- Hardware & Software IT Services

- Green Data Center Market

Green Data Center Market Size, Share, and Growth Forecast, 2025 – 2032

Green Data Center Market By Component (Hardware, Software, Services), Data Center Size (Small & Medium Data Center, Large Data Center), End-user (Cloud Providers, Colocation Providers, Enterprises), and Regional Analysis for 2025 – 2032

Green Data Center Market Size and Trends

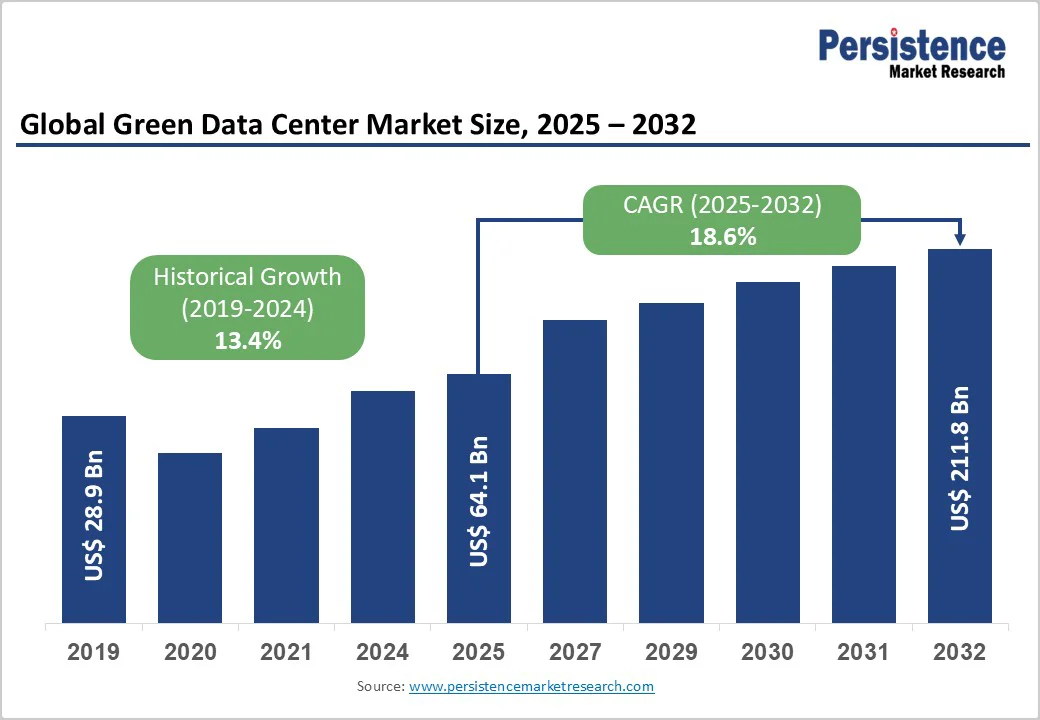

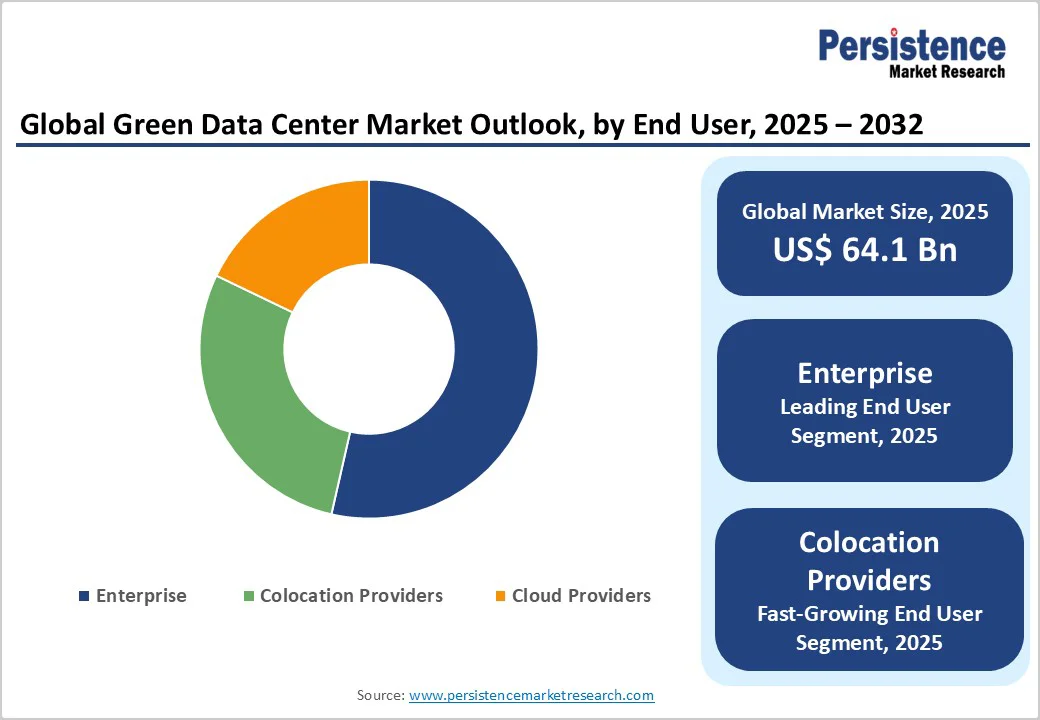

The global green data center market size is likely to be valued at US$64.1 Billion in 2025 and is expected to reach US$211.8 Billion by 2032 growing at a CAGR of 18.6% during the forecast period from 2025 to 2032, driven by exponential growth in artificial intelligence workloads, cloud computing adoption, and corporate commitments to carbon neutrality, positioning green data centers as the sustainable backbone of digital infrastructure in an era where data centers are projected to consume up to 8-12% of total electricity demand by 2030. Enterprises and hyperscale operators are increasingly prioritizing operational efficiency, reliability, and long-term cost savings.

Key Industry Highlights:

- Leading Component: Hardware accounts for over 58% share in 2025, driven by energy-efficient servers, storage, and networking equipment. Services are growing the fastest due to rising demand for consulting, monitoring, and managed solutions for green operations.

- Leading Data Center Size: Large data centers hold more than 72% share in 2025, due to scale advantages for renewable energy, energy-efficient cooling, and smart power management. Small and medium facilities are growing rapidly, driven by demand for edge computing, low-latency solutions, and modular green designs.

- Leading End-user: Enterprises capture over 45% share in 2025, prioritizing energy-efficient, scalable infrastructure to manage AI and cloud workloads. The BFSI sector holds more than 27% share, driven by regulatory compliance requirements such as Europe’s DORA. Colocation providers grow rapidly through interconnection ecosystems and sustainability certifications.

