- Advanced Materials

- Green Concrete Market

Green Concrete Market Size, Share, and Growth Forecast, 2026 – 2033

Green Concrete Market by Product Type (Recycled Aggregate Concrete, Geopolymer Concrete, Others), Application (Residential, Commercial, Others), and Regional Analysis for 2026 – 2033

Green Concrete Market Size and Trends Analysis

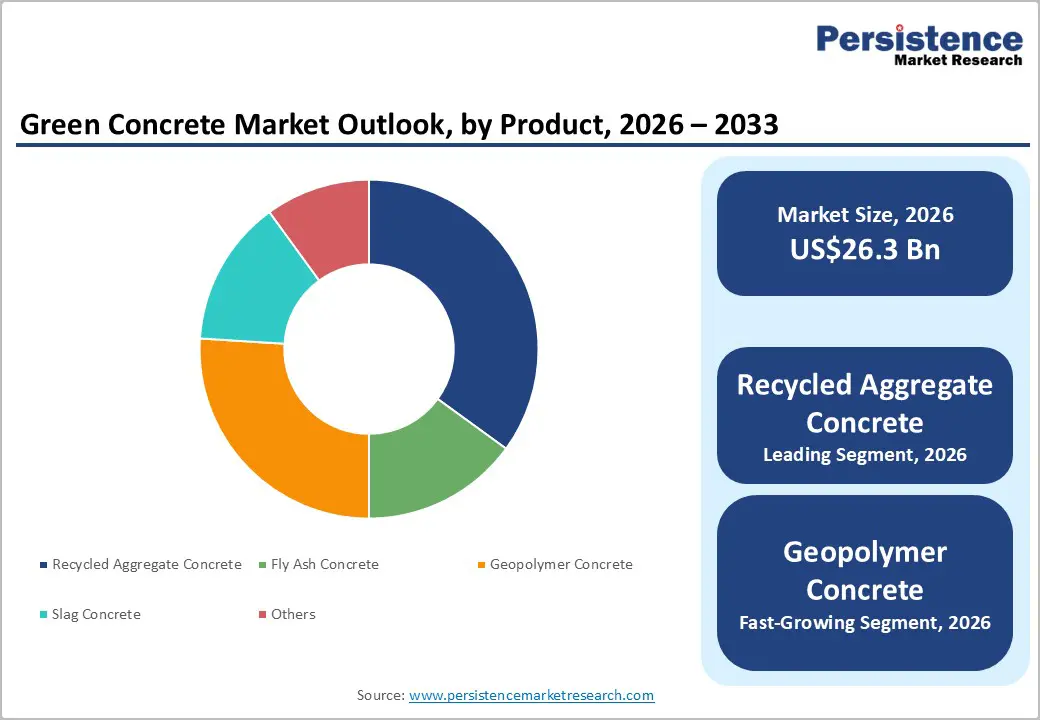

The global green concrete market size is likely to be valued at US$26.3 billion in 2026 and is expected to reach US$49.1 billion by 2033, growing at a CAGR of 9.3% during the forecast period from 2026 to 2033, driven by stricter environmental regulations, net-zero commitments by governments and corporations, and the rapid expansion of green building standards and certifications across residential, commercial, and infrastructure projects.

Green concrete, which incorporates recycled aggregates, industrial by-products such as fly ash and slag, geopolymer binders, and emerging carbon-capture technologies, offers a lower-environmental-impact alternative to conventional concrete without compromising structural performance. Large-scale urbanization and infrastructure development, particularly in emerging economies, are accelerating adoption as public authorities increasingly prioritize sustainable materials in procurement policies.

Key Industry Highlights:

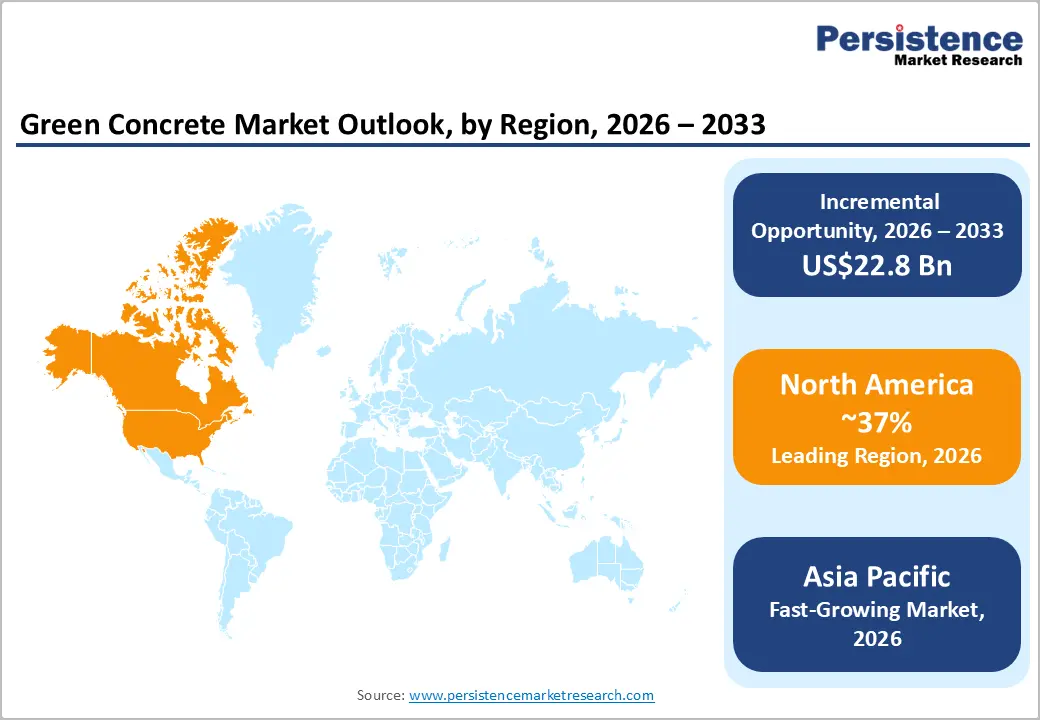

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 37% in 2026, driven by strong regulations, green building codes, infrastructure renewal, and advanced low-carbon technology adoption.

- Fastest-growing Region: Asia-Pacific is likely to be the fastest-growing region for green concrete in 2026, supported by rapid urbanization, robust infrastructure development, supportive sustainability policies, and the wide availability of industrial by-products.

- Leading Product Type: Recycled aggregate concrete is projected to represent the leading product type in 2026, accounting for 40% of the revenue share, driven by strong circular economy adoption and cost advantages.

- Leading Application: Infrastructure is expected to be the leading application type, accounting for over 45% of revenue in 2026, supported by large-scale public projects and emissions-reduction mandates.

| Global Market Attributes | Key Insights |

|---|---|

| Green Concrete Market Size (2026E) | US$26.3 Bn |

| Market Value Forecast (2033F) | US$49.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis-Stringent Environmental Regulations and Carbon Reduction Mandates

Governments across North America, Europe, and the Asia Pacific are implementing strict emission norms, carbon pricing mechanisms, and sustainability benchmarks for construction materials. Since traditional cement production is a major contributor to CO-emissions, regulatory bodies are actively promoting low-carbon alternatives. Green concrete aligns well with national climate goals, net-zero targets, and emission reduction roadmaps, making it increasingly preferred in both public and private construction projects.

These mandates are reinforced through green building codes, environmental impact assessments, and public procurement policies that prioritize sustainable materials. Infrastructure tenders are increasingly setting embodied carbon limits, prompting contractors to adopt green concrete formulations. Adhering to environmental regulations not only minimizes legal risks for builders but also increases the likelihood of projects qualifying for incentives and certifications. As regulatory enforcement intensifies, the adoption of green concrete is expected to accelerate, positioning it as a compliance-driven material choice rather than a voluntary sustainability option.

Rising Demand for Sustainable Construction and Infrastructure Development

Rapid urbanization, population growth, and infrastructure expansion, especially in emerging economies, are increasing demand for environmentally responsible building materials. Developers and governments are prioritizing sustainability to minimize environmental impacts across the lifecycle while maintaining structural performance. Green concrete offers a reduced carbon footprint, improved durability, and efficient resource utilization, making it well-suited for modern infrastructure such as highways, bridges, smart cities, and mass housing projects.

