- Specialty & Fine Chemicals

- Phospholipids Market

Phospholipids Market Size, Share, and Growth Forecast, 2026 - 2033

Phospholipids Market by Product Type (Phosphatidylcholine, Phosphatidylserine, and Others), by Source (Soy, Sunflowers, Eggs, and Others), by End Use (Nutraceutical Supplements, Food and Beverages, Pharmaceuticals, and Others), and Regional Analysis for 2026 - 2033

Phospholipids Market Size and Trends Analysis

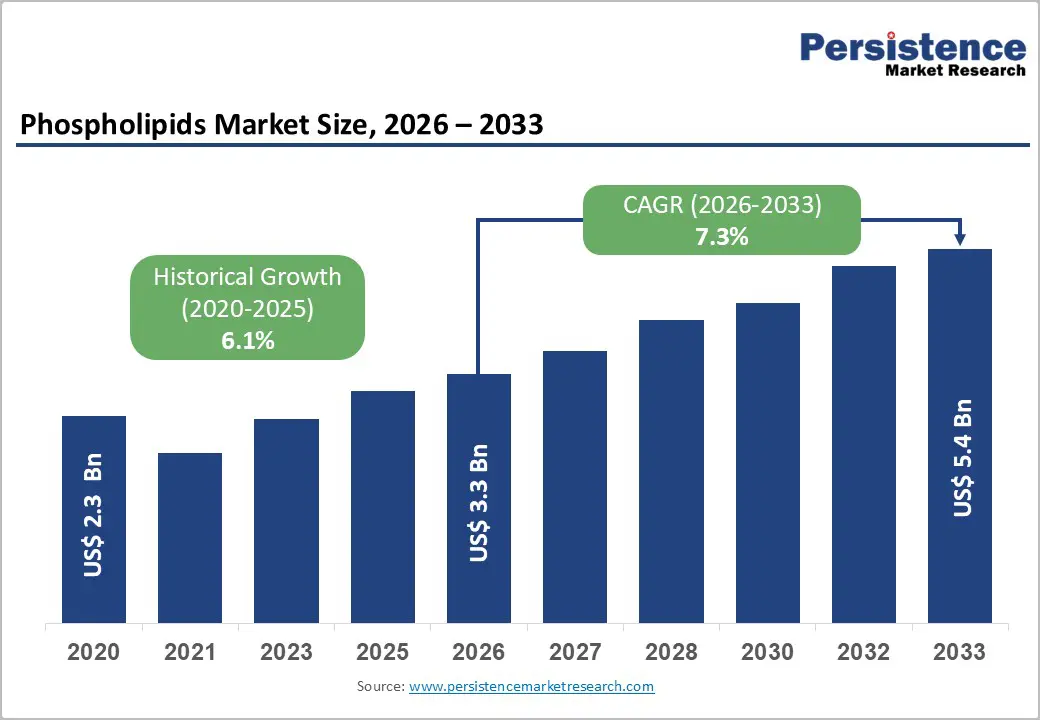

The global phospholipids market size is likely to be valued at US$ 3.3 billion in 2026 and is projected to reach US$ 5.4 billion by 2033, growing at a CAGR of 7.3% during the forecast period.

Key Industry Highlights:

- Highest-Margin Segment Pharmaceutical Grade: Pharmaceutical-grade phospholipids (PC, PS at USP/Ph.Eur. purity) command the market's highest unit economics; LNP drug delivery pipeline growth positions this sub-segment to outpace overall market CAGR through 2033.

- Growth Segment Concentration PS and Sunflower: Phosphatidylserine (8.2% CAGR) and sunflower-derived phospholipids (8.4% CAGR) are growing above market average; operators with PS fractionation and non-GMO sunflower sourcing capabilities capture disproportionate margin expansion.