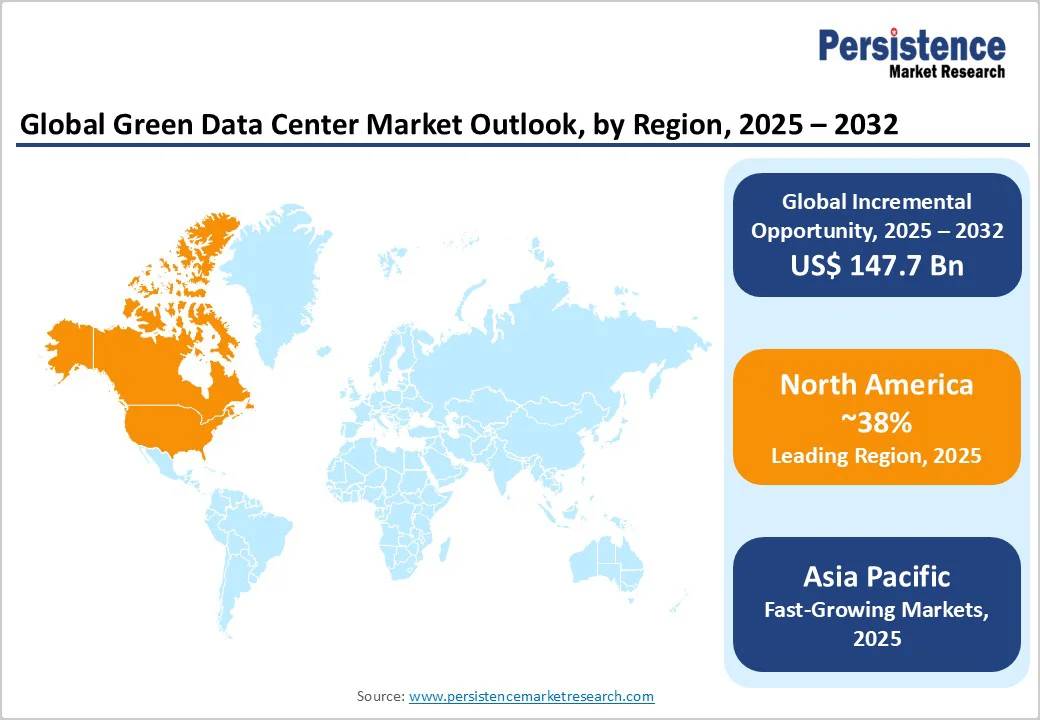

- Leading Region: North America is projected to capture nearly a 38% share in 2025, driven by corporate sustainability goals, regulatory mandates, and hyperscale and edge computing growth. Asia Pacific is the fastest-growing region, fueled by AI adoption, renewable energy procurement, and digital transformation across sectors. Europe grows steadily, supported by EU Green Deal mandates, high renewable electricity penetration, and cold climates enabling free-air cooling.

| Key Insights | Details |

|---|---|

| Green Data Center Market Size (2025E) | US$64.1 Bn |

| Market Value Forecast (2032F) | US$211.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 18.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 13.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Energy Consumption and Cost Pressures Driving Efficiency Imperatives

Global data center electricity consumption reached approximately 415 terawatt-hours (TWh) in 2024, representing 1.5% of global electricity demand, and is projected to more than double to 945-1,100 TWh by 2026-2030. This unprecedented surge, catalyzed by artificial intelligence and high-performance computing workloads, has intensified operational cost pressures. According to IEA, China and the U.S. will drive nearly 80% of global data center electricity growth by 2030, with the U.S. consumption rising ~240?TWh (+130%), China ~175?TWh (+170%), Europe >45?TWh (+70%), and Japan ~15?TWh (+80%) compared to 2024 levels.

AI workloads consume approximately 10 times more energy than traditional computing tasks. Energy expenses constitute 40-50% of total data center operational costs, compelling operators to adopt green technologies that deliver measurable efficiency improvements. Data centers achieving power usage effectiveness (PUE) ratios of 1.3 or lower through advanced cooling systems, renewable energy procurement, and AI-powered optimization realize 20-40% reductions in energy consumption, translating directly into competitive cost advantages and enhanced profitability over traditional infrastructure.

AI and Machine Learning Workload Proliferation Necessitating Advanced Cooling Infrastructure

Artificial intelligence applications have catalyzed fundamental shifts in data center architecture requirements. GPU-rich server configurations supporting AI model training and inference operations generate rack densities ranging from 30 - 100+ kW, compared to 7-10 kW for traditional enterprise servers. Europe's data center electricity consumption is projected to grow from 62 TWh in 2024 to over 150 TWh by 2030, largely due to the rise in AI workloads, compelling rapid adoption of liquid cooling technologies that remove heat 15-25 times faster than conventional air systems.