Rising awareness among stakeholders regarding climate change and resource depletion is influencing material selection decisions. Green certifications and ESG compliance are becoming essential benchmarks in residential, commercial, and institutional construction. Infrastructure projects funded by international agencies increasingly mandate the use of sustainable materials, thereby increasing demand. This growing preference for low-impact construction solutions supports sustained adoption of green concrete across both new developments and renovation projects worldwide.

Barrier Analysis - Limited Awareness and Standardization Issues

Limited awareness regarding green concrete technologies remains a key restraint. Many contractors, builders, and end users still lack a sufficient understanding of the performance, durability, and long-term benefits of green concrete. Conventional concrete continues to dominate due to familiarity, established practices, and perceived reliability. In developing regions, knowledge gaps and limited technical expertise hinder adoption, particularly among small and mid-scale construction firms. Limited exposure through pilot projects and demonstration infrastructure reduces confidence in large-scale deployment. The absence of targeted training programs slows acceptance across the construction value chain.

Standardization challenges restrict market penetration. Variability in raw materials such as fly ash, slag, and recycled aggregates leads to inconsistent performance, complicating standard formulation. Inadequate harmonized standards and codes across regions create uncertainty in approvals and design acceptance. This lack of uniform specifications impedes widespread implementation, particularly in structural applications, underscoring the need for clearer guidelines and industry education initiatives. Differences in regional regulatory frameworks complicate cross-border adoption. Limited inclusion of green concrete in mainstream building codes delays its acceptance in critical load-bearing and public infrastructure projects.

Production Scalability Challenges

Scaling up green concrete production presents operational and economic challenges. The availability of suitable industrial byproducts, such as fly ash and slag, varies significantly across regions, limiting consistent supply. Declining coal-based power generation in some countries is reducing fly ash availability, directly impacting production capacity. Recycled aggregate processing requires advanced sorting and quality control, increasing operational complexity and costs. Transportation of alternative raw materials from distant sources increases logistics costs and concerns about the carbon footprint. These supply-side constraints limit the ability of producers to scale output reliably across multiple project locations.

Production scalability is constrained by the need for specialized equipment, modified batching processes, and skilled labor. Smaller manufacturers often lack the capital to invest in upgrading facilities for green concrete production. These challenges make large-scale commercialization difficult, particularly in price-sensitive markets. Limited access to financing and uncertainty around demand volumes also discourage capacity expansion. Until supply chain integration improves and economies of scale are achieved, scalability issues will continue to restrain faster market expansion.

Opportunity Analysis - Technological Convergence with Carbon Capture and Circular Economy Practices

Innovations such as CO mineralization during concrete curing enable permanent carbon sequestration while improving material strength. This convergence transforms green concrete from a low-carbon alternative into a carbon-utilizing material, significantly enhancing its environmental value proposition. The integration of carbon capture technologies also supports compliance with emerging embodied-carbon regulations for large infrastructure and commercial projects. Lifecycle carbon accounting becomes more prominent, and carbon-sequestering concrete solutions gain preference among developers and public authorities seeking measurable emission reductions.

Circular economy practices strengthen this opportunity by promoting the reuse of industrial waste, demolition debris, and recycled aggregates. This reduces reliance on landfills and conserves natural resources. Governments and corporations are increasingly supporting circular construction models through incentives and sustainability frameworks. As technology adoption expands, green concrete producers can differentiate their offerings, improve environmental performance, and unlock new revenue streams in climate-focused construction markets.

Precast, 3D-Printed, and Modular Construction Applications

Emerging construction methods such as precast, 3D-printed, and modular construction create significant opportunities for green concrete adoption. These methods emphasize material efficiency, precision, reduced waste, and faster project timelines, attributes that align well with green concrete properties. Controlled manufacturing environments enable greater consistency in quality, addressing earlier concerns about material variability. Factory-based production allows optimized curing and mix control, enhancing strength and durability outcomes. This alignment makes green concrete particularly suitable for large-scale, repeatable construction components.

Green concrete formulations are increasingly optimized for prefabrication and additive manufacturing, enabling lightweight structures and complex designs with lower environmental impact. Governments and developers are investing heavily in modular housing and smart infrastructure to meet rapid urban demand. The use of green concrete in these applications supports reduced on-site emissions and labor dependency. As these construction techniques gain traction, green concrete is well-positioned to become a preferred material, supporting scalable, sustainable, and future-ready construction solutions.