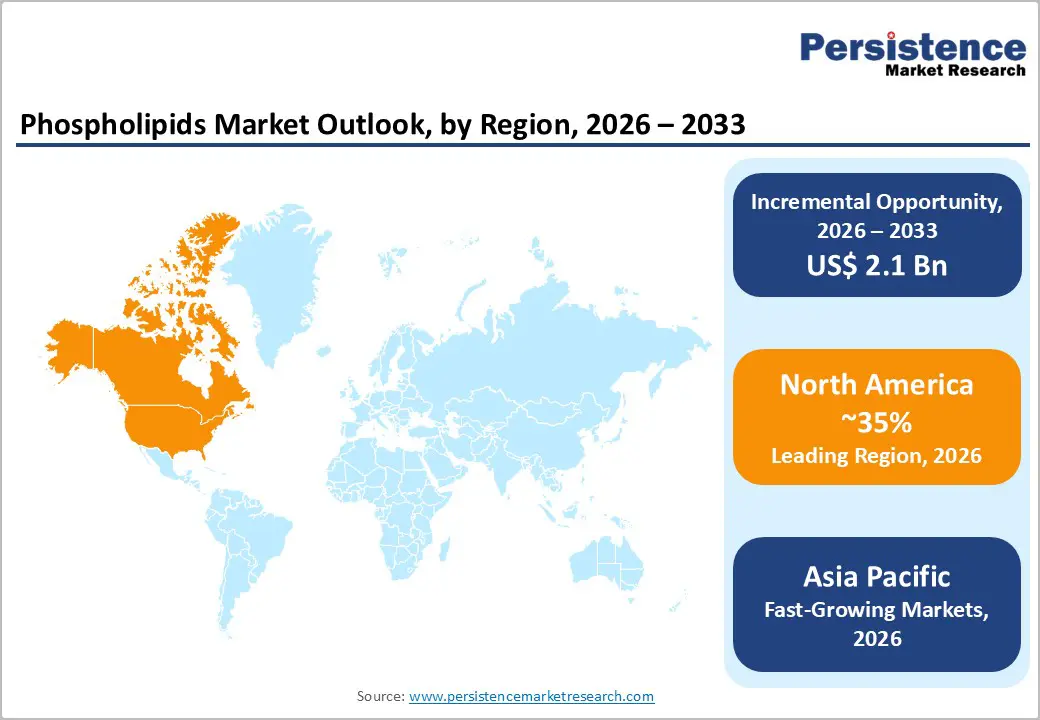

- Regional Capital Allocation Priority Asia Pacific: Asia Pacific's 8.3% CAGR is the fastest-growing region and combined with manufacturing cost competitiveness and import-substitution dynamics in China and India, constitutes the highest-priority geographic capital deployment thesis.

- North America Anchors Premium Revenue: North America's 35%+ revenue share in 2026 (approximately US$ 1.15 Bn+) is structurally defended by FDA regulatory infrastructure, pharmaceutical R&D demand, and established supplement industry procurement channels.

- Structural Risk Feedstock Concentration: Soy-derived phospholipids represent 55%+ of 2026 supply; soybean commodity price volatility creates EBITDA margin exposure of 300-600 bps for non-hedged operators a material risk factor in M&A due diligence and capital allocation modeling.

- M&A and Consolidation Signal: Post-2023 activity Avril Group asset acquisition, Cargill capacity expansion, Aker BioMarine distribution partnership signals an active strategic M&A environment oriented toward vertical integration, non-GMO supply control, and pharmaceutical-grade positioning.

| Key Insights | Details |

|---|---|

| Phospholipids Market Size (2026E) | US$ 3.3 Bn |

| Market Value Forecast (2033F) | US$ 5.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Dynamics

Drivers - Population ageing increases demand for cognitive and metabolic support

WHO indicates global population ageing is accelerating, including a projection that by 2030, 1 in 6 people will be aged 60 years or over. In commercial terms, this supports higher baseline demand for nutraceutical and medical-nutrition formats where phospholipids (e.g., phosphatidylserine and phosphatidylcholine) are used as functional lipids or formulation aids. As the addressable consumer base expands, product managers increasingly prioritize ingredients with clear biochemical relevance (cell membranes, lipid transport) and acceptable safety status for repeated use. The business implication is a more resilient demand floor for standardized phospholipid inputs and a higher willingness to pay for traceability, allergen management, and consistent specifications.