Schneider Electric's December 2024 launch of liquid-cooled AI cluster designs and Microsoft's £2.5 Billion (US$3.28 Billion) AI-focused campus in Leeds exemplify how sustainable innovations enable scalability and efficiency for AI-ready facilities. Liquid cooling deployments are expanding rapidly, with more than one-third of enterprise data centers expected to employ these solutions by 2026, representing a near-doubling from early 2024 adoption levels.

Barrier Analysis - Power Grid Constraints and Interconnection Delays Limiting Development Velocity

Rapidly expanding data center power requirements are straining existing electrical grid infrastructure across major markets. Northern Virginia, the world's largest data center market with 3,046 MW inventory, faces ongoing power supply challenges despite Dominion Energy's transmission upgrade initiatives expected to enhance capacity by 2026. Phoenix and Atlanta markets have experienced power availability constraints from utility providers, placing unprecedented pressure on grid operators. Interconnection queue delays average three to five years in many jurisdictions, with over 1,200 GW of generation and storage projects awaiting connection approvals in the U.S. alone. These bottlenecks slow development timelines, increase project risks, and create competitive disadvantages for regions unable to deliver reliable power access at scale.

Opportunity Analysis - Carbon Credit Markets and Green Financing Mechanisms Enhancing Project Economics

Financial innovation is enhancing the viability of green data center projects through mechanisms such as green bonds, REIT-style financing, and carbon monetization. Digital Realty’s US$7.2 Billion in green bond issuances underscores the sector’s growing access to sustainable capital, while REIT models in Asia-Pacific markets are cutting WACC by 50–100 basis points. Carbon credit programs and verified renewable energy certificates allow operators to monetize emissions reductions. Proposed inclusion of data centers in the EU ETS may add compliance requirements but also unlock liquid secondary markets, reshaping financial models for sustainable infrastructure.

Edge Computing Proliferation Creating Distributed Green Infrastructure Demand

The acceleration of 5G, IoT, and edge computing is fueling demand for distributed, low-latency micro data centers, creating strong opportunities for modular and green solutions. With over 4.1 million 5G base stations deployed in China by 2024, enterprises and telecoms are increasingly adopting 1–5 MW facilities integrating renewable energy, free-air cooling, and AI-driven energy optimization. The shift toward sustainable, pre-fabricated, and scalable designs enables efficient deployment in secondary markets, aligning high-performance needs with environmental goals.

Technological Innovation in Renewable Energy Integration and Alternative Power Sources

Data center operators are exploring next-generation energy solutions such as Small Modular Reactors (SMRs), which promise cost-effective, low-carbon baseload power beyond traditional renewables, though widespread adoption is still in early stages due to regulatory and public acceptance challenges. Companies such as AWS and Google have signed PPAs with SMR developers, and European operators such as Data4 are evaluating potential deployment. Liquid cooling and waste heat recovery technologies are being piloted to offset 30–40% of facility heating and enable district heating integration in Germany, Denmark, and the Netherlands. Supported by government incentives, these circular energy models offer promising future opportunities for monetization and carbon-neutral operations.

Category-wise Analysis

Component Insights

Hardware is expected to account for more than 58% share in 2025, due to the critical need for energy-efficient servers, storage systems, and networking equipment that reduce power consumption and operational costs. As data processing demands grow, driven by AI, cloud services, and edge computing, organizations prioritize high-performance, low-power hardware to meet sustainability goals. Hardware procurement cycles averaging 3-5 years ensure sustained segment revenue, particularly as hyperscale operators deploy thousands of racks annually across global expansion projects requiring standardized, pre-validated configurations that minimize deployment timelines and operational risks.