Category-wise Analysis

Product Type Insights

Recycled aggregate concrete is expected to lead, accounting for approximately 40% of revenue in 2026, driven by the increasing reuse of construction and demolition waste, which significantly reduces dependence on virgin aggregates and aligns strongly with circular economy principles. This segment benefits from cost efficiencies, particularly in urban and demolition-intensive regions where recycled materials are readily available. For example, its widespread use in road sub-bases and pavements in European urban renewal projects, where sustainability criteria prioritize recycled materials.

Geopolymer concrete is likely to represent the fastest-growing segment in 2026, supported by its low-clinker or clinker-free composition. This material offers significantly lower embodied carbon and superior resistance to heat, chemicals, and sulfate exposure, making it ideal for harsh environments. Strong research and development investments by cement manufacturers and material science firms are accelerating commercialization and performance optimization. Geopolymer concrete is gaining momentum in applications such as industrial flooring, marine structures, and waste containment facilities, where durability is essential. For instance, its growing use in industrial and infrastructure projects in Australia highlights its role in replacing traditional Portland cement in precast components.

Application Insights

Infrastructure is projected to lead the market, accounting for approximately 45% of revenue in 2026. Large-scale public works such as highways, bridges, tunnels, rail corridors, and dams prioritize durability, long service life, and reduced life-cycle emissions, key advantages of green concrete. Green concrete’s resistance to weathering, sulfate attack, and heavy loading makes it well-suited for long-term use in infrastructure. For example, its application in low-carbon highway and metro rail projects in North America, where public procurement guidelines encourage the use of recycled aggregates and supplementary cementitious materials.

Residential construction is expected to be the fastest-growing sector in 2026, fueled by increasing demand for green housing, energy-efficient buildings, and materials that minimize embodied carbon throughout the building lifecycle. Developers are progressively adopting green concrete to achieve sustainability certifications and meet consumer expectations for eco-friendly homes. Lightweight formulations and enhanced thermal performance make it ideal for both low-rise and high-density residential projects. A notable example is the use of fly ash and recycled aggregate concrete in large-scale affordable housing developments in India, where sustainability and cost-efficiency are key priorities.

Regional Insights

North America Green Concrete Market Trends

North America is expected to lead the market, capturing 37% of the share in 2026, driven by robust environmental policies and sustainability frameworks that influence both public and private construction practices. Regulatory pressure from federal and state agencies in the U.S., along with Canada’s carbon pricing and green building incentives, is accelerating the adoption of low-carbon and recycled concrete solutions in major infrastructure projects, including highways, transit systems, and public buildings.

For instance, CarbonCure Technologies Inc., a Canadian innovator, has deployed its CO-mineralization technology across hundreds of concrete plants in the U.S., including large commercial and industrial projects. This technology permanently embeds captured carbon in the concrete mix, thereby reducing embodied emissions in construction materials.

The North America market is shaped by ongoing innovation and growing commercial investment in sustainable construction technologies. Companies are developing new binders, supplementary cementitious materials, and carbon capture solutions that enhance performance while reducing environmental impact, making green concrete increasingly competitive with traditional mixes. The construction landscape is evolving as contractors and developers adopt digital quality tracking, prefabrication, and circular material sourcing practices to optimize both cost efficiency and sustainability outcomes.

Europe Green Concrete Market Trends

Europe is likely to be a significant market for green concrete in 2026, due to countries implementing ambitious climate objectives tied to the European Green Deal, Fit for 55, and Renovation Wave initiatives, which demand significant reductions in embodied carbon from construction materials. These stringent regulatory frameworks are encouraging widespread adoption of low-carbon concrete solutions in infrastructure, commercial, and residential projects. A key trend is the integration of supplementary cementitious materials such as fly ash, slag, and calcined clay into traditional mixes, lowering clinker content and enhancing sustainability without compromising performance.

Innovation and corporate commitment to sustainability are defining trends in Europe’s market, as manufacturers and material suppliers expand offerings, invest in technology, and align with local climate goals. For example, Ecocem, an Irish multinational that produces low-carbon cement by significantly reducing clinker content and incorporating industrial by-products, prevents millions of tonnes of CO-emissions through its products across France, the U.K., and Benelux markets. Ecocem’s focus on supplementary cementitious technology demonstrates the region’s push toward greener binders and strengthens adoption among builders prioritizing lower emissions.