Regulatory clarity enables wider, compliant phospholipid usage

In the U.S., lecithin defined in regulation as a naturally occurring mixture of phosphatides is listed under 21 CFR § 184.1400 and can be used in food with no limitation other than current good manufacturing practice. FDA’s “Substances Added to Food” database also lists lecithin with multiple technical effects (including emulsifier and nutrient supplement) and references relevant CFR sections. In the EU, EFSA has evaluated health claims related to phosphatidylserine under Regulation (EC) No 1924/2006, illustrating that market access depends on evidence thresholds and compliant wording. Strategically, regulatory clarity de-risks formulation investment, encourages long-term supply contracts, and raises the value of documentation-ready supply (CoA discipline, contaminant controls, and clear source declarations).

Restraint - Health-claim substantiation increases time-to-market and compliance costs

EFSA’s health-claim evaluation approach emphasizes that substantiation depends on characterisation of the food/constituent, the claimed effect being beneficial, and evidence establishing a cause-and-effect relationship. EFSA has also published scientific opinions specifically assessing phosphatidylserine-related claims under EU health-claim regulations, reinforcing that not all proposed claims meet evidentiary standards. From a business perspective, this creates cost and timeline risk for premium positioning strategies that rely on consumer-facing cognition or performance claims, especially when portfolios are launched across multiple jurisdictions. Publicly available data indicates that companies mitigate this through conservative claims, third-party testing, and documentation-led go-to-market planning.

Opportunity - Non-GMO Sunflower Phospholipid Premium Market Capture

The sunflower-derived phospholipid segment is growing at an 8.4% CAGR the highest source-level growth rate in the market driven by the structural demand shift toward non-GMO, allergen-free ingredient specifications. The addressable revenue pool is partially quantifiable: sunflower lecithin occupies an estimated sub-10% share of 2026 revenues within the US$ 3.3 Billion market, representing a competitive white space of well over US$ 300 Million at current pricing. The monetization pathway is direct: manufacturers capable of securing identity-preserved, non-GMO-certified sunflower supply chains and achieving third-party verification (Non-GMO Project, EU Organic) can access premium retail and ingredient channels with meaningfully higher per-kilogram realizations. Capital deployment in European sunflower processing infrastructure presents the most proximate investment opportunity.

Asia Pacific Market Entry via Nutraceutical Channel Development

Asia Pacific is the fastest growing regional market at an 8.3% CAGR, generating an incremental revenue opportunity within the 2026-2033 forecast window that is disproportionate relative to the region's 2026 base. China, Japan, India, and ASEAN economies each present structurally distinct entry vectors: China's volume scale in liver health and cognitive supplements, Japan's FOSHU-regulated functional food framework providing validated commercial infrastructure, and India's expanding middle-class supplement adoption intersecting with FSSAI regulatory modernization. The white space is concentrated in locally manufactured, regulatory-compliant phospholipid supply capable of displacing import dependency. Greenfield investment or joint venture structures with regional distributors represent viable capital deployment pathways, with production cost arbitrage available relative to European origination costs.

Pharmaceutical-Grade Phospholipid Supply for LNP Drug Pipelines

The pharmaceutical segment, while not the dominant end-use by revenue share, represents the market's highest-value monetization opportunity. The structural driver is the expansion of clinical pipelines utilizing lipid nanoparticle excipient systems across oncology, gene editing, and RNA therapeutics. Based on publicly available clinical trial registries, the number of LNP-dependent therapeutic candidates in active development is material. The addressable premium revenue pool for USP/Ph.Eur.-compliant phospholipid supply is estimated to represent a multi-hundred-million-dollar sub-market growing above overall market CAGR. The competitive white space is narrow but high-barrier: operators capable of demonstrating GMP compliance, validated analytical methods, and batch-to-batch consistency for sub-ppm purity specifications face limited competition and can secure long-duration, contractually anchored supply agreements at premium unit economics.

