospitals, maternity centers, and public health programs strengthen market reach and recurring demand. Regulatory compliance and adherence to newborn screening standards remain critical competitive factors.

Key Developments

- In January 2026, Moldova successfully achieved a 95.3% national coverage rate in universal newborn hearing screening, meeting World Health Organization standards for early hearing detection.

- In March 2026, researchers from the University of the Philippines Manila developed the country’s first locally manufactured AI-powered newborn hearing screening device called Hearing for Life (HeLe).

Companies Covered in Neonatal Hearing Screening Devices Market

- Natus Medical Incorporated

- MAICO Diagnostics GmbH

- Interacoustics A/S

- Vivosonic Inc.

- Path Medical GmbH

- Grason-Stadler (GSI)

- Welch Allyn

- GN Otometrics

- Otodynamics Ltd.

- Intelligent Hearing Systems (IHS)

- Starkey Hearing Technologies

- Siemens Healthineers

- MED-EL Medical Electronics

Frequently Asked Questions

The global neonatal hearing screening devices market is estimated to be valued at US$ 45.3 billion in 2026.

The primary demand drivers are the global rollout of legislated EHDI and UNHS programs, with the U.S. achieving over 98% newborn screening coverage under the CDC EHDI program, high global birth volumes of approximately 140 million annually per UNFPA estimates, and expanding NICU infrastructure investments across Asia-Pacific, driving institutional device procurement.

North America leads the global neonatal hearing screening devices market with approximately 38% of the total market share in 2025.

The integration of AI-powered automated result interpretation and teleaudiology connectivity into portable and handheld neonatal hearing screening platforms represents the most significant growth opportunity. This convergence enables community-level screening in LMICs where the WHO estimates the majority of the 34 million children with disabling hearing loss reside, unlocking substantial untapped demand beyond established hospital-based screening programs.

The key market players include Natus Medical Incorporated, MAICO Diagnostics GmbH, Interacoustics A/S, GN Otometrics, Grason-Stadler (GSI), Vivosonic Inc.