Services are expected to grow at the highest rate as organizations increasingly need expertise to design, operate, and optimize energy-efficient infrastructure. The rising complexity of integrating renewable energy, advanced cooling, and AI-driven management systems drives demand for consulting, monitoring, and managed services. Companies are outsourcing sustainability compliance, energy audits, and retrofitting to reduce costs and meet ESG goals. Dell Technologies’ November 2024 launch of Implementation Services for Sustainable Data Centers exemplifies this trend, providing design, planning, and deployment support for low-carbon operations.

Data Center Size Insights

Large data centers are expected to account for over 72% share in 2025, as they host massive computing workloads that drive significant energy consumption, creating a critical need for efficient, low-carbon solutions. Their scale enables the adoption of advanced renewable energy systems, energy-efficient cooling, and smart power management technologies. Regulatory pressures and corporate sustainability goals push these facilities to prioritize green practices. The economic benefits of operational cost reduction further reinforce their focus on sustainable infrastructure.

Small and medium data centers are growing fastest due to organizations' demand for localized, energy-efficient infrastructure for digital transformation and low-latency applications. These facilities, typically 1–50?MW, offer scalable, cost-effective green solutions with faster adoption of renewable energy, advanced cooling, and modular designs, reducing carbon footprints. They support latency-sensitive applications such as autonomous vehicles and industrial IoT, while providing redundancy for mission-critical workloads across regions. Modular, pre-fabricated designs enable turnkey deployment in four to six months, democratizing access to technologies once limited to hyperscale operators.

End-user Insights

Enterprises are expected to account for more than 45% of the market share in 2025, due to their high energy consumption. They require scalable, energy-efficient infrastructure to manage increasing workloads. Enterprises prioritize operational cost reduction and long-term energy savings, making green data centers a strategic necessity. The BFSI sector is particularly active, holding a 27% share in 2025, driven by Europe’s Digital Operational Resilience Act (DORA), which mandates robust IT risk management, third-party vendor controls, and operational continuity standards, necessitating redundant and geographically distributed data center presence.

Colocation providers are expected to grow rapidly as enterprises outsource data center operations to specialized operators delivering economies of scale, interconnection ecosystems, and sustainability certifications difficult for individual organizations to replicate cost-effectively. Equinix's achievement of 96% renewable energy coverage across its global facilities and an average PUE of 1.39 demonstrates competitive differentiation through sustainability leadership. Direct interconnection to 15–20+ cloud service providers within colocation facilities reduces data transfer costs and latency while enabling hybrid multi-cloud architectures. This creates network effects that concentrate tenant demand in established colocation hubs, despite premium pricing relative to wholesale data center alternatives.

Regional Insights

North America Green Data Center Market Trends

North America is set to capture over 38% of the green data center market, driven by enterprises’ sustainability goals, stricter emissions regulations, and rising stakeholder demand for energy-efficient IT infrastructure. Hyperscale and edge computing growth, modular design innovations, and advanced power management are enabling scalable, cost-effective adoption. Federal and state policies, including the EPA’s 2024 baseline targeting a 28–40% emissions reduction by 2030, California’s Title 24 energy code, and tax incentives, have catalyzed over US$70 Billion in M&A, exemplified by Blackstone’s A$24 Billion (US$15.6 Billion) AirTrunk deal.

Data centers’ electricity demand is projected to reach 9% of U.S. usage by 2030, with peak loads hitting 759,180 MW in July 2025, while pilots in Small Modular Reactors represent a zero-carbon innovation frontier. Investment volumes dipped below US$1 Billion in H1 2025 due to supply and economic challenges, but rebounded in H2 with US$7 Billion in CoreWeave-backed AI build-to-suit projects.

Asia Pacific Green Data Center Market Trends

Asia Pacific constitutes the fastest-growing market, driven by hyperscale expansions, government net-zero mandates, and digital transformation across sectors such as BFSI, e-commerce, manufacturing, and telecom. AI-driven high-density workloads, with rack densities rising from 10 kW to over 100 kW, are accelerating adoption of liquid cooling solutions, including direct-to-chip and immersion cooling by operators such as SK Telecom, Equinix, and Alibaba.