Asia Pacific Green Concrete Market Trends

The Asia-Pacific region is likely to be the fastest-growing market in 2026, driven by unprecedented levels of urbanization, infrastructure investment, and government mandates for low-carbon construction. The region accounted for a significant share of the market, supported by policy frameworks in countries such as China, India, Japan, and Australia that emphasize reduced emissions, enhanced energy efficiency, and sustainability certification standards in building codes and public infrastructure tenders.

Rapid development of highways, metro systems, smart city projects, and affordable housing is creating high demand for sustainable concrete mixes that incorporate industrial byproducts such as fly ash, slag, and calcined clay, aligning with circular economy principles.

Innovation and corporate growth are driving the market in the Asia Pacific, with leading companies expanding their sustainable product offerings and bolstering production capabilities. A prime example is UltraTech Cement Ltd., which has set ambitious climate goals by incorporating low-clinker products, renewable energy solutions, and increased use of industrial by-products such as fly ash and ground granulated blast-furnace slag (GGBS) in its concrete formulations. The company has earned GreenPro certifications for many of its products, further highlighting its commitment to sustainability.

Competitive Landscape

The global green concrete market exhibits a moderately fragmented structure, driven by a mix of large multinational cement and materials companies and innovative niche players competing to meet rising demand for sustainable construction solutions amid tightening environmental regulations and low-carbon targets. These established firms leverage decades of industry expertise, optimized supply chains, and regional market presence to sustain leadership and respond to government emission mandates and increasing green building standards worldwide.

With key leaders including CarbonCure Technologies Inc., Solidia Technologies Inc., and Sika AG driving innovation in carbon utilization, admixtures, and performance-enhancing green formulations, competition is intensifying across advanced technology and service differentiation. These players compete through technological innovation, strategic partnerships, mergers and acquisitions, and geographic expansion, aiming to enhance product efficacy, reduce embodied carbon, and capture emerging demand in infrastructure, residential, and commercial sectors.

Key Industry Developments:

- In December 2025, India and Sweden launched seven green-industry projects under the India–Sweden Industry Transition Partnership (ITP) to decarbonize the cement and steel sectors, focusing on low-carbon cement innovation. The initiative connected Indian cement producers, research institutions, and Swedish clean-tech developers, with key projects including a carbon capture feasibility study led by Ambuja Cements Ltd, EcoTech Solutions, and IIT Bombay.

- In October 2025, RMI and the Center for Green Market Activation launched the Sustainable Concrete Buyers Alliance (SCoBA) to accelerate low-carbon cement adoption. The alliance, including major buyers such as Amazon, Prologis, and Meta, collectively procured low-carbon concrete environmental attribute certificates, driving investment in advanced production and decarbonization technologies. SCoBA introduced a unique book-and-claim system, allowing companies to financially support sustainable concrete production regardless of material delivery.

- In September 2025, Holcim AG and CRH PLC invested US$75 million in U.S.-based green cement startup Sublime Systems. The investment, including long-term offtake agreements, supported Sublime's electrochemical cement manufacturing process, which eliminates the need for heating limestone and reduces CO- emissions from conventional cement production.

Companies Covered in Green Concrete Market

- HOLCIM

- CEMEX

- HeidelbergCement AG

- CRH

- UltraTech Cement Ltd

- Sika AG

- Buzzi S.p.A.

- Vicat SA

- TAIHEIYO CEMENT CORPORATION

- Ecocem

- BASF SE

- Cement Australia Holdings Pty Limited

- Tarmac

- St. Mary's Cement Inc.

- CarbonCure Technologies Inc.

- SOLIDIA TECHNOLOGIES

- Giatec Scientific Inc.

- Aggregate Industries

Frequently Asked Questions

The global green concrete market is projected to reach US$26.3 billion in 2026.

The green concrete market is driven by stringent carbon-reduction regulations, rising demand for sustainable construction materials, and growing adoption of low-carbon technologies in infrastructure development.

The green concrete market is expected to grow at a CAGR of 9.3% from 2026 to 2033.

Key market opportunities in the green concrete market include carbon capture–enabled cement technologies, circular use of industrial by-products, and growing adoption in infrastructure, modular, and green building projects.

Holcim, CEMEX, HeidelbergCement AG, CRH, UltraTech Cement Ltd., and Sika AG are the leading players.