Category-wise Analysis

Product Type Insights

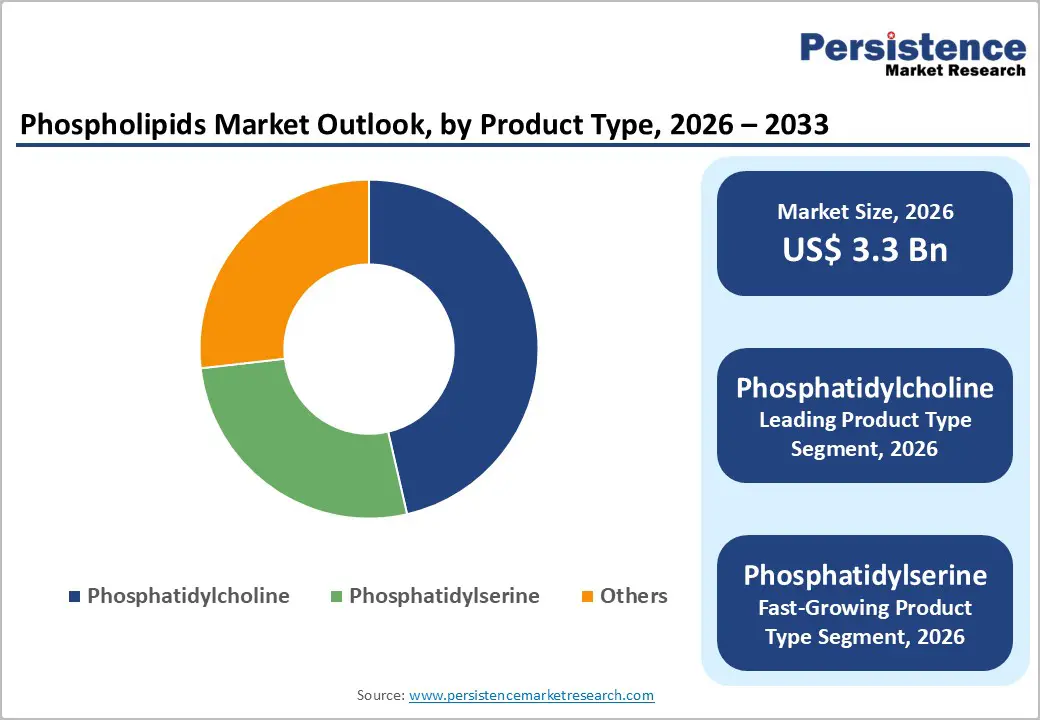

Phosphatidylcholine (PC) commands above 45% of 2026 revenues, anchored by its dual-market application across pharmaceutical excipient systems and mainstream nutraceutical formulations. PC's revenue dominance reflects both volume scale, driven by its widespread use in food-grade emulsification, liposomal drug delivery, and liver health supplements and unit pricing stability. PC's established regulatory acceptance under GRAS (U.S.) and E322 (EU) frameworks eliminates approval risk, reducing the cost-of-commercialization for downstream manufacturers. Its position as the primary structural phospholipid in LNP drug delivery systems further insulates PC demand from discretionary spending cycles.

Phosphatidylserine (PS) is the market's fastest-growing product type at an 8.2% CAGR, driven by its differentiated clinical profile and expanding application in premium cognitive health and sports recovery supplement formulations. PS's growth trajectory is causally linked to consumer willingness to pay for clinically validated brain-health ingredients and the FDA-issued qualified health claim for PS and cognitive function. The demand economics are favorable: PS commands a material unit price premium over PC, and its slower shift away from bovine-derived to plant-derived sourcing has not materially constrained supply. Net margin per kilogram for PS producers exceeds that of PC-focused operators, making PS segment share a meaningful determinant of overall company profitability.

Source Insights

Soy-derived phospholipids hold above 55% revenue share in 2026, a position maintained by structural supply economics: soybean crushing infrastructure is globally established, extraction yields are well-characterized, and multi-decade supplier ecosystems provide competitive pricing for food-grade applications. The economic logic of soy dominance is grounded in scale: the volume throughput of soybean crushing operations generates lecithin as a co-product with low marginal extraction cost, enabling food-grade soy phospholipids to undercut alternative source-derived equivalents on price. However, soy's dominance is structurally eroding in premium channels due to GMO labeling obligations and allergen disclosure requirements, creating a ceiling on soy's addressable market share in clean-label, premium-positioned applications.

Sunflower-derived phospholipids represent the fastest growing source at an 8.4% CAGR 110 basis points above overall market growth, reflecting the structural value premium commanded by non-GMO, allergen-free positioning. The demand economics are distinct from soy: sunflower phospholipid volumes are smaller, extraction is not a co-product of large-scale crushing in the same manner, and per-unit costs are therefore higher. However, the premium pricing achieved in non-GMO and allergen-free channels more than offsets the input cost differential, yielding a superior gross margin per kilogram. Investment capital is actively flowing into European sunflower crushing capacity expansion, with origination concentrated in Eastern Europe, improving the supply economics of sunflower phospholipids over the forecast period.

End-user Insights

Nutraceutical supplements command above 38% of 2026 revenues, the largest single end-use segment reflecting both the high phospholipid loading rates per finished product unit and the premium ingredient pricing environment of the branded supplement channel. The demand economics within this segment are characterized by high ingredient value-add: a kilogram of pharmaceutical-grade PS or PC in a branded cognitive supplement generates disproportionate downstream revenue relative to its food-grade equivalent in a commodity emulsifier application. The nutraceutical segment also provides the most direct commercialization pathway for clinical evidence investment: operators with clinical validation programs for their phospholipid ingredients can convert research expenditure into branded pricing premiums through health claim authorization.

Food and Beverages is the fastest growing end-use segment at an 8.0% CAGR, driven by the industrial reformulation imperative toward natural emulsifiers and expanding functional food product development across infant nutrition, sports beverages, and plant-based food categories. The volume opportunity is material: the food processing industry's scale of phospholipid consumption across bakery, confectionery, dairy, infant formula, and emerging plant-based meat alternatives translates into large-volume, contract-structured procurement that provides production volume baseloads for phospholipid manufacturers. Margin dynamics are lower per-unit than nutraceutical applications but are stabilized by long-term supply contracts and volume scale efficiency. The convergence of functional food innovation and regulatory emulsifier substitution mandates creates a compounding demand expansion mechanism.

Regional Insights and Trends

North America Leads Global Phospholipids Market Through Structural, Regulatory and Pharmaceutical Advantages

North America commands above 35% of global phospholipids revenue in 2026, the largest regional share, generating an estimated US$ 1.15 billion or more in annual market value. The region's dominance is structurally sustained by four reinforcing factors: the world's largest branded dietary supplement industry providing high-volume ingredient procurement; a pharmaceutical R&D ecosystem that is a primary commercial driver of pharmaceutical-grade phospholipid demand; the FDA GRAS framework that provides regulatory certainty enabling ingredient commercialization without jurisdictional uncertainty; and a mature cold-chain logistics infrastructure preserving phospholipid integrity through distribution.

The United States accounts for the substantial majority of regional revenue, with Canada contributing a secondary growth market underpinned by Natural Health Product (NHP) regulatory frameworks governing phospholipid-containing supplements. Supply dynamics within the region are characterized by import dependency for refined and specialty-grade phospholipids from European processors, notably German and Swiss manufacturers, supplemented by domestic soy lecithin production from midwestern crushing operations.

Investment flows are concentrated in two areas: pharmaceutical contract manufacturing organizations (CMOs) investing in GMP-compliant phospholipid handling capabilities to serve LNP drug development pipelines, and specialty ingredient distributors building non-GMO and organic-certified inventory positions to serve clean-label supplement brand demand. Competitive structure is moderately concentrated at the premium end, where supplier qualification requirements and GMP compliance create high switching costs and more fragmented in the food-grade commodity lecithin supply. Regulatory sensitivity is high: any reclassification of synthetic emulsifiers in North American food standards would directly accelerate natural phospholipid adoption timelines.

Manufacturing Cost Arbitrage and Demand Scale Define APAC Strategic Priority

Asia Pacific is the market's fastest-growing region at an 8.3% CAGR 100 basis points above the global average driven by China's dominant market scale, India's demand acceleration, Japan's structured functional food regulatory pathway, and ASEAN's expanding middle-class health expenditure. The region functions as both a high-growth consumption market and a competitive production base, particularly for soy-derived lecithin sourced from Chinese and Brazilian soybean processing operations serving intra-regional demand.

China represents the region's largest single-country demand driver, with phospholipid consumption concentrated in liver health supplements, traditional medicine modernization applications, and infant formula fortification. China's National Health Commission regulatory framework governs health ingredient approvals, and while approval timelines can extend to 24-36 months for novel ingredients, the scale of the addressable market justifies the compliance investment for international market entrants. Japan's FOSHU (Foods for Specified Health Uses) regulatory system provides the region's most mature health claim framework, creating a validated commercial pathway for phospholipid-enriched cognitive and cardiovascular health products.

India's phospholipids market is at an earlier growth stage but is expanding at an above-average rate as urbanization, rising disposable incomes, and FSSAI regulatory modernization converge. ASEAN markets (South Korea, Vietnam, Singapore, Indonesia) are demonstrating accelerating supplement adoption. Regional supply-demand dynamics are shifting: while Asia Pacific has historically been import-dependent for specialty phospholipids, domestic processing investment particularly in China and India is progressively reducing import dependency for food-grade applications. Investment strategy for market entrants should differentiate between consumer-facing brand entry (high capital, long regulatory lead time) and B2B ingredient supply partnerships (lower capital, faster revenue generation).

Competitive Landscape

The global phospholipids market exhibits a bifurcated competitive structure: high consolidation at the pharmaceutical-grade tier (where GMP compliance, validated analytical capabilities, and long supplier qualification processes create substantial barriers to entry and confer significant pricing power to a small number of operators) and moderate fragmentation at the food-grade commodity lecithin tier (where margin compression from soybean price volatility creates consolidation pressure). Vertical integration from oilseed crushing through extraction, fractionation, and formulation is the dominant competitive advantage mechanism, enabling cost control across feedstock cycles and supply chain transparency for regulated applications. Pricing power is inversely correlated with commodity exposure.

Key Developments:

- In March 2025, Lipoid GmbH introduced a new range of non-GMO soybean-derived phospholipids, strategically aligning with rising clean-label supplement demand and strengthening its leadership in premium natural phospholipid ingredients.

- In November 2024, Cellectar Biosciences partnered with SpectronRx to manufacture iopofosine I-131, an oncology therapy built on a phospholipid drug conjugate delivery platform. This collaboration enhances global-scale production capabilities and reinforces supply chain resilience for phospholipid-based therapeutics.

- In March 2024, VAV Lipids expanded into Latin America, supplying high-purity lipids and phospholipids to pharmaceutical, nutraceutical, and cosmetic manufacturers across Mexico, Brazil, Argentina, Peru, and Colombia. The EU-GMP-certified company is distributing its full portfolio-including plant-based lecithins (LECIVA), egg lecithins (LIPOVA), synthetic phospholipids, and neutral lipids-through regional networks with integrated technical and marketing support.

- In 2020, VAV Life Sciences inaugurated a cGMP-compliant phospholipid manufacturing facility in Mirjole, Ratnagiri, Maharashtra. The plant was established to address the expanding healthcare applications of lecithins and phospholipids in functional foods, nutritional supplements, advanced pharmaceuticals, and cosmetics. Products manufactured at the facility carry a “Made in India” designation, with nearly 80% of output exported to North America, Europe, Asia, and the Rest of the World, reinforcing India’s role in the global phospholipid supply chain.

Companies Covered in Phospholipids Market

- Lipoid GmbH

- Cargill, Incorporated

- ADM (Archer-Daniels-Midland)

- Lecico GmbH

- Aker BioMarine

- Avanti Polar Lipids (Croda)

- Avril Group (Saipol)

- American Lecithin Company

- NOF Corporation

- Lucas Meyer Cosmetics (IFF)

- Lipoceutical AG

- Sime Darby Unimills

- Doosan Corporation

- Guangzhou Haiankangren

- Other Market Players

Frequently Asked Questions

The Phospholipids market is estimated to be valued at US$ 3.3 Bn in 2026.

The key demand driver for the phospholipids market is the rapid expansion of pharmaceutical and nutraceutical applications, particularly in advanced drug delivery systems and functional health formulations.

In 2026, the North America Pacific region will dominate the market with an exceeding 35% revenue share in the global Phospholipids market.

Phosphatidylcholine leads the global phospholipids market in 2026, accounting for over 45% of total revenue, driven by its extensive utilization in nutraceutical supplements, pharmaceutical formulations, liver health products, and functional food applications across developed markets.

The phospholipids market is led by key players including Lipoid GmbH, Cargill, Incorporated, ADM, Lecico GmbH, Aker BioMarine, Avanti Polar Lipids, and Avril Group, driving innovation and global supply leadership.