Google’s US$2 Billion Selangor data center, expected to generate US$3.2 Billion and 26,500 jobs by 2030, will use water-cooling technology to reduce energy use and emissions. Policy support, including China’s energy efficiency mandates, ASEAN data sovereignty rules, and corporate renewable energy agreements, is driving adoption, with STT Global Data Centers sourcing 62.5% of electricity from renewables in 2023, exceeding its 60% 2026 target. India’s digitalization, with over 886 million users in 2024 set to surpass 900 million by 2025, further fuels demand for sustainable, scalable storage.

Europe Green Data Center Market Trends

Europe’s green data center demand is driven by stringent EU mandates such as the Green Deal, Energy Efficiency Directive, NIS2, and DORA, requiring energy, carbon, cybersecurity, and IT risk compliance. Nordic countries (Sweden, Norway & Denmark) attract investment due to 80–95% renewable grid electricity, cold climates enabling free-air cooling for 8–10 months, and district heating integration for waste heat revenue. FLAPD markets (Frankfurt, London, Amsterdam, Paris & Dublin) expand as cloud interconnection hubs, though land scarcity and water restrictions constrain growth.

The proposed EU Cloud and AI Development Act aims to triple data center capacity in five to seven years via private investments and streamlined permitting for sustainable, resource-efficient facilities. Frankfurt remains Europe’s top connectivity hub, balancing high network density with regulatory constraints.

Competitive Landscape

The global green data center market demonstrates moderate concentration, with leading players holding approximately 30–40% of the combined market share in 2025, while mid-tier regional operators and enterprise-focused specialists account for the remainder. Market fragmentation is rising as specialized green technology providers, modular data center manufacturers, and alternative energy integrators enter segments previously dominated by traditional infrastructure vendors. Manufacturers adopt strategic partnerships with renewable energy providers and software vendors to deliver integrated, energy-efficient solutions and differentiated service offerings.

Key Industry Developments

- In October 2025, AdaniConneX and Google partnered to develop India’s largest AI data center campus in Visakhapatnam, with a US$15?Billion investment over 2026?2030, supported by clean energy, subsea cables, and robust infrastructure to drive advanced AI workloads. The project includes co-investment in transmission lines, renewable energy, and energy storage, enhancing both data center operations and India’s grid resilience.

- In August 2025, the Asian Development Bank (ADB) and GSA Data Center 01 Company Limited signed a deal for a THB900 million (~US$26.8 Million) local currency green loan to develop a 25.6 MW colocation green data center in Samut Prakan, Thailand. The facility will feature Tier III reliability, a PUE of 1.4, and is expected to achieve LEED Gold certification.

- In March 2025, Nippon Yusen, NTT FACILITIES, Eurus Energy, MUFG Bank, and Yokohama City signed an MoU to demo an offshore green data center on a 25m × 80m mini-float at Osanbashi Pier. The floating facility will run on 100% renewable energy from solar and battery storage, with results guiding future waterfront developments.

Companies Covered in Green Data Center Market

- Eaton Corporation

- Equinix, Inc.

- Schneider Electric

- Vertiv Group Corp.

- Daikin

- ABB

- Cisco Systems, Inc.

- Microsoft

- Huawei Technologies Co., Ltd.

- IBM

- Delta Electronics, Inc.

- Stulz GmbH

Frequently Asked Questions

The green data center is projected to be valued at US$64.1 Billion in 2025.

The need for energy-efficient, sustainable infrastructure that reduces operational costs and carbon footprints while supporting growing digital workloads is a key driver of the market.

The green data center market is poised to witness a CAGR of 18.6% from 2025 to 2032.

Technological innovation in renewable energy integration and alternative power sources is creating strong growth opportunities.

Eaton Corporation, Equinix, Inc., Schneider Electric , Vertiv Group Corp., Daikin, and ABB are among the leading